ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

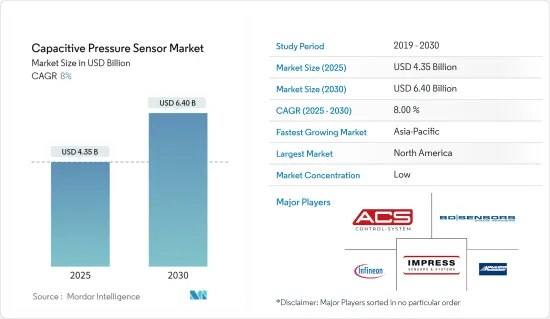

정전식 압력 센서 시장 규모는 2025년에 43억 5,000만 달러로 추정되며, 예측기간 중(2025-2030년)의 연평균 성장율(CAGR)은 8%로, 2030년에는 64억 달러에 달할 것으로 예측되고 있습니다.

주요 하이라이트

정전식 셀이 장착된 압력 센서는 기존 장비에 고유하고 정확한 결과를 제공하도록 설계되었습니다. 세라믹 소재의 뚜렷한 장점 덕분에 센서는 압력에 대한 높은 저항성과 함께 장기적인 안정성과 신뢰성을 제공합니다.

정전식 압력 센서는 뛰어난 감도, 정확도, 마모 문제가 없어 저항식 센싱 기술에 비해 점점 더 인기를 얻고 있습니다. 다양한 뛰어난 기능으로 인해 많은 애플리케이션에서 정전식 센서가 저항식 센서를 점점 더 많이 대체하고 있습니다. 또한 센서 기술의 발전으로 인해 더 작은 센서가 만들어지고 변화하면서 업계 리더들에게 수많은 기회가 생겼습니다.

정전식 압력 센서의 단순하고 견고한 기계적 구조는 여러 산업 분야에 활용될 수 있습니다. 정전식 압력 센서는 세라믹을 사용하기 때문에 열악한 산업 환경에서도 견딜 수 있으며 응답 속도가 더 빠릅니다.

MEMS 기술이 발전함에 따라 정전식 압력 센서의 크기가 작아져 더 많은 산업 분야에서 유용하게 사용되고 있습니다. 정전식 압력 센서의 소형화로 인해 생산 비용이 절감되었습니다. 따라서 정전식 압력 센서 시장은 저렴하고 효율적이며 다양한 응용 분야로 성장하고 있습니다.

또한 자동차, 특히 전기 자동차의 판매량이 작년에 크게 증가했습니다. 이는 앞으로 더욱 증가할 것으로 예상되며, 정전식 압력 센서 시장에도 영향을 미칠 것으로 보입니다.

또한 코로나19는 전 세계 각국 정부의 봉쇄 및 기타 규칙과 규제로 인해 시장에 큰 영향을 미쳤습니다. 하지만 팬데믹 이후에는 자동차, 의료, 석유 및 가스, 기타 산업 등 정전식 압력 센서를 사용하는 산업이 빠르게 성장하면서 시장이 크게 성장했습니다.

하지만 진입 장벽이 높지 않아 현재 많은 회사에서 정전식 압력 센서를 제공하고 있습니다. 이로 인해 가격 경쟁이 매우 치열하고 제품 간 차별화가 어려워 시장 성장이 둔화되고 있습니다.

정전식 압력 센서 시장 동향

자동차 부문이 대폭적인 시장 성장을 이룰 전망

자동차에 사용할 압력 센서를 설계하고 제작할 때 가장 중요한 것 중 하나는 다양한 온도, 진동, 매체, 충격 및 전자기 조건에서 잘 작동해야 한다는 것입니다. 즉, 센서가 제 역할을 할 수 있을 만큼 내구성이 뛰어나야 합니다.

자율주행차나 전기 자동차의 등장으로 자동차 산업이 빠르게 발전하면서 애플리케이션용 장비의 소형화가 강조되고 있으며, 이는 주로 시장 성장을 주도하고 있습니다.

