ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

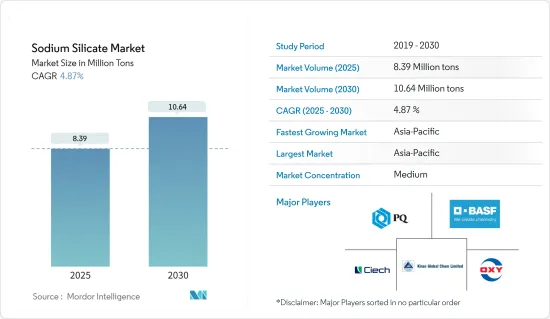

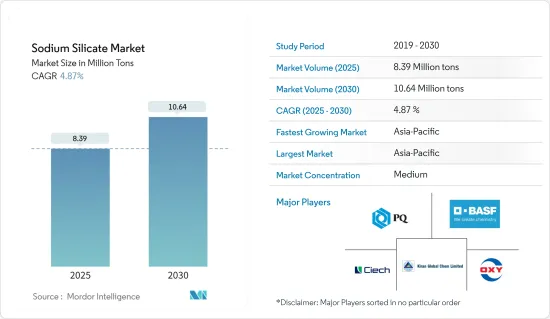

규산나트륨 시장 규모는 2025년에 839만 톤으로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 4.87%로, 2030년에는 1,064만 톤에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 시장에 부정적인 영향을 미쳤습니다. 봉쇄와 규제에 의해 제조시설이나 공장이 폐쇄되었기 때문입니다. 공급망과 운송의 혼란은 시장에 더 이상 장애를 가져왔습니다. 그러나 업계는 2021년에 회복을 목격하여 연구 된 시장에 대한 수요가 반등했습니다.

주요 하이라이트

중기 적으로 폐지 재활용에 대한 수요 증가와 고무 및 타이어 산업의 침전 실리카 수요 증가는 연구 된 시장의 성장을 이끄는 요인 중 일부입니다.

반면에 엄격한 정부 규제와 규산 나트륨의 유해한 영향으로 인한 건강 위험 증가는 규산 나트륨 시장의 성장을 저해 할 것으로 예상됩니다.

그러나 건설 부문의 성장은 예측 기간 동안 많은 기회를 제공할 것으로 예상됩니다.

아시아태평양은 다양한 용도의 높은 수요로 시장을 독점하고 있습니다.

규산나트륨 시장 동향

건강한 수요를 확인하는 세제 부문

규산 나트륨은 실리카와 나트륨 산화물로 이루어진 무색 화합물입니다. 비누, 세제 및 실리카겔 제조에 사용됩니다. 세제 성분에서 규산나트륨의 역할은 지방과 유기 오일의 부식, 알칼리화 및 유화를 제어하고 칼슘과 마그네슘의 경도를 낮추는 것입니다.

금속 세척, 섬유 가공, 세탁, 종이 잉크 제거 등 많은 세제 작업에서 규산나트륨을 사용하여 식기, 유제품 장비, 병, 바닥, 기관차 등을 세척합니다.

액체 세탁 세제는 주로 세탁물을 청소하는 데 사용되며 주거용과 상업용이라는 두 가지 주요 최종 사용자 세그먼트가 있습니다. 액체 세탁 세제에 대한 수요는 세제 분말보다 편안하고 사용하기 쉬우며 낭비가 적기 때문에 증가하고 있습니다.

현재 북미는 전 세계 액체 세탁 세제의 수요와 소비를 주도하는 지역입니다. 미국은 가정용 및 산업용 세제의 선진 시장 중 하나입니다. 예를 들어, Happi Magazine에 따르면 2022년 10월 30일까지 52주 동안 미국에서 액체 세탁 세제 카테고리의 판매량은 총 약 6억 4,100만 개에 달했습니다.

또한, 2022년 미국에서 단위 용량 세탁 세제 브랜드 1위는 12억 달러 이상의 매출을 기록한 Tide였으며, 그 뒤를 이어 'Gain'과 'All' 브랜드가 뒤를 이었습니다. '올' 브랜드는 1억 달러 이상의 매출을 기록했습니다.

독일에서는 국민들의 건강과 위생적인 생활에 대한 관심이 높아지면서 세탁 세제에 대한 수요가 증가하고 있습니다. 예를 들어, IKW에 따르면 2022년 독일의 세탁 세제 및 청소용품 매출은 51억 4,400만 유로(약 5조 4,200억 원)로 2021년 대비 1% 증가한 것으로 나타났습니다. 따라서 세탁 세제의 소비가 증가하면 규산나트륨 시장에도 긍정적인 영향을 미칠 것으로 예상됩니다.

이러한 용도는 규산나트륨 수요를 높일 것으로 예상됩니다.

아시아태평양이 규산나트륨 시장을 독점

아시아 태평양은 여러 중대형 및 소규모 산업이 있는 주요 산업화 지역입니다. 아시아 태평양 규산나트륨 시장은 중국, 인도 등의 높은 제품 수요로 인해 성장할 것으로 예상됩니다.

중국은 전 세계에서 가장 큰 물 소비국 중 하나로, 식수 첨가제 소비량이 6,100억 입방미터에 달합니다. 이는 규산나트륨이 식용 식수 첨가제로 승인된 이후 수처리에 광범위하게 사용되어 왔기 때문에 규산나트륨 시장의 잠재적인 원동력이 되고 있습니다. 예를 들어, 2022년 6월 물 환경 관리에 중점을 둔 환경 보호 회사인 중국 에버브라이트 워터는 산둥성 즈보시에 있는 장뎬이스트 화학 산업단지 산업 폐수 처리 확장 및 업그레이드 프로젝트를 확보했습니다. 이 프로젝트는 일일 산업 폐수 처리 용량이 약 5,000m3로 설계된 BOT(건설-운영-이전) 모델로 운영될 예정입니다.

게다가 중국은 2022년 3월에 1,246만 톤의 가공 종이 및 판지를 생산하여 2021년 3월의 1,197만 톤에 비해 4%의 성장률을 기록했습니다. 2022년 9월 중국의 가공 종이 및 판지 생산량은 약 1,160만 톤이었습니다.

한국에서는 2016-2025년 물 환경 관리 마스터 플랜에 따른 정부 지원이 한국의 수처리 활동을 더욱 활성화하여 예측 기간 동안 규산나트륨 시장 성장을 확산시킬 것으로 예상됩니다.

인도네시아에서는 수처리와 폐수 처리가 중요한 과제입니다. 인도네시아의 수자원은 세계의 6%, 아시아태평양의 21%를 차지하고 있지만, 이 나라의 하천의 68%는 처리되지 않고 폐수가 배출되고 있기 때문에 오염이 심각해, 수처리 시스템에의 거액의 투자가 필요해, 이 나라의 규산나트륨 시장 수요를 증대시키고 있습니다. 예를 들어, 유니세프에 따르면 인도네시아 국민의 75%만이 완전한 물 접근성과 위생 시설을 갖추고 있습니다. 정부는 식수 부문이 낙후되지 않도록 수처리를 위한 충분한 인프라를 구축하기 위해 많은 노력을 기울이고 있습니다. 완전히 발전된 식수 위생을 보장하기 위해서는 1인당 연간 7만 IDR(미화 5.00달러)의 투자가 필요합니다. 자카르타의 깨끗한 물 수요는 2017년 초당 28m3/s에서 2030년까지 41.6m3/s로 증가할 것으로 예상됩니다.

중국 국가통계국에 따르면 중국의 제지 및 제지 제품 제조업체는 2022년에 2,175억 달러 이상의 매출을 올렸으며, 이는 2021년에 비해 3.59% 증가한 수치입니다. 또한, 국제 무역에 관한 UN COMTRADE 데이터베이스에 따르면 중국의 종이 및 판지, 펄프, 종이 및 보드의 수출액은 2022년에 316억 3,000만 달러에 달했습니다. 따라서 이러한 제지 및 판지 수출은 규산나트륨 시장에 상승 여력을 제공할 것으로 예상됩니다.

다양한 산업에서의 이러한 성장은 예측 기간 동안 아시아태평양의 규산나트륨 시장을 견인할 것으로 예상됩니다.

규산나트륨 산업 개요

규산나트륨 시장은 그 특성상 부분적으로 통합되어 있습니다. 이 시장의 주요 기업(특정한 순서 없음)에는 CIECH Group, Kiran Global Chem Limited., PQ Corporation, BASF SE, Occidental Petroleum Corporation 등이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

폐지 재활용 수요 증가

고무 및 타이어 산업으로부터의 침전 실리카 수요 증가

기타 촉진요인

억제요인

규산나트륨의 유해성

기타 억제요인

밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(수량 기준 시장 규모)

유형

고체

액체

용도

접착제와 도료

세제

식품 보존

침전 실리카

제지

수처리

기타 용도(건축, 금속 주조)

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

Alumina doo Zvornik

BASF SE

CIECH Group

C THAI GROUP

Evonik Industries AG

FUJI SILYSIA CHEMICAL LTD.

Hindcon

Kiran Global Chem Limited

Occidental Petroleum Corporation

PQ Corporation

Silmaco

WR Grace & Co.-Conn.

Z. Ch. Rudniki SA

제7장 시장 기회와 앞으로의 동향

건설 부문의 성장

기타 기회

HBR

영문 목차

영문목차

The Sodium Silicate Market size is estimated at 8.39 million tons in 2025, and is expected to reach 10.64 million tons by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

Over the medium term, the increasing demand for waste paper recycling and increasing demand for precipitated silica from the rubber and tyre industry are some of the factors driving the growth of the market studied.

On the flip side, stringent government regulations and increased health risks due to the hazardous effects of sodium silicate are expected to hinder the growth of the sodium silicate market.

However, growth in construction sector is anticipated to provide numerous opportunities over the forecast period.

Asia-Pacific dominated the market, owing to the high demand from various applications.

