ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

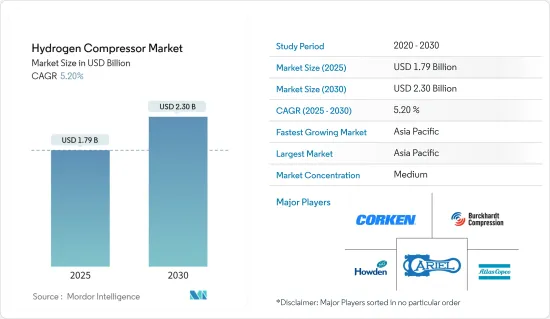

수소 압축기 시장 규모는 2025년에 17억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 5.2%로, 2030년에는 23억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

비료 및 정유소와 같은 최종 사용자 산업의 수소 수요 증가, 운송을 위한 전 세계 수소 파이프라인 인프라 구축 증가와 같은 요인이 예측 기간 동안 수소 압축기 시장을 견인할 것으로 예상됩니다

반면에 제조업 활동과 글로벌 무역의 급격한 감소로 인한 산업 및 경제 활동의 둔화, 관세 인상 및 무역 정책 불확실성 장기화는 수소를 사용하는 산업의 자본재 수요를 감소시켜 연구 대상 시장의 성장을 억제 할 것으로 예상됩니다.

그럼에도 불구하고 태양열 및 풍력과 같은 청정 에너지원과 함께 전기분해를 이용한 수소 생산 기술 발전과 새로운 에너지원은 시장 성장에 충분한 기회를 제공할 것으로 보입니다.

예측 기간 동안 아시아태평양은 수소 압축기 시장을 독점할 것으로 예상되며, 수요의 대부분은 중국, 인도, 일본에서 발생할 것으로 전망됩니다.

수소 압축기 시장 동향

시장을 독점하는 오일 기반 부문

오일 기반 윤활식 압축기는 오일 프리 압축기보다 비용이 저렴하고 수명이 더 깁니다. 오일 오염의 결과가 매우 심각하여 오일 프리 압축기가 필수인 산업에서 사용하는 경우를 제외하고는 상업용 및 산업용에 이상적인 것으로 간주됩니다.

오일 기반 압축기는 오일이 냉각 매체 역할을 하여 압축 과정에서 압축기 열의 약 80%를 제거하므로 오일 프리 압축기보다 더 효율적인 것으로 간주됩니다. 또한 높은 압축비가 요구되는 산업용으로 더 적합한 것으로 간주됩니다.

자본 지출 측면에서 윤활식 오일 기반 압축기는 종종 오일 프리 압축기보다 저렴한 것으로 간주되며, 가격 차이는 30-40% 범위에서 차이가 나는 경우가 많습니다. 용량 및 산업별 요구 사항과 같은 요인에 따라 50%에 이를 수도 있으며, 이로 인해 오일 기반 수소 압축기에 대한 수요가 증가합니다.

오일 기반 압축기는 오일 프리 압축기보다 저렴하지만 지속적인 유지보수가 필요하고 오일 누출 위험을 없애기 위해 필터 및 기타 구성품을 교체하는 데 더 많은 주의가 필요합니다. 지속적인 오일 오염은 제품 변질 또는 안전하지 않은 제품, 생산 중단 시간, 법적 문제 등 심각한 결과를 초래할 수 있습니다.

오일 기반 수소 압축기는 주로 유리 정제, 철강 산업, 반도체 제조, 발전소의 용접, 어닐링, 금속 열처리(발전기 냉각수), 항공우주 분야, 제약 등의 제조 산업에서 선호되고 있습니다.

미국 지질조사국에 따르면 2023년 미국의 철강 원재료 생산량은 8천만 톤으로 추정됩니다. 미국 철강 산업의 2023년 조강 생산액은 약 1,100억 달러로 2022년 1,280억 달러에서 15% 감소할 것으로 예상됩니다. 산업화가 증가함에 따라 철강 생산량은 계속 증가할 수 있으며, 이는 석유 기반 수소 압축기에 대한 수요를 창출할 수 있습니다.

또한 세계철강협회에 따르면 철강 수요는 2024년에 1.7% 증가하고 2025년에는 1.2% 성장하여 1,815백만 톤에 달할 것으로 예상됩니다. 따라서 철강 수요의 증가는 향후 시장의 성장을 견인할 것입니다.

불충분한 윤활은 수소 압축기 부품의 조기 마모를 지속적으로 위협하며, 이는 오일 기반 수소 압축기의 유지 보수 비용을 증가시키고 수요를 제한 할 수 있습니다.

이러한 요인으로부터 예측기간 동안 오일 기반 유형의 수소 압축기가 시장을 독점할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양 지역은 중국, 일본, 인도와 같은 국가의 우호적인 정부 정책으로 인해 향후 몇 년 동안 연료 전지의 유망한 시장이 될 것으로 예상됩니다.

중국은 세계에서 가장 크고 빠르게 성장하는 수소 압축기 시장 중 하나입니다. 중국은 최근 몇 년 동안 화학, 석유, 가스 및 제조 부문에서 상당한 성장을 목격했습니다.

수소 원심 압축기는 에틸렌 플랜트와 같은 정유 및 석유화학 산업에서 크랙가스 압축 및 냉동 서비스에 사용됩니다. 에틸렌과 벤젠 생산 부족으로 인해 중국은 에틸렌과 벤젠 생산 능력을 늘리는 데 투자하고 있습니다.

또한 여러 압축기 회사들이 압축기 시장을 확대하기 위해 아시아 국가에 투자하고 있습니다. 예를 들어, 2024년 4월, PDC Machines와 Kirloskar Pneumatic Company Limited는 인도 전역에 수소 압축 솔루션을 제공하기로 합의했습니다. 이 계약에 따라 PDC는 인도 현지 수소 시장을 지원하여 KPCL의 기존 고객 기반을 활용하여 아시아 시장에서의 영향력을 확대할 것입니다. 이를 통해 이 지역에서 수소 압축기 시장의 중요성이 더욱 커질 것입니다.

수소 연료전지 차량의 개발과 수소 연료전지 차량에 충전하기 위한 수소 연료 스테이션의 건설을 목표로 하는 일본의 움직임은 수소 압축기 시장을 견인할 것으로 예상됩니다.

예를 들어, AIRIA(일본)에 따르면 2023년 3월 현재 일본에서는 2015년 200대 미만이었던 연료전지 전기차가 74만 7천 대가 사용 중이며, 이는 2015년보다 증가한 수치입니다. 이 차량의 대부분은 주로 수소 연료 승용차였습니다. 이는 예측 기간 동안 수소 연료 충전소용 수소 압축기에 대한 수요를 견인할 것으로 예상됩니다.

따라서 이러한 요인으로 인해 예측 기간 동안 아시아태평양이 수소 압축기 시장을 독점할 것으로 예상됩니다.

수소 압축기 산업 개요

수소 압축기 시장은 적당히 세분화됩니다. 주요 기업으로는 Corken Inc., Ariel Corporation, Burckhardt Compression AG, Howden Group Ltd, Atlas Copco Group 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

최종 사용자 산업에서 수소 수요 증가

수송용 수소 파이프라인 인프라 도입 증가

억제요인

제조 활동과 세계 무역의 급격한 감소에 의한 산업, 경제 활동의 둔화

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

기술

단단식

다단식

유형

오일

오일 프리

최종 사용자 산업

화학

석유 및 가스

기타

시장 분석 : 2028년까지 시장 규모와 수요 예측(지역별)

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

이탈리아

러시아

노르딕

스페인

기타 유럽

아시아태평양

인도

중국

일본

호주

말레이시아

인도네시아

태국

기타 아시아태평양

중동 및 아프리카

사우디아라비아

남아프리카

카타르

아랍에미리트(UAE)

나이지리아

이집트

기타 중동 및 아프리카

남미

브라질

아르헨티나

콜롬비아

기타 남미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Corken Inc.

