ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

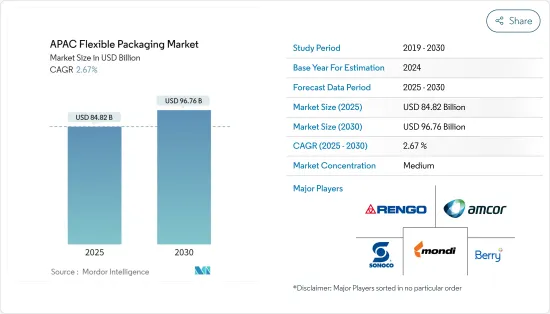

아시아태평양의 연질 포장 시장 규모는 2025년에 848억 2,000만 달러로 추정되며 예측 기간 중(2025-2030년) 연평균 성장율(CAGR)은 2.67%로, 2030년에는 967억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

아시아태평양의 연질 포장은 예측 기간 동안 안정적인 성장률을 보일 것으로 예상됩니다. 이 지역의 저명한 공급업체 중 일부는 포장 수명 주기의 세 단계인 제조, 운송, 폐기에 걸쳐 효율적인 제조 기술을 채택함으로써 환경 지속 가능성에 대한 우려가 커지고 있는 것에 초점을 맞추고 있습니다.

소매 판매가 급증함에 따라 시장은 새로운 제품을 도입하고 기존 제품의 범위를 넓히며 확장하는 경향이 있습니다. 식음료에서 제약, 퍼스널 케어에 이르기까지 다양한 산업에서 다양한 제품 범주에 걸쳐 다용도로 사용할 수 있는 연질 포장을 활용하고 있습니다. 따라서 소매 판매의 증가는 연질 포장 시장의 다양한 부문을 강화할 것입니다.

아시아태평양에서는 중국과 인도 등 신흥 경제권의 급속한 도시화로 인해 아시아태평양 지역에서 연질 포장에 대한 국내 수요가 크게 증가하고 있습니다. 이 지역의 최종 사용자 전반에 걸친 건강한 성장으로 인해 주로 랩 및 파우치 부문에서 연질 포장 제품에 대한 수요가 더욱 증가하고 있으며, 주로 이 지역의 증가하는 중산층 인구의 소량 소매 수요를 해결하기 위해 사용되고 있습니다.

연질 포장 제품에 대한 수요는 주로 이 지역의 밀레니얼 세대 소비자들이 주도하고 있는데, 이들은 1인분 및 이동식 식음료 제품을 매우 선호하기 때문입니다. 이러한 제품은 일반적으로 휴대가 간편하고 내구성이 뛰어나며 가볍기 때문에 연질 포장은 인기 있는 옵션입니다. 신선식품과 가공식품 모두에서 가장 빠르게 성장하는 스낵 식품 분야가 식음료 업계의 연질 포장 수요를 좌우할 것으로 예상됩니다. 2023년에는 인도의 퍼프 스낵 과자 기업 중 Bingo와 Kurkure가 각각 10% 이상의 높은 시장 점유율을 가졌습니다. 이에 이어지는 것은 Taka Tak이었으며 동기간 시장 점유율은 6%였습니다.

음료 산업은 이 지역 전체에서 연질 포장의 잠재적 성장 기회를 제공합니다. 식품 회사들은 이러한 수요 증가에 대응하기 위해 지역 및 제품 라인 측면에서 사업을 확장하고 있습니다. 예를 들어, 1760년에 설립된 중국에서 가장 오래된 식품 회사 중 하나인 Shou Quan Zhai는 새로운 레이디 음료 제품 라인에서 음료 산업에 진출했습니다.

2024년 1월 중국의 음료 브랜드는 국제 시장에서 뛰어나고 일관된 고품질의 제품과 서비스를 제공함으로써 지역사회에 정착했습니다. 허난성 정주 출신으로 세계 3만 6,000개 이상의 매장망을 자랑하는 Mixue Group은 홍콩에 신규 주식 공개를 신청하여 중요한 한 걸음을 내디뎠습니다. 음료 산업에서 이러한 확장은 시장 성장을 더욱 촉진할 수 있습니다.

러시아와 우크라이나 전쟁으로 인해 국제 유가가 변동하면서 플라스틱, 폴리에틸렌, 폴리프로필렌 및 기타 석유화학 유도체와 같은 연질 포장재에 사용되는 원자재 가격에 직접적인 영향을 미쳤습니다. 이 원료는 연질 포장에 사용되는 필름, 파우치 및 랩의 제조에 필수적입니다. 석유 기반 제품의 비용 상승은 이 지역의 연질 포장 및 제조업체의 생산 비용을 인상하여 최종 제품의 가격 상승으로 이어지고 있습니다.

