ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

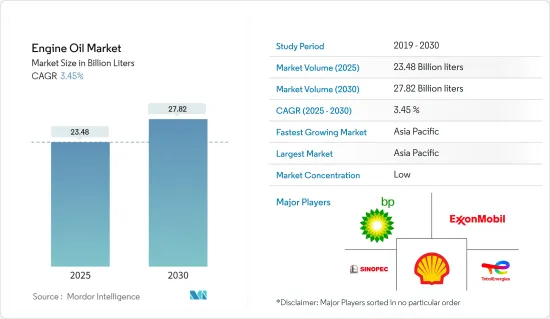

엔진오일 시장 규모는 2025년에 234억 8,000만 리터로 추정되고, 2030년에는 278억 2,000만 리터에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 3.45%로 전망됩니다.

COVID-19 위기는 세계 자동차 산업에 영향을 주었고 대부분 지역에서 자동차 생산과 판매가 갑자기 멈췄습니다. 이러한 작업 정지로 인해 전 세계적으로 수백만 대의 자동차 생산이 손실되었습니다. 엔진오일은 전체 엔진의 효율을 향상시키고 배출 가스를 줄이는 데 사용되기 때문에 자동차 산업은 엔진오일 시장에 직접적인 영향을 미칩니다. 그러나 2021년 후반에 규제가 해제된 후 자동차 산업 활동이 활발해지면서 시장 성장이 꾸준히 회복되어 시장 회복으로 이어졌습니다.

주요 하이라이트

중기적으로는 자동차의 생산 및 판매 대수 증가와 고성능 윤활유의 채용 확대가 시장의 성장을 견인하는 중요한 요인입니다.

그러나 드레인 간격의 연장과 전기자동차(EV)의 작은 영향은 예측기간 동안 대상산업의 성장을 억제할 것으로 예상되는 주요 요인입니다.

중동 및 아프리카에서 자동차 산업의 성장과 북미와 아시아태평양의 수많은 향후 건설 프로젝트는 곧 세계 시장에 유리한 성장 기회를 가져올 것으로 예상됩니다.

아시아태평양이 시장을 독점하고 예측 기간 동안 가장 높은 CAGR로 추이할 가능성이 높습니다.

엔진오일 시장 동향

자동차 산업에서 수요 증가

엔진오일은 내연 엔진의 윤활에 널리 사용됩니다. 엔진오일은 75-90%의 기유와 10-25%의 첨가제로 구성되어 있으며 세계 자동차 및 기타 운송 부문에서 주로 사용됩니다.

엔진오일을 사용하는 주요 이점은 마모 및 손상 감소, 부식 방지, 엔진의 부드러운 작동입니다. 엔진오일은 움직이는 부품 사이에 얇은 멤브레인을 만들어 열 전달을 촉진하고 부품이 접촉 할 때의 긴장을 완화합니다.

소형차 생산 및 판매 증가는 엔진오일의 소비에 직접적인 영향을 미칠 것으로 추정됩니다. 그 결과 예측 기간 동안 엔진오일 수요가 증가할 것으로 예상됩니다.

국제자동차공업회(OICA)에 따르면 2022년 세계 자동차 생산량은 8,501만 6,728대에 달하고, 전년 대비 5.9% 증가했습니다. 2021년과 2022년 자동차 생산 대수의 전년 대비 성장률은 6%였습니다.

마찬가지로 OICA에 따르면 2022년 상용차 생산량은 5,749만 대에 달했으며 2021년 5,644만 대에 비해 성장세를 기록했습니다.

한편 미국 상무부 경제분석국에 따르면 2022년 소형차 소매판매 대수는 1,375만 4,300대로 2021년 1,494만 6,900대에 비해 최저가 됐습니다.

또한 독일 자동차 공업회(Verband der Automobilindustrie)에 따르면 독일의 자동차 생산 대수는 2022년 340만 대에 달하였고, 2021년 310만 대에 비해 9.6%의 성장을 기록했습니다.

그 결과, 상기 요인은 향후 엔진오일 시장에 큰 유익한 영향을 미칠 것으로 예상됩니다.

시장을 독점하는 아시아태평양

아시아태평양은 주로 자동차 생산과 발전 산업의 거대한 수요 증가로 인해 엔진오일 시장을 독점하고 있습니다.

중국은 세계 최고의 자동차 제조업체입니다. 이 나라의 자동차산업은 연비 향상과 배출가스 감축을 목표로 하는 자동차 생산에 중점을 두고 제품의 진보를 도모하고 있습니다.

중국 기차공업협회(CAAM)에 따르면 2022년에는 중국에서 승용차가 약 2,356만대, 상용차가 약 330만대 판매되었습니다.

마찬가지로 India Brand Equity Foundation에 따르면 2022 회계 연도에는 인도의 발전 능력이 약 400GW로 증가합니다. 이로 인해 이전부터 발전 능력의 성장이 계속되고 있습니다. 1992-2022년 사이 인도의 발전 능력은 5배로 증가했습니다.

내각부의 발표에 따르면, 2022년 국내 제조업체로부터의 중전 수주액은 약 2조 2,500억 엔(약 152억 2,000만 달러)으로, 전년의 약 2조 1,500억 엔(약 145억 5,000만 달러)으로부터 증가합니다.

그 결과 위의 요인은 향후 몇 년동안 이 지역의 엔진오일 시장에 큰 영향을 미칠 것으로 예상됩니다.

엔진오일 산업 개요

엔진오일 시장은 세분화되어 있습니다. 주요 진출기업은 Total Energies, Exxon Mobile Corporation, BP plc, Shell PLC, China Petrochemical Corporation 등입니다(순부동).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

자동차 생산 및 판매 증가

고성능 윤활유의 채용 증가

억제요인

드레인 간격의 연장

미래 전기자동차(EV)의 완만한 영향

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

규제 시책 분석

제5장 시장 세분화(시장 규모-수량 기준)

최종 사용자 산업별

발전

자동차 및 기타 운송 장비

중장비

야금 및 금속가공

화학제조

기타

지역별

아시아태평양

중국

인도

일본

한국

필리핀

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

북미

미국

멕시코

캐나다

기타 북미

유럽

독일

영국

프랑스

이탈리아

러시아

스페인

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

카타르

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

AMSOIL INC

Bharat Petroleum Corporation Limited

BP plc

Chevron Corporation

China Petrochemical Corporation

Eni SPA

Exxon Mobil Corporation

FUCHS

Gazpromneft-Lubricants, Ltd

Gulf Oil International

Hindustan Petroleum Corporation Limited

Idemitsu Kosan Co.,Ltd

Illinois Tool Works Inc.

Indian Oil Corporation Ltd

JX Nippon Oil & Gas Exploration Corporation

LUKOIL

Motul

Petrobras

PETRONAS Lubricants International

Phillips 66 Company

PT Pertamina Lubricants

Repsol

Shell PLC

SK Enmove CO., Ltd

Tide Water Oil Co.(India) Ltd

TotalEnergies

Valvoline Cummins Pvt. Ltd.

제7장 시장 기회 및 향후 동향

중동 및 아프리카에서의 자동차 산업의 성장

북미와 아시아태평양의 수많은 건설 프로젝트

AJY

영문 목차

영문목차

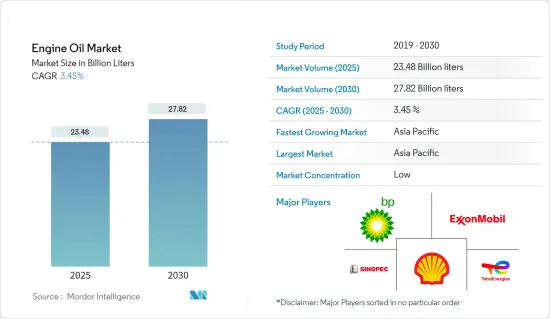

The Engine Oil Market size is estimated at 23.48 billion liters in 2025, and is expected to reach 27.82 billion liters by 2030, at a CAGR of 3.45% during the forecast period (2025-2030).

The COVID-19 crisis impacted the global automotive industry, as both the production and sales of motor vehicles came to a sudden halt in most regions. These work stoppages led to a loss in the production of millions of vehicles across the world. The automobile industry has a direct effect on the engine oil market as it is used to improve the overall efficiency of an engine and reduce emissions. However, the market growth picked up steadily, owing to increased automotive activities after the lifting of restrictions in the second half of 2021, leading to market recovery.

Key Highlights

Over the medium term, the increasing automotive production and sales and the increasing adoption of high-performance lubricants are significant factors driving the growth of the market studied.

However, extended drain intervals and the modest impact of electric vehicles (EVs) are key factors anticipated to restrain the growth of the target industry over the forecast period.

Nevertheless, the growing automotive industry in the Middle East and Africa and numerous upcoming construction projects in North America and APAC are likely to create lucrative growth opportunities for the global market soon.

Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Engine Oil Market Trends

Increasing Demand from Automotive Industry

Engine oils are widely used to lubricate internal combustion engines. They are composed of 75-90% base oils and 10-25% additives and are mostly used in automotive and other transport segments across the world.

The major advantages of using engine oils are wear and tear reduction, corrosion protection, and the engine's smooth operation. They function by creating a thin film between the moving parts for enhancing heat transfer and reducing tension during the contact of parts.