현재 주요 자동차 제조업체들은 전기 자동차 부문에서 제조 역량을 강화하고 있습니다. 2022년 6월에 발표된 폭스바겐과 지멘스의 발표를 예로 들 수 있습니다. 이들은 4억 5,000만 달러라는 상당한 금액을 투자하겠다는 의사를 밝혔는데, 이는 일렉트리파이 아메리카의 가치를 24억 5,000만 달러로 평가할 수 있는 금액입니다. 이 공동 노력은 2026년까지 미국과 캐나다 전역에서 Electrify America의 충전소 수를 두 배로 늘리는 것을 목표로 하고 있습니다.

EV-Volumes.com에 따르면 2022년 상반기 전기차의 세계 판매량은 BEV와 PHEV에서 430만대를 넘습니다고 합니다. 자동차에 대한 엄청난 수요와 급속한 개발은 정전식 압력 센서 시장을 확대할 것으로 예상됩니다.

또한 IEA에 따르면 2022년에는 약 1,020만 대의 플러그인 전기 경차(PEV)가 판매될 것으로 예상됩니다. 또한 유럽 5대 시장의 전기 자동차 판매량은 2022년에 크게 증가했습니다. 또한 미국의 순수 전기 및 플러그인 전기 자동차 판매량은 2022년에 정점을 찍었습니다. 예를 들어, EERE와 미국 에너지부의 아르곤 국립연구소에 따르면 2022년 미국의 플러그인 전기 자동차(PEV) 판매량은 2021년 607,600대에 비해 918,500대에 달했습니다. 이러한 전기 자동차의 증가는 전 세계적으로 정전식 압력 센서에 대한 수요를 증가시킬 것으로 보입니다.

북미가 시장을 독점할 전망

북미는 대륙 전체의 안정적인 산업 구조로 인해 정전식 압력 센서 시장을 지배할 것으로 예상됩니다. 이 지역에서 점점 더 많은 연구 개발(R&D)이 이루어지고 있어 혁신과 시장 출시의 선두주자가 될 것입니다.

정전식 센서의 의료 용도는 지난 1년간 큰 성장을 보였습니다. 호흡기, 인공 호흡기, 생체 신호 모니터, 기류 용도는 주요 의료 최종 사용자용도입니다. 많은 첨단기업들이 새로운 연구를 수행하고 혈압 모니터링을 위한 제품을 시장에 투입하고 있습니다. 예를 들어, 기술 대기업인 Apple은 혈압 모니터링용 커프스 특허를 신청했습니다.

이 지역은 항공우주 및 방위 산업도 선도하고 있습니다. 미국은 국방비가 가장 높은 나라입니다. SIPRI에 따르면 2022년 세계 군사비는 실질 기준으로 3.7% 증가하여 2조 2,400억 달러의 새로운 최고치에 도달했습니다. 세계 지출은 2013년부터 22년의 스팬으로 19.0%라는 대폭적인 성장을 기록하고, 2015년 이후는 매년 일관되게 상승하고 있습니다. 또한 NASA는 태양계 확장 및 탐사에 중점을 둔 향후 프로젝트 계획을 발표했습니다. 이러한 항공 우주 및 산업 분야의 증가는 이 지역에서 정전식 압력 센서에 대한 더 많은 수요를 가져올 것으로 보입니다.

게다가 이 지역의 기관들의 다양한 산업에 대한 이러한 대규모 투자가 정전식 압력 센서 및 그 응용 분야 시장을 주도하고 있습니다.

정전식 압력 센서 산업 개요

정전용량식 압력 센서 시장은 다수의 진출기업이 존재하기 때문에 경쟁이 심합니다. 정전식 압력 센서의 제품 비용이 낮아짐에 따라 이 제품을 제공하는 진출기업의 수가 증가하고 있습니다. 또한 제품 제공의 차별화의 필요성 때문에 공급업체는 경쟁적인 가격 전략을 채택하고 있습니다. 이 시장에는 ACS-Control-System GmbH, BD Sensors GmbH, Infineon Technologies, TE Connectivity 등의 주요 기업이 있습니다.

2023년 6월, Infineon Technologies AG는 두 가지 새로운 XENSIV 기압계 기압(BAP) 센서인 KP464와 KP466을 출시했습니다. 이 센서는 자동차 애플리케이션을 위해 특별히 설계되었으며 다양한 이점을 제공합니다. KP464는 엔진 제어 관리에 이상적이며, KP466 BAP 센서는 특히 시트 컴포트 기능을 향상시키기 위해 고안되었습니다. KP464 및 KP466 센서는 정전용량식 측정 원리를 활용하는 고성능, 고정밀, 소형 디지털 절대 압력 센서입니다.

