ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

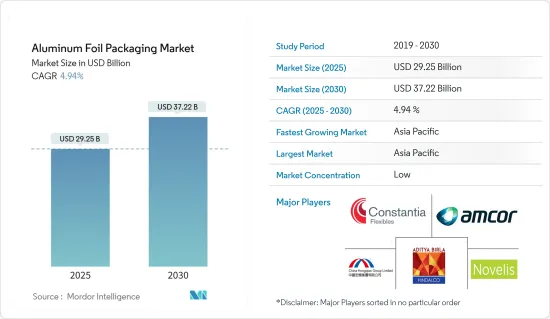

알루미늄 포일 포장 시장 규모는 2025년에 292억 5,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 4.94%로, 2030년에는 372억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

알루미늄 포일은 습기, 빛, 산소, 박테리아로부터 제품을 보호하기 때문에 식품, 음료, 의약품 등 산업의 주요 요구 사항을 충족합니다. 알루미늄 포일은 주로 식음료 산업에서 소비됩니다. 종이 형태로 제조된 알루미늄 복합재료는 거대한 낙농 산업에 더 높은 수요가 있습니다. 또한 알루미늄 포일은 88%의 반사율을 가지며 단열재로 유용합니다. 알루미늄 시트는 또한 증기 보호막을 제공하기 때문에 식품 포장에 이상적입니다.

햇빛은 많은 식료품에 빠르게 영향을 미치며 외관과 맛을 손상시킵니다. 포일은 이러한 포장 요구 사항을 충족하는 가장 현실적인 솔루션이므로 이 재료는 유제품, 과자 및 음료의 이상적인 핵심 포장 재료로 간주됩니다.

주요 하이라이트

예를 들어, 라미네이트 포일로 만들어진 밀봉 포장 건조 우유의 유통 기한은 2년입니다. 기타 연질 포장 솔루션의 사용 급증도 예측 기간 동안 관찰될 수 있습니다. 알루미늄의 수요 증가는 중국에서 알루미늄 포일 수입의 급증으로 이어졌으며, 중국에서 미국으로의 알루미늄 포일 출하는 지난 10년간 크게 증가했습니다. 현재 연질 포장은 주로 식품에 사용되고 있으며 가장 빠르게 확장되는 부문은 커피, 스낵 과자, 신선 식품, 조리 식품 및 반려동물 식품입니다.

알루미늄 포일 포장 시장 수요는 플라스틱이나 유리에 비해 알루미늄이 가볍고 내구성이 뛰어나며 유연성이 있고 보호성이 있기 때문에 확대가 예상되고 있습니다. 알루미늄은 편의성, 안전성, 경량성 및 내구성으로 다양한 산업 및 가정에서 사용하기에 이상적입니다.

제약 산업에서는 의약품에 블리스터 팩을 사용하는 경우가 많습니다. 블리스터 팩은 블리스터 필름 또는 리드 필름으로 알려진 알루미늄 포일로 구성된 푸시 스루 밀봉과 개별 정제용 성형 플라스틱, 소위 푸시 스루 블리스터로 구성됩니다. 의약품에는 다양한 블리스터 포장재가 채용되고 있습니다. 의약품의 포장에는 주로 알루미늄 플라스틱 포장이 채용되고 있지만, 기타 의약품에는 다른 포장의 채용도 적지 않습니다.

게다가, 의약품이나 온라인 주문 식품용의 알루미늄 랩이나 알루미늄 용기 등, 알루미늄 포일 포장 수요는 최근 대폭 증가하고 있습니다. Aluminum Stewardship Initiative(ASI)는 사회 및 환경 정책에 대한 많은 기준을 수립했습니다. ASI는 COVID-19의 대유행 동안 전국적으로 실시된 운영 정지에 의해 중단된 알루미늄 포일 포장재 공급사슬을 회복시킬 것으로 기대되고 있습니다.

알루미늄의 지속가능성은 경쟁업체의 우위를 창출하는 동시에 제품 개발의 우위를 가져옵니다. 알루미늄 협회에 따르면 생산된 모든 알루미늄의 거의 75%가 다시 사용되고 있습니다. 또한 알루미늄 폐기물을 폐기할 때 물이나 지상에 해로운 오염물질을 가하지 않고 경제적으로 재활용할 수 있어 지속가능성을 제공합니다.

알루미늄 포일 포장 시장 동향

압연 포일 부문이 시장에서 큰 점유율을 차지

의약품 및 온라인 주문 식품용 알루미늄 랩 및 용기를 포함한 알루미늄 포일 포장은 수요의 현저한 증가를 기록하고 있습니다. Aluminum Stewardship Initiative(ASI)는 많은 사회 환경 시책 기준을 제정하고 있습니다. ASI는 COVID-19 팬데믹 시에 전국적으로 실시된 운영 정지에 의해 중단된 알루미늄 포일 포장재 공급사슬을 회복시킬 것으로 기대되고 있습니다.

알루미늄 포일 포장재는 밝기와 반사성을 유지하며 소매 공간에서 소비자의 관심을 끌고 있습니다. 게다가 알루미늄 포일은 컬러 래커 가공이나 브랜드 식별 디자인 인쇄가 가능합니다. 특히 식품 산업에서는 지속가능한 포장에 대한 수요가 증가하고 있으며 알루미늄 포일 포장은 매력적인 선택이 될 것으로 예상됩니다.

알루미늄 포일 랩은 접었을 때 펴지지 않는 성질 및 엠보싱 가공성과 같은 다른 포장 재료에서는 얻을 수 없는 특유의 특성을 갖추고 있습니다. 예측 기간 동안 식품, 담배, 화장품 산업이 알루미늄 포일 랩 성장의 주요 원동력이 될 것으로 예상됩니다.

게다가 알루미늄 포일은 사용하기 쉽고 버리기 쉬우며 일반 금속의 2배의 속도로 열을 전달할 수 있기 때문에 다양한 식품의 조리에 점점 사용되고 있습니다. 일반 가정에서 조리가 늘어나면서 알루미늄 포일은 식품을 싸거나 구울 때 사용됩니다.

최근 몇 년간 알루미늄 생산량도 증가하고 있으며, 많은 나라가 앞다투어 제련소 수를 늘려 대량의 알루미늄을 생산하고 있습니다. 2024년 1월 발표된 미국 지질조사소 보고서에 따르면 중국 제련소는 2023년 약 410만 톤의 알루미늄을 생산했습니다. 주요 비철금속인 알루미늄은 포장 산업 전반에 걸쳐 광범위한 용도가 있습니다.

아시아태평양이 시장에서 큰 점유율을 차지

아시아태평양 부문은 예측 기간 내내 우위를 유지할 것으로 예상됩니다. 알루미늄 포장을 생산하는 중국의 알루미늄 포일 대량 소비는 이 지역의 재료에 대한 강한 수요의 주요 원인이며 알루미늄 포일 시장의 상승으로 이어지고 있습니다. 이 지역에서는 알루미늄 포일이 식품 저장에 사용되는 경우가 늘어나고 있습니다. 식품, 제약, EV 배터리 제조업체 등 주요 산업이 시장 성장을 가속할 것으로 예상됩니다.

아시아태평양 국가는 알루미늄의 대부분을 파우치와 가방 생산에 사용하고 있습니다. 이들 국가에서는 보다 건강한 라이프스타일과 소비 패턴의 필요성이 알루미늄 포일에 대한 수요를 증가시키고 있습니다. 개발도상국의 인구 증가로 알루미늄 포일 포장의 요구가 높아지고 있습니다. 아시아태평양 국가에서는 환경 친화적인 소비를 장려하고 식품 안전을 보장하며 식품을 보존하고 환경 지속가능성 원칙을 지지하기 위해 알루미늄 포장에 대한 수요가 증가하고 있습니다.

또한 국가 통계국에 따르면 2023년 중국의 1차 알루미늄 생산량은 4,200만 톤으로 2022년 4,021만 톤에서 증가하고 있습니다. 지난 10년간 중국의 연간 1차 알루미늄 생산량은 꾸준히 증가했으며, 2019년에는 3,504만 톤에 달했습니다.

게다가 제37회 AAHAR 국제 식품 및 호스피탈리티 박람회에서는 LSKB Aluminum Foils Pvt.Ltd가 인도 최초의 골든 엠보싱 가공 HOMEFOIL을 발표하였습니다. LSKB Aluminium Foils Pvt.Ltd.가 출시한 1kg과 555g의 금색과 은색 엠보스 HOMEFOIL의 두께는 18미크론이며, 75m, 25m, 9m는 12미크론입니다. 제품은 위생을 유지하기 위해 안전하고 환경 친화적이고 환기가 잘되는 실내에서 혁신적인 기술을 사용하여 제조됩니다. 포장에는 포일을 안전하게 절단하기 위한 포일 커터도 함께 제공됩니다.

인도는 중국에 이어 세계 2위의 담배 소비국이기 때문에 짧은 알루미늄 포일 랩 수요가 높습니다. 현재 알루미늄 포일은 특히 담배 상자의 내부 라이닝 소재로 선호되고 있습니다. 그 이유는 가볍고 튼튼하고 재봉이 간단하며 탁월한 「촉감」과 외관을 겸비해, 각 블렌드나 브랜드의 특징적인 향기를 유지할 수 있기 때문입니다.

ITC India Ltd의 담배 부문 매출은 2023 회계 연도에 3,120억 루피(37억 3,000만 달러) 이상으로 급증했으며, 2019년 약 2,610억 루피(27억 3,000만 달러)에서 크게 증가했습니다. 주목할만한 점은 ITC Ltd가 인도의 FMCG 산업에서 주요 기업으로서의 지위를 확립하고 있으며, 담배는 주요 제품 중 하나입니다. 따라서 이러한 담배 수익의 성장 동향은 전국의 알루미늄 포일 수요를 밀어 올릴 수 있습니다.

알루미늄 포일 포장 산업 개요

알루미늄 포일 포장 시장은 진입 장벽이 낮고 수요가 증가함에 따라 세분화되었습니다. 시장의 주요 기업으로는 Amcor Limited, Constantia Flexibles, China Hongqiao Group Limited, Hindalco Industries Limited(Aditya Birla Group), Novelis 등이 있습니다.

2024년 2월, Constantia Flexibles는 유럽의 유명 포장업체인 Aluflexpack 주식의 약 57%를 구매하는 계약을 체결했다고 발표했습니다. Aluflexpack은 주로 소비자 및 제약 산업을 위한 포일 및 필름 포장 전문 기업으로 알려져 있습니다. 이 인수로 Constantia Flexibles는 다양한 부문에 걸쳐 알루미늄 포일 포장 시장에서의 지위를 크게 강화할 것입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

산업 가치사슬 분석

제5장 시장 역학

촉진요인

용도 확대

알루미늄 제품의 지속가능성

시장의 과제

비교 장벽 특성과 낮은 탄소 발자국을 가진 대체 재료의 출현

제6장 시장 세분화

유형별

압연 포일

보강 포일

기타 유형(블리스터)

용도별

컨버터용 포일

용기용 포일

기타 용도(가정용)

최종 사용자별

식품

음료

의약품

화장품 및 퍼스널케어

기타

지역별

북미

미국

캐나다

유럽

영국

독일

프랑스

스페인

아시아

중국

인도

일본

한국

태국

호주 및 뉴질랜드

라틴아메리카

브라질

멕시코

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

제7장 경쟁 구도

기업 프로파일

Amcor PLC

Constantia Flexibles

Coppice Alupack Limited

China Hongqiao Group Limited

Hindalco Industries Limited(Aditya Birla Group)

Ess Dee Aluminum Ltd

Novelis Inc.

Alcoa Corporation

Penny Plate LLC

Eurofoil Luxembourg SA

Alufoil Products Pvt. Ltd

United Company RUSAL

Zhangjiagang Goldshine Aluminium Foil Co. Ltd

제8장 투자 분석

제9장 시장의 미래

CSM

영문 목차

영문목차

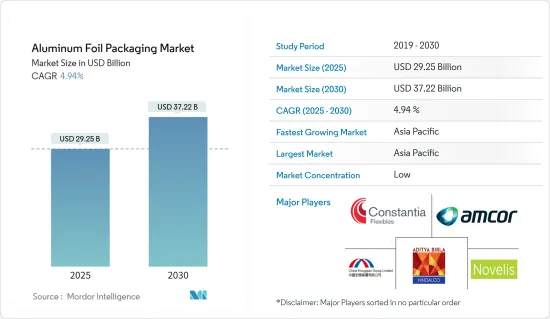

The Aluminum Foil Packaging Market size is estimated at USD 29.25 billion in 2025, and is expected to reach USD 37.22 billion by 2030, at a CAGR of 4.94% during the forecast period (2025-2030).

Key Highlights

Aluminum foil protects against moisture, light, oxygen, and bacteria, thus fulfilling a critical requirement for industries like food, beverage, and pharmaceuticals. Aluminum foil is consumed majorly by the food and beverage industries. Aluminum composites prepared with paper products are in high demand due to the vast dairy industry. Additionally, aluminum foil is 88% reflective, which makes it useful for thermal insulation. The aluminum sheet also provides a protective vapor barrier, making it ideal for use in food packaging.

Sunlight quickly affects many groceries, damaging their appearance and taste. Foil is the most viable solution to cater to these packaging requirements, which has led to the material being regarded as the ideal core packaging material for dairy products, pastries, and beverages.

Key Highlights

For instance, dry milk in hermetically sealed packages made from laminated foil has a shelf life of two years. A surge in the usage of other flexible packaging solutions might also be observed during the forecast period. The increased domestic demand for aluminum has led to an upsurge in aluminum foil imports from China, whose shipments to the United States increased significantly in the last decade. Currently, flexible packaging is mainly used for food, with the fastest areas of expansion being coffee, snack foods, fresh produce, ready-to-eat meals, and pet food.

The market demand for aluminum foil packaging is expected to grow, owing to aluminum's lightweight, durability, flexibility, and barrier properties compared to plastic and glass. The ease of use, convenience, safety, lightweight, and durability of aluminum make it ideal for use across various verticals and households.

The pharmaceutical business frequently uses blister packs for medicinal products. They comprise a push-through closure composed of aluminum foil known as blister film or lid film and the so-called push-through blister, a molded plastic with cavities for individual tablets. Different blister packing materials are employed in medicines for various items. Mainly, aluminum plastic packaging is employed in medicine packaging, while a few other medications use all packaging.

Furthermore, the demand for aluminum foil packaging, including aluminum wraps and containers for pharmaceuticals and online-ordered food, has significantly increased in recent years. The Aluminum Stewardship Initiative (ASI) sets many standards for social and environmental policies. The organization is expected to restore the disrupted supply chains for aluminum foil packaging materials caused by nationwide lockdowns imposed during the COVID-19 pandemic.

Aluminum's sustainability creates competitive business advantages while simultaneously providing product development advantages. According to the Aluminum Association, nearly 75% of all aluminum produced is still in use. Moreover, when disposed of, aluminum waste does not add poisonous contaminants to the water or ground but can be economically recycled and more sustainable.

Aluminum Foil Packaging Market Trends

Rolled Foils Segment Accounts for a Significant Share in the Market

Aluminum foil packaging, including aluminum wraps and containers for pharmaceuticals and online-ordered food, has registered a significant increase in demand. The Aluminum Stewardship Initiative (ASI) has set many social and environmental policy standards. The organization is expected to restore the disrupted supply chains for aluminum foil packaging materials caused by the nationwide lockdowns imposed during the COVID-19 pandemic.

Aluminum foil wrappers maintain brightness and reflectivity, attracting consumer attention in retail spaces. Besides, aluminum foil can be color-lacquered or printed with brand-identifying designs. The increasing demand for sustainable packaging, especially in the food and beverage industries, will likely make aluminum foil wrappers an attractive option.

An aluminum foil wrap provides specific characteristics, such as dead fold and embossability, which other packaging materials cannot obtain. The food, tobacco, and cosmetics industries are expected to be the primary drivers of the growth of aluminum foil wraps over the forecast period.

Additionally, aluminum rolled foils are increasingly used in the culinary preparation of different foods due to their ease of use and disposal and ability to transfer heat twice as quickly as regular metal. As part of a growing culinary practice in households, aluminum foil is used to wrap and bake food.

In the past few years, the production of aluminum has also increased, and many countries have taken the initiative to increase the number of smelters for the production of large metric tons of aluminum. According to a US Geological Survey report published in January 2024, China's smelters collectively produced approximately 4.1 million metric tons of aluminum in 2023. Aluminum, the predominant non-ferrous metal, has extensive applications across the packaging industry.

Asia-Pacific Accounts for a Significant Share in the Market

The Asia-Pacific regional segment is anticipated to maintain its dominance throughout the forecast period. China's massive consumption of aluminum foil for producing aluminum packaging is mainly responsible for the region's strong demand for the material, leading to the rise of the aluminum foil market. Aluminum foil is increasingly used for food goods storage in the region. Key industries, including food, pharmaceutical, and EV battery producers, are anticipated to propel market growth.

Asia-Pacific countries produce and use the majority of aluminum in pouches and bags. The need for healthier lifestyles and consumption patterns in these countries is increasing the demand for aluminum foil. The need for aluminum foil packaging is rising due to increasing populations in developing countries. The demand for aluminum packaging is increasing across several Asia-Pacific countries as they seek to encourage environmentally friendly consumption, ensure food safety, preserve food, and uphold the principles of environmental sustainability.

In addition, according to the National Bureau of Statistics, in 2023, the production volume of primary aluminum in China was 42 million tons, an increase from 40.21 million tons in 2022. In the past decade, China's annual primary aluminum production steadily increased, reaching 35.04 million tons in 2019.

Moreover, at the 37th AAHAR International Food and Hospitality Fair, India's 1st Golden Embossed HOMEFOIL was launched by LSKB Aluminum Foils Pvt. Ltd. The thickness of 1 kg and 555 g golden and silver embossed HOMEFOIL launched by LSKB Aluminium Foils Pvt. Ltd is 18 Micron, and for 75 m, 25 m, and 9 m, it is 12 Micron. The products are manufactured using innovative technologies in safe, environment-friendly, well-ventilated premises to maintain hygiene. The package also has an attached foil cutter to cut the foil safely.

India is the second-largest country worldwide after China in tobacco consumption, resulting in high demand for short aluminum foil wraps. Nowadays, aluminum foil is the preferred barrier material, particularly for the inner liner of cigarette packets. This is because it combines an exceptional "feel" and appearance that is light, robust, and simple to reseal with the capacity to preserve the distinctive aroma of each blend and brand.

ITC India Ltd's Cigarette segment's revenue surged to over INR 312 billion (USD 3.73 billion) in the financial year 2023, marking a significant increase from about INR 261 billion (USD 2.73 billion) in 2019. Notably, ITC Ltd stands as a major player in India's FMCG industry, with cigarettes being its flagship product. Therefore, such growth trends in cigarette revenue may have pushed the demand for aluminum foil nationwide.

Aluminum Foil Packaging Industry Overview

The aluminum foil packaging market is fragmented due to low entry barriers and growing demand. Some key players in the market are Amcor Limited, Constantia Flexibles, China Hongqiao Group Limited, Hindalco Industries Limited (Aditya Birla Group), and Novelis.

February 2024: Constantia Flexibles announced that it had inked a deal to purchase about 57% of Aluflexpack's shares, a prominent European packaging producer. Aluflexpack is known for its foil and film packaging expertise, catering primarily to the consumer and pharma industries. This move significantly bolsters Constantia Flexibles' position in the aluminum foil packaging market, spanning various segments.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitutes

4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increased Spectrum of Applications

5.1.2 Sustainable Nature of Aluminum Products

5.2 Market Challenges

5.2.1 Emergence of Alternative Materials with Comparative Barrier Properties and Low Carbon Footprint

6 MARKET SEGMENTATION

6.1 By Type

6.1.1 Rolled Foil

6.1.2 Backed Foil

6.1.3 Other Types (Blister)

6.2 By Application

6.2.1 Converter Foils

6.2.2 Container Foils

6.2.3 Other Applications (Household)

6.3 By End User

6.3.1 Food

6.3.2 Beverage

6.3.3 Pharmaceutical

6.3.4 Cosmetics and Personal Care

6.3.5 Other End Users

6.4 By Geography

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.2.4 Spain

6.4.3 Asia

6.4.3.1 China

6.4.3.2 India

6.4.3.3 Japan

6.4.3.4 South Korea

6.4.3.5 Thailand

6.4.4 Australia and New Zealand

6.4.5 Latin America

6.4.5.1 Brazil

6.4.5.2 Mexico

6.4.6 Middle East and Africa

6.4.6.1 United Arab Emirates

6.4.6.2 Saudi Arabia

6.4.6.3 South Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Amcor PLC

7.1.2 Constantia Flexibles

7.1.3 Coppice Alupack Limited

7.1.4 China Hongqiao Group Limited

7.1.5 Hindalco Industries Limited (Aditya Birla Group)