ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

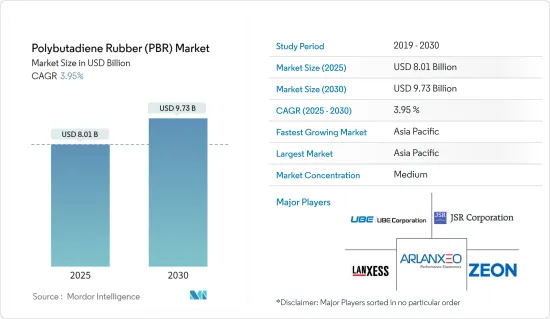

폴리부타디엔 고무(PBR) 시장 규모는 2025년에 80억 1,000만 달러로 추정됩니다. 2030년에는 97억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 3.95%입니다.

COVID-19의 유행은 폴리부타디엔 고무 시장에 부정적인 영향을 미쳤습니다. 전국적인 봉쇄와 엄격한 사회적 격리 조치로 자동차 생산이 중단되고 폴리부타디엔 고무 시장에 영향을 미쳤습니다. 그러나 COVID 유행 후 규제가 해제되면서 시장은 순조롭게 회복되었습니다. 타이어 제조, 신발, 스포츠 액세서리 응용 분야에서 폴리부타디엔 고무 수요가 증가함에 따라 시장이 크게 회복되었습니다.

주요 하이라이트

자동차 산업 수요 증가와 합성 고무 산업의 성장이 폴리부타디엔 고무 시장을 견인할 것으로 예상됩니다.

엄격한 환경 규제와 폴리부타디엔 노출에 대한 건강 우려가 시장 성장을 방해할 것으로 예상됩니다.

미래의 소비자 전기자동차로의 전환은 예측 기간 동안 시장에 기회를 가져올 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상됩니다. 또한 타이어 제조, 신발, 스포츠 액세서리 응용 분야에서 폴리부타디엔 고무 수요 증가로 인해 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

폴리부타디엔 고무 시장 동향

타이어 제조 용도 부문이 시장을 독점

부타디엔은 폴리부타디엔 고무(PBR), 스티렌 부타디엔 고무(SBR), 니트릴 고무(NR), 폴리클로로프렌(네오프렌) 등의 합성 고무 및 엘라스토머의 제조에 사용됩니다.

PBR은 타이어 제조에 사용됩니다. 폴리부타디엔은 주로 자동차용 타이어의 제조에 이용됩니다. 타이어 제조 공정은 세계 폴리부타디엔 생산량의 70% 이상을 소비하는 것으로 추정됩니다. 폴리부타디엔은 주로 타이어의 측벽으로 사용되어 주행 중 지속적인 굴곡으로 인한 피로를 줄입니다. 부타디엔은 다른 다양한 자동차 부품에도 사용됩니다.

미국 등에서는 타이어의 출하량이 증가하고 있어 폴리부타디엔 고무 시장을 견인하고 있습니다. 미국 타이어 공업회(USTMA)에 따르면 타이어의 총 출하량은 2022년 3억 3,200만개, 2019년 3억 3,270만개에 비해 2023년 3억 3,420만개에 이를 전망입니다.

게다가 미국 타이어 공업회(USTMA)에 따르면 2023년 승용차용 타이어, 소형 트럭용 타이어, 트럭용 타이어의 OEM(Original Equipment) 출하 횟수는 각각 2.3%, 1.3%, -0.6% 변화해 합계로 100만개 증가가 전망되고 있습니다. 따라서 자동차 OEM 산업 수요 증가는 현재 조사 시장을 견인합니다.

자동차 생산량 증가는 타이어 제조에 사용되는 폴리부타디엔 고무 시장을 견인하고 있습니다. OICA에 따르면 세계 자동차 생산 대수는 2021년 8,020만대에 비해 2022년에는 8,500만대에 이르며 성장률은 6%입니다. 중국, 미국, 인도는 세계적으로 가장 두드러진 자동차 시장입니다.

