ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

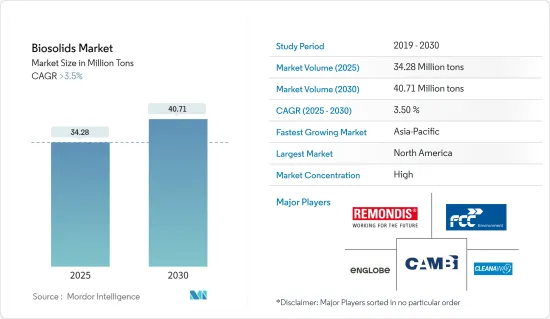

바이오 솔리드 시장 규모는 2025년 3,428만 톤으로 예측되며, 2030년에는 4,071만 톤에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 3.5%를 초과할 것으로 예측됩니다.

COVID-19 팬데믹은 2020년 바이오 솔리드 시장에 부정적인 영향을 미쳤습니다. 그러나 농지에서의 바이오 솔리드 수요 증가는 팬데믹 이후 산업 전체의 성장을 뒷받침하고 있습니다.

주요 하이라이트

시장을 견인하는 주요 요인 중 하나는 위험한 화학 비료를 대체 할 필요성과 세계 각국의 엄격한 배출 규제입니다.

한편, 일반적으로 이용 가능한 바이오 솔리드에 대한 잘못된 정보는 조사 대상 시장의 성장을 둔화시킬 것으로 예상됩니다.

아시아태평양, 주로 중국과 인도에서 슬러지 처리에 대한 관심 증가는 곧 산업 성장의 새로운 길로 이어질 것으로 예상됩니다.

북미는 친환경 기술에 대한 정부의 공적 지원으로 바이오 솔리드 시장을 독점하고 있습니다.

바이오 솔리드 시장 동향

농지 이용이 시장을 독점

바이오 솔리드는 농지, 숲, 방목지 또는 매립이 필요한 교란지에서 사용할 수 있습니다.

소비량에서는 농지 용도가 가장 많은 바이오 솔리드를 소비하고 있습니다. 아시아태평양과 북미의 일관된 인구 증가는 농업 수율의 필요성을 증가시킬 것으로 예상되며, 이는 이 부문에서의 바이오 솔리드 소비에 긍정적인 영향을 미칠 수 있습니다.

국제곡물협회에 따르면 2021-2022년도 세계의 곡물 총생산량은 약 22억 9,400만톤으로 전년도보다 약 3.05% 증가했습니다. 또한 이 협회의 예측에 따르면 2022-2023년도 세계의 곡물 총생산량은 22억 6,700만 톤으로 감소하지만 2023-2024년도에는 2,310톤에 달할 것으로 예상되고 있습니다.

중국은 세계 곡물 생산 전체의 약 7%를 차지하고 세계 인구의 22%를 차지하고 있습니다. 중국은 쌀, 면화, 감자 및 기타 작물을 포함한 다양한 작물의 가장 큰 생산 국가입니다.

농업농촌부의 제3차 농작물 생산 사전 예측에 의하면, 2022-23년의 국내의 총 식량 곡물 생산량은 3억 5,560만 톤(MT)에서 3억 3,050만 톤(MT)이 되었습니다.

과학자와 농업 종사자는 작물의 생산성을 향상시키고 불균형 인구 증가로 인한 식량 수요를 충족시키는 새로운 기술을 요구하고 있습니다. 게다가 미국 등에서는 지난 10년간 이용가능한 농지면적이 감소하고 있습니다.

바이오 솔리드는 비료와 토양 개량제로 인간 작물 생산에 효과적으로 사용할 수 있습니다. 바이오 솔리드는 일반적으로 기존의 농기구를 사용하여 토양에 투입되며 비료로도 이용되고 있습니다.

대기업과 농업 종사자들은 축산과 육류 분야에 뛰어들고 있습니다. 이들은 축산물 생산에 대한 수요를 증가시키고 있으며, 이는 축산물 생산을 위한 비료로서 바이오솔리드를 이용하는 원동력이 되고 있습니다. 따라서 농지 이용에서 바이오 솔리드 수요가 증가하고 있습니다.

바이오 솔리드는 비료 비용을 줄이는 데도 도움이 되며 작물 성장에 필요한 미량 영양소를 많이 공급합니다. 세계 인구 증가는 농업에 대한 요구를 증가시킬 것으로 예상되며, 이는 농업 부문에서 바이오 솔리드의 사용에 영향을 미칠 수 있습니다.

따라서 예측 기간 동안 농지 이용이 시장을 독점할 것으로 예상됩니다.

북미가 시장을 독점

북미는 미국과 캐나다 등 국가에서 친환경 기술에 대한 정부의 공적 지원으로 시장을 독점하고 있습니다.

미국에서는 바이오 솔리드 시장은 정부와 일반 시민 모두 환경에 좋은 기술에 대한 선호가 큰 원동력이 되고 있습니다.

미국 환경보호청(EPA)은 고품질의 하수처리 슬러지를 오염물질을 대량으로 함유한 생 슬러지와 구별하기 위해 '바이오솔리드'라는 명칭을 채택했습니다.

재사용할 수 없는 폐수에서 바이오 솔리드를 처분하는 방법(매립지에 넣는 등)과, 좋은 방법으로 이용하는 방법(바이오 가스나 에너지 회수를 수반하는 매립 등)이 있습니다.

바이오 솔리드는 폐수 처리 과정에서 발생하며 미국 환경보호청의 40 CFR Part 503 규정을 충족시키기 위해 널리 사용됩니다.

현재 미국 내에서 발생하는 바이오 솔리드의 대부분은 낮은 수준의 오염 물질을 포함한 EQ 또는 PC 바이오 솔리드로 예상됩니다. 발생하는 바이오 솔리드의 약 절반은 토양 개선에 유익하게 활용됩니다.

미국에서는 바이오 솔리드가 재활용되거나 비료로 적용되어 생산성이 높은 토양을 개선하고 유지하며 식물의 성장을 가속하고 있습니다. 하수 슬러지를 처리함으로써 바이오 솔리드는 매립지 및 기타 처분장에서 장소를 차지하는 대신 귀중한 비료로 사용됩니다. 바이오 솔리드의 약 절반은 토지로 재활용됩니다.

미국 인구가 증가함에 따라 식량 수요는 빠르게 성장하고 있습니다. 2022년에는 미국 평균 가구의 식량 지출이 약 12.72% 증가하여 9,343달러에 달했습니다.

농업 부문 증가는 바이오 솔리드 소비를 더욱 높일 것으로 예상됩니다. 농업 및 관련 산업은 2022년 미국 국내총생산(GDP)의 약 5.5%에 기여합니다.

위의 요인들로부터 예측기간 동안 북미가 최대 시장 점유율을 차지할 것으로 예상됩니다.

바이오 솔리드 시장 산업 개요

바이오 솔리드 시장은 부분적으로 통합되어 있습니다. 주요 기업(순서부동)에는 REMONDIS SE&Co.KG, Cambi ASA, FCC Group, Englobe, Cleanaway 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

촉진요인

북미의 유해 화학 비료로부터 대체

정부의 엄격한 배출규제

기타 촉진요인

억제요인

바이오 솔리드에 대한 올바른 지식과 인식의 부족

기타 억제요인

산업 가치사슬 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(시장 규모(수량 기준))

유형

클래스 A

클래스 A EQ(엑셉셔널 퀄리티)

클래스 B

형태

케이크

액체

펠렛

용도

농지 이용

인용작물 생산용 비료/토양 개량제

축산용 비료 - 목초지

비농지 이용

삼림작물(토지의 수복과 임업)

토지의 매립(도로와 도시 습지)

광산터의 매립

조경, 레크리에이션장, 가정내 이용

에너지 회수 에너지 생산

열생성, 소각, 가스화

석유와 시멘트 생산

상업이용

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

노르딕

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율 분석

주요 기업의 전략

기업 프로파일

Agrivert Ltd

Aguas Andinas SA

Alan Srl

Allevi Srl

BCR Environmental

CRE-Centro di Ricerche Ecologiche

Cambi ASA

Casella Waste Systems Inc.

Cleanaway

DC Water

Eco-trass

Englobe

FCC Group

Lystek International

Merrell Bros. Inc.

Parker Ag Services LLC

Recyc Systems Inc.

REMONDIS SE & Co. KG

Saur

SYLVIS

Synagro Technologies

Terrapure BR Ltd

Walker Industries

제7장 시장 기회와 앞으로의 동향

아시아태평양의 슬러지 처리 주목 증가

기타 기회

CSM

영문 목차

영문목차

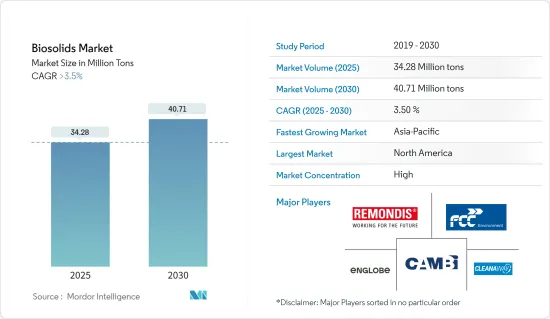

The Biosolids Market size is estimated at 34.28 million tons in 2025, and is expected to reach 40.71 million tons by 2030, at a CAGR of greater than 3.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the biosolids market in 2020. However, the growing demand for biosolids on agricultural land has fueled overall industry growth since the pandemic.

Key Highlights

One of the main things driving the market that was looked at is the need to replace dangerous chemical fertilizers and strict emission laws in many countries around the world.

On the other hand, contradictory information about biosolids that is available to the public is expected to slow the growth of the market studied.

The rising focus on sludge treatment in the Asia-Pacific, mainly in China and India, is anticipated to offer new avenues for industry growth shortly.

North America dominated the biosolids market due to government and public support for environmental-friendly technologies.

Biosolids Market Trends

Agricultural Land Application to Dominate the Market

Biosolids can be used on agricultural land, in forests, on rangelands, or in disturbed land needing reclamation.

In terms of consumption, agricultural land applications consume the most biosolids. Consistent population growth across Asia-Pacific and North America is expected to augment the need for agricultural yields, which may positively affect the consumption of biosolids in the sector.

According to the International Grains Council, in FY 2021-2022, the total grain production globally was about 2,294 million metric tons, about 3.05% more than the previous year. Furthermore, as per the council's estimation in FY 2022-2023, the total global grain production will decrease to 2,267 million metric tons. However, it is anticipated to reach 2,310 in FY 2023-2024.

China accounts for about 7% of the overall crop production globally, thus feeding 22% of the world's population. The country is the largest producer of different crops, including rice, cotton, potatoes, and other crops.

According to the Third Advance Estimates for crop production by the Ministry of Agriculture and Farmers Welfare, total foodgrain production in the country in 2022-23 was valued at 330.5 million tonnes (MT) from 315.6 MT.

Scientists and farmers are looking for new technologies to increase the productivity of crops and meet the food demand arising from disproportionate population growth. In addition, there has been a decrease in the total available cropland area in countries such as the United States over the last decade.

Biosolids can be effectively used as fertilizers and soil conditioners for human crop production. These are usually incorporated into the soil with conventional farm equipment. They are also used as fertilizer for animal crop production.

Big enterprises and farmers are increasingly making their presence felt in cattle farming and meat products. They are augmenting the demand for animal crop production, which is providing impetus to the application of biosolids as fertilizers for animal crop production. This has led to an increase in demand for biosolids in agricultural land applications.

They also help reduce fertilizer costs and provide many micronutrients for crop growth. The increasing world population is expected to give rise to a growing need for agriculture, which may impact the use of biosolids in the sector.

