ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

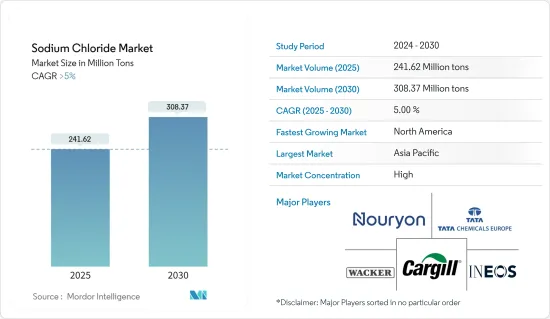

염화나트륨 시장 규모는 2025년에 2억 4,162만 톤으로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 5%를 넘고, 2030년에는 3억 837만 톤에 달할 것으로 예측됩니다.

2020년에 발생한 코로나19는 건설 작업의 일시적인 중단과 전 세계 화학 제조 시설의 폐쇄로 인해 시장에 악영향을 미쳤습니다. 그러나 시장은 회복세를 보였으며 예측 기간 동안 유사한 예측을 따를 것으로 예상됩니다.

주요 하이라이트

북미와 유럽에서는 식음료 산업에서 염화나트륨 수요 증가와 의약품 등급 염화나트륨 수요가 시장 확대의 원동력이 될 전망입니다.

그러나 방부제 및 제빙제로 활용될 수 있는 향상된 특성을 가진 수많은 대체 화학 물질의 출현은 시장 성장을 저해할 수 있습니다.

나트륨계 배터리의 사용 증가와 염소 알칼리 제품의 생산은 미래 시장 성장에 다양한 기회를 제공할 것으로 예상됩니다.

아시아태평양 지역이 시장을 지배하고 있으며 북미는 예측 기간 동안 빠르게 발전 할 것으로 예상됩니다.

염화나트륨 시장 동향

시장을 독점하는 화학제품 생산 부문

염화나트륨은 유기 및 무기, 염소, 소다회, 가성소다와 같은 염소 알칼리 화합물을 포함한 많은 화학 물질을 생산합니다. 이러한 물질은 폴리염화비닐(PVC), 세제, 유리, 염료, 비누 등 다양한 제품을 만드는 데 사용됩니다.

탄산나트륨(소다재)은 세제 및 야금 산업에 활용될 뿐만 아니라 인산염, 규산염, 유리 등 중화학 제품 생산에 사용됩니다. 석회석과 염화나트륨은 모두 저렴하고 널리 구할 수 있어 솔베이 공정에 사용됩니다. 암모니아와 이산화탄소는 소금과 석회석을 탄산나트륨으로 전환합니다.

2023년 상반기에는 EU27개국, 노르웨이, 스위스, 영국에서 약 362만 8,468톤의 염소가 생산되었습니다. 그러나 이는 2022년 상반기에 비해 생산량이 19.4% 감소했습니다. 2023년 9월의 염소 생산량은 2022년 9월에 비해 2% 증가가 관찰되었습니다.

보고서에 따르면 생산된 염소의 대부분은 PVC, EDC/VCM 용도로 사용되어 약 31.6%를 차지했으며, 이소시아네이트 및 산소산염(30.8%), 무기물(12.7%)이 그 뒤를 이었습니다.

미국 인구조사국에 따르면 2023년 건설 규모는 1조 9,787억 달러로, 2022년 1조 8,487억 달러보다 7% 증가했습니다. 이에 따라 경질 폼 단열 패널과 같은 PVC 제품 및 폴리우레탄 기반 건설 산업 자재에 대한 수요가 증가했습니다.

또한 가성소다는 목재를 목재 펄프로 전환하는 크래프트 공정에 사용되며 여전히 제지 제조에서 지배적인 방법입니다. 염소-알칼리 산업 리뷰에 따르면 2023년 9월까지 EU-27 국가, 노르웨이, 스위스, 영국에서 2,422.5킬로톤의 가성소다가 생산되었으며 유기물이 가장 큰 비중을 차지했습니다.

따라서 위에서 언급 한 요인에 따라 화학 제품 부문은 향후 몇 년 동안 시장을 지배 할 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아 태평양 지역은 화학 산업에서 수요가 증가하면서 글로벌 시장 점유율을 장악했습니다. 중국은 전 세계에서 생산되는 화학 물질의 대부분을 차지하는 화학 처리의 허브입니다.