Ariel Corporation

Burckhardt Compression AG

Hydro-Pac Inc.

Haug Kompressoren AG

Sundyne Corp.

Howden Group Ltd

Indian Compressors Ltd

Atlas Copco Group

Ingersoll Rand Inc.

시장 랭킹, 점유율 분석

제7장 시장 기회와 앞으로의 동향

수소 제조의 기술적 진보와 새로운 공급원

HBR

영문 목차

영문목차

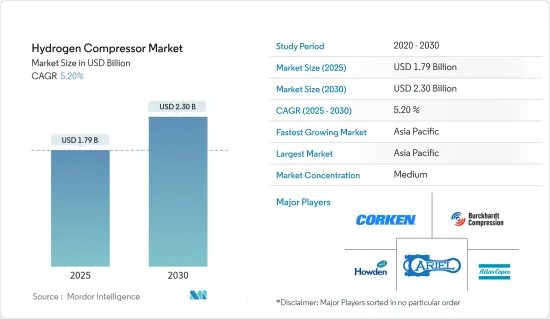

The Hydrogen Compressor Market size is estimated at USD 1.79 billion in 2025, and is expected to reach USD 2.30 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

Factors such as the increase in demand for hydrogen from end-user industries, such as fertilizers and oil refineries, and increasing deployment of hydrogen pipeline infrastructure globally for transportation are expected to drive the hydrogen compressor market during the forecast period.

On the other hand, the slowdown in industrial and economic activities due to a sharp decline in manufacturing activity and global trade, with higher tariffs and prolonged trade policy uncertainty, is expected to decrease the demand for capital goods from industries using hydrogen, thereby restraining the growth of the market studied.

Nevertheless, the technological advancements and emerging sources for hydrogen production using electrolysis in combination with cleaner sources, such as solar and wind, are likely to provide ample opportunities for the market's growth.

Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period, with the majority of the demand coming from China, India, and Japan.

Hydrogen Compressor Market Trends

Oil-based Segment Expected to Dominate the Market

Oil-based lubricated compressors cost less and provide a longer service life than oil-free compressors. They are considered ideal for commercial and industrial applications until and unless they are used in industries where the consequences of oil contamination are considered very high and having an oil-free compressor is a must.

Oil-based compressors are considered more efficient than oil-free compressors, as oil acts as a cooling medium, taking out approximately 80% of the compressor's heat during the compression process. They are also considered more suitable for industrial usage with requirements of a high compression ratio.

In terms of capital outlay, lubricated oil-based compressors are often considered less expensive than oil-free compressors, with price differences often varying in the range of 30-40%. It may even reach 50%, depending upon factors such as capacity and industry-specific requirements, resulting in increased demand for oil-based hydrogen compressors.

Although oil-based compressors are more affordable than oil-free compressors, they require continuous maintenance and greater attention to replacing filters and other components used to eliminate the risk of oil leakage. Ongoing oil contamination may result in severe consequences, such as spoiled or unsafe products, production downtime, and legal issues.

Oil-based hydrogen compressors are mostly preferred in the manufacturing industry for glass purification, iron and steel industry, semiconductor manufacturing, welding, annealing, and heat-treating metals in power plants (coolant for generators), aerospace applications, pharmaceuticals, etc.

According to the United States Geological Survey, in 2023, raw steel production in the United States was estimated to be 80 million metric tons. The US iron and steel industry produced raw steel in 2023 with an estimated value of about USD 110 billion, a 15% decrease from USD 128 billion in 2022. With the increasing industrialization, steel production may continue to increase, which, in turn, may create demand for oil-based hydrogen compressors.

Furthermore, according to the World Steel Association, steel demand is expected to increase by 1.7% in 2024 and grow by 1.2% in 2025 to reach 1,815 million tonnes. Thus, the increase in demand for steel will drive the market's growth in the future.

Insufficient lubrication persistently threatens premature wear of hydrogen compressor components, which may increase the maintenance cost of oil-based hydrogen compressors and limit their demand.