Hence, agricultural land application is expected to dominate the market studied during the forecast period.

North America to Dominate the Market

North America dominated the market owing to the government and public support for environmental-friendly technologies in countries such as the United States and Canada.

In the United States, the biosolids market is mostly driven by the fact that both the government and the public want to use technologies that are good for the environment.

The US EPA adopted the name "biosolids" to differentiate high-quality treated sewage sludge from raw sewage sludge, which contains large amounts of pollutants.

There are two ways to get rid of biosolids from wastewater that cannot be used again (like putting them in a landfill) and ways to use them in a good way (like landfilling with biogas and energy recovery).

Biosolids are generated during wastewater treatment processes and are extensively used to satisfy the US EPA's 40 CFR Part 503 regulations.

The majority of the biosolids that are currently generated in the country are expected to be EQ or PC biosolids containing low levels of pollutants. About half of the biosolids produced in the country are being beneficially used to improve soils.

In the United States, biosolids are either recycled or applied as fertilizer to improve and maintain productive soils and stimulate plant growth. By treating sewage sludge, the biosolids are used as valuable fertilizer instead of taking up space in a landfill or other disposal facility. Approximately half of all biosolids are recycled to land.

The demand for food is growing rapidly with the rising population in the United States. In 2022, the average household spending in the United States on food increased by about 12.72% and was valued at USD 9,343.

The rising agriculture sector is expected to further boost the consumption of biosolids. Agriculture and related industries contributed to about 5.5% of the US gross domestic product (GDP) in 2022.

Therefore, due to the above factors, North America is anticipated to have the largest market share during the forecast period.

Biosolids Market Industry Overview

The biosolids market is partially consolidated in nature. The major players (not in any particular order) include REMONDIS SE & Co. KG, Cambi ASA, FCC Group, Englobe, and Cleanaway, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Replacing Hazardous Chemical Fertilizers in North America

4.1.2 Stringent Government Emission Laws

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Lack of Proper Knowledge and Awareness on Biosolids

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Class A

5.1.2 Class A EQ (Exceptional Quality)

5.1.3 Class B

5.2 Form

5.2.1 Cakes

5.2.2 Liquid

5.2.3 Pellet

5.3 Application

5.3.1 Agriculture land Application

5.3.1.1 Fertilizer/Soil Conditioner for Human Crop Production

5.3.1.2 Fertilizer for Animal Crop Production - Pastures

5.3.2 Non-agricultural Land Application

5.3.2.1 Forest Crops (Land Restoration and Forestry)

5.3.2.2 Land Reclamation (Roads and Urban Wetlands)

5.3.2.3 Reclaiming Mining Sites

5.3.2.4 Landscaping, Recreational Fields, and Domestic Use

5.3.3 Energy Recovery Energy Production

5.3.3.1 Heat Generation, Incineration, and Gasification

5.3.3.2 Oil and Cement Production

5.3.3.3 Commercial Uses

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Spain

5.4.3.6 NORDIC

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 United Arab Emirates

5.4.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Agrivert Ltd

6.4.2 Aguas Andinas SA

6.4.3 Alan Srl

6.4.4 Allevi Srl

6.4.5 BCR Environmental

6.4.6 C.R.E. - Centro di Ricerche Ecologiche

6.4.7 Cambi ASA

6.4.8 Casella Waste Systems Inc.

6.4.9 Cleanaway

6.4.10 DC Water

6.4.11 Eco-trass

6.4.12 Englobe

6.4.13 FCC Group

6.4.14 Lystek International

6.4.15 Merrell Bros. Inc.

6.4.16 Parker Ag Services LLC

6.4.17 Recyc Systems Inc.

6.4.18 REMONDIS SE & Co. KG

6.4.19 Saur

6.4.20 SYLVIS

6.4.21 Synagro Technologies

6.4.22 Terrapure BR Ltd

6.4.23 Walker Industries

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Focus on Sludge Treatment in Asia-Pacific