ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

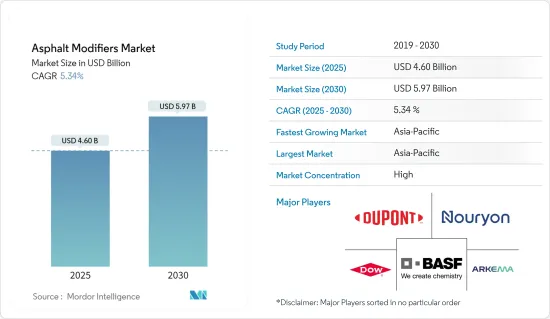

아스팔트 개질제 시장 규모는 2025년에 46억 달러로 예측되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 5.34%로, 2030년에는 59억 7,000만 달러에 달할 것으로 예측되고 있습니다.

코로나19는 제조 산업에 큰 영향을 미쳐 시장 성장을 저해했습니다. 그러나 이후 해당 산업은 팬데믹에서 회복되었습니다. 그 이후로 건설 산업의 꾸준한 성장이 시장의 주요 동력이 되었습니다.

주요 하이라이트

예측 기간 동안 도로의 교통량 증가와 하중 증가, 초절전 설계 사양 충족, 포장 수명 연장, MRO 비용 절감 등이 시장의 수요를 견인할 것으로 보입니다.

반면 개질 아스팔트 시멘트 사용의 높은 비용과 아스팔트 작업의 건강 위험은 시장의 성장을 둔화시킬 가능성이 높습니다.

HMA(핫믹스 아스팔트) 수요 증가, RAP(재생 아스팔트 포장)의 인기 증가, 생물재생 가능한 개질제의 개발, 웜믹스 아스팔트 기술의 개선, 아스팔트(나노클레이)를 변경하기 위해 나노기술을 사용하는 연구로부터 시장의 미래 기회가 기대되고 있습니다.

아스팔트 수요가 높기 때문에 아시아태평양이 가장 중요하며 앞으로 몇 년동안 계속 성장할 것으로 예상됩니다.

아스팔트 수정제 시장 동향

포장 용도로부터 수요 증가

아스팔트와 콘크리트의 혼합물은 도로, 공항 활주로, 유도로, 자전거 도로 등을 건설하는 데 많이 사용되어 왔습니다. 바인더 개질제(폴리머, 엘라스토머, 섬유, 고무 등)와 골재 개질제(석회, 과립 고무, 스트립 방지제 등)는 아스팔트 포장의 성능을 개선하여 열 균열, 틀어짐, 박리 등의 문제에 대한 저항력을 높여주는 데 사용됩니다. 이를 통해 포장 도로의 수명을 연장할 수 있습니다.

최근 몇 년 동안 아스팔트 개질제에 대한 전 세계 수요는 평균 이상의 성장세를 보이고 있습니다. 아스팔트 개질제에 대한 수요는 전 세계에서 진행 중인 도로 건설 활동의 수준과 직접적인 상관관계가 있습니다.

미국 인구조사국에 따르면 2022년에 미국에서 시행되는 연방 고속도로 및 도로 건설의 가치는 약 17억 달러로, 전년의 총 가치인 약 14억 달러보다 18% 증가할 것으로 예상됩니다. 도로와 고속도로에 더 많은 자금이 투입되면 사업의 중요한 부분인 아스팔트 개질제에 대한 수요도 늘어날 것입니다.

또한 폴란드 중앙통계청은 12월 월간 보고서에서 2022년 폴란드의 아스팔트 총 생산량은 약 164만 톤으로 전년도 생산량인 약 154만 톤보다 약 6% 증가할 것이라고 밝혔습니다.

유럽 아스팔트 포장 협회(EAPA)에 따르면 유럽은 2021년에 약 2억 9,060만 톤의 핫 및 웜 믹스 아스팔트를 생산했습니다. 이는 전년도 생산량보다 1,370만 미터톤이 늘어난 수치입니다. 독일이 전체 생산량의 13% 이상을 차지하며 가장 많은 양을 생산했고, 이탈리아와 프랑스가 그 뒤를 이었습니다.

세계 각지에서 더 많은 고속도로와 도로가 건설됨에 따라 아스팔트 포장에 대한 수요가 증가하여 아스팔트 개질제에 대한 수요도 증가할 것으로 보입니다.

아시아태평양이 시장을 독점

아시아태평양 지역은 중국, 인도, 일본과 같은 국가에서 건설 수요가 확대됨에 따라 아스팔트 개질제 시장을 지배하고 있습니다. 이 지역의 시장 성장은 새로운 공항 활주로 건설과 교통망 확장에 의해 촉진되고 있습니다.

중국 정부가 산업 및 서비스 부문의 확장을 견디기 위해 철도 및 도로 인프라를 대폭 개발하면서 지난 몇 년간 부동산 부문의 불안정한 성장에도 불구하고 최근 몇 년간 중국 건설 산업이 크게 성장했습니다.