최근 전기자동차 수요가 높아지고 있어 소비자의 전기자동차로의 전환이 가까워지고 있기 때문에 예측기간 중에 폴리부타디엔 고무(PBR) 타이어에 비즈니스 기회가 생길 것으로 예상됩니다. 유럽에서는 독일, 영국 등에서 전기자동차 생산량이 증가하고 있습니다.

독일에서는 자동차 제조업체가 전기자동차 생산에 많은 돈을 투자하고 있습니다. 예를 들어, 2023년 6월, 포드는 독일의 하이테크 생산 시설인 쾰른 전기자동차 센터의 낙성을 발표하고 수백만 명의 유럽 고객을 위한 포드의 새로운 세대 전기 승용차를 생산할 예정입니다. 포드에 따르면 쾰른 센터 전기자동차의 연간 생산 능력은 250,000 대입니다. 따라서 전기차 생산량 증가는 현재 연구 시장을 견인할 것으로 예상됩니다.

따라서 예측 기간 동안 타이어 제조 용도 부문이 시장을 독점하게 됩니다.

시장을 독점하는 아시아태평양

예측 기간 동안 아시아태평양은 폴리부타디엔 고무 시장을 독점할 것으로 예상됩니다. 중국, 인도, 일본 등의 국가에서는 타이어 제조, 산업용 고무 제조, 신발 등의 용도로부터 수요가 증가하고 있기 때문에 시장의 비약적인 성장이 전망되고 있습니다.

중국은 생산과 판매의 양면에서 세계 최대의 자동차 시장입니다. 국제자동차건설기구(OICA)에 따르면 중국의 자동차 생산대수는 2022년 2,702만대에 달했으며, 동시기 2021년 대비 3% 증가했습니다.

중국에서는 소비자의 배터리 구동 차량에 대한 지향이 높아지고 있으며, 자동차 산업은 동향의 전환을 목격하고 있습니다. 중국승용차협회에 따르면 2022년 EV와 플러그인 판매량은 567만대로 2021년의 거의 두 배에 달할 전망입니다. 이러한 동향은 이 나라에서 자동차용 타이어 수요를 증가시키고 현재 조사된 시장을 견인합니다.

게다가 중국 고무공업협회(CRIA)에 따르면 이 나라에서는 2025년까지 연간 7억 400만개의 타이어가 생산될 것으로 예측되고 있습니다. 그 내역은 승용차용 레이디얼 타이어가 5억 2,700만개, 트럭·버스용 레이디얼 타이어가 1억 4,800만개, 바이어스 트랙용 타이어가 야가 1,200만개, 항공기 타이어가 5만 4,000개가 되고 있습니다. 따라서 폴리부타디엔 고무에 대한 수요는 이 나라에서 성장할 것으로 예상됩니다.

또한 인도는 아시아태평양에서 가장 큰 고무 생산국·소비국 중 하나입니다. 인도의 고무 산업은 고무 생산 부문과 급성장하는 고무 제품 제조·소비 부문이 공존하고 있습니다.

자동차 타이어 산업회(ATMA)에 따르면 인도의 타이어 산업 수익은 2022년도 90억 달러에 비해 2032년에는 220억 달러에 이를 것으로 예상됩니다. 따라서 타이어 수요 증가는 현재 조사 중인 시장을 견인할 것으로 예상됩니다.

인도에서는 고무의 약 12%가 신발 생산에 사용됩니다. 국제 브랜드의 침투와 도시화가 함께, 이 나라의 신발 시장을 견인하고 있습니다. 정부는 '메이크업 인디아' 구상 하에 신발 산업에 주력하고 있습니다. 현재 세계 연간 신발 생산량의 약 9%를 생산하고 있습니다. 인도의 신발 분야는 중국에 이어 지역 최대입니다.

이러한 요인으로 인해 이 지역의 폴리부타디엔 고무 시장은 예측 기간 동안 성장할 것으로 예상됩니다.