2023년 5월, Dwyer Instruments는 최신 산업용 차압 트랜스미터를 출시했습니다. 산업용 차압 트랜스미터 시리즈 IDPT는 내구성이 뛰어난 방수 하우징으로 설계되어 까다로운 산업 환경을 견딜 수 있습니다. 뛰어난 정확도와 안정성을 제공하여 다양한 산업 분야에서 장기간 사용하기에 이상적입니다. 이 압력 트랜스미터는 0-0.25기압에서 0-1기압 범위의 정전식 압력 센서와 0-2.5기압에서 0-10기압 범위의 피에조 센서를 갖추고 있으며, 고객은 0.25% 또는 0.5% 풀스케일 정확도 옵션 중에서 선택할 수 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

기술 스냅샷

시장 성장 촉진요인

제품의 소형화와 첨단 기술의 통합의 중시

자동차와 산업분야에서의 용도수 증가

시장 성장 억제요인

제품차별화의 부족

밸류체인 분석

산업의 매력 - Porter's Five Forces 분석

신규 진입업자의 위협

구매자, 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

최종 사용자별

자동차

의료

화학제품 및 석유화학제품

항공우주

발전

기타

지역

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제6장 경쟁 구도

기업 프로파일

ACS-Control-System GmbH

BD Sensors GmbH

Impress Sensors & Systems Ltd

Infineon Technologies Inc.

Kavlico

Metallux SA

Murata Manufacturing Co. Ltd

TE Connectivity Ltd

Pewatron AG

Bourns Ltd

Sensata Technologies Holding NV

VEGA Controls Ltd

제7장 투자 분석

제8장 시장 기회와 앞으로의 동향

HBR

영문 목차

영문목차

The Capacitive Pressure Sensor Market size is estimated at USD 4.35 billion in 2025, and is expected to reach USD 6.40 billion by 2030, at a CAGR of 8% during the forecast period (2025-2030).

Key Highlights

Pressure sensors with a capacitive cell have been designed to offer unique and accurate results to the existing equipment. The distinct advantages of ceramic material allow sensors to provide long-term stability and reliability with high resistance to pressure.

Capacitive pressure sensors have become increasingly popular compared to resistive sensing technology due to their impressive sensitivity, accuracy, and lack of wear and tear issues. Due to their numerous standout features, these sensors increasingly replace resistive sensors in many applications. Additionally, advancements in sensor technology have resulted in the creation and shift towards smaller sensors, presenting numerous opportunities for industry leaders.

The capacitive pressure sensor's simple and robust mechanical structure enables several industrial applications. Capacitive pressure sensors can sustain harsh industrial conditions due to the use of ceramics and provide a quicker response rate.

As MEMS technology has improved, capacitive pressure sensors have become smaller, which has made them useful in more industries. The miniaturization of capacitive pressure sensors has reduced their production costs. Hence, the capacitive pressure sensor market is growing with its cheap, efficient, and wide array of applications.

Furthermore, sales of automobiles, particularly electric vehicles, have increased significantly in the last year. That is expected to grow more in the future and thus will impact the market for capacitive pressure sensors as well.

Additionally, the COVID-19 impacted the market very heavily due to lockdowns and other rules and regulations imposed by governments around the globe. However, in the post pandemic scenario, the market had grown a lot due to the fast growth of the industries that used it, such as the automotive, medical, oil and gas, and other industries.

However, there is not as much of a barrier to entry, many companies now offer capacitive pressure sensors. This makes prices very competitive and makes it hard to differentiate one product from another, which is slowing market growth.

Capacitive Pressure Sensor Market Trends

Automotive Segment is Expected to Observe Significant Market Growth

One of the most important things when designing and making pressure sensors for use in cars is that they work well in a wide range of temperatures, vibrations, media, shocks, and electromagnetic conditions. In other words, the sensor must be durable enough to do its job.

The rapid evolution of the automotive sector, with the advent of autonomous vehicles or electric vehicles, emphasizes the miniaturization of equipment for applications, primarily driving the market's growth.

