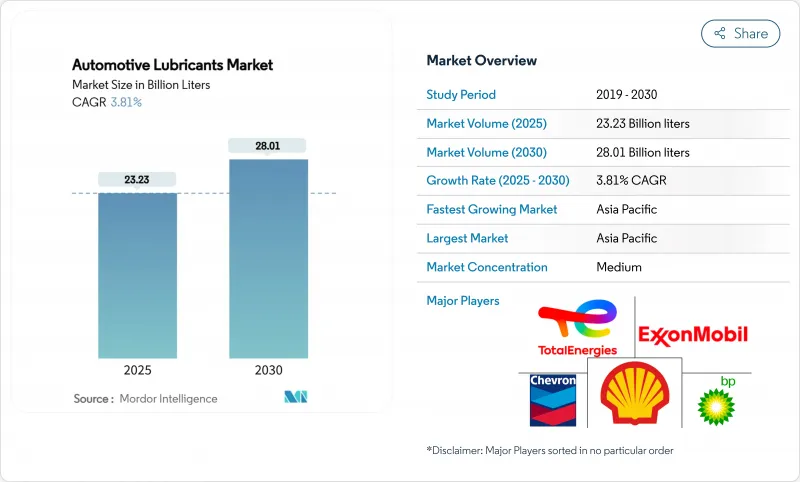

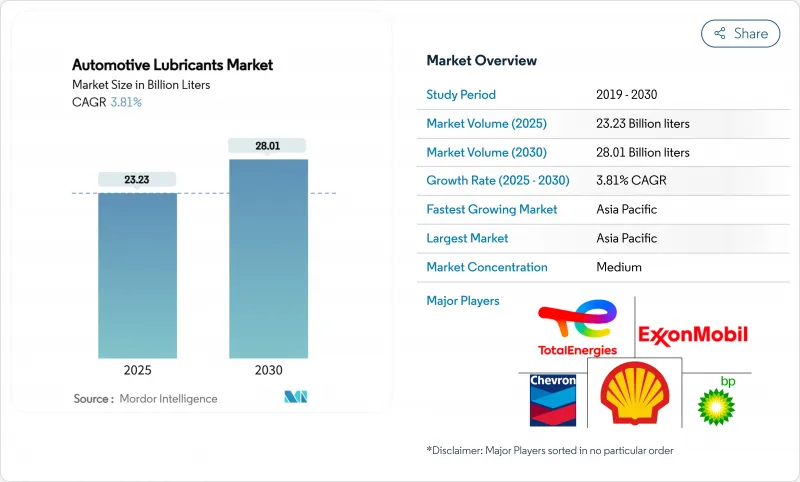

자동차 윤활유 시장 규모는 2025년에 232억 3,000만 리터, 2030년에는 280억 1,000만 리터에 이르고, 예측기간(2025-2030년)의 CAGR은 3.81%를 나타낼 전망입니다.

성장을 지원하는 것은 선진 지역에서 세계적인 자동차 대수의 고령화, 신흥 경제권에서의 이륜차와 상용차의 꾸준한 유입, 연비를 개선하고 드레인 배출 간격을 연장하는 프리미엄 합성차로의 전환에 힘입어 이루어졌습니다. 아시아태평양은 자동차 보유량 증가와 현지 제조업 투자로 인해 여전히 수요의 중심이며, 북미와 유럽은 애프터마켓 매출을 유지하기 위해 자동차 수명에 의존하고 있습니다. 경쟁 강도는 보통 수준을 유지합니다. 전기자동차(EV)의 보급이 가속되고 있으며, 2024년에는 중국 도로에서 3,140만대가 사용되어 OEM 지정의 롱 드레인 인터벌과 같은 역풍이 불고 있지만, API SQ와 같은 저점도 합성유의 단가가 높기 때문에 이 역풍은 완화되고 있습니다.

자동차의 긴 수명화가 윤활유 수요 프로파일을 재구성하고 있습니다. 미국에서는 반도체 부족과 인플레이션으로 자동차 교체율이 둔화되고 있으며, 소유자는 오일 교환 빈도를 늘리고 보다 고품질의 합성유에 투자하게 되었습니다. 유럽의 차량은 더욱 오래되었고, 구미에서는 18.1년, 동유럽에서는 28.4년이 되었습니다. 낡은 엔진은 씰의 열화, 열응력, 오염에 시달리고, 이들 모두가 오일의 열화를 촉진하고, 프리미엄 베이스 스톡 수요에 박차를 가하고 있습니다. 차령 6년에서 15년 사이의 차량 유지보수 비용은 단 1년 만에 514달러에서 537달러로 증가하여 차령과 비용의 관련성이 돋보였습니다. 폐차율은 지난 20년간 최소 4.20%까지 하락하여 애프터마켓의 수익원을 장기화하고 있습니다. 소유자는 보호 성능을 향상시키고 총 소유 비용을 줄이기 위해 고가의 합성 수지가 서비스 베이의 대부분을 차지하고 있습니다.

신흥국은 성숙시장에서 EV 관련 대수 감소를 상쇄했습니다. 중국의 자동차 보유 대수는 4억 5,300만대에 달하고, 2024년 신규 등록 대수는 3,583만대가 됩니다. 인도와 동남아시아에서는 도시 지역의 정체 완화와 저렴한 모빌리티에 힘입어 이륜차 보유 대수가 급증하고 있습니다. 전자상거래 및 마지막 원마일의 배송 경로를 달리는 상업용 차량은 주행 거리가 길고 배수 빈도의 배율을 높입니다. 이 지역의 국내 자동차 제조업체는 현지 블렌더와 협력하여 다양한 연료 품질과 극단적인 기후에 맞는 비용 효율적인 오일을 기동적으로 개발할 수 있습니다. 그 결과, 자동차 윤활유 시장은 세계적인 감속 속에서도 확대를 계속하고 있습니다.

EV는 크랭크 케이스 오일과 많은 구동 시스템 오일을 서비스 메뉴에서 제거합니다. 중국은 2024년 말까지 전년 대비 51.49% 증가한 3,140만대의 신에너지 자동차를 주행시켰습니다. IEA는 2030년까지 세계 재고가 2억 5,000만 대를 넘어 석유 수요가 최대 430만 배럴/일 감소할 것으로 예측했습니다. 그럼에도 불구하고 EV는 새로운 틈새 시장을 도입합니다. 즉, E 모터 베어링용 에스테르, 유전체 쿨런트, 고회전과 전자 양립성에 최적화된 기어 그리스 등입니다. 공급업체의 경우 특수 유체는 기존 엔진 오일의 2-3배 가격 프리미엄을 요구하므로 과제는 양에서 가치로 이동합니다.

엔진 오일은 2024년 판매량의 58.61%를 차지하며 불꽃 점화 및 압축 점화 엔진에서 널리 사용되며 자동차 윤활유 시장을 지원합니다. 소형 트럭이나 오프 하이웨이 기계에서는 섬프 용량이 크기 때문에 점유율이 확대되고 있습니다. 변속기 오일, 유압 오일, 기어 오일은 좁은 용도, 수동 상자, 습식 브레이크 및 파워 스티어링 회로에 필수적입니다. 그리스는 자동차 윤활유 시장 규모의 일부에 불과하지만 EV가 고회전과 전식에 대응하는 베어링 전용 그리스를 필요로 하기 때문에 CAGR 4.28%로 가장 급속히 성장하고 있습니다. 공급업체는 합성 에스테르와 폴리 우레아 증점제를 혼합하여 전도성 제어 및 열 안정성을 실현하여 제품 믹스의 가치를 높입니다.

API SQ 호환 오일의 보급에 따라이 부문의 판매 구성은 합성 오일로 이동합니다. 0W-16 및 0W-12와 같은 초저점도 처방으로 OEM은 특히 일본과 유럽에서 차량 평균 CO2 목표를 달성할 수 있습니다. 헤비 듀티 오일에서도 15W-40에서 5W-30으로의 전환은 연료 비용을 줄이는 더 얇고 높은 HTHS 블렌드에 대한 수요를 보여줍니다. 점도 등급이 좁아짐에 따라 첨가제 패키지도 다양화되어 붕소 에스테르, 이황화 몰리브덴, 무회 세제가 차세대 SKU의 기축이되었습니다. 따라서 자동차 윤활유 시장은 수량 감소와 풍부한 단위당 마진의 균형을 맞추고 있습니다.

자동차 윤활유 시장 보고서는 제품 유형별(엔진 오일, 변속기 기어 오일, 작동유, 그리스), 차량 유형별(승용차, 상용차, 이륜차), 지역별(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)으로 분류되어 있습니다.

2024년 자동차 윤활유 시장은 아시아태평양이 42.25%의 점유율을 차지했고, 2030년까지 연률 4.16%로 성장이 예측되고 있습니다. 중국만으로도 4억 5,300만대의 자동차를 보유하고 있으며, 2024년에는 3,583만대의 신규 등록을 기록하고 있으며, 방대한 팩토리 필 수요와 거대한 서비스 마켓플레이스가 결합되어 있습니다. ASEAN 각국 정부는 EV 조립 허브를 육성하고 있습니다. 태국의 동부 경제 회랑 계획은 쉘사를 움직여 태국의 그리스 생산 능력을 3배로 끌어올려 지역 공급의 탄력성을 확보했습니다. 베트남과 인도네시아에서는 이륜차의 가구 보급률이 70%를 넘어, 이륜차용 유지의 판매량이 증가.

북미는 완만하면서도 안정된 성장에 기여. EV의 판매 대수는 연간 140만대를 넘지만, 사용후 차량의 8% 미만에 그치고, 2030년까지 대규모 내연 기관 차량이 유지됩니다. OEM은 API SQ 합성유를 중시하고 드레인 간격은 10,000마일을 넘기 때문에 퀵루브 체인은 재고를 저점도 처방으로 업그레이드하도록 촉구하고 있습니다.

유럽에서는 신차 등록 대수가 가로임에도 불구하고 18-28년차의 자동차 보유 대수가 윤활유 수요를 지지하고 있습니다. 이 대륙은 CO2 배출량 규제의 선구자로, PSA, VW 508/509, ACEA C6 사양에 뒷받침된 0W-20 및 0W-16 오일의 채택에 박차를 가하고 있습니다. 30,000km까지 연장된 서비스 인터벌은 프리미엄 등급 구매를 촉구하고 판매량 감소를 부분적으로 상쇄했습니다.

중동 및 아프리카와 남미는 현재 세계 판매량에 차지하는 비율이 낮은 것, 큰 성장을 전망하고 있습니다. 아프리카 23개국에서 Vivo Energy의 브랜드 윤활유 확대와 인도의 쉘 Raj Petro 인수는 남남 경쟁의 추세를 돋보이게 합니다. 인프라 정비, 농업 기계화, 광업 프로젝트는 분진 및 높은 주변 온도에 강한 유압 작동유 및 대형 엔진 오일에 대한 수요를 창출하고 있습니다.

The Automotive Lubricants Market size is estimated at 23.23 billion liters in 2025, and is expected to reach 28.01 billion liters by 2030, at a CAGR of 3.81% during the forecast period (2025-2030).

Growth is anchored by an aging global vehicle parc in developed regions, a steady influx of two-wheelers and commercial vehicles in emerging economies, and the sector's pivot toward premium synthetics that improve fuel economy and extend drain intervals. Asia-Pacific remains the core demand center thanks to rising ownership levels and local manufacturing investments, while North America and Europe rely on vehicle longevity to sustain aftermarket sales. Competitive intensity stays moderate: Shell led for the 18th straight year in 2024, but regional blenders gain ground through local capacity additions and tailored formulations. Headwinds such as accelerating electric-vehicle (EV) penetration-31.4 million units on Chinese roads in 2024-and OEM-specified long-drain intervals are mitigated by the higher unit values of API SQ and similar low-viscosity synthetics.

Vehicle longevity is reshaping lubricant demand profiles. Semiconductor shortages and inflation have slowed vehicle replacement rates in the US, prompting owners to increase oil-change frequency and invest in higher-quality synthetic oils. Europe's fleet is even older-18.1 years in the West and 28.4 years in the East-driving more workshop visits and raising per-vehicle lubricant consumption. Older engines suffer seal degradation, thermal stress, and contamination, all of which accelerate oil degradation and spur demand for premium base stocks. Maintenance outlays for vehicles aged 6-15 years rose from USD 514 to USD 537 in just one year, underscoring the link between age and spend. Scrappage has fallen to 4.20%, the lowest in two decades, prolonging aftermarket revenue streams. Higher-value synthetics now dominate service bays as owners seek extended protection and lower total cost of ownership.

Emerging economies offset EV-related volume erosion in mature markets. China's motor-vehicle stock reached 453 million units, supported by 35.83 million new registrations in 2024. Two-wheeler ownership continues to surge in India and Southeast Asia, propelled by urban congestion relief and affordable mobility. Commercial fleets running e-commerce and last-mile delivery routes accumulate higher mileage, boosting drain-frequency multiples. Domestic automakers in these regions collaborate with local blenders, allowing agile development of cost-effective oils tailored to varied fuel quality and climate extremes. As a result, the automotive lubricants market keeps expanding even amid global moderation.

EVs remove crankcase oils and many driveline fluids from service menus. China logged 31.4 million new-energy vehicles on its roads by end-2024, up 51.49% year-on-year. The IEA projects global stock could eclipse 250 million by 2030, cutting oil demand by up to 4.3 million bbl/d. Nonetheless, EVs introduce new niches: esters for e-motor bearings, dielectric coolants, and gear greases optimized for high RPM and electromagnetic compatibility. For suppliers, the challenge shifts from volume to value as specialized fluids command two-to-three-fold price premiums over conventional engine oil.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Engine oil held 58.61% of 2024 volumes, anchoring the automotive lubricants market through ubiquitous use in spark-ignition and compression-ignition engines. Larger sump capacities in light trucks and off-highway machinery amplify its share. Transmission fluids, hydraulic oils, and gear oils serve narrower applications yet remain vital for manual boxes, wet brakes, and power-steering circuits. Greases, though just a fraction of the automotive lubricants market size, are the fastest riser at a 4.28% CAGR as EVs require dedicated bearing greases that handle high RPM and electrical pitting. Suppliers blend synthetic esters and polyurea thickeners to deliver conductivity control and thermal stability, elevating product mix value.

The segment's revenue mix swings toward synthetics as API SQ-compliant oils gain traction. Ultra-low viscosity formulations such as 0W-16 and 0W-12 enable OEMs to meet fleet-average CO2 targets, especially in Japan and Europe. Even within heavy-duty oils, the shift from 15W-40 to 5W-30 illustrates demand for thinner, high-HTHS blends that cut fuel costs. As viscosity grades narrow, additive packages diversify-boron esters, molybdenum disulfide, and ashless detergents become cornerstones in next-generation SKUs. The automotive lubricants market therefore balances declining unit volumes against richer per-unit margins.

The Automotive Lubricants Market Report is Segmented by Product Type (Engine Oil, Transmission and Gear Oil, Hydraulic Fluids, Greases), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Motorcycles), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Asia-Pacific dominated the automotive lubricants market with a 42.25% share in 2024 and is forecast to grow 4.16% per year through 2030. China alone hosts 453 million vehicles and recorded 35.83 million new registrations in 2024, pairing vast factory-fill demand with a colossal service marketplace. ASEAN governments nurture EV assembly hubs; Thailand's Eastern Economic Corridor plans drove Shell to triple Thai grease capacity, ensuring regional supply resilience. Two-wheeler penetration surpasses 70% of households in Vietnam and Indonesia, bolstering motorcycle-oil volumes.

North America contributes to stable if modest growth. EV sales exceed 1.40 million units annually yet remain below 8% of in-service vehicles, preserving a sizeable internal-combustion fleet through 2030. OEMs emphasize API SQ synthetics with drain intervals topping 10,000 miles, prompting quick-lube chains to upgrade inventories to low-viscosity formulations.

Europe's 18-28 year car fleet sustains lubricant demand despite flat new-car registrations. The continent pioneers CO2 cap compliance, spurring adoption of 0W-20 and 0W-16 oils backed by PSA, VW 508/509, and ACEA C6 specifications. Extended-service intervals of up to 30,000 km partially offset volume loss by encouraging premium-grade purchases.

The Middle East & Africa and South America jointly contribute a smaller share of the global volume today but deliver outsized upside. Vivo Energy's branded-lube expansion across 23 African nations and Shell's Raj Petro acquisition in India highlight a south-south competitive trend. Infrastructure build-out, agricultural mechanization, and mining projects generate demand for hydraulic fluids and heavy-duty engine oils resilient to dust and high ambient temperatures.