폴리부타디엔 고무 산업 개요

폴리부타디엔 고무 시장은 부분적으로 통합되어 있습니다. 시장의 주요 기업으로는 ENEOS Materials Corporation, Arlanxeo, Zeop Co., Lanxees, UBE Co. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

자동차 산업에서의 수요 증가

합성 고무 산업의 성장

기타 촉진요인

성장 억제요인

엄격한 환경 규제

폴리부타디엔에의 노출에 관한 건강 우려

밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

용도

타이어 제조

신발

스포츠 액세서리

기타 용도(화학, 폴리머 개질 등)

지역

아시아태평양

중국

인도

일본

한국

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

러시아

북유럽 국가

터키

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

카타르

아랍에미리트(UAE)

나이지리아

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

ARLANXEO

Indian Oil Corporation Ltd

ENEOS Materials Corporation

KUMHO PETROCHEMICAL

LANXESS

LG Chem

Reliance Industries Limited

SABIC

SIBUR International GmbH

Synthos

Trinseo

UBE Corporation

THE YOKOHAMA RUBBER CO., LTD

ZEON CORPORATION

KURARAY CO., LTD.

Versalis SpA

제7장 시장 기회와 앞으로의 동향

전기자동차로 전환하는 소비자

기타 기회

KTH

영문 목차

영문목차

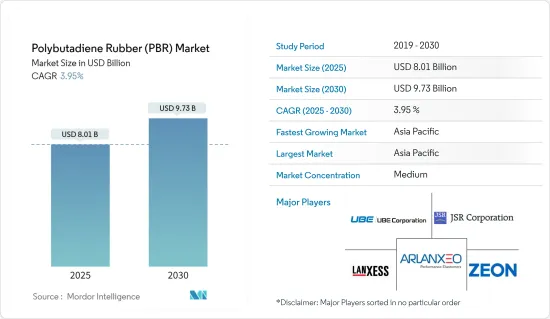

The Polybutadiene Rubber Market size is estimated at USD 8.01 billion in 2025, and is expected to reach USD 9.73 billion by 2030, at a CAGR of 3.95% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively impacted the market for polybutadiene rubber market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in automotive vehicle manufacturing, thereby affecting the market for polybutadiene rubber. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in demand for polybutadiene rubber in tire manufacturing, footwear, and sports accessories applications.

Key Highlights

The increasing demand from the automobile industry and the growth in the synthetic rubber industry are expected to drive the polybutadiene rubber market.

The stringent environmental regulations and the health concerns regarding exposure to polybutadiene are expected to hinder the market's growth.

The upcoming consumer shift to electric vehicles is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for polybutadiene rubber in tire manufacturing, footwear, and sports accessories applications.

Polybutadiene Rubber Market Trends

Tire Manufacturing Application Segment to Dominate The Market

Butadiene is used in the manufacturing of synthetic rubbers and elastomers that include polybutadiene rubber (PBR), styrene-butadiene rubber (SBR), nitrile rubber (NR), and polychloroprene (Neoprene), all of which are used in the production of other goods and materials.

PBR is used in the manufacturing of tires. Polybutadiene is primarily utilized in the production of automotive tires. It is estimated that the tire manufacturing process consumes over 70% of the world's polybutadiene production. It is primarily utilized in tires as a sidewall to reduce fatigue caused by continual flexing throughout the run. Butadiene is also used in a variety of other automotive components.

In countries like the United States, the shipment of tires is increasing, which is driving the market for Polybutadiene rubber. According to the U.S. Tire Manufacturers Association (USTMA), the total shipments of tires are expected to reach 334.2 million units in 2023, as compared to 332.0 million units in 2022 and 332.7 million units in 2019.

Furthermore, according to the U.S. Tire Manufacturers Association (USTMA), in 2023, Original Equipment (OE) shipments for passenger, light truck, and truck tires are expected to change by 2.3%, 1.3% and -0.6%, respectively, with a total increase of 1.0 million units. Thus, the increasing demand for automotive OEM industries will drive the current studied market.