The increasing production and sales of light-duty vehicles are estimated with a direct impact on engine oil consumption. It, in turn, is anticipated to drive the demand for engine oil during the forecast period.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production reached 85,016,728 units in 2022, and the production increased by 5.9% when compared to the previous year's data. Motor vehicle production growth year-on-year between the 2021 and 2022 markets was at 6%.

Similarly, as per OICA, commercial vehicle production reached 57.49 million units in 2022 and registered growth when compared to 56.44 in 2021.

Meanwhile, as per the Bureau of Economic Analysis of the United States Department of Commerce, light vehicle retail sales reached 13,754.3 thousand units, registering the lowest production when compared to 14,946.9 thousand units in 2021.

Further, according to the German Association of the Automotive Industry (Verband der Automobilindustrie), automobile production in Germany reached 3.4 million in 2022 and registered a growth of 9.6% when compared to 3.1 million in 2021.

As a result, the factors above are anticipated with a substantial beneficial influence on the engine oil market in the future years.

The Asia-Pacific Region to Dominate the Market

Asia-Pacific dominated the engine oil market primarily due to the huge growing demand for automotive production and power generation industries.

China holds the title of the world's leading automobile manufacturer. The nation's automotive industry is poised for product advancement, emphasizing the production of vehicles aimed at enhancing fuel efficiency and reducing emissions, addressing escalating environmental concerns attributed to increasing pollution levels in the country

According to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.56 million passenger cars and 3.3 million commercial vehicles were sold in China.

Similarly, according to the India Brand Equity Foundation, in the financial year 2022, India's power generation capacity rose to nearly 400 GW. Thereby, the growth in generation capacity from the previous years continues. Between 1992 and 2022, the country's electricity capacity experienced a five-fold increase.

As per Cabinet Office Japan, in 2022, the order value for heavy electrical machinery from manufacturers in Japan amounted to approximately JPY 2.25 trillion (~USD 15.22 billion), increasing from around JPY 2.15 trillion (~USD 14.55 billion) in the previous year.

As a result, the factors above are projected to have a substantial influence on the engine oil market in the region in the coming years.

Engine Oil Industry Overview

The engine oil market is fragmented in nature. The major players include (not in particular order) Total Energies, Exxon Mobile Corporation, BP p.l.c., Shell PLC, and China Petrochemical Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Automotive Production and Sales

4.1.2 Increasing Adoption of High-performance Lubricants

4.2 Restraints

4.2.1 Extended Drain Intervals

4.2.2 Modest Impact of Electric Vehicles (EVs) in the Future

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 End-user Industry

5.1.1 Power Generation

5.1.2 Automotive and Other Transportation

5.1.3 Heavy Equipment

5.1.4 Metallurgy and Metalworking

5.1.5 Chemical Manufacturing

5.1.6 Other End-user Industries

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Philippines

5.2.1.6 Indonesia

5.2.1.7 Malaysia

5.2.1.8 Thailand

5.2.1.9 Vietnam

5.2.1.10 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Mexico

5.2.2.3 Canada

5.2.2.4 Rest of North America

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United kingdom

5.2.3.3 France

5.2.3.4 Italy

5.2.3.5 Russia

5.2.3.6 Spain

5.2.3.7 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Qatar

5.2.5.4 United Arab Emirates

5.2.5.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 AMSOIL INC

6.4.2 Bharat Petroleum Corporation Limited

6.4.3 BP p.l.c

6.4.4 Chevron Corporation

6.4.5 China Petrochemical Corporation

6.4.6 Eni SPA

6.4.7 Exxon Mobil Corporation

6.4.8 FUCHS

6.4.9 Gazpromneft - Lubricants, Ltd

6.4.10 Gulf Oil International

6.4.11 Hindustan Petroleum Corporation Limited

6.4.12 Idemitsu Kosan Co.,Ltd

6.4.13 Illinois Tool Works Inc.

6.4.14 Indian Oil Corporation Ltd

6.4.15 JX Nippon Oil & Gas Exploration Corporation

6.4.16 LUKOIL

6.4.17 Motul

6.4.18 Petrobras

6.4.19 PETRONAS Lubricants International

6.4.20 Phillips 66 Company

6.4.21 PT Pertamina Lubricants

6.4.22 Repsol

6.4.23 Shell PLC

6.4.24 SK Enmove CO., Ltd

6.4.25 Tide Water Oil Co. (India) Ltd

6.4.26 TotalEnergies

6.4.27 Valvoline Cummins Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Automotive Industry in Middle East and Africa

7.2 Numerous Upcoming Construction Projects In North America and APAC