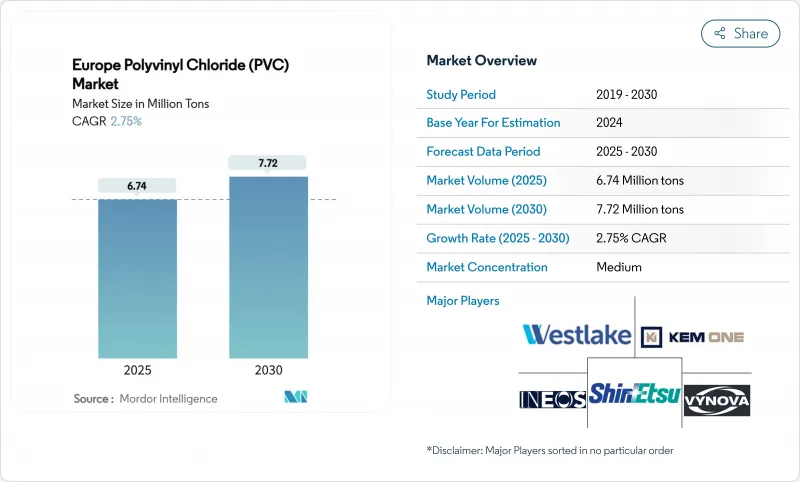

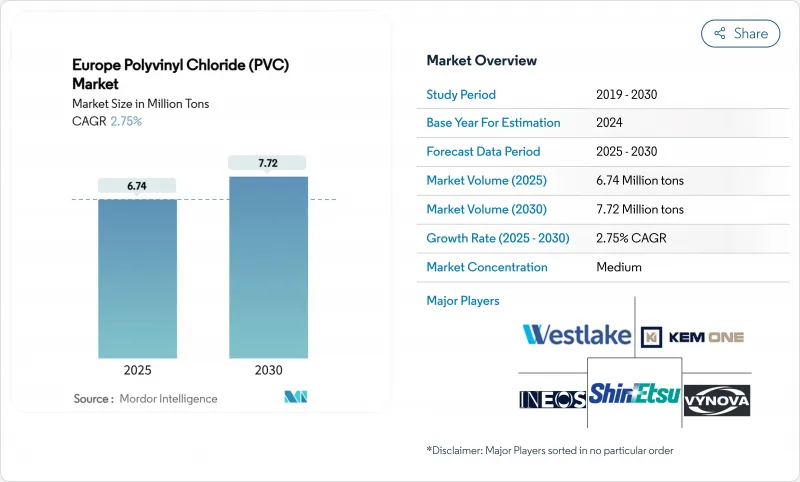

유럽의 폴리염화비닐(PVC) 시장 규모는 2025년에 674만 톤으로 추정되고 예측 기간(2025-2030년)의 CAGR은 2.75%로, 2030년에는 772만 톤에 이를 것으로 예상됩니다.

파이프, 프로파일 및 피팅의 견조한 수요는 주택 건설의 완만한 회복과 함께 당분간 수량 증가를 지원합니다. REACH에 의한 규제 압력은 계속해서 칼슘 아연 안정제의 채택을 가속화하지만, 지속적인 인프라 지출은 전환 비용을 완화시킵니다. 에너지 효율적인 개축 프로그램, 전력망의 정비, 물 관리 프로젝트가 구조 수요를 지지하는 한편, 순환형 경제의 의무화에 의해 재활용이나 생물 유래의 PVC에 대한 투자가 급피치로 진행되고 있습니다. 경쟁의 격렬함은 중간 정도에 그치지만, 이것은 종합 제조업체가 규모, 전용 원료, 독자 기술을 활용해 컴플라이언스·코스트를 상쇄하고 있기 때문입니다.