The increasing production volume of automotive vehicles is driving the market for Polybutadiene Rubber used in tire manufacturing. According to OICA, global automotive vehicle production reached 85 million in 2022, as compared to 80.2 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

The rising demand for electric vehicles in recent years, as well as an impending consumer shift to electric vehicles, are expected to provide opportunities for polybutadiene rubber (PBR) tires during the forecast period. In Europe, the production volume of electric vehicles is increasing in countries like Germany and the United Kingdom.

In Germany, automakers are investing heavily in producing electric vehicles in the country. For instance, In June 2023, Ford announced the inauguration of the Cologne Electric Vehicle Center, a hi-tech production facility in Germany that will build Ford's new generation of electric passenger vehicles for millions of European customers. According to Ford, the Cologne Center has an annual production capacity of 250,000 electric vehicles. Thus, the increasing production of electric vehicles is expected to drive the current studied market.

Thus, the tire manufacturing application segment to dominate the market during the forecast period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region is expected to dominate the market for polybutadiene rubber during the forecast period. In countries like China, India, and Japan, the market is expected to grow exponentially owing to the increasing demand from applications such as tire manufacturing, industrial rubber manufacturing, and footwear.

China is the world's biggest automobile market in terms of both production and sales. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), vehicle production in China reached a total of 27.02 million units in 2022, which is an increase of 3% over 2021 for the same period.

In China, the automotive industry is witnessing switching trends as the consumer inclination toward battery-operated vehicles is higher. As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, almost double the sales figures achieved in 2021. These trends will increase the demand for automotive tires in the country, thereby driving the current studied market.

Furthermore, according to the China Rubber Industry Association (CRIA), the country is projected to produce 704 million tires per year by 2025, including 527 million passenger radial tires, 148 million truck/bus radial tires, 29 million bias truck tires, 20,000 extra-large industrial tires, 12 million agricultural tires, and 54,000 aircraft tires. Thus, the demand for polybutadiene rubber is expected to grow in the country.

India is also one of the largest producers and consumers of rubber in the Asia-Pacific region. The Indian rubber industry exhibits the co-existence of the rubber production sector and the fast-growing rubber products manufacturing and consuming sector.

According to the Automotive Tire Manufacturers' Association (ATMA), the Indian tire industry revenue is expected to reach USD 22 billion by FY 2032, as compared to USD 9 billion registered in FY 2022. Thus, the increase in demand for tires is expected to drive the market for the current studied market.

In India, about 12% of rubber is used to produce footwear. The penetration of international brands, coupled with urbanization, has driven the footwear market in the country. The government has focused on the footwear industry under the 'Make in India' initiative. The country is currently producing around 9% of the global annual production of footwear. The footwear sector in India is one of the largest in the region, behind China.

Due to all such factors, the market for polybutadiene rubber in the region is expected to grow during the forecast period.

Polybutadiene Rubber Industry Overview

The polybutadiene rubber market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) ENEOS Materials Corporation, Arlanxeo, Zeop Co., Lanxees, and UBE Co., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand From the Automobile Industry

4.1.2 Growth in the Synthetic Rubber Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Enviornmental Regulations

4.2.2 Health Concerns Regarding Exposure to Polybutadiene

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Application

5.1.1 Tire Manufacturing

5.1.2 Footwear

5.1.3 Sports Accessories

5.1.4 Other Applications (Chemicals, Polymer Modification, etc.)

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Indonesia

5.2.1.6 Malaysia

5.2.1.7 Thailand

5.2.1.8 Vietnam

5.2.1.9 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Spain

5.2.3.6 Russia

5.2.3.7 NORDIC Countries

5.2.3.8 Turkey

5.2.3.9 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Qatar

5.2.5.4 UAE

5.2.5.5 Nigeria

5.2.5.6 Egypt

5.2.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements