화학제품 주입 정량 펌프 및 밸브 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Chemical Injection Metering Pumps And Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640426

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

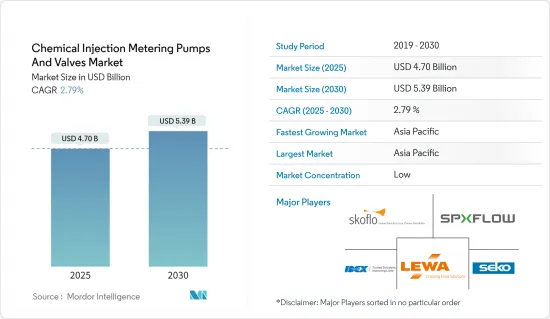

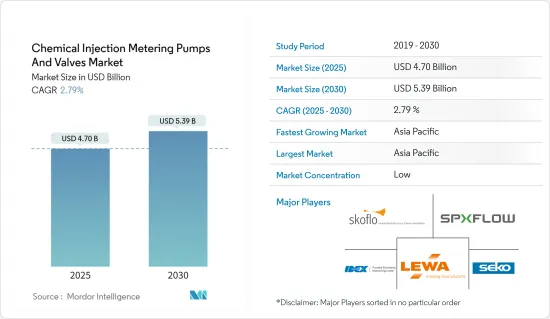

화학제품 주입 정량 펌프 및 밸브 시장 규모는 2025년 47억 달러로 추정됩니다. 예측기간(2025-2030년)의 CAGR은 2.79%를 나타낼 전망이며, 2030년에는 53억 9,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 발생으로 2020년에는 세계 봉쇄, 제조 활동 및 공급망의 혼란, 생산 정지가 발생하여 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 상황이 회복되기 시작하여 시장의 성장 궤도가 회복되었습니다.

주요 하이라이트

시장 조사의 주요 촉진요인 중 하나는 폐수 처리 용도에 대한 수요의 가속입니다.

그러나 일부 용도에서는 유지 보수 및 교체 비용이 높아 시장 성장을 방해할 것으로 예상됩니다.

에너지, 전력, 화학산업이 시장을 독점하고 있으며 예측기간 동안에도 성장이 예상됩니다. 상수·폐수 처리 산업은 향후 수년간 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

아시아태평양이 시장을 독점하고, 북미, 유럽이 이어지며, 중국, 일본, 인도 등의 국가에 의한 소비가 가장 많습니다.

제약 산업에서의 수요의 높아짐이 향후 기회가 될 것 같습니다.

화학제품 주입 정량 펌프 및 밸브 시장 동향

에너지, 전력, 화학이 시장을 독점

에너지, 전력, 화학은 주입 정량 펌프 및 밸브 시장의 주요 최종 사용자 부문입니다. 종이 펄프 산업도이 부문에 포함됩니다.

화학 산업은 최종 제품 또는 중간 제품의 합성으로 구성됩니다. 정량 펌프와 밸브는 다양한 온도 및 화학 처리 압력에서 다양한 독성 화학물질을 처리하는 데 도움이 됩니다.

화학제품 주입 시스템은 발전에도 사용됩니다. 황산 제2철 및 황산과 같은 화학물질은 물을 보일러용 초순수로 바꾸기 위해 정확한 측정이 필요합니다.

프랑스에서는 미국과 중동 국가의 수입이 석유 제품 수요의 대부분을 충족합니다. 프랑스에서는 에너지의 약 60%가 화석 자원으로 사용됩니다. 에너지 원은 주로 석유 제품, 천연 가스, 석탄입니다. 따라서 에너지 생산은 원유가 사우디아라비아, 러시아, 카자흐스탄, 알제리, 나이지리아에서 수입에, 가스는 러시아, 노르웨이, 나이지리아, 네덜란드에서 수입에 따라 달라집니다.