Major automotive manufacturers are currently increasing their manufacturing capacity in the electric vehicle sector. An example is the announcement by Volkswagen and Siemens made in June 2022. They stated their intention to invest a significant amount of USD 450 million, which would value Electrify America at USD 2.45 billion. This collaborative effort aims to double the number of Electrify America charging stations across the US and Canada by 2026.

The global sales of electric vehicles will cross 4.3 million new BEVs and PHEVs during the first half of 2022, as stated by EV-Volumes.com. The huge demand for automotive vehicles and their rapid developments are expected to augment the capacitive pressure sensor market.

Additionally, According to IEA, In 2022, an estimated 10.2 million units of plug-in electric light vehicles (PEVs) were sold. Additionally, electric vehicle sales in Europe's five major markets witnessed a significant increase in 2022. Also, United States sales of all-electric and plug-in electric vehicles peaked in 2022. For instance, according to EERE and the U.S. Department of Energy's Argonne National Laboratory, plug-in electric vehicle (PEV) sales reached 918,500 units in the United States in 2022, compared to 607,600 units in 2021. Such rise in electric vehicles is likely to boost the demand for capacitive pressure sensors gloablly.

North America Region is Expected to Dominate the Market

North America is expected to dominate the capacitive pressure sensor market due to the stable industrial structure across the continent. More and more research and development (R&D) is being done in the area, making it the leader in innovation and getting it to market.

Medical applications of capacitive sensors have shown significant growth over the past year. Respirators, ventilators, vital sign monitors, and airflow applications are major medical end-user applications. Many tech companies are conducting new research and launching their products on the market for monitoring blood pressure. For instance, technology giant Apple Inc. filed a patent application for a blood pressure monitoring cuff.

The region also leads the aerospace and defense industries. The United States is the country with the highest defense spending. According to SIPRI, World military expenditure increased by 3.7% in real terms in 2022, reaching a new peak of USD 2,240 billion. Global spending has experienced a significant growth of 19.0% over the span of 2013-22 and has consistently risen each year since 2015. In addition, NASA has announced its plans for future projects, focusing on expanding and exploring the solar system. Such rise in aerospace and industries are likely to bring more demand for capacitive pressure sensors in the region.

Additionally, These massive investments across various industries by organizations in the region are driving the market for capacitive pressure sensors and their applications.

Capacitive Pressure Sensor Industry Overview

The Capacitive Pressure Sensor Market is highly fragemented with numerous players. With the declining product cost of capacitive pressure sensors, a rise in the number of players offering the product is observed. Additionally, the need for more differentiation in the product offerings made the vendors adopt competitive pricing strategies. The market has several leading players, such as ACS-Control-System GmbH, BD Sensors GmbH, Infineon Technologies, TE Connectivity, etc.

June 2023: Infineon Technologies AG introduced its two new XENSIV barometric air pressure (BAP) sensors: the KP464 and KP466. These sensors are specifically designed for automotive applications and offer a range of benefits. The KP464 is ideal for engine control management, while the KP466 BAP sensor is specifically intended for enhancing seat comfort functions. The KP464 and KP466 sensors are high-performance, high-precision, and compact digital absolute pressure sensors that utilize the capacitive measurement principle.

May 2023: Dwyer Instruments released its latest industrial differential pressure transmitter. The Series IDPT industrial differential pressure transmitter from Dwyer is designed with durable and water-resistant housing, ensuring it can withstand challenging industrial environments. It offers exceptional accuracy and stability, making it ideal for long-term use in various industrial applications. This pressure transmitter features a capacitive pressure sensor for ranges of 0 to 0.25 in w.c. to 0 to 1 in w.c. and a piezo sensor for ranges of 0 to 2.5 in w.c. to 0 to 10 in w.c. Customers can choose between accuracy options of 0.25% or 0.5% full-scale.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Technology Snapshot

4.3 Market Drivers

4.3.1 Emphasis on Miniaturization and Integration of Advanced Technology in Products

4.3.2 Growing Number of Applications in the Automotive and Industrial Sectors

4.4 Market Restraints

4.4.1 Lack of Product Differentiation

4.5 Industry Value Chain Analysis

4.6 Industry Attractiveness - Porter's Five Forces Analysis