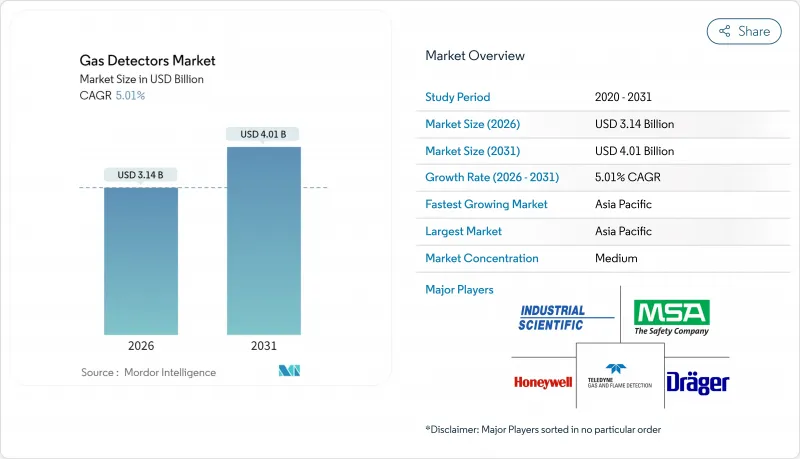

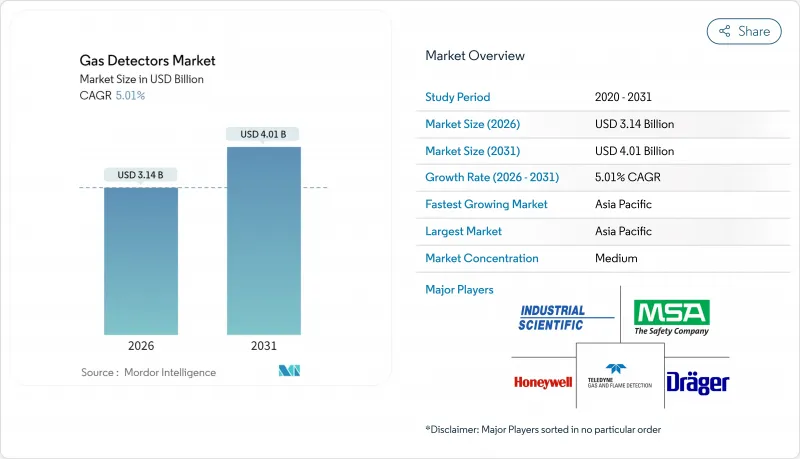

가스 감지기 시장은 2025년에 29억 9,000만 달러로 평가되었고, 2026년 31억 4,000만 달러에서 2031년까지 40억 1,000만 달러에 이를 것으로 전망됩니다.

예측 기간(2026-2031년)의 CAGR은 5.01%를 나타낼 것으로 예상됩니다.

이 성장 궤적은 실시간 근로자 안전 솔루션에 대한 자본 투자 증가, 기존 플랜트의 수리 수요 증가, 예측 분석 엔진에 정보를 제공하는 연결 감지 플랫폼의 통합을 반영합니다. OSHA(미국노동안전보건국), NFPA 72(미국방화협회 표준) 및 지역광업규제의 엄격한 시행이 설비 갱신주기를 촉진하는 한편, 중류 LNG허브, 수소생산자산, 리튬 이온 배터리 라인의 지속적인 확장이 가연성 가스 및 유독가스 모니터링의 기반 수요를 높이고 있습니다. 안전 시스템을 위한 사이버 보안 규제 강화로 인증된 센서 하드웨어와 보안 IoT 소프트웨어 스택을 결합할 수 있는 공급업체에 조달이 진행되고 있습니다. 유선 네트워크가 기존 설비(브라운필드) 설치에서는 여전히 주류이지만, 무선 메쉬 토폴로지와 다년간 대응 배터리 모듈의 진보로 총 설치 비용이 저하되고, 원격 갱구나 일시적인 턴어라운드 존 등 미개척의 틈새 시장이 개척되고 있습니다. 기존 세계공급업체가 낮은 드리프트율, 수소 특이성 또는 구독형 교정 서비스를 약속하는 전문 분야의 신규 진출기업에 대해 점유 방어를 도모하는 가운데 경쟁이 격화되고 있습니다.

