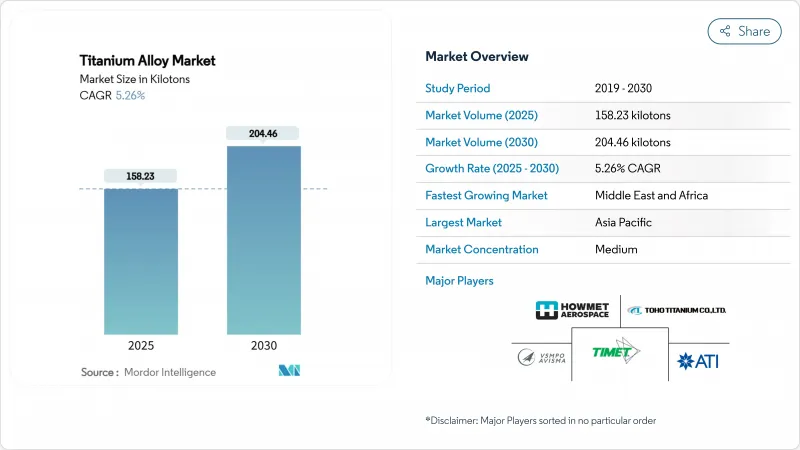

티타늄 합금 시장 규모는 2025년에 158.23킬로톤으로 추정되고, 2030년에는 204.46킬로톤에 이를 것으로 예측되며, 예측 기간(2025-2030년) CAGR 5.26%로 성장할 전망입니다.

보잉과 에어버스의 안정적인 수주 잔여, 국방 조달 사이클의 부활, 의료용 임플란트의 고객 기반 확대가 수요를 지지하고 있습니다. 성능의 지속성은 티타늄의 높은 강도 대 중량비, 내식성, 생체적합성에 달려 있으며, 이러한 특성은 중요한 용도에서 높은 제조 비용을 능가하고 있습니다. 생산자는 공급 병목 현상을 완화하기 위해 수소 보조 환원과 첨가제 제조를 통해 용융 능력을 추가하는 반면 고객은 지정학적 위험을 줄이기 위해 조달을 다양화하고 있습니다. 비용 절감을 위한 기술 혁신과 연료 효율적인 항공기에 대한 규제의 뒷받침은 티타늄 합금 시장의 성장 시나리오를 더욱 강화합니다.

15,000대가 넘는 민간 항공기의 주문은 경량화가 연료 절약으로 이어지는 구조, 착륙 장치, 엔진 부품에 티타늄을 집중시키고 있습니다. ATI는 2025년 1분기 수익의 66%를 항공우주 및 방위 분야에서 얻고 있으며, 에어버스사와 5년간 10억 달러 공급 계약을 체결하고 있습니다. 하우멧 에어로스페이스는 엔진 수요의 급증으로 2024년 3분기 민간 항공우주 분야 매출이 17% 증가했습니다. 티타늄의 강도는 현재 제트 엔진 중량의 15-25%에 달하며, 방위 프로그램에서는 스텔스성과 내구성을 위해 합금이 지정되어 있습니다. 러시아산 원료로부터의 다양화가 일본이나 중동 공급업체와의 새로운 파트너십을 촉진해, 티타늄 합금 시장의 생산 재편을 강화하고 있습니다.

방위 계획의 입안자는 방호를 희생하지 않고 항속거리 및 적재량을 향상시키기 위해, 장갑, 드라이브 트레인, 서스펜션에 있어서 강철을 티타늄으로 대체하는 것이 늘고 있습니다. 미국 국방부에 의한 IperionX사에 대한 4,710만 달러의 상금은 안전하고 저비용의 티타늄 능력을 요구하는 국가적인 뒷받침을 강조하는 것입니다. 재료 사양을 조화시키는 NATO 규격은 국경을 넘은 수요를 증폭시켜, 티타늄 부품이 강철을 대체했을 경우의 15-20%의 연료 절약을 나타내는 실지 데이터가 있습니다. 첨단 제조는 부품 목록을 단축하고, 배치된 차량의 유지보수 부담을 줄이며, 티타늄 합금 시장의 장기적인 기세에 박차를 가합니다.

기존의 크롤링법에서는 1톤당 11-13MWh를 소비하기 때문에 티타늄의 가격은 알루미늄의 3-4배, 강철의 10-15배가 됩니다. 반응성 야금은 불활성 분위기와 특수 절삭액을 필요로 하며, 하류 기계 가공의 생산성을 방해합니다. 수소 어시스트 환원 경로는 더 낮은 온도를 약속하지만 상용화에는 이르지 못합니다. 이트륨 반응에 의한 산소 제거를 위한 도쿄 대학의 기술은 비용 절감 가능성을 제공하지만, 산업적 스케일링에는 수년이 걸립니다. 새로운 공정이 성숙할 때까지 높은 전환 비용이 티타늄 합금 시장의 잠재력을 제한합니다.

베타 합금은 2030년까지 연평균 복합 성장률(CAGR) 6.14%로 성장할 것으로 예측되며, 알파 베타 등급은 2024년 티타늄 합금 시장 점유율의 51.67%를 유지했습니다. Ti-5553은 뛰어난 주조성을 나타내며 날개 캐리 스루와 랜딩 기어 구조에 필수적인 고강도 중량비를 실현합니다. 지르코늄과 하프늄을 포함한 높은 엔트로피 금속간 화합물의 조사는 8%의 소성 변형으로 1.5GPa의 항복 강도를 달성하여 극초음속 용도의 선택을 넓히고 있습니다.

현재 진행 중인 Additive Manufacturing의 전개는 니어넷 모양 생산을 가능하게 하고, 구매에서 비행까지의 비율을 최대 60% 삭감하며, 터빈 블레이드의 복잡한 냉각 채널 구조를 지원합니다. 베타 합금의 티타늄 합금 시장 규모는 분말 원자화 능력과 중요한 비행 하드웨어 인증 시험의 시너지 이익에 의해 지원되며, 전체량의 약 25%로 10년을 마무리하려고 합니다. 500℃를 넘는 알파 합금과 니어 알파 합금에 대한 병렬 관심은 가스 터빈과 우주 추진에 대한 수요를 유지합니다. 생산자가 진공 아크 재용해 매개변수를 표준화함에 따라 합금의 화학적 특성이 안정되고 항공우주 및 방위 프라임 간의 신뢰성이 향상됩니다.

티타늄 합금 보고서는 미세 구조별(알파 및 니어 알파, 알파 베타, 베타), 최종 사용자 산업별(항공우주, 자동차 및 조선, 화학 처리, 전력 및 해수 담수화, 의료 및 치과 임플란트 및 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분할됩니다. 시장 예측은 킬로톤으로 제공됩니다.

아시아태평양은 2024년 티타늄 합금 시장의 41.35%를 차지했고, 중국의 세계 금속 생산량의 60% 점유율이 그 주역입니다. 그러나 이 지역의 항공우주 인증 격차는 고가치 제트기 프로그램에 대한 즉각적인 침투를 억제하고 있습니다. 인도는 HAL과 DRDO와 협력하여 자체 스폰지 생산 능력을 확보하고 호주 광산업자는 밸류체인의 보다 멀리서 이폭을 확보하기 위해 강하에서 합금화를 모색하고 있습니다. 이러한 이니셔티브는 품질면에서 장애물이 남지만, 일반적으로 견조한 수량 증가를 지원합니다.

중동 및 아프리카는 5.94%의 연평균 복합 성장률(CAGR)로 확대되었으며, 사우디아라비아의 460억 달러의 광업 전략에서 이익을 얻고 있습니다. 이 전략은 2030년까지 광업의 GDP 점유율을 750억으로 인상시킬 전망이며, 왕국을 중립적인 티타늄 공급업체로 자리매김하는 것을 목표로 합니다. 북미의 소비량은 스폰지의 생산량이 적음에도 불구하고 높은 수준을 유지하고 있습니다. 노스캐롤라이나 주 캠버랜드 카운티는 수소 보조 환원으로 인한 국내 생산 능력을 재구성하기 위해 8억 6,700만 달러의 플랜트를 확보했습니다. 캐나다에서는 퀘벡의 수력 발전 일메나이트 사업이 저탄소 스폰지에 수직 통합을 모색하고 있습니다.