중국은 도로 개발 및 유지 보수에 대한 투자를 두 배로 늘렸습니다. 또한 중국은 현재 진행 중이거나 예정된 여러 도로 및 고속도로 건설 프로젝트가 있습니다. 쩡청-포산 고속도로는 중국 광둥성에서 2,376만 달러 규모의 프로젝트로, 쩡청에서 톈허 구간까지 38.4km의 고속도로를 건설하는 프로젝트입니다. 2021년 3분기에 공사가 시작되어 2025년 4분기에 완공될 예정입니다.

한편, 인도는 580만 킬로미터가 넘는 도로를 보유하고 있어 세계에서 두 번째로 큰 도로 시스템을 보유하고 있으며, 도로교통 및 고속도로부는 2022-2023년 연합 예산에서 INR 199,107.71억(미화 260.04억 달러)을 배정받았습니다.

또한 인도 브랜드 자산 재단은 인도국도청(NHAI)이 2022-2023년에 하루 50킬로미터의 속도로 25,000킬로미터의 국도를 건설할 계획이라고 보고했습니다. 또한, NHAI는 인프라 투자 신탁을 통해 40,000억 루피(57억 2,000만 달러)를 조달하여 고속도로 자산(InvIT)을 수익화할 계획입니다.

일본 국토교통성(MLIT)에 따르면 2021 회계연도 일본의 건설용 아스팔트 국내 수요는 약 106만 톤이었습니다. 이는 이전 회계연도의 약 120만 톤에서 감소한 수치입니다.

프로젝트 실행 속도는 향후 몇 년 동안 더 빨라질 것으로 보입니다. 이 지역의 도로 및 고속도로 인프라 개발에 대한 투자는 예측 기간 동안 증가할 것으로 예상됩니다. 전반적으로 이러한 투자와 개발이 아시아 태평양 지역의 아스팔트 개질제 시장을 견인할 것으로 예상됩니다.

아스팔트 개질제 산업 개요

아스팔트 개질제 시장은 부분적으로 통합되어 주요 기업이 큰 점유율을 차지하고 있습니다. 아스팔트 개질제 시장의 주요 기업에는 DuPont, BASF SE, Arkema, Nouryon, Dow 등이 포함됩니다(특정한 순서 없음).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

높은 교통량과 무거운 하중

초절전 설계 사양 충족에 대한 강조

포장 작업 수명 증가 및 MRO 비용 절감 이점

억제요인

개질 아스팔트 시멘트를 사용에 대한 높은 초기 비용

아스팔트와 관련된 산업 보건 위험

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

규제 시책

제5장 시장 세분화(금액 기준 시장 규모)

용도

포장

지붕

기타

최종 사용자 산업

물리적 개질제

플라스틱

고무

기타 물리적 개질제

화학 개질제

섬유

접착성 향상제

증량제

충전제

산화 방지제

스트립 방지제

기타

지역

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

카타르

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 시장 순위 분석

주요 기업의 전략

기업 프로파일

Arkema

ArrMaz Products, Inc.

BASF SE

Cargill

Dow

DuPont

Engineered Additives LLC

Evonik Industries AG

Exxon Mobil Corporation

Genan Holding A/S

Honeywell International Inc.

Kao Corporation

Kraton Corporation

McAsphalt Industries Limited

Nouryon

PQ Corporation

Sasol

제7장 시장 기회와 앞으로의 동향

HMA(핫믹스 아스팔트)에의 선호도 증가

재생 아스팔트 포장(RAP)의 인기 증가

바이오 재생 가능한 개질제의 개발

웜믹스 아스팔트 기술의 진보

아스팔트 개질에 나노 기술을 접목하기 위한 연구(나노 클레이)

HBR

영문 목차

영문목차

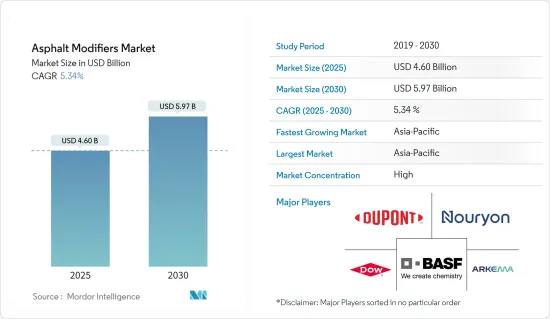

The Asphalt Modifiers Market size is estimated at USD 4.60 billion in 2025, and is expected to reach USD 5.97 billion by 2030, at a CAGR of 5.34% during the forecast period (2025-2030).

COVID-19 had a major impact on the manufacturing industry, thus hampering market growth. However, the industries have since recovered from the pandemic. Since then, the construction industry's steady growth has been the market's main driver.

Key Highlights

During the forecast period, the demand for the market is likely to be driven by things like more traffic and heavier loads on roads, a focus on meeting super-save design specifications, longer pavement life, and lower MRO costs.

On the other hand, the high cost of using modified asphalt cement and the health risks of working with asphalt are likely to slow the growth of the market.