규제 당국은 정기적인 점검이 아니라 실시간 환경 텔레메트리를 요구하고 있으며, 광산, 정유소, 화학 콤비나트에 연속 감시 네트워크의 도입을 촉구하고 있습니다. OSHA(미국 노동안전보건국)의 2025년 데이터 구동 검사 프로그램은 운영자에게 기존의 단일 가스 감지기에서 측정을 중앙 집중식 관리 대시보드로 전송하는 네트워크화된 다중 가스 어레이로 업데이트를 촉구합니다. 호주 석탄 관련 법규에서는 갱내 배수로(MDR)의 인증이 의무화되고 있으며, 방폭형 고정 헤드와 지하 메탄을 3차원으로 매핑하는 UAV 탑재 센서의 주문이 급증하고 있습니다. 지방자치단체의 수도사업자는 황화수소에 관한 NFPA 820의 역치에 준거할 필요가 있어, 습식 펌프실의 환기 설비에 수천대 규모의 개수가 행해지고 있습니다. 주요 벤더는 경보 작동 전에 이상 패턴을 감지하는 예측 분석 소프트웨어로 대응해, 인더스트리얼 사이언티픽사의 「2050년까지 직장 사망 사고를 근절한다」라고 하는 제로햄 지령에 따르고 있습니다. 단일 정유소의 연간 컴플라이언스 비용은 100,000달러를 초과할 수 있으며, 이로 인해 갱신 주기와 서비스 계약이 고정화됩니다.

IoT 연결을 통해 가스 감지기 시장은 제품 판매에서 데이터 서비스 에코시스템으로 전환하고 있습니다. Blackline의 EXO 8은 1회 충전으로 100일 동안 클라우드로 데이터를 스트리밍하여 원격지의 안전 팀이 실시간으로 노출 동향을 모니터링할 수 있도록 합니다. Honeywell의 Sensepoint XCL은 Bluetooth Low Energy로 스마트폰과 연계하여 기술자를 단계적으로 이끌고 교정 기간을 최대 30% 단축합니다. 예측 대시보드는 센서 교체를 자동으로 예약하여 숙련된 노동자 부족을 완화하고 예기치 않은 다운타임을 줄입니다. Industry Scientific의 iNet Exchange와 같은 구독 번들은 하드웨어, 소모품 및 분석 기능을 여러 해 계약으로 통합하여 자본 지출에서 운영 지출로 조달을 마이그레이션합니다. 자동화된 컴플라이언스 기록은 감사 준비를 몇 주에서 몇 시간으로 단축하고 다른 지역 규정을 다루는 다국적 기업에게 매력적인 이점을 제공합니다.

산업용 멀티 가스 휴대형 감지기의 단가는 500-1,500달러입니다만, 설치 기기·시운전·유저 트레이닝을 포함하면 배증합니다. AimSafety PM400은 558.57달러, Gas Clip의 유지관리 프리형 MGC Simple은 697.07달러로 교정 불필요한 제품만큼 가격 프리미엄이 현저합니다. 저비용의 아시아 클론 제품은 확립된 브랜드를 최대 50% 미만의 가격으로 판매하고 있으며, 예산 제약이 있는 플랜트에서는 이익률을 압박하고 갱신 계획을 지연시키고 있습니다. 고정 시스템 설치 비용은 인증 배관, 제어반 및 기능 테스트를 포함하여 중간 규모 정유소 섹션에서 100만 달러를 초과할 수 있습니다. 규제 집행이 여전히 일관되지 않는 지역에서는 가격 민감도가 높아지고 일부 사업자는 업그레이드를 미루는 상황이 발생하고 있습니다.

유선 부문은 2025년 수익의 50.35%를 차지했습니다. 기존의 정유소, LNG 플랜트, 화학 공업 단지에서는 위험 구역 기준을 충족하는 검증된 유선 루프를 채용하고 있기 때문입니다. 이러한 레거시 환경에서는 방폭형 접속 박스나 전자 간섭을 견디는 장갑 케이블 배선이 가스 감지기 시장에서 계속 선호되고 있습니다. 그러나 무선 솔루션은 2031년까지 연평균 복합 성장률(CAGR) 7.05%로 확대될 것으로 전망되고 있습니다. 이는 드릴링 비용과 일시적인 운영 중단 스케줄이 신속한 도입을 필요로 하는 프로젝트에 의해 지원됩니다. 초기 세대의 무선 시스템은 배터리 수명의 제한에 시달리고 있었지만, 2세대의 메쉬 설계에서는 단일 충전으로 최대 100일간의 가동을 실현해, 복수의 게이트웨이를 경유해 데이터를 중계하는 것으로 플랜트의 감시 제어 네트워크에 도달하는 것이 가능해지고 있습니다. 신규 건설의 수소 허브와 배터리 플랜트에서는 무선 노드가 유선 연결 안전 구역 게이트웨이에 데이터를 공급하는 하이브리드 아키텍처의 예산 배분이 증가하여 유연성과 확정적인 가동 시간을 양립하고 있습니다. 규제 당국은 적절한 중복성을 갖춘 무선 생명 안전 루프의 인가를 개시하고 있으며, 이 정책의 진화에 의해 유럽 연합이나 미국의 일부 지역 등에 있어서 종래의 도입 장벽이 없어지고 있습니다. 이에 따라 장비 제조업체는 연구 개발을 펌웨어 기반 사이버 보안, OT 네트워크 세분화, 미국 국립 표준 기술 연구소(NIST) 가이드라인을 준수하는 무선 센서 교정 루틴에 주력하고 있습니다. 이 전환은 솔루션 전체의 평균 판매 가격(ASP)을 높이고 공급업체가 네트워크 상태를 원격으로 모니터링하는 구독 수익을 도입합니다. 이로 인해 향후 5년 동안 유선 노드의 절대 센서 수가 우세함에도 불구하고 가스 감지기 시장의 가치 풀이 확대됩니다.

무선 기술의 보급은 분산된 현장 장비를 공통 자산 성능 대시보드로 통합하려는 디지털 변환 예산에서도 혜택을 누리고 있습니다. 조달팀이 총소유비용을 산정할 때 도관·케이블 트레이·화기 작업 허가증의 불필요화가 무선 분석 장치의 프리미엄 정가를 상쇄하는 경우가 많습니다. 가동성 향상은 턴어라운드 작업 중에 안전 커버 범위를 확대합니다. 이 기간에는 가설 배관의 변경에 의해 매일 새로운 누설 경로가 생기기 때문입니다. 2024년 턴어라운드 시즌에 무선팩을 시험 도입한 하류 석유화학 기업에서는 폐소 작업 위반이 15% 감소, 유지보수 기간이 8% 단축되었다는 보고가 전해지고 있습니다. 이러한 운용상의 성과는 투자회수 모델을 강화하여 경영진의 지지를 확고히 하고, 가스 감지기 시장 전체에서 무선기술의 점유율 확대를 더욱 가속화하고 있습니다.

아시아태평양은 2025년 세계 수익의 48.60%를 차지했으며 중국의 석탄화학 복합시설 급증, 인도 신규 정유소 건설, 동남아시아 배터리 공급망 투자 확대를 배경으로 6.92%라는 가장 빠른 CAGR을 유지할 것으로 예측됩니다. 중국 국가 긴급 관리부의 빈번한 안전 감사로 시설 운영자는 인증되지 않은 저비용 수입품에서 ATEX 및 IECEx 준수 장비로 전환을 촉구하고 있습니다. 한국과 일본은 수소 충전 네트워크를 가속화하고 있으며, 소방법규에서 의무화된 이중 중복 수소 센서를 각 펌프에 내장하고 있습니다. 인도의 'Jal Jeevan Mission'은 수천의 수처리 시설에서 염소·오존 감시 시스템의 갱신을 촉구해 수요를 더욱 확대하고 있습니다. 국내 전자기기 제조업체는 질화갈륨 파워스위치의 제조를 확대하고 있으며, 특수한 암모니아 및 염화수소 검출장치에 새로운 기회가 탄생하고 있습니다.

북미는 수익 점유율로 2위를 차지하고 있으며, OSHA(미국 노동안전위생국)의 규제 강화, 셰일가스 처리, 멕시코 걸프의 액화천연가스 수출터미널이 견인하고 있습니다. 뉴욕시의 지 방법 157호에 의해 2025년 5월까지 주택용 천연 가스 감지기의 설치가 의무화되어 가스 감지기 시장의 주택·소규모 상업 분야에 수백만대 규모 수요가 창출되었습니다. 미국에서는 인프라 투자 고용법에 근거한 수소 허브 사업에서 암호화 무선 백본을 갖춘 멀티 가스 고정 네트워크가 규정되어 수소 전용 센서의 수주를 촉진하고 있습니다. 캐나다의 오일 샌드 사업에서는 -40℃에서도 정밀도를 유지하는 히터나 분석 장치가 지정되어 극한 대응 기기 라인을 가지는 벤더가 우위입니다. 멕시코의 몬테레이 및 바히오 주변 산업 회랑에서는 자동차 도장 공장에 VOC 감지기를 통합하여 OEM의 지속가능성 감사에 대응하고 있습니다.

유럽에서는 ATEX(방폭 지령)의 엄격한 준수, EPBD(에너지 성능 지령)에 근거한 실내 공기질 규제, 탈탄소화 목표가 함께 지속적인 기기 갱신이 유지되고 있습니다. 독일 라인 강을 따라 대규모 화학 산업 지역에서 벤젠과 부타디엔 모니터링에 투자하여 누출 배출량을 줄이기 위해 노력하고 있습니다. 한편 영국에서는 상업 사무실에서 CO2 모니터링을 의무화하여 이용자의 건강 증진을 추진하고 있습니다. 홋카이오 해안 플랫폼에서는 100ppm을 넘는 황화수소 농도에 대응하는 인증이 끝난 감지 헤드가 요구되고 있어 플랫폼 상부 구조를 200미터에 걸쳐 커버하는 개방형 적외선 유닛도 아울러 도입되고 있습니다. 동유럽 회원국은 EU 결속 기금을 활용하여 지역 난방 플랜트의 근대화를 진행하고 있으며, 열전 병급 모듈에 일산화탄소 및 메탄 센서를 통합하고 있습니다. 지중해 지역의 LNG 수입터미널에서는 운용을 중단하지 않고 기존 부두를 개수하기 위해 무선식 화염 감지·가스 감지 패키지를 채용하고 있습니다.

중동 및 아프리카는 수익 점유율이야말로 작은 것, 그린 수소 파일럿 플랜트, 액화 플랜트, 광업 확장 회랑에서 견조한 도입이 진행되고 있습니다. GCC 지역의 정제소는 유로 VI 황 규제에 대응하기 위해 수소화 분해 장치를 개수하고, 그 과정에서 촉매 비드식 LEL 감지 헤드를 업그레이드하고 있습니다. 남아프리카의 금광산에서는 광물자원성에 의한 감독 강화에 의해 심부갱도에서의 연속고정 감시가 의무화되고 있습니다. 라틴아메리카에서는 브라질의 프레솔트 앞바다 유전이 고농도의 황화수소에 대응한 고사양 감지기를 필요로 하는 한편, 칠레의 리튬 염수 처리 시설에서는 환경법령 준수를 위해 염화수소 분석 장치를 도입하고 있습니다. 이러한 지역적인 동향이 함께, 예측 기간을 통해 가스 감지기 시장은 다층적인 균형 성장을 유지할 전망입니다.

The gas detectors market was valued at USD 2.99 billion in 2025 and estimated to grow from USD 3.14 billion in 2026 to reach USD 4.01 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031).

The trajectory reflects rising capital investment in real-time worker-safety solutions, growing retrofit demand across legacy plants, and the integration of connected detection platforms that feed predictive analytics engines. Strict enforcement of OSHA, NFPA 72, and regional mining codes is stimulating equipment replacement cycles, while sustained buildouts of midstream LNG hubs, hydrogen production assets, and lithium-ion battery lines elevate baseline demand for combustible and toxic-gas monitoring. Intensifying cybersecurity rules for safety systems is steering procurement toward vendors that can combine certified sensor hardware with secured IoT software stacks. Although wired networks still dominate brownfield installations, advances in wireless mesh topologies and multiyear battery modules are lowering total installed cost and unlocking untapped niches such as remote wellheads and temporary turnaround zones. Competitive activity is accelerating as incumbent global suppliers defend share against specialist entrants promising lower drift rates, hydrogen specificity, or subscription-based calibration services.

Regulators now require live environmental telemetry rather than periodic spot checks, compelling mines, refineries, and chemical complexes to deploy continuous monitoring networks. OSHA's 2025 program of data-driven inspections is motivating operators to replace legacy single-gas units with networked multigas arrays that transmit readings into centralized dashboards. Australian coal legislation mandates mine-drained-roadway (MDR) certification, prompting orders for explosion-proof fixed heads and UAV-mounted sensors that map underground methane in three dimensions. Municipal water utilities must comply with NFPA 820 thresholds for hydrogen sulfide, leading to multi-thousand-unit retrofits of wet-well ventilated spaces. Leading vendors respond with predictive analytics software that flags abnormal patterns before alarms trigger, aligning with zero-harm directives such as Industrial Scientific's vision to eliminate workplace fatalities by 2050. Annual compliance spending can top USD 100,000 for a single refinery, locking in replacement cycles and service contracts.

IoT connectivity converts the gas detectors market from product sales to data-service ecosystems. Blackline's EXO 8 streams to the cloud for 100 days on a single charge, allowing remote safety teams to watch exposure trends in real time. Honeywell's Sensepoint XCL pairs with smartphones through Bluetooth Low Energy, guiding technicians step-by-step and shortening calibration windows by up to 30%. Predictive dashboards schedule sensor replacement automatically, mitigating skilled-labor shortages and cutting unplanned downtime. Subscription bundles such as Industrial Scientific's iNet Exchange shift procurement from capex to opex, bundling hardware, consumables, and analytics in multi-year contracts. Automated compliance logs shave audit preparation from weeks to hours, an attractive benefit for multinationals juggling disparate regional regulations.

Industrial-grade multigas portables range from USD 500 to USD 1,500 per unit, figures that double once installation hardware, commissioning, and user training are included. The AimSafety PM400 lists at USD 558.57 while Gas Clip's maintenance-free MGC Simple commands USD 697.07, highlighting price premiums linked to no-calibration claims. Low-cost Asian clones undercut established brands by up to 50%, compressing margins and delaying replacement programs in budget-constrained plants. Fixed-system installs often exceed USD 1 million for a mid-size refinery section once certified conduit, control cabinets, and functional testing are included. Price sensitivity is amplified in regions where enforcement remains inconsistent, enabling some operators to defer upgrades.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The wired segment held 50.35% of 2025 revenue as established refineries, LNG trains, and chemical parks rely on proven hardwired loops that meet hazardous-area standards. In these legacy environments, the gas detectors market continues to favor flameproof junction boxes and armored cable runs that withstand electromagnetic interference. However, wireless solutions are on a 7.05% CAGR through 2031, buoyed by projects where trenching costs or temporary turnaround schedules favor rapid deployment. Early-generation radio systems suffered from limited battery life, yet second-generation mesh designs now deliver up to 100 days of uptime on a single charge and can hop data through multiple gateways to reach a plant's supervisory control network. New-build hydrogen hubs and battery plants increasingly budget for hybrid architectures in which wireless nodes feed hardwired safe-area gateways, blending flexibility with deterministic uptime. Regulators are beginning to clear suitably redundant wireless life-safety loops, a policy evolution that removes a historic adoption barrier in jurisdictions such as the European Union and parts of the United States. Equipment manufacturers thus channel research and development into firmware-based cybersecurity, OT network segmentation, and over-the-air sensor calibration routines that align with National Institute of Standards and Technology guidelines. The shift lifts overall solution ASPs and introduces subscription revenue as vendors monitor network health remotely, thus enlarging the gas detectors market value pool even though absolute sensor counts continue to favor wired nodes for the next five years.