프랑스에서 소비되는 석유의 95% 이상은 기타 국가에서 수입됩니다. 석유의 대부분은 러시아에서 수입되어 프랑스 수요를 충족합니다. 그러나 러시아와 우크라이나 전쟁이 시작된 이래 EU는 유럽 시장에서 러시아 석유를 쫓는 방법을 모색하고 있습니다. 프랑스는 EU 최대의 석유 수입국 중 하나이기 때문에 프랑스 정부는 이미 아랍에미리트(UAE)과 러시아 석유 구매를 대체하기위한 협의를 강화하고 있습니다.

대부분의 석유화학시설에서는 발전열을 이용하여 보일러를 가동시켜 현장의 전력 수요를 충족하고 있습니다.

미국 인구조사국에 따르면, 광업·채석업의 수익은 2021년 136억 8,000만 달러에 비해 2022년에는 143억 9,000만 달러에 달했습니다. 이 부문의 수익은 2023년에 152억 5,000만 달러에 달할 것으로 예상됩니다.

광업과 야금은 캐나다의 주요 산업입니다. 캐나다는 60개 이상의 금속 및 광물을 세계 각국에 공급하고 있습니다. 광업은 혁신과 신기술에 투자하고 이 분야를 빠르게 재건하고 있습니다. 광업은 또한 통합을 보여주고 향후 몇 년 동안 이 산업의 성장 전망에 대한 추측을 불러 일으켰습니다.

화력발전소나 원자력발전소 등의 전력산업에서는 보일러 시스템에 급수하기 위해 화학제품이 필요하게 되는 경우가 많습니다.

투자가 증가함에 따라 에너지, 전력 및 화학 부문의 성장은 예측 기간 동안 조사된 시장 수요를 촉진하는 것으로 보입니다.

아시아태평양에서는 중국이 시장을 독점

아시아태평양은 화학제품 주입 정량 펌프와 밸브 수요를 지배할 것으로 예상됩니다. 중국에서만 아시아태평양 시장의 약 35%를 차지합니다.

정량 펌프와 밸브의 소비는 석유 및 가스로 높고, 이 나라에서는 하류 생산이 증가하고 있으며, 석유 화학제품의 생산 능력도 증가하고 있습니다.

중국에서 두드러진 다른 최종 사용자 산업은 화학 공장이며, 시장의 많은 대기업은 중국에서 화학 공장을 가지고 있으며, 그들은 또한 화학 주입 정량 펌프와 밸브의 소비를 증가 생산 능력을 증가하고 있습니다. 다른 주요 산업은 국내 수처리 시설, 다양한 산업에서 사용됩니다.

폐수 처리는 주로 석탄, 철강, 철강 산업이 일상 활동에 참수를 필요로 하기 때문입니다. 중국 북부에는 국내 석탄 관련 산업의 약 90%가 있습니다.

중국 정부는 이 지역의 귀중한 수자원을 개선하기 위해 물의 사용과 배출에 관한 규제를 제정했습니다. 최근 정부는 화북의 석탄·화학공장에 대한 규제를 강화하고 제로액체 배출(ZLD)을 의무화하고 있습니다.

중국 식음료 산업은 거대하며 국내 경제에서 중요한 역할을 하고 있습니다. 구매력 있는 중산계급 인구가 증가하고 식품의 안전성과 품질에 대한 관심이 높아지면서 식음료산업은 앞으로도 계속 성장할 것으로 예상됩니다.

석유 및 가스 업스트림 산업에서 제조업체는 항상 생산 능력, 전체 프로세스 효율성 및 기계 가동 중지 시간 개선을 추구합니다. 석유 및 가스 회사는 생산량 증가, 부식 감소, 석유 및 가스·물 분리, 탐사 및 회수 활동의 수익성 향상을 위해 화학 주입 정량 펌프와 밸브를 사용합니다.

중국은 세계 제2위의 석유 및 가스 소비국이지만, 생산국으로서는 세계 제6위에 지나지 않습니다. 석유의 대소비국인 중국의 석유소비량은 성장률을 변화시키면서 해마다 증가하고 있습니다. 그러나 석유 공급이 아직 수요를 충족시키지 못했기 때문에 중국은 주로 수입에 의존하고 있습니다.

예측 기간 동안 위에서 언급한 다양한 최종 사용자 산업의 성장은 국내 화학 주입 정량 펌프와 밸브에 대한 수요를 높일 것으로 예상됩니다.

화학제품 주입 정량 펌프 및 밸브 산업 개요

세계의 화학제품 주입 정량 펌프 및 밸브 시장은 매우 세분화되어 있으며 주요 기업 5개사의 시장 점유율은 매우 작습니다. 주요 기업으로는 Idex Corporation, SPX Flow, Lewa GmbH, SkoFlo Industries Inc., Seco SpA 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

폐수 처리 용도로부터 수요의 가속

환경 규제를 위한 견고한 운영 절차

기타 촉진요인

성장 억제요인

일부 용도에 있어서 높은 유지보수 및 교체 비용

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(규모별)

펌프 유형

다이어프램

피스톤/플런저

기타 펌프 유형

최종 사용자 산업

에너지, 전력, 화학

석유 및 가스

물 및 폐수 처리

음식

제약

지역

아시아태평양

중국

인도

일본

한국

아세안 국가

호주 및 뉴질랜드

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

러시아

스페인

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작사업, 제휴, 협정

시장 랭킹/공유(%) 분석

주요 기업의 전략

기업 프로파일

Cameron(Schlumberger)

Hunting PLC

Idex Corporation

ITC Dosing Pumps

Lewa GmbH

McFarland-Tritan LLC

Milton Roy

ProMinent

Seepex GmbH

Seko SpA

SkoFlo Industries Inc.

SPX FLOW Inc.

Swelore Engineering Pvt Ltd.

제7장 시장 기회와 앞으로의 동향

제약산업 수요 증가

기술적으로 진보된 화학물질 주입 시스템의 개발

KTH

영문 목차

영문목차

The Chemical Injection Metering Pumps And Valves Market size is estimated at USD 4.70 billion in 2025, and is expected to reach USD 5.39 billion by 2030, at a CAGR of 2.79% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

One of the major factors driving the market study is the accelerating demand for wastewater treatment applications.

However, high maintenance and replacement costs in some applications are expected to hinder the market's growth.

The energy, power, and chemicals industry dominated the market and is expected to grow during the forecast period. The water and wastewater treatment industry is expected to register the highest CAGR in the coming years.

Asia-Pacific dominated the market, followed by North America and Europe, with the largest consumption from countries such as China, Japan, and India.

Growing demand from the pharmaceutical industry will likely act as an opportunity in the future.

Chemical Injection Metering Pumps & Valves Market Trends

Energy, Power, and Chemicals to Dominate the Market

Energy, power, and chemicals are major end-user segments in the injection metering pumps and valves market. Even the pulp and paper industry is considered in this segment.

The chemical industry consists of the synthesis of finished or intermediate products. Metering pumps and valves help handle various toxic chemicals at different temperatures and chemical processing pressures.

Chemical injection systems also find major use in power generation. Chemicals, such as ferric sulfate and sulphuric acid, are needed in precise measurements to transform water into ultra-pure water for boilers.

In France, imports from the United States and Middle Eastern countries meet most of the demand for petroleum products. Around 60% of the energy is utilized in the form of fossil resources in France. Energy is primarily derived from petroleum products, natural gas, and coal. Hence energy generation depends on imports from Saudi Arabia, Russia, Kazakhstan, Algeria, and Nigeria for crude oil while upon Russia, Norway, Nigeria, and the Netherlands for gas.

Over 95% of the oil consumed in France is imported from other nations. A large share of oil is imported from Russia to fulfill the country's demand. However, since the onset of the Russia-Ukraine war, European Union has been finding ways to push out Russian oil from the European market. Since France is one of the largest oil importers in the European Union, the French government has already strengthened talks with United Arab Emirates (UAE) to replace Russian oil purchases.

Most petrochemical facilities use generated heat to run boilers to meet site power requirements.

As per the United States Census Bureau, revenue in mining and quarrying amounted to USD 14.39 billion in 2022, compared to USD 13.68 billion in 2021. The revenue from this sector is projected to amount to USD 15.25 billion in 2023.

Mining and metallurgy are key industries in the country. Canada supplies over 60 metals and minerals to different countries worldwide. The mining industry invests in innovation and new technologies, rapidly reshaping the sector. The mining industry also witnessed consolidations, which led to speculations regarding the growth prospects for the industry in the coming years.

Power industries, such as thermal and nuclear plants, often require chemicals to inject the feed water into the boiler system.

The growth in the energy, power, and chemicals sectors with increasing investments is likely to drive the demand in the market studied during the forecast period.

China to Dominate the Market in Asia-Pacific Region

Asia-Pacific region is expected to dominate the demand for chemical injection metering pumps and valves. China alone accounts for about 35% of the market in the Asia-Pacific region.

The consumption of metering pumps and valves is high in oil and gas; the downstream production has increased in the country, which has also increased the production capacities of petrochemicals; therefore, it will augment the consumption of chemical injection metering pumps and valves in the country.

The other end-user industry prominent in China is the chemical plants, many big companies in the market have their chemical plants in China, and they have even increased their production capacities, which will increase the consumption of chemical injection metering pumps and valves. The other major industry is a water treatment facility in the country, used in different industries.

Wastewater treatment is mainly because the coal, steel, and iron industries require fresh water for daily activities. North China has approximately 90% of the country's coal-based industries.

The Chinese government has enacted water use and discharge regulations to improve the region's precious water resources. Recently, the government has tightened the rules for coal and chemical plants in North China, which require zero-liquid discharge (ZLD).

China's food and beverage industry is enormous and plays an important role in the country's economy. The food and beverages industry is expected to continue growing because of the increasing middle-class population with more purchase power and growing attention to food safety and quality.

In the upstream Oil & Gas industry, manufacturers constantly seek to improve their production capacities, overall process efficiency, and machinery downtime. Oil and gas companies use chemical Injection metering pumps and valves to increase production, reduce corrosion, separate oil/gas/water, and improve the profitability of all exploration and recovery efforts.

China is the world's second-largest consumer of oil and gas but only the sixth-largest producer of the same. As a big oil consumer, China's oil consumption is increasing yearly with fluctuating growth rates. However, China mainly relies on imports because the oil supply still cannot meet the demand.

The growth in those mentioned above various end-user industries in the forecast period is expected to boost the demand for chemical injection metering pumps and valves in the country.

Chemical Injection Metering Pumps & Valves Industry Overview

The global chemical injection metering pumps and valves market is highly fragmented, with the top 5 players accounting for a very small market share. The major companies include Idex Corporation, SPX Flow, Lewa GmbH, SkoFlo Industries Inc., and Seko SpA.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Accelerating Demand from Wastewater Treatment Applications

4.1.2 Robust Operational Procedures for Regulating Environmental Concerns

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Maintenance and Replacement Costs in Some Applications

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Pump Type

5.1.1 Diaphragm

5.1.2 Piston/Plunger

5.1.3 Other Pump Types

5.2 End-user Industry

5.2.1 Energy, Power, and Chemicals

5.2.2 Oil and Gas

5.2.3 Water and Wastewater Treatment

5.2.4 Food and Beverage

5.2.5 Pharmaceutical

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 ASEAN Countries

5.3.1.6 Australia and New Zealand

5.3.1.7 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Russia

5.3.3.6 Spain

5.3.3.7 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking/Share (%) Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Cameron (Schlumberger)

6.4.2 Hunting PLC

6.4.3 Idex Corporation

6.4.4 ITC Dosing Pumps

6.4.5 Lewa GmbH

6.4.6 McFarland-Tritan LLC

6.4.7 Milton Roy

6.4.8 ProMinent

6.4.9 Seepex GmbH

6.4.10 Seko SpA

6.4.11 SkoFlo Industries Inc.

6.4.12 SPX FLOW Inc.

6.4.13 Swelore Engineering Pvt Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Demand in the Pharmaceutical Industry

7.2 Development of Technologically Advanced Chemical Injection Systems