Sodium Silicate Market Trends

Detergents Segment to Witness Healthy Demand

Sodium silicate is a colorless compound of silica and oxides of sodium. It is used in soaps, detergents, and the making of silica gel. The role of sodium silicate in the composition of detergents is to control the corrosion, alkalization, and emulsion of fats and organic oils, and reduce the hardness of calcium and magnesium.

Many detergent operations are performed using sodium silicates, such as metal cleaning, textile processing, laundering, and de-inking paper, to wash dishes, dairy equipment, bottles, floors, and locomotives.

Liquid laundry detergent is primarily used in cleaning laundry and has two main end-user segments, namely, residential and commercial. The demand for liquid laundry detergent is growing due to the comfort and ease of application and lesser wastage than detergent powders.

North America is currently the region leading the global demand and consumption of liquid laundry detergent. The United States is among the developed markets for household and industrial detergents. For instance, according to Happi Magazine, for the 52 weeks that ended October 30, 2022, the liquid laundry detergent category had sales totaling approximately 641 million units in the United States.

Moreover, in 2022, Tide was the leading unit dose laundry detergent brand in the United States, registering over USD 1.2 billion in sales, followed by the brands "Gain" and "All". The brand, All, had a sales value of over USD 100 million.

In Germany, due to increasing demand for laundry detergent drugs owing to growing concerns regarding the health and hygienic living among the people. For instance, according to IKW, in 2022, revenue from laundry detergents and cleaning products in Germany amounted to EUR 5.14 billion (~USD 5.42 billion), which showed an increase of 1% compared to 2021. Therefore, increasing the consumption of laundry detergents is expected to create an upside for the sodium silicate market.

Such aforementioned applications are, in turn, expected to boost the demand for sodium silicate.

Asia-Pacific to Dominate the Market for Sodium Silicate

Asia-Pacific is a major industrialized region that houses multiple heavy, medium, and small-scale industries. The Asia-Pacific sodium silicate market is expected to experience growth on account of high product demand in China, India, etc.

China is one of the biggest water consumers worldwide, with a consumption volume of 610 billion cubic meters of drinking water additives for human consumption. This is a potential driver for the sodium silicate market, as sodium silicate has been extensively used in water treatment since its approval as a drinking water additive for human consumption. For instance, in June 2022, an environmental protection company that focuses on water environment management, named China Everbright Water secured the expansion and upgrading project of the ZhangdianEast Chemical Industry Park Industrial Wastewater Treatment in Zibo City, Shandong Province. This project will be operated on a BOT (Build-Operate-Transfer) model, with a designed daily industrial wastewater treatment capacity of around 5 thousand m3.

Moreover, China produced 12.46 million metric tons of processed paper and cardboard in March 2022, compared to 11.97 million metric tons in March 2021, registering a growth of 4%. In September 2022, the production volume of processed paper and cardboard in the country was around 11.6 million metric tons.

In South Korea, the government initiative, under the Water Environment Management Master Plan of 2016-2025 plan, is likely to further boost the water treatment activities in the country, which, in turn, will proliferate the sodium silicate market growth during the forecast period.

Water and wastewater treatment is an important issue in Indonesia. Indonesia's water resources account for 6% of the world's and 21% of Asia-Pacific's water resources, and yet 68% of rivers in Indonesia are heavily polluted due to the discharge of wastewater without treatment, thus, requiring huge investment in water treatments system that will augment the demand sodium silicate market in the country. For instance, according to UNICEF, only 75% of Indonesians have complete water accessibility and sanitation. The government is trying to put significant efforts to build sufficient infrastructure for water treatment so that the drinking water sector is not left behind. An investment of IDR 70 thousand (USD 5.00) per capita per year is needed in the country to ensure fully developed water sanitation. Clean water needs in Jakarta are expected to rise from 28 cubic meters per second (m3/s) in 2017 to 41.6 m3/s by 2030.

According to the National Bureau of Statistics, paper and paper product manufacturers in China generated a revenue of more than USD 217.5 billion in 2022, which showed an increase of 3.59% compared to 2021. Moreover, according to United Nations COMTRADE database on international trade, China's exports of paper and paperboard, articles of pulp, paper, and board amounted to USD 31.63 billion in 2022. Therefore, these paper and paperboard exports are expected to create an upside for the sodium silicate market.

Such growth in various industries is expected to drive the market for sodium silicate in the Asia-Pacific region during the forecast period.

Sodium Silicate Industry Overview

The Sodium Silicate Market is partially consolidated in nature. The major players in this market (not in a particular order) include CIECH Group, Kiran Global Chem Limited., PQ Corporation, BASF SE, and Occidental Petroleum Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Waste Paper Recycling

4.1.2 Rising Demand for Precipitated Silica from the Rubber and Tyre Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Hazardous Effects of Sodium Silicate

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Solid

5.1.2 Liquid

5.2 Application

5.2.1 Adhesives and Paints

5.2.2 Detergents

5.2.3 Food Preservation

5.2.4 Precipitated Silica

5.2.5 Paper Production

5.2.6 Water Treatment

5.2.7 Other Applications (Construction, Metal Casting)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements