ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

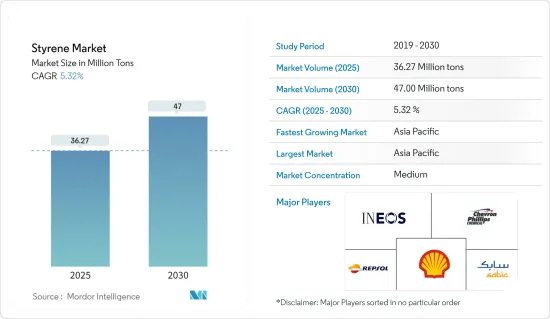

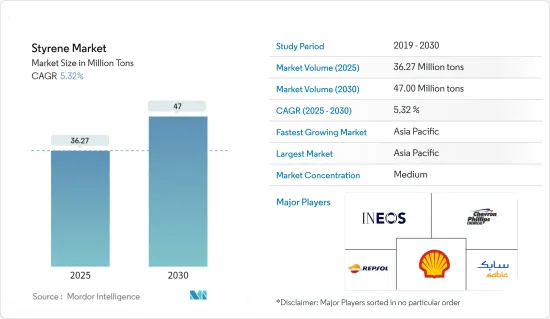

스티렌 시장 규모는 2025년에 3,627만 톤으로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 5.32%로, 2030년에는 4,700만 톤에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 스티렌 시장에 부정적인 영향을 미쳤습니다. 그러나 포장, 건설, 자동차 등 다양한 산업에서의 소비 증가로 시장은 2021년에 크게 회복되었습니다.

주요 하이라이트

단기적으로 소비자 가전 산업의 수요 증가는 연구 대상 시장의 성장을 이끄는 주요 요인입니다.

그러나 포장 산업에서 바이오 플라스틱의 사용 증가는 시장 성장을 억제할 가능성이 높습니다.

바이오 폴리스티렌을 개발하기 위한 연구가 진행되고 있으며, 세계 시장에 수익성있는 성장 기회를 창출 할 것입니다.

아시아태평양이 스티렌 시장을 독점하고 있으며, 가장 큰 소비국은 중국, 일본, ASEAN 국가 등입니다.

스티렌 시장 동향

포장산업이 시장을 견인

스티렌은 유리한 특성으로 인해 포장 산업에서 일반적으로 사용됩니다. 스티렌은 투명도, 내충격성, 단열성이 뛰어난 다용도 경량 플라스틱입니다. 이러한 특성 덕분에 다양한 포장 용도에 적합합니다.

포장 산업에서 스티렌의 가장 일반적인 용도 중 하나는 발포 폴리스티렌(EPS) 또는 스티로폼이라고도 하는 폴리스티렌 폼을 생산하는 것입니다. EPS 폼은 완충재, 부패하기 쉬운 상품의 단열재, 경량 배송 컨테이너 등 보호 포장에 널리 사용됩니다.

스티렌은 식품 포장에 일반적으로 사용되는 경질 폴리스티렌을 생산하는 데도 사용됩니다. 클램쉘, 컵, 트레이와 같은 투명 폴리스티렌 용기는 고객이 내용물을 쉽게 확인할 수 있어 식품 서비스 업계에서 인기가 높습니다.

또한, 폴리스티렌은 의료 및 헬스케어 산업에서도 다양한 포장 용도로 사용되고 있으며, IQVIA에 따르면 최근 몇 년간 전 세계 제약 시장이 크게 성장했습니다. 2022년까지 전 세계 제약 시장의 총 규모는 1조 4,800억 달러에 달할 것으로 예상됩니다. 이는 1조 4,200억 달러 규모였던 2021년에 비해 소폭 증가한 수치입니다.

아시아태평양에서는 라이프스타일 변화, 가처분 소득 증가, 직장인 수 증가, 패스트푸드 선호도 증가로 인해 포장 식품에 대한 수요가 증가하고 있습니다.

중국은 1인당 소득 증가와 중국 내 거대 이커머스 기업의 성장 등의 요인으로 인해 전 세계에서 가장 큰 포장재 소비국입니다. 인도의 포장 산업은 세계에서 5번째로 큰 규모이며, 인도 플라스틱 산업 협회에 따르면 매년 약 22-25%씩 성장하고 있습니다. 고도로 숙련된 노동력과 저렴한 인건비 덕분에 식품 포장 및 가공 비용은 유럽보다 40% 낮습니다. 인구 증가와 포장에 대한 수요 증가가 시장을 견인할 것으로 예상됩니다.

마찬가지로 2022년 유럽 식음료 산업은 460만 명의 직원을 고용하고 1조 1,000억 유로(1조 1,590억 달러)의 매출과 2,300억 유로(2,423억 7,000만 달러)의 부가가치를 창출하여 유럽에서 가장 큰 제조업 중 하나가 될 것입니다. 따라서 이 지역의 식음료 산업이 성장함에 따라 식품 포장에 대한 수요가 증가하고 있으며 연구 대상 시장도 확대되고 있습니다.

독일 통계청에 따르면 독일 포장 산업의 매출은 2022년 354억 4천만 유로(377억 1천만 달러)에 달하며 전년 대비 성장세를 기록했습니다.

이러한 요인은 포장 부문의 연구 대상 시장에 대한 수요를 뒷받침할 것으로 보입니다.

아시아태평양이 시장을 독점할 전망

아시아태평양이 시장을 독점하고 있으며 예측 기간 동안에도 그 지배는 계속 될 것으로 보입니다.

이 지역의 패키징 용도의 증가, 전기 및 전자 제품에 대한 견고한 수요, 자동차 및 운송 부문의 급속한 성장이 스티렌 시장을 적극적으로 활성화하고 있습니다.

ZEVI에 따르면 2021년 아시아 전기전자 시장 규모는 10% 증가한 3조 1,100억 유로(3조 6,700억 달러)에 달했습니다. 2022년에는 수요가 13% 증가했으며 2023년에는 7%의 성장률을 기록할 것으로 예상됩니다. 중국 시장은 세계에서 가장 큰 시장으로, 모든 선진국 시장을 합친 것보다 훨씬 더 큰 규모입니다. 2021년 중국 시장은 세계 시장의 41.6%인 2조 7,700억 유로(2조 4,500억 달러)를 차지했으며, 중국 전자 산업은 2022년에 14% 성장했고 2023년에는 8% 성장할 것으로 예상됩니다.

중국자동차제조협회(CAAM)에 따르면 중국은 세계에서 가장 큰 자동차 생산 기지를 보유하고 있으며, 2022년 총 자동차 생산량은 2,700만 대로 작년 2,600만 대에 비해 3.4% 증가할 것으로 예상됩니다.

중국은 세계 주요 패키징 산업 중 하나입니다. 중국은 맞춤형 포장의 증가와 식품 부문의 포장 소비재 수요 증가로 인해 예측 기간 동안 지속적인 성장을 보일 것으로 예상됩니다. Interpak에 따르면 중국의 식료품 포장 부문에서 2023년 총 포장재는 4470억 개에 달할 것으로 예상됩니다.

업계 발표에 따르면 2021-2022년에 시노펙 구레이, 저장 석유화학, 산둥 리화야와 같은 기업의 신규 시설을 포함해 총 350만 톤 이상의 폴리스티렌 및 ABS 플라스틱 공장이 가동될 것으로 예상되었습니다. 그러나 중국의 에너지 위기로 인해 지연될 수 있습니다.

마찬가지로 인도 포장 산업 협회(PIAI)에 따르면 인도 포장 산업은 예측 기간 동안 22%의 성장률을 보일 것으로 예상됩니다. 또한 인도 패키징 시장은 2025년까지 2,481억 달러에 달할 것으로 예상되며, 2020년부터 2025년까지 26.7%의 연평균 성장률을 기록할 것으로 전망됩니다. 따라서 플라스틱 사출 성형 시장은 이 지역에서 성장할 것으로 예상됩니다.

일본의 전자정보기술산업협회(JEITA)에 따르면 전 세계 전자 및 IT 산업의 생산량은 2022년 3조 4,400억 달러로 2021년 3조 3,600억 달러에 비해 1%의 성장률을 기록할 것으로 추정됩니다.

따라서 위에서 언급한 요인들은 이 지역의 다양한 최종 사용자로부터 스티렌에 대한 수요가 증가하고 있음을 나타냅니다.

스티렌 산업 개요

조사한 시장은 주요 기업에 의해 부분적으로 세분화됩니다. 주요 기업(특정한 순서 없음)에는 Shell PLC, Chevron Phillips Chemical Company LLC, SABIC, Repsol, INEOS 등이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

소비자용 전자기기 산업에서의 수요 증가

포장 산업에서의 수요 증가

기타 촉진요인

억제요인

포장 산업에서 바이오 플라스틱의 사용 증가

기타 억제요인

산업의 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(수량 기준 시장 규모)

제품 유형

폴리스티렌

아크릴로니트릴, 부타디엔, 스티렌

스티렌 부타디엔 고무

기타 제품 유형(스티렌, 아크릴로니트릴)

최종 사용자 산업

포장

건축

소비재

자동차 및 운송

전기 및 전자

기타 최종 사용자 산업(섬유)

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

남아프리카

사우디아라비아

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

Chevron Phillips Chemical Company

Covestro AG

한화그룹

INEOS(INEOS Styrolution)

LG Chem

LyondellBasell Industries Holdings BV

Reliance Industries Ltd

Repsol

SABIC

Shell PLC

Versalis SpA(Eni SpA)

제7장 시장 기회와 앞으로의 동향

바이오 기반 폴리스티렌 개발을 위한 연구 진행 중

기타 기회

HBR

영문 목차

영문목차

The Styrene Market size is estimated at 36.27 million tons in 2025, and is expected to reach 47.00 million tons by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the styrene market. However, the market recovered significantly in 2021, owing to rising consumption of various industries, such as packaging, construction, automotive, and others.

Key Highlights

Over the short term, the growing demand from the consumer electronics industry is a major factor driving the growth of the market studied.