Therefore, based on such factors, the oil-based type segment is expected to dominate the hydrogen compressor market during the forecast period.

Asia-Pacific Expected to Dominate the Market

Asia-Pacific is expected to be a promising market for fuel cells in the coming years because of the favorable government policies in countries such as China, Japan, and India.

China is one of the world's largest and fastest-growing hydrogen compressor markets. The country has witnessed significant growth in its chemical, oil, gas, and manufacturing sectors in recent years.

Hydrogen centrifugal compressors are used in refining and petrochemical industries, such as ethylene plants, for cracked-gas compression and refrigeration services. Due to ethylene and benzene production shortages, China has been investing in increasing its ethylene and benzene production capacities.

Furthermore, several compressor companies are investing in Asian countries to expand the compressor market. For instance, in April 2024, PDC Machines and Kirloskar Pneumatic Company Limited agreed to provide hydrogen compression solutions throughout India. As per the agreement, PDC will support the local Indian hydrogen market, amplifying its reach in Asia by leveraging KPCL's existing customer base. This will boost the significance of the hydrogen compressor market in the region.

The development of hydrogen fuel cell vehicles and Japan's aim to build hydrogen fuel stations for recharging the vehicles are expected to drive the hydrogen compressor market.

For instance, according to AIRIA (Japan), as of March 2023, 7.47 thousand fuel-cell electric vehicles were in use in Japan, increasing from less than 200 in 2015. The majority of these vehicles were primarily hydrogen-fueled passenger cars. This, in turn, is expected to drive the demand for hydrogen compressors for hydrogen fuel stations during the forecast period.

Therefore, based on such factors, Asia-Pacific is expected to dominate the hydrogen compressor market during the forecast period.

Hydrogen Compressor Indsutry Overview

The hydrogen compressor market is moderately fragmented. Some of the major companies include (in no particular order) Corken Inc., Ariel Corporation, Burckhardt Compression AG, Howden Group Ltd, and Atlas Copco Group.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increase in Demand for Hydrogen from End-user Industries

4.5.1.2 Increasing Deployment of Hydrogen Pipeline Infrastructure for Transportation

4.5.2 Restraints

4.5.2.1 The Slowdown in Industrial and Economic Activities Due to a Sharp Decline in Manufacturing Activity and Global Trade

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Technology

5.1.1 Single-stage

5.1.2 Multistage

5.2 Type

5.2.1 Oil-based

5.2.2 Oil-free

5.3 End-user Industry

5.3.1 Chemical

5.3.2 Oil and Gas

5.3.3 Other End-user Industries

5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (For Regions Only)})

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 United Kingdom

5.4.2.3 France

5.4.2.4 Italy

5.4.2.5 Russia

5.4.2.6 NORDIC

5.4.2.7 Spain

5.4.2.8 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 India

5.4.3.2 China

5.4.3.3 Japan

5.4.3.4 Australia

5.4.3.5 Malaysia

5.4.3.6 Indonesia

5.4.3.7 Thailand

5.4.3.8 Rest of Asia-Pacific

5.4.4 Middle East and Africa

5.4.4.1 Saudi Arabia

5.4.4.2 South Africa

5.4.4.3 Qatar

5.4.4.4 United Arab Emirates

5.4.4.5 Nigeria

5.4.4.6 Egypt

5.4.4.7 Rest of Middle East and Africa

5.4.5 South America

5.4.5.1 Brazil

5.4.5.2 Argentina

5.4.5.3 Colombia

5.4.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Corken Inc.

6.3.2 Ariel Corporation

6.3.3 Burckhardt Compression AG

6.3.4 Hydro-Pac Inc.

6.3.5 Haug Kompressoren AG

6.3.6 Sundyne Corp.

6.3.7 Howden Group Ltd

6.3.8 Indian Compressors Ltd

6.3.9 Atlas Copco Group

6.3.10 Ingersoll Rand Inc.

6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Advancements and Emerging Sources for Hydrogen Production