중국 국가통계국에 따르면 중국은 화학, 수처리, 금속 가공에 사용되는 수산화나트륨을 3,900만 톤 이상 생산했습니다. 수산화나트륨은 산업용 외에도 가정용 세제에서도 흔히 발견됩니다.

Invest India가 발표한 통계에 따르면 인도의 주요 화학물질 생산량은 2023-2024년(2023년 8월까지) 53.54만 톤으로 감소했으며, 2022-2023년 해당 기간 동안 54.32만 톤 이상이 생산된 것으로 나타났습니다. 그러나 2023년 8월까지의 유기 화학물질 생산량은 전년도 같은 기간에 비해 4.52% 증가했습니다.

염화나트륨은 제약 산업의 다양한 응용 분야에서도 사용됩니다. 투석 및 주입 용액, 주사제, 식염수, 구강 재수 화염과 같은 API 및 기타 제품 제조에 사용됩니다.

인도 브랜드 자산 재단(IBEF)에 따르면 인도 제약 산업은 2030년까지 약 1,300억 달러에 달할 것으로 예상됩니다. 인도는 전 세계 최대 백신 생산국으로, 전 세계 백신의 약 60%를 생산하고 있습니다. 또한 의약품 생산량 기준으로는 전 세계 3위를 차지하고 있습니다.

염화나트륨 시장과 관련된 다양한 부문 수요가 계속 늘어나고 있기 때문에 이 시장은 아시아태평양이 독점할 것으로 예상됩니다.

염화나트륨 산업 개요

염화나트륨 시장은 주요 기업에서 굳어지고 있습니다. 주요 기업(특정한 순서 없음)에는 Nouryon, Cargill Incorporated, Wacker Chemie AG, INEOS, Tata Chemicals Europe 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

식음료 산업으로부터의 염화나트륨 수요 증가

북미와 유럽에서 의약품 등급의 염화나트륨 수요 증가

억제요인

방부제와 제빙제로서 이용 가능한 대체 화학제품의 출현

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(수량 기준 시장 규모)

등급

암염

태양염

진공염

용도

화학제품 제조

제빙

수질 조정

농업

식품가공

제약

기타

지역

아시아태평양

중국

인도

일본

한국

베트남

말레이시아

인도네시아

태국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

러시아

터키

이탈리아

노르딕

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

카타르

나이지리아

아랍에미리트(UAE)

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

Cargill, Incorporated.

CK 생명과학 인텔(Holdings) Inc.

Compass Minerals

INEOS

KS Aktiengesellschaft

Nouryon

Pon Pure Chemicals Group

Rio Tinto

Sudwestdeutsche Salzwerke AG

Swiss Salt Works AG

Tata Chemicals Europe

Wacker Chemie AG

제7장 시장 기회와 앞으로의 동향

나트륨계 배터리의 사용 증가

염소계 알칼리 제품의 생산 증가

HBR

영문 목차

영문목차

The Sodium Chloride Market size is estimated at 241.62 million tons in 2025, and is expected to reach 308.37 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 outbreak in 2020 had a detrimental influence on the market due to the temporary halt in construction operations and the worldwide shutdown of chemical manufacturing facilities. However, the market picked up and is expected to follow a similar projection during the forecast period.

Key Highlights

The increasing demand for sodium chloride in the food and beverage industry and the demand for pharmaceutical-grade sodium chloride in North America and Europe are expected to fuel the market expansion.

However, the emergence of numerous alternative chemicals with improved properties that can be utilized as preservatives and deicing agents may stifle market growth.

The increasing usage of sodium-based batteries and the production of chlor alkali products are expected to offer various opportunities for future market growth.

Asia-Pacific dominates the market, and North America is predicted to develop quickly throughout the forecast period.

Sodium Chloride Market Trends

The Chemical Production Segment to Dominate the Market

Sodium chloride produces many chemicals, including organic and inorganic, and chlor alkali compounds, such as chlorine, soda ash, and caustic soda. These materials are then used to make various products, including polyvinyl chloride (PVC), detergents, glass, dyes, and soaps.

In addition to being utilized in the production of detergents and the metallurgical industry, sodium carbonate (soda ash) is employed in producing heavy chemicals, including phosphates, silicates, and glass. Limestone and sodium chloride, both of which are inexpensive and widely accessible, are used in the Solvay process. Ammonia and carbon dioxide turn salt and limestone into sodium carbonate.

In the first half of 2023, about 3,628,468 tonnes of chlorine were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom. However, this was a 19.4% decrease in production volume compared to the first half of 2022. In September 2023, an increase of 2% was observed in chlorine production volume over September 2022.

According to the report, most chlorine produced was used in the PVC, EDC/VCM application, accounting for approximately 31.6%, followed by isocyanates and oxygenates (30.8%) and inorganics (12.7%).

According to the US Census Bureau, the value of construction in 2023 was USD 1,978.7 billion, 7% above the USD 1,848.7 billion spent in 2022. It, in turn, enhanced the demand for PVC products and polyurethane-based construction industry materials, such as rigid foam insulation panels.

Furthermore, caustic soda is used in the Kraft process, which converts wood into wood pulp and is still the dominant method in paper manufacturing. According to the Chlor-Alkali Industry Review, 2,422.5 kilotons of caustic soda were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom till September 2023, with organics accounting for the major share.

Therefore, based on the factors mentioned above, the chemical products segment is expected to dominate the market in the coming years.

Asia-Pacific to Dominate the Market

Asia-Pacific dominated the global market share, with rising demand from the chemical industry. China is a hub for chemical processing, accounting for most chemicals produced globally.

According to the National Bureau of Statistics of China, the country generated over 39 million metric tons of sodium hydroxide, which is used to make chemicals, water treatment, and metal processing. In addition to industrial use, sodium hydroxide is commonly found in domestic cleaning detergents.

According to the statistics presented by Invest India, the production of major chemicals in India decreased to 53.54 lakh tonnes during 2023-24 (up to August 2023), with over 54.32 lakh tonnes produced during the corresponding period of 2022-2023. However, the production of organic chemicals up to August 2023, as compared to the corresponding period of the previous year, recorded an increase of 4.52%.

Sodium chloride also serves its purpose in various applications in the pharmaceutical industry. It is used in manufacturing APIs and other products, such as dialysis and infusion solutions, injections, saline drips, and oral rehydration salts.

According to the India Brand Equity Foundation (IBEF), the Indian pharmaceutical industry is expected to reach ~USD 130 billion by 2030. The country is the largest producer of vaccines worldwide, accounting for around 60% of the total vaccines globally. Additionally, the country ranks third across the globe for pharmaceutical production by volume.

With the ever-increasing demands in the different sectors related to the sodium chloride market in one way or another, the market for the same is expected to be dominated by Asia-Pacific.

Sodium Chloride Industry Overview

The sodium chloride market is consolidated among the top players. The key players (not in a particular order) include Nouryon, Cargill Incorporated, Wacker Chemie AG, INEOS, and Tata Chemicals Europe.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Sodium Chloride from Food and Beverage Industry

4.1.2 Increasing Demand for Pharmaceutical-grade Sodium Chloride in North America and Europe

4.2 Restraints

4.2.1 Emergence of Numerous Alternative Chemicals that can be Utilized as Preservatives and Deicing Agents

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Grade

5.1.1 Rock Salt

5.1.2 Solar Salt

5.1.3 Vacuum Salt

5.2 Application

5.2.1 Chemical Production

5.2.2 Deicing

5.2.3 Water Conditioning

5.2.4 Agriculture

5.2.5 Food Processing

5.2.6 Pharmaceutical

5.2.7 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Vietnam

5.3.1.6 Malaysia

5.3.1.7 Indonesia

5.3.1.8 Thailand

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Russia

5.3.3.6 Turkey

5.3.3.7 Italy

5.3.3.8 NORDIC

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Qatar

5.3.5.4 Nigeria

5.3.5.5 United Arab Emirates

5.3.5.6 Egypt

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Cargill, Incorporated.

6.4.2 CK Life Sciences Int'l. (Holdings) Inc.

6.4.3 Compass Minerals

6.4.4 INEOS

6.4.5 K+S Aktiengesellschaft

6.4.6 Nouryon

6.4.7 Pon Pure Chemicals Group

6.4.8 Rio Tinto

6.4.9 Sudwestdeutsche Salzwerke AG

6.4.10 Swiss Salt Works AG

6.4.11 Tata Chemicals Europe

6.4.12 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Use of Sodium-based Batteries

7.2 Increasing Production of Chlor-alkali Products