Wireless uptake also benefits from digital transformation budgets that seek to unify disparate field instruments under common asset-performance dashboards. When procurement teams tally the total cost of ownership, the elimination of conduit, cable trays, and hot-work permits often offsets the premium list price of wireless analyzers. Added mobility widens safety coverage during turnaround events, where temporary pipework changes create fresh leak paths each day. Downstream petrochemical players that trialed wireless packs during 2024 turnaround seasons report 15% fewer confined-space entry violations and 8% shorter maintenance windows. These operational wins reinforce payback models and solidify management buy-in, further accelerating wireless share gains within the broader gas detectors market.

The Gas Detectors Market Report is Segmented by Communication Type (Wired, and Wireless), Detector Type (Fixed - Electrochemical, Semiconductor, and More), End-User Industry (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Metal and Mining, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 48.60% of global revenue in 2025 and is forecast to maintain the fastest 6.92% CAGR, anchored by China's surge in coal-to-chemicals complexes, India's new-build refineries, and Southeast Asia's battery-supply-chain investment wave. Frequent safety audits under China's Ministry of Emergency Management are compelling facility operators to replace uncertified low-cost imports with ATEX and IECEx-compliant equipment. South Korea and Japan accelerate hydrogen refueling networks, each pump incorporating dual redundant hydrogen sensors as mandated by fire codes. India's Jal Jeevan Mission triggers upgrades in chlorine and ozone monitoring across thousands of water plants, further widening demand. Domestic electronics firms ramp gallium-nitride power-switch fabrication, creating fresh opportunities for specialty ammonia and hydrogen chloride detection.

North America ranks second by revenue share, driven by OSHA enforcement, shale gas processing, and liquid-natural-gas export terminals along the Gulf Coast. New York City's Local Law 157 requires residential natural-gas detectors by May 2025, injecting multi-million-unit volume into the residential and light-commercial slice of the gas detectors market. U.S. hydrogen hubs funded under the Infrastructure Investment and Jobs Act prescribe multigas fixed networks with encrypted wireless backbones, stimulating orders for hydrogen-specific sensors. Canada's oil sands operations specify heaters and analyzers that remain accurate at -40 °C, favoring vendors with arctic-rated equipment lines. Mexico's industrial corridors around Monterrey and Bajio integrate VOC detectors in auto-paint shops to meet OEM sustainability audits.

Europe maintains strict ATEX compliance, EPBD indoor-air-quality mandates, and decarbonization targets that collectively sustain steady upgrades. Germany's large chemical basin along the Rhine invests in benzene and butadiene monitoring to cut fugitive emissions, while the United Kingdom enforces CO2 monitoring in commercial offices to improve occupant well-being. Offshore North Sea platforms demand detector heads certified for hydrogen sulfide concentrations exceeding 100 ppm, alongside open-path infrared units that span 200 metres across platform topsides. Eastern European member states leverage EU cohesion funds to modernize district-heating plants, integrating carbon-monoxide and methane sensors into combined-heat-and-power modules. Mediterranean LNG import terminals adopt wireless flame and gas packages to retrofit legacy jetties without disrupting operations.

The Middle East and Africa region captures a smaller revenue share but sees robust adoption in green-hydrogen pilot plants, liquefaction trains, and mining expansion corridors. GCC refiners retrofit hydrocracker units to meet Euro VI sulfur limits, upgrading catalytic bead LEL heads in the process. South African gold mines face stricter Department of Mineral Resources oversight that mandates continuous fixed monitoring in deep-level shafts. In Latin America, Brazil's pre-salt offshore fields require high-specification detectors rated for high hydrogen-sulfide concentrations, while Chile's lithium brine processors install hydrogen-chloride analyzers to comply with environmental statutes. Collectively, these regional dynamics sustain balanced multilayer growth in the gas detectors market across the forecast horizon.