이 지역의 주택 부족과 건물 스톡의 노후화에 의해 개축의 움직임이 활발해지고 있으며, 유럽의 폴리염화비닐(PVC) 시장에서는 창재와 사이딩의 수량이 늘고 있습니다. 열가소성 수지 인서트로 강화된 PVC 프레임의 열 성능은 12-13% 향상되어 EU의 에너지 효율 규제에의 적합성이 높아지기 때문에 경질 PVC는 리노베이션 프로젝트에 더욱 침투하고 있습니다. 가맹국의 부흥기금이 토목공사에의 지출에 충당되어, 농업 인프라에 있어서 PVC의 기능적·비용적 우위성이 보수 배수 시스템으로 실증되고 있습니다. 금리 안정화와 재료 가격 정상화는 북유럽 시장 전체 프로젝트의 실행 가능성을 높이고 있지만, 남유럽에서는 재정적 제약이 계속 성장을 억제하고 있습니다. 전반적인 효과로 PVC 파이프와 프로파일에 대한 수요가 중기적으로 잘 분산되어 증가하고 있습니다.

전기자동차의 보급에 의해 내장 부품의 사양이 변경되어 와이어 하네스나 바닥재에 난연성 연질 PVC를 사용할 기회가 퍼지고 있습니다. 2025년 초에 독일의 자동차 생산 대수는 전년 대비 3% 증가하여 지역의 컴파운드 공장에서 수지 인수를 밀어 올렸습니다. 바이오 첨가 PVC 등급은 인장 성능과 열 성능을 유지하면서 요람에서 게이트까지의 CO2 배출량을 58% 줄여 OEM이 플랫폼을 재설계하지 않고 ESG 목표를 달성할 수 있도록 합니다. 독일, 프랑스, 북이탈리아 주변의 성장 클러스터는 최적화된 물류와 저스트-인-시퀀싱 공급 모델을 촉진하고 있습니다. Tier One 공급업체는 디지털 품질 관리 도구와 소재 혁신을 결합하여 트림 낭비를 없애고 사이클 시간을 단축합니다.

서유럽의 주요 슈퍼마켓 체인은 PVC 트레이와 클린 필름을 단계적으로 폐지하고 있으며, 컨버터 각사는 단소재의 PET나 종이를 베이스로 한 포맷으로의 이행을 강요당하고 있습니다. 최근 예정된 포장 및 포장 폐기물 규정은 PFAS 및 BPA 규정을 추가하여 기존 PVC 제형의 규정 준수 경로를 복잡하게 만듭니다. 의약용 블리스터 팩은 여전히 적용되지 않지만 대량의 신선한 식품 분야가 즉시 대체품으로 전환되기 때문에 유럽 폴리염화비닐(PVC) 시장의 유연한 필름 수요가 감소합니다. 브랜드 소유자의 구매 정책이 업스트림으로 연결되어 컴파운드 공급업체는 대체 수지를 인증하고 틈새 시장에서 배리어성이 중요한 용도를 위한 재활용 가능한 PVC 블렌드를 개발해야 합니다. 동유럽 시장에서는 금지조치의 도입이 늦어져 일시적인 완화가 되고 있는 것, 궁극적으로는 지역 전체의 이행을 시사하고 있습니다.

2024년 유럽의 폴리염화비닐(PVC) 시장 점유율은 파이프, 프로파일 및 피팅이 건축물 및 급수 네트워크에서 우위를 유지하고 있기 때문에 경질 등급이 60.74%를 차지했습니다. 저연 PVC는 베이스는 작은 것, 대량 운송 기관, 터널, 공공시설 건설 프로젝트에 있어서 방화 안전 규제를 배경으로, 2030년까지의 CAGR이 3.89%로 가장 높을 전망입니다. 연질 PVC는 의료용 튜브를 위한 바이오플라스틱화 투명 등급 수요가 식품 포장용 필름의 축소를 보완하고 있습니다. 염소화 PVC는 수입 관세와 물류 비용을 줄이기 위해 현지 생산을 활용하여 산업용 온수 라인에 침투합니다.

성숙한 수요 패턴이 가동률을 80% 전후로 안정시키기 때문에 생산 능력 증강은 규율 정확하게 유지됩니다. 압출기는 그린 필드 확장보다 다이 헤드 업그레이드 및 인라인 측정 시스템에 중점을두고 수율을 높입니다. 컨버터는 화학처리용 사이트글라스의 경질 클리어 오더와 시관계약의 벌크 커미트먼트를 양립시키기 때문에 제품 믹스의 민첩성이 경쟁적인 차별화 요인이 됩니다. 따라서 유럽의 폴리염화비닐(PVC) 시장은 안정적인 대량 경질 수요와 낮은 연기 및 CPVC의 특수 성장 틈새 분야 간의 균형을 유지합니다.

2024년에는 칼슘 아연 용액이 안정제 소비량의 42.88%를 차지했지만, 이는 EU의 납 금지령 후 시장의 축족발을 명확하게 나타내는 것입니다. 이 패키지는 2030년까지 연평균 복합 성장률(CAGR) 3.61%를 나타낼 것으로 예상되며 유럽 폴리염화비닐(PVC) 시장의 첨가제 수준의 가치 성장의 대부분을 견인합니다. 납계 안정제는 현재 일시적인 규제 완화 하에서 주로 재생 경질 재료의 흐름 속에서 살아나고 있지만, 주석계는 내열 전선 피복의 틈새 분야에서 존속하고 있습니다. 바륨 아연계와 액상 혼합 금속계는 특수 시트 캘린더에 공급되고 있지만, 그린 케미스트리의 통일 기준이 하류에 퍼지면서 판매량의 감소에 직면하고 있습니다.

화학제품 공급업체는 주요 압출 허브 근처에 모듈식 배합 시설을 확장하여 저스트-인-타임 납품과 엄격한 배합 관리를 보장합니다. 프로파일 제조업체와의 공동 자격 인증 프로그램은 라인 변경 승인을 가속화하고 변환 일정을 압축합니다. 안정제의 변화는 규제 요청이 공급망을 재구성하고 연구 개발의 깊이와 통합된 물류를 가진 사업자에게 유리한 방법을 명확하게 보여줍니다.

유럽의 폴리염화비닐(PVC) 시장 보고서는 제품 유형(경질 PVC, 연질 PVC, 저발연 PVC, 기타), 안정제 유형(칼슘계, 납계, 주석·유기 주석계, 기타), 용도(파이프·피팅, 필름 및 시트, 전선 및 케이블, 기타), 최종 사용자 산업(건축 및 건설, 자동차, 전기 및 전자, 기타), 지역(독일, 프랑스, 영국)으로 구분됩니다.

The Europe Polyvinyl Chloride Market size is estimated at 6.74 million tons in 2025, and is expected to reach 7.72 million tons by 2030, at a CAGR of 2.75% during the forecast period (2025-2030).

Robust demand in pipes, profiles, and fittings, coupled with moderate recovery in residential construction, underpins near-term volume gains. Regulatory pressure from REACH continues to accelerate calcium-zinc stabilizer adoption, yet sustained infrastructure spending cushions transition costs. Energy-efficient renovation programs, electrical grid upgrades, and water-management projects anchor structural demand, while circular-economy mandates fast-track investment in recycling and bio-attributed PVC. Competitive intensity remains moderate as integrated producers leverage scale, captive feedstocks, and proprietary technology to offset compliance costs.

The region's housing shortage and aging building stock keep renovation activity high, driving window-profile and siding volumes in the Europe PVC market. Thermal-performance gains of 12-13% in PVC frames reinforced with thermoplastic inserts improve compliance with EU energy-efficiency codes, further entrenching rigid PVC in retrofit projects. Member-state recovery funds earmark civil-works spending, with water-retention drainage systems illustrating PVC's functional and cost advantages in agricultural infrastructure. Stabilizing interest rates and normalized material prices enhance project viability across Northern markets, though fiscal constraints continue to cap growth in Southern Europe. The overall effect is a well-distributed, medium-term lift in PVC pipe and profile demand.

Electric-vehicle adoption is reshaping interior-component specifications, widening the aperture for flame-retardant flexible PVC in wire harnesses and floor coverings. German motor-vehicle output advanced 3% YoY in early 2025, boosting resin off-take from regional compounding plants. Bio-attributed PVC grades cut cradle-to-gate CO2 emissions by 58% while preserving tensile and thermal performance, enabling OEMs to meet ESG targets without platform redesign. Growth clusters around Germany, France, and northern Italy facilitate optimized logistics and just-in-sequence supply models. Tier-one suppliers are pairing digital quality-control tools with material innovations to eliminate trim waste and reduce cycle times.

Large supermarket chains across Western Europe are phasing out PVC trays and cling films, pressuring converters to shift toward mono-material PET or paper-based formats. The forthcoming Packaging and Packaging Waste Regulation adds PFAS and BPA constraints, complicating compliance pathways for legacy PVC formulations. While pharmaceutical blister packs remain exempt, high-volume fresh-food segments experience immediate substitution, shaving flexible-film demand in the Europe PVC market. Brand-owner purchasing policies cascade upstream, compelling compounders to qualify alternative resins or develop recyclable PVC-blends for niche, barrier-critical applications. Eastern markets show lagged uptake of bans, offering temporary relief yet signaling an eventual region-wide transition.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Rigid grades anchored 60.74% of the Europe PVC market share in 2024 as pipes, profiles, and fittings retain dominance across building and water-supply networks. Low-smoke PVC, although a smaller base, is set to clock the strongest 3.89% CAGR through 2030 on the back of fire-safety regulations in mass-transit, tunnel, and public-assembly projects. Flexible PVC volumes face mixed fortunes: demand for bio-plasticized clear grades in medical tubing offsets contraction in food-packaging films. Chlorinated PVC penetrates industrial hot-water lines, leveraging localized production to mitigate import tariffs and logistics costs.

Capacity additions stay disciplined as mature demand patterns stabilize operating rates around 80%. Extruders focus on die-head upgrades and inline-measurement systems to boost yields rather than greenfield expansions. Product-mix agility becomes a competitive differentiator as converters juggle rigid-clear orders for chemical-processing sight-glasses alongside bulk commitments for municipal pipe contracts. The Europe PVC market thus balances steady, high-volume rigid demand with specialty growth niches in low-smoke and CPVC segments.

Calcium-zinc solutions held 42.88% of stabilizer consumption in 2024, a clear signal of market pivot after the EU lead ban These packages are projected to expand at 3.61% CAGR to 2030, driving most additive-level value growth in the Europe PVC market. Lead-based stabilizers now persist mainly in recycled rigid streams under temporary derogations, while tin systems linger in heat-resistant wire-coating niches. Barium-zinc and liquid-mixed-metal formats supply specialty sheet calendaring but face volume erosion as unified green-chemistry criteria spread downstream.

Chemical suppliers scale modular blending facilities near major extrusion hubs, ensuring just-in-time deliveries and tighter formulation control. Collaborative qualification programs with profile manufacturers accelerate line-change approvals, compressing conversion timelines. The stabilizer shift underscores how regulatory imperatives reshape supply chains in favor of actors with R&D depth and integrated logistics.

The Europe PVC Market Report is Segmented by Product Type (Rigid PVC, Flexible PVC, Low-Smoke PVC, and More), Stabilizer Type (Calcium Based, Lead Based, Tin and Organotin Based, and More), Application (Pipes and Fittings, Films and Sheets, Wires and Cables, and More), End-User Industry (Building and Construction, Automotive, Electrical and Electronics, and More), and Geography (Germany, France, United Kingdom, Italy, and More).