However, increasing usage of bio-based plastics in the packaging industry is likely to restrain the growth of the market.

Nevertheless, ongoing research to develop bio-based polystyrene is likely to create lucrative growth opportunities for the global market soon.

The Asia-Pacific region dominates the styrene market, with the largest consumption coming from countries such as China, Japan, ASEAN countries, etc.

Styrene Market Trends

Packaging Industry to Drive the Market

Styrene is commonly used in the packaging industry due to its favorable properties. It is a versatile, lightweight plastic with excellent clarity, impact resistance, and thermal insulation. These characteristics make it suitable for a wide range of packaging applications.

One of the most common uses of styrene in the packaging industry is in producing polystyrene foam, often referred to as expanded polystyrene (EPS) or Styrofoam. EPS foam is widely used for protective packaging, including cushioning materials, insulation for perishable goods, and lightweight shipping containers.

Styrene is also used to produce rigid polystyrene, which is commonly employed in food packaging. Clear polystyrene containers, such as clamshells, cups, and trays, are popular in the food service industry due to their transparency, allowing customers to view the contents easily.

Furthermore, polystyrene is also used in the medical and healthcare industries for various packaging applications; IQVIA shows that the global pharmaceutical market has grown significantly in recent years. The total global pharmaceutical market was valued at USD 1.48 trillion by 2022. This is only a slight increase from 2021 when the market was valued at USD 1.42 trillion.

In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food.

China is the world's largest packaging consumer across the world owing to the factors such as growing per capita income, coupled with rising e-commerce giants in the country. India's packaging industry is the fifth-largest in the world, and it is growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

Similarly, in 2022, the Europe food and beverages industry employs 4.6 million people and generates EUR 1.1 trillion (USD 1.159 trillion) in revenue and EUR 230 billion (USD 242.37 billion) in value-added, making it one of the largest manufacturing industries in Europe. Thereby, the growing food and beverages industry in the region is increasing the demand for food packaging, as well as boosting the market studied.

According to Statistisches Bundesamt, the revenue of the packaging industry in Germany has reached EUR 35.04 billion (USD 37.71 billion) in 2022 and has registered growth when compared to previous years.

Such factors are likely to support the demand for the studied market from the packaging segment.

Asia-Pacific is Expected to Dominate the Market

Asia-Pacific dominated the market and will likely continue its dominance during the forecast period.

Increasing packaging applications across the region, robust demand for electrical and electronic products, and the rapid growth of automotive and transportation sectors are actively boosting the styrene market.

According to ZEVI, the Asian electro market reached EUR 3.11 trillion (USD 3.67 trillion) in 2021, a 10% rise. The demand increased by 13% in 2022 and estimated a 7% growth rate for 2023. China's market is the largest in the world, even more significant than the combined markets of all industrialized countries. In 2021, the Chinese market contributed EUR 2.07 trillion (USD 2.45 trillion), or 41.6% of the world market; additionally, the Chinese electronic industry expanded by 14% in 2022, and the sector is expected to grow by 8% in 2023.

According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year.

China is one of the key packaging industries in the world. The country is expected to witness consistent growth during the forecast period due to the rise of customized packaging and increased demand for packaged consumer goods in the food segment. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023.

According to industry publications, in 2021-2022, new factories for polystyrene and ABS plastics were expected to launch with a combined capacity of over 3.5 million tons, including new facilities for companies like Sinopec Gulei, Zhejiang Petrochemical, and Shandong Lihuaya. However, a delay may be observed due to the energy crisis in the country.

Similarly, according to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the plastic injection molding market is expected to grow in the region.

Considering electronics, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021.

Thus, the abovementioned factors indicate the rising demand for styrene from various end users in the region.

Styrene Industry Overview

The market studied is partially fragmented among the top players. The key players (not in any particular order) include Shell PLC, Chevron Phillips Chemical Company LLC, SABIC, Repsol, and INEOS, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rising Demand from the Consumer Electronics Industry

4.1.2 Increasing Demand from Packaging Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Increasing Usage of Bio-based Plastics in the Packaging Industry

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Polystyrene

5.1.2 Acrylonitrile Butadiene Styrene

5.1.3 Styrene Butadiene Rubber

5.1.4 Other Product Types (Styrene-Acrylonitrile)

5.2 End-user Industry

5.2.1 Packaging

5.2.2 Construction

5.2.3 Consumer Goods

5.2.4 Automotive and Transportation

5.2.5 Electrical and Electronics

5.2.6 Other End-user Industries (Textile)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 South Africa

5.3.5.2 Saudi Arabia

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Chevron Phillips Chemical Company

6.4.2 Covestro AG

6.4.3 Hanwha Group

6.4.4 INEOS (INEOS Styrolution)

6.4.5 LG Chem

6.4.6 LyondellBasell Industries Holdings BV

6.4.7 Reliance Industries Ltd

6.4.8 Repsol

6.4.9 SABIC

6.4.10 Shell PLC

6.4.11 Versalis SpA (Eni SpA)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Ongoing Research to Develop Bio-based Polystyrene