Future opportunities for the market are expected to come from the growing demand for HMA (Hot Mix Asphalt), the growing popularity of RAP (Reclaimed Asphalt Pavement), the development of bio-renewable modifiers, the improvement of warm mix asphalt technologies, and research into using nanotechnology to change asphalt (Nano-Clay).

Due to the high demand for asphalt, the Asia-Pacific region has been the most important and will continue to grow over the next few years.

Asphalt Modifiers Market Trends

Increasing Demand from Paving Application

Mixtures of asphalt and concrete have been used a lot to build roads, airport runways, taxiways, and bike lanes, among other things. Binder modifiers (like polymers, elastomers, fibers, and rubber) and aggregate modifiers (like lime, granulated rubber, and anti-strip agents) are used to improve the performance of asphalt pavements by making them more resistant to problems like thermal cracking, rutting, stripping, and so on. This makes the pavement last longer.

In recent years, the global demand for asphalt modifiers has been witnessing above-average growth. The demand for asphalt modifiers has a direct correlation with the level of ongoing road construction activities around the world.

According to the US Census Bureau, the value of federal highway and street construction put in place in the United States in 2022 will be around USD 1.7 billion, representing an increase of 18% over the previous year's total value of approximately USD 1.4 billion. With more money going into roads and highways, there would be more demand for asphalt modifiers, which are an important part of the business.

The Central Statistical Office of Poland in its December monthly report also stated that the total production of asphalt in Poland in 2022 was about 1.64 million metric tons, about 6% more than the previous year's production value of about 1.54 million metric tons.

According to the European Asphalt Pavement Association (EAPA), Europe made about 290.6 million metric tons of hot and warm mix asphalt in 2021. This is just 13.7 million metric tons more than what was made the year before. Germany produced the most, making up over 13% of the total output, followed by Italy and France.

With more highways and roads being built in different parts of the world, this is likely to increase the demand for asphalt pavements, which will in turn increase the demand for asphalt modifiers.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region dominated the asphalt modifier market as a result of the expanding need for construction in nations like China, India, and Japan. Market growth in the area is being fueled by the construction of new airport runways and transportation expansions.

The significant development of rail and road infrastructure by the Chinese government to withstand the expanding industrial and service sectors has resulted in significant growth of the Chinese construction industry in recent years, despite the volatile growth in the real estate sector in the last couple of years.

China has doubled its investment in road development and maintenance. Furthermore, the country has several present and prospective road and highway construction projects. The Zengcheng-Foshan Expressway is a USD 2,376 million project in Guangdong, China, that involves the construction of a 38.4-km highway from Zengcheng to Tianhe Section. Construction began in the third quarter of 2021 and is scheduled to finish in the fourth quarter of 2025.

India, on the other hand, has over 5.8 million kilometers of roads, which makes it the second-largest road system in the world.The Ministry of Road Transport and Highways has been given INR 199,107.71 crore (USD 26.04 billion) in the Union Budget 2022-23.

Furthermore, the India Brand Equity Foundation reports that the National Highway Authority of India (NHAI) intends to build 25,000 kilometers of national highways in 2022-23 at a rate of 50 kilometers per day. In addition, NHAI intends to raise INR 40,000 crore (USD 5.72 billion) through an infrastructure investment trust to monetize its motorway assets (InvIT).

According to the Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), Japan's domestic demand for asphalt for construction in fiscal year 2021 was about 1.06 million metric tons. This was down from about 1.2 million tons in the prior fiscal year.

The pace of project execution is likely to increase further in the coming years. Investments in the development of roads and highway infrastructure in the region are anticipated to rise during the forecast period. Overall, such investments and development are expected to drive the asphalt modifiers market in the Asia-Pacific region.

Asphalt Modifiers Industry Overview

The asphalt modifiers market is partially consolidated, with the top players having a significant share of the market. Key players in the asphalt modifiers market include (not in any particular order) DuPont, BASF SE, Arkema, Nouryon, and Dow, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 High Traffic Volume and Heavier Loads

4.1.2 Emphasis on Meeting Super-save Design Specifications

4.1.3 Increased Pavement Work-life and Reduced MRO Cost Advantages

4.2 Restraints

4.2.1 High Initial Cost for Using Modified Asphalt Cement

4.2.2 Occupational Health Hazards Regarding Asphalt

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Regulatory Policy

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Application

5.1.1 Paving

5.1.2 Roofing

5.1.3 Other Applications

5.2 End-user Industry

5.2.1 Physical Modifiers

5.2.1.1 Plastics

5.2.1.2 Rubbers

5.2.1.3 Other Physical Modifiers

5.2.2 Chemical Modifiers

5.2.3 Fibers

5.2.4 Adhesion Improvers

5.2.5 Extenders

5.2.6 Fillers

5.2.7 Antioxidants

5.2.8 Anti-strip Modifiers

5.2.9 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Australia

5.3.1.6 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East & Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Qatar

5.3.5.4 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements