ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

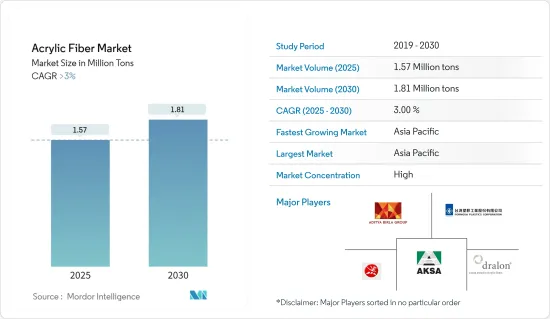

아크릴 섬유 시장 규모는 2025년에 157만 톤으로 추정되고, 2030년에는 181만 톤에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 3%를 초과할 것으로 예측됩니다.

2021년 COVID-19의 대유행으로 기업, 제품, 제조시설이 둔화되고 경제활동이 저하되었기 때문에 시장은 부정적인 영향을 받았습니다. 그러나 예측 기간 동안 시장은 회복될 것으로 보입니다.

주요 하이라이트

시장 성장을 가속하는 주요 요인으로는 의류 수요 상승과 산업 용도 확대를 들 수 있습니다.

반면에, 폴리에스테르와 같은 대체품 및 아크릴 섬유의 생산에 관한 세계적으로 엄격한 규제가 시장 성장을 방해할 것으로 예상됩니다.

그러나 아크릴지의 성장 기회와 미래 시장은 예측 기간 동안 충분한 성장 기회를 제공할 것으로 기대됩니다.

아시아태평양은 아세안 국가와 인도의 높은 수요로 인해 아크릴 섬유 시장을 독점하고 있습니다.

아크릴 섬유 시장 동향

시장을 독점하는 양모 부문

의류에 양모를 사용하는 역사는 고대까지 거슬러 올라갑니다. 양모는 주름이 쉽게 지지않고 흡습성과 보온성 등의 뛰어난 특성을 가지고 있습니다. 양모의 큰 특징은 시간이 지남에 따라 변형에서 회복한다는 점입니다. 그러므로 이 섬유로 만든 의류는 매력적입니다.

100% 양모 섬유로 짠 직물은 스웨터, 후드티, 부츠, 부츠 안감, 모자, 장갑, 운동복, 카펫, 담요, 롤러 브러쉬, 의자 패브릭, 바닥 러그, 보호복, 가발, 붙임머리 등 의류품 제조의 표준이 되고 있습니다.

아크릴 섬유의 대부분은 양모와 아크릴 혼방에 사용되며 매우 인기가 있습니다. 양모 55%와 아크릴 45%의 혼방은 원형 니트 제품에 사용됩니다. 이 혼방은 특히 스포츠웨어 제조에 사용되며 손질의 용이성, 내구성, 외관 유지, 색상 스타일링, 부드러운 촉감 등의 특징이 있습니다.

세계적으로 요구에 따라 다양한 블렌드가 사용되고 있으며 50/50과 70/30의 아크릴 양모 혼방은 저렴하고 보기 좋으며 취급하기 쉬운 의류에 인기가 있습니다. 아크릴 양모 50/50 혼방은 내구성과 보형성이 뛰어난 경량 의류에, 아크릴 양모 70/30 혼방은 슬랙스에 사용됩니다.

국제양모섬유기구에 따르면, 양모 섬유의 세계 최대 구매자는 여전히 중국이지만 미국에서도 양모 수요가 증가하고 있습니다. 2022년 11월까지 1년 동안 미국에 반입된 양모 의류 양은 2021년 동시기에 비해 47% 증가했습니다.

그러므로 양모 부문에서 아크릴 섬유 수요 증가는 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

중국이 아시아태평양 시장을 독점

중국은 세계 최대의 아크릴 섬유 생산국으로 세계 아크릴 섬유 생산량의 30% 이상의 점유율을 차지하고 있습니다. 아세안 국가, 유럽, 미국 및 일본을 중심으로 한 국내외 시장 수요로 인해 중국 섬유 산업은 해마다 성장하고 있습니다.

이란, 인도, 베트남, 파키스탄, 아랍에미리트(UAE)는 중국이 아크릴 섬유를 수출하는 최대 시장입니다. 또한 일본, 독일, 태국, 한국, 튀르키예 등의 나라에서도 아크릴 섬유를 수입하고 있습니다.

중국은 세계 최대의 섬유 생산 수출국입니다. 세계 섬유 수출 총액 중 금액 기준으로 약 43%의 점유율을 차지하고 있습니다. 따라서 중국 의류산업의 성장이 아크릴섬유 시장을 밀어올릴 것으로 예상됩니다.

중국은 섬유 부문에서 현저한 성장을 이루고 있습니다. 중국 국가통계국에 따르면 2023년 중국 주요 섬유기업의 총수익은 전년대비 7.2% 증가했습니다. 2023년 중국의 섬유제품 및 의류품 수출액은 지난 최고 2,936억 달러에 달했습니다.

따라서 이러한 모든 시장 동향으로 볼 때 예측 기간 동안 중국의 아크릴 섬유 시장에 대한 수요는 상승할 것으로 예상됩니다.

아크릴 섬유 산업의 세분화

아크릴 섬유 시장은 통합된 채로 유지되고 있습니다. 시장의 주요 기업으로는 Aksa Akrilik Kimya Sanayii AS, Dralon, Jilin Chemical Fiber Group, Aditya Birla Management Corporation Pvt.Ltd, Formosa Plastics Corporation 등이 있습니다(순서부동).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

촉진요인

의류에 대한 높은 수요

산업용도 증가

기타 촉진요인

억제요인

폴리에스테르와 같은 대체품의 이용가능성

아크릴 섬유 생산에 관한 세계적인 엄격한 규제

가치사슬 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(시장 규모(수량 기준))

형태

스테이플

필라멘트

혼방

양모

면

기타 혼방(셀룰로오스)

용도

의류

가정용 가구

산업용

기타 용도(가구 패브릭)

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

노르딕

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%) 분석

주요 기업의 전략

기업 프로파일

Aditya Birla Management Corporation Pvt. Ltd

Aksa Akrilik Kimya Sanayii AS

China Petrochemical Corporation(Sinopec)

Dralon

Formosa Plastics Corporation

Indian Acrylics Limited

Japan Exlan Co., Ltd

Jiangsu Zhongxin Resources Group

Jilin Chemical Fiber Group Co. Ltd

Kaltex

Kaneka Corporation

Mitsubishi Chemical Corporation

Pasupati Acrylon

PetroChina Company Limited

Taekwang Industrial Co. Ltd

Toray Industries Inc.

Vardhman Acrylics Ltd

제7장 시장 기회와 앞으로의 동향

아크릴지의 장래 시장

기타 기회

CSM

영문 목차

영문목차

The Acrylic Fiber Market size is estimated at 1.57 million tons in 2025, and is expected to reach 1.81 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2021, as the pandemic resulted in the slowdown of businesses, products, and manufacturing facilities, resulting in less economic activity. However, the market is expected to recover during the forecast period.

Key Highlights

The major factors driving the growth of the market studied include the high demand for apparel and increasing industrial applications.

On the flip side, the availability of substitutes like polyester and stringent regulations worldwide on the production of acrylic fiber are expected to hinder the growth of the market.

However, growing opportunities and the future market for acrylic paper are expected to offer ample growth opportunities during the forecast period.

Asia-Pacific dominated the acrylic fiber market due to high demand from the ASEAN countries and India.

Acrylic Fiber Market Trends

The Wool Segment to Dominate the Market

The use of wool for clothing dates back to ancient times. Wool has outstanding properties, such as resistance to wrinkles, moisture absorption, and warmth. A significant feature of wool is its ability to recover from deformation over time. Hence, clothing made from these fibers is attractive.

Fabrics woven or knitted with 100% wool fiber have become a standard in making apparel, such as sweaters, hoodies, boots, boot lining, hats, gloves, athletic wear, carpeting, blankets, roller brushes, upholstery, area rugs, protective clothing, wigs, and hair extensions.

A majority of acrylic fiber is used to make wool and acrylic blends, which are very popular. A blend of 55% wool and 45% acrylic fiber is used to make circular knit goods. This blend is particularly used in making sportswear, with characteristics like ease of care, durability, appearance retention, color styling, and palatability.

Different blends are used worldwide depending on the requirements. The 50/50 and 70/30 acrylic wool blends are popular among those apparel that are inexpensive, look good, and are easy to handle. The 50/50 acrylic wool blend is used to make lightweight apparel that has excellent durability and shape retention, while the 70/30 acrylic wool blend is used to make slacks.

According to the International Wool Textile Organization, China remains the top buyer of wool fiber globally, yet there is an increasing demand for wool in the United States. During the year that concluded in November 2022, the quantity of wool clothing brought into the United States increased by 47% compared to the same period in 2021.

Hence, increasing demand for acrylic fiber in the wool segment is expected to dominate the market over the forecast period.

China to Dominate the Market in Asia-Pacific

China is the largest producer of acrylic fibers in the world, accounting for a share of more than 30% of global acrylic fiber production. Owing to the demand from domestic and international markets, primarily from ASEAN countries, Europe, the United States, and Japan, the textile industry in China has expanded over the years.

Iran, India, Vietnam, Pakistan, and the United Arab Emirates are some of the largest markets where China exports acrylic fibers. The country also imports acrylic fiber from countries like Japan, Germany, Thailand, South Korea, and Turkey.

China is the largest textile-producing and exporting country in the world. It holds about 43% share of the world's total textile exports in terms of value. Thus, the growth in China's clothing industry is anticipated to boost the market for acrylic fibers.

The country has witnessed significant growth in the textiles segment. According to the National Bureau of Statistics of China, in 2023, the combined earnings of China's leading textile companies increased by 7.2% compared to the previous year. In 2023, China's exports of textiles and clothing reached a record high of USD 293.6 billion.

Hence, all such market trends are expected to add to the demand for the acrylic fibers market in China during the forecast period.

Acrylic Fiber Industry Segmentation

The acrylic fiber market is consolidated in nature. Some of the major players in the market include (not in any particular order) Aksa Akrilik Kimya Sanayii AS, Dralon, Jilin Chemical Fiber Group Co. Ltd, Aditya Birla Management Corporation Pvt. Ltd, and Formosa Plastics Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 High Demand for Use in Apparel

4.1.2 Increasing Industrial Application

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Availability of Substitutes, like Polyester

4.2.2 Stringent Regulations Worldwide on the Production of Acrylic Fiber

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Form

5.1.1 Staple

5.1.2 Filament

5.2 Blending

5.2.1 Wool

5.2.2 Cotton

5.2.3 Other Blendings (Cellulose)

5.3 Application

5.3.1 Apparel

5.3.2 Household Furnishing

5.3.3 Industrial

5.3.4 Other Applications (Upholstery)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Spain

5.4.3.6 NORDIC

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 United Arab Emirates

5.4.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Aditya Birla Management Corporation Pvt. Ltd