아시아태평양의 연질 포장 시장 동향

확대되는 식품산업이 시장 성장을 견인할 전망

연질 포장은 스무디, 스낵, 유제품, 과자류 등의 식품에 일반적으로 사용됩니다. 전형적인 연질 식품 포장에는 치즈, 육류, 빵, 채소 등을 포장하는 필름, 파우치, 알루미늄 뚜껑, 종이 봉투 등이 있습니다. 이러한 연포장은 경우에 따라 1차 포장뿐만 아니라 2차 포장으로도 사용할 수 있습니다.

포장 식품 산업은 식품 가공 기술의 혁신과 소비자 라이프스타일의 변화로 인해 성장세를 보이고 있습니다. 이러한 추세는 결국 제품 수요를 증가시켜 예측 기간 동안 시장의 성장을 촉진할 것으로 예상됩니다. 예를 들어 PepsiCo India는 2024년 2월 감자칩의 라인업에 새로운 서브브랜드 Lay's Shapez를 도입했습니다. 이 혁신적인 제품은 감자로 만든 하트 모양의 펠렛을 발표합니다.

또한 2024년 8월, 스리랑카에서 가장 오래된 제과 제조업체인 Uswatte Confectionery Works Pvt. Ltd는 유명한 감자칩 브랜드인 Chirpy Chips의 부활을 발표했습니다. 이 회사는 이전에 고품질 감자 수입을 제한하는 정부 정책으로 인해 이 브랜드를 중단한 바 있습니다. 스리랑카 제과 제조업체의 감자 스낵 재진출은 시장 성장에 도움이 될 것으로 기대됩니다.

다층 필름이나 라미네이트 등의 연질 포장 재료는 식품을 습기, 산소, 오염물질로부터 보호하는 중요한 장벽 특성을 갖추고 있습니다. 이는 유제품, 육류, 제과류와 같은 부패하기 쉬운 품목의 유통기한을 연장하는 데 도움이 됩니다. 소비자와 식품 제조업체 모두 제품의 신선도를 유지하면서 식품 안전을 보장하는 포장 솔루션을 찾고 있으며, 연질 포장이 바람직한 옵션이 되고 있습니다.

2023년 일본에서의 청량음료의 온라인 소매 매출은 약 26억 달러에 이르렀으며 식품기반 전자상거래 산업에서 가장 큰 부문이 되었습니다. 중국국가통계국에 따르면 2023년 중국 외식산업의 연간 매출액은 약 5조 3,000억 위안에 달했습니다. 이는 전년 대비 약 20% 증가를 보여줍니다.이러한 전자상거래 및 음식 배달 서비스의 확대로 인해 배송의 혹독함을 견딜 수 있는 가볍고 내구성이 뛰어나며 보호 기능이 있는 포장재의 필요성이 가속화되었습니다. 연질 포장은 비용 효율적이고 건조 식품과 액체 식품 모두에 적용할 수 있어 이러한 요구를 충족합니다.

현저한 시장 성장이 기대되는 인도

인도는 경제, 사회, 산업이 빠르게 발전하고 있기 때문에 연질 포장 시장의 성장을 이끌어내는 중요한 역할을 합니다.14억 명이 넘는 인구를 보유한 인도는 세계에서 가장 큰 소비 시장 중 하나입니다. 급속한 도시화로 인해 더 많은 사람들이 도시로 이주하고 포장재에 대한 수요가 증가하면서 라이프스타일이 변화하고 있습니다. 비카지에 따르면 포장 식품의 시장 가치는 2026년까지 5조 루피를 넘어설 것으로 예상됩니다.

인도의 식음료 산업은 소비자 선호도의 변화와 가공 및 포장 식품에 대한 지출 증가로 인해 상당한 성장을 경험하고 있습니다. 이 산업은 인도에서 가장 큰 연질 포장 최종 사용처입니다. 2023년 인도에서 천연 건강 음료의 소매 판매 가치는 뜨거운 음료의 경우 11억 달러 이상으로 가장 높았습니다. 또한 같은 해 천연 건강 음료의 소매 판매 가치는 16억 달러를 넘어섰습니다.

인도를 비롯한 신흥 경제국에서 스낵 시장이 확대되면서 스낵 파우치, 랩, 가방 등을 만드는 데 연포장재를 적용하여 시장 공급업체에게 성장 기회를 창출하고 있습니다. 또한 인도의 스낵 브랜드인 비카지는 2023년 7월 인도의 스낵 시장이 성장세를 보이고 있다고 보고했습니다.

인도는 전 세계 제약 산업에서 중요한 역할을 하는 국가로, 연질 포장에 대한 수요가 증가하고 있습니다. 연질 포장은 정제, 캡슐, 시럽 등 제약 제품을 위한 변조 방지, 내습성, 보호 솔루션을 제공합니다. 특히 코로나19 이후 위생과 안전에 대한 관심이 높아지면서 의료 부문이 확장됨에 따라 연질 포장은 제품의 무결성과 안전을 보장하는 데 점점 더 중요한 역할을 하고 있습니다.

인도 소비자와 기업들 사이에서 지속 가능성과 플라스틱 폐기물 감소의 중요성에 대한 인식이 높아지고 있습니다. 이는 친환경적이고 재활용 가능한 연질 포장재에 대한 수요 증가로 이어졌습니다. 인도 정부는 일회용 플라스틱 사용 금지 및 지속 가능한 관행을 장려하는 정책을 도입했습니다. 이러한 규제로 인해 제조업체들은 생분해성 및 퇴비화 가능한 연질 포장과 같은 혁신적인 패키징 솔루션으로 전환하고 있습니다.

아시아태평양의 연질 포장 산업 개요

아시아태평양의 연질 포장 시장은 부문화되어 있으며 Amcor Ltd, Berry Plastics Corporation, Mondi Group, Sonoco Products Company 및 Rengo와 같은 중요한 기업이 존재합니다.

The APAC Flexible Packaging Market size is estimated at USD 84.82 billion in 2025, and is expected to reach USD 96.76 billion by 2030, at a CAGR of 2.67% during the forecast period (2025-2030).

Key Highlights

Flexible packaging in Asia-Pacific is expected to witness a stable growth rate during the forecast period. Some of the prominent vendors in the region are focusing on the ever-growing concern regarding environmental sustainability by adopting efficient manufacturing techniques throughout the three stages of the packaging life cycle: manufacturing, transportation, and disposal.

As retail sales surge, markets tend to expand, introducing new products and broadening the reach of existing ones. Diverse industries, ranging from food and beverages to pharmaceuticals and personal care, utilize flexible packaging due to its versatility across various product categories. Consequently, a rise in retail sales stands to bolster various segments of the flexible packaging market. In 2023, Japan's retail industry achieved sales of approximately JPY 163 trillion, marking its highest value over the previous 15 years, as reported by METI (Japan).

There is a considerable increase in domestic demand for flexible packaging in Asia-Pacific, owing to the rapid urbanization across emerging economies, such as China and India. Healthy growth across end users in the region is further driving the need for flexible packaging products, primarily in the wraps and pouches segment, majorly to address the small quantity retailing needs of the rising middle-income population in the region.

The demand for flexible packaging products is mainly driven by millennial consumers in the region, as they have an avid preference for single-serving and on-the-go style food and beverage products. As these products are generally designed to be portable, durable, and lightweight, flexible packaging is a popular option. The fastest-growing areas of snack foods, both in terms of fresh items and processed foods, are expected to govern the demand for flexible packaging from the food and beverage industry. In 2023, Bingo and Kurkure had the highest market share of over 10% each among the puffed snacks companies in India. This was followed by Taka Tak, with a 6% market share during the same period.

The beverage industry offers potential growth opportunities for flexible packaging across the region. Food companies are expanding their businesses in terms of geography and product lines to cater to this rising demand. For instance, Shou Quan Zhai, founded in 1760 and one of the oldest food companies in China, expanded into the beverage industry with a new line of ready-to-drink products.

In January 2024, Chinese beverage brands made strides in international markets, embedding themselves into local communities by offering consistent quality products and services. Mixue Group, hailing from Zhengzhou in Henan province and boasting a network of over 36,000 stores globally, took a significant step by filing for an initial public offering in Hong Kong. Such expansion in the beverage industry may further propel market growth.

The Russia-Ukraine War caused fluctuations in global oil prices, directly impacting the cost of raw materials used in flexible packaging, such as plastics, polyethylene, polypropylene, and other petrochemical derivatives. These materials are essential for producing films, pouches, and wraps used in flexible packaging. The increased cost of petroleum-based products raised the production costs for flexible packaging manufacturers in the region, leading to price increases for end products.

APAC Flexible Packaging Market Trends

Expanding Food Industry Expected to Drive Market Growth

Flexible packaging is commonly used for food products such as smoothies, snacks, dairy, confectionery, etc. Typical flexible food packaging applications include films, pouches, aluminum lids, and paper bags to package cheeses, meats, bread, and vegetables. This flexible packaging can be used as primary packaging as well as secondary packaging in some cases.

The packaged food industry has been witnessing growth owing to innovations in food processing techniques and changes in consumer lifestyles. These trends are anticipated to eventually boost product demand, propelling the growth of the market during the forecast period. For instance, in February 2024, PepsiCo India introduced a new sub-brand, Lay's Shapez, to its potato chips lineup. The innovative product showcases heart-shaped pellets made from potatoes.

Also, in August 2024, Uswatte Confectionery Works Pvt. Ltd, Sri Lanka's oldest confectionery manufacturer, announced the revival of its famous potato chip brand, Chirpy Chips. The company had previously discontinued the brand due to government policies restricting the import of high-quality potatoes into the country. This re-entry of potato snacks by confectionery manufacturers in Sri Lanka is expected to support market growth.

Flexible packaging materials, such as multilayer films and laminates, provide significant barrier properties that protect food from moisture, oxygen, and contaminants. This helps to extend the shelf life of perishable items like dairy products, meat, and baked goods. Consumers and food manufacturers alike seek packaging solutions that maintain product freshness while also ensuring food safety, making flexible packaging a preferred choice.

In 2023, online retail sales of soft drinks in Japan amounted to around USD 2.6 billion, making it the largest segment within the food-based e-commerce industry. According to the National Bureau of Statistics of China, in 2023, the annual revenue of the foodservice industry in China amounted to around CNY 5.3 trillion. This indicated an increase in revenue of approximately 20% compared to the previous year. Such expansion of e-commerce and food delivery services has accelerated the need for lightweight, durable, and protective packaging that can withstand the rigors of shipping. Flexible packaging fits these needs by being cost-effective and adaptable for both dry and liquid food products.

India Is Expected to Witness Significant Market Growth

India is playing a significant role in driving the growth of the flexible packaging market due to its rapidly evolving economic, social, and industrial landscape. With a population of over 1.4 billion, India is one of the largest consumer markets in the world. Rapid urbanization is leading to lifestyle changes, with more people moving to cities and a higher demand for packaged goods. According to Bikaji, the market value of packaged food is likely to surpass INR 5 trillion by 2026.

India's food and beverage industry is experiencing significant growth, driven by changing consumer preferences and increasing spending on processed and packaged foods. This industry is the largest end user of flexible packaging in the country. In 2023, the retail sales value of naturally healthy beverages in India was the highest for hot drinks at over USD 1.1 billion. Furthermore, the retail sales value of the naturally healthy beverages surpassed USD 1.6 billion that same year.

The snacks market has been expanding in emerging economies, including India, creating a growth opportunity for market vendors due to the application of flexible packaging in making snack pouches, wraps, bags, and others. Additionally, Bikaji, a snack brand in India, reported that the savory snacks market in India witnessed growth in July 2023.

India is a significant player in the global pharmaceutical industry, and the demand for flexible packaging is growing. Flexible packaging offers tamper-evident, moisture-resistant, and protective solutions for pharmaceutical products, including tablets, capsules, and syrups. As the healthcare sector expands, especially with the increasing focus on hygiene and safety post-COVID-19, flexible packaging plays an increasingly crucial role in ensuring product integrity and safety.

There is growing awareness among Indian consumers and companies about the importance of sustainability and reducing plastic waste. This has led to improved demand for eco-friendly and recyclable flexible packaging materials. The Indian government has introduced policies such as the ban on single-use plastics and initiatives promoting sustainable practices. These regulations are pushing manufacturers toward innovative packaging solutions like biodegradable and compostable flexible packaging.

APAC Flexible Packaging Industry Overview

The APAC flexible packaging market is fragmented, with the presence of significant companies like Amcor Ltd, Berry Plastics Corporation, Mondi Group, Sonoco Products Company, and Rengo Co. Ltd. The companies continuously invest in strategic collaborations and product developments to gain market share.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of the Impact of Key Macroeconomic Trends on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increased Demand for Convenient Packaging

5.1.2 Demand for Longer Shelf Life and Innovative Packaging

5.2 Market Restraints

5.2.1 Concerns About the Environment and Recycling of Packaging Material