대서양의 다른 쪽에서는 유럽의 OEM이 제재 조치의 준수와 생산의 연속성을 양립하기 위해 카자흐스탄과 일본 공급업체와의 합작 협의를 진행하고 있습니다. EU의 중요한 원재료법은 노르웨이와 스페인에서 스폰지 프로젝트의 허가를 가속화하고 있습니다. 남미는 여전히 주로 원석 수출국이지만, 브라질의 국영개발은행은 기존 일메나이트 광산 근처의 다운스트림 합금 공장에 대한 공동대출에 관심을 보이고 있습니다. 전반적으로 공급 발자국의 변화는 티타늄 합금 시장의 형태를 계속 바꾸고 있습니다.

The Titanium Alloy Market size is estimated at 158.23 kilotons in 2025, and is expected to reach 204.46 kilotons by 2030, at a CAGR of 5.26% during the forecast period (2025-2030).

Consistent order backlogs at Boeing and Airbus, revived defense procurement cycles, and a widening medical-implant customer base anchor demand. Sustained performance hinges on titanium's high strength-to-weight ratio, corrosion resistance, and biocompatibility, traits that continue to outweigh its higher production cost in critical applications. Producers are adding melt capacity, often through hydrogen-assisted reduction or additive manufacturing, to alleviate supply bottlenecks, while customers diversify sourcing to mitigate geopolitical risk. Cost-down innovation and regulatory push for fuel-efficient aircraft further reinforce the growth narrative of the titanium alloy market.

Orders exceeding 15,000 commercial aircraft place titanium squarely in structural, landing-gear, and engine components, where weight reduction translates into fuel savings. ATI drew 66% of Q1 2025 revenue from aerospace and defense and locked in a five-year USD 1 billion supply pact with Airbus. Howmet Aerospace recorded 17% commercial-aerospace sales growth in Q3 2024 on surging engine demand. Titanium intensity now reaches 15-25% of a jet engine's weight, while defense programs specify the alloy for stealth and durability. Diversification away from Russian feedstock is driving new partnerships with Japanese and Middle Eastern suppliers, reinforcing the titanium alloy market's production realignment.

Defense planners increasingly swap steel for titanium in armor, drivetrains, and suspensions to boost range and payload without sacrificing protection. The U.S. Department of Defense's USD 47.1 million award to IperionX underscores a national push for secure, low-cost titanium capacity. NATO standards that harmonize material specifications amplify cross-border demand, and field data show 15-20% fuel savings when titanium components replace steel. Advanced manufacturing shortens part lists, easing maintenance burden for deployed vehicle fleets and fueling long-run momentum in the titanium alloy market.

The legacy Kroll route burns 11-13 MWh per ton, making titanium 3-4 times pricier than aluminum and 10-15 times pricier than steel. Reactive metallurgy demands inert atmospheres and specialized cutting fluids, hampering productivity in downstream machining. Hydrogen-assisted reduction pathways promise lower temperatures but remain pre-commercial. University of Tokyo techniques for oxygen removal via yttrium reactions offer potential cost savings, yet industrial scaling is several years. Until new processes mature, elevated conversion costs cap the full potential of the titanium alloy market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Beta alloys are projected to register a 6.14% CAGR through 2030, while Alpha-Beta grades retained 51.67% of the titanium alloy market share in 2024. Ti-5553 demonstrates superior castability, delivering high strength-to-weight ratios vital for wing-carry-throughs and landing-gear structures. Research into high-entropy intermetallics incorporating zirconium and hafnium achieves yield strengths of 1.5 GPa with 8% plastic strain, expanding options for hypersonic applications.

Ongoing additive-manufacturing deployments enable near-net-shape production, slashing buy-to-fly ratios by up to 60% and supporting intricate cooling-channel architectures in turbine blades. Beta alloys' titanium alloy market size is on track to close the decade at roughly 25% of overall volume, supported by synergistic gains in powder-atomization capacity and qualification tests for critical flight hardware. Parallel interest in Alpha and Near-Alpha alloys for temperatures above 500 °C preserves demand in gas turbines and space-propulsion contexts. As producers standardize vacuum-arc-remelting parameters, alloy chemistries stabilize, improving confidence among aerospace and defense primes.

The Titanium Alloy Report is Segmented by Microstructure (Alpha and Near-Alpha, Alpha-Beta, and Beta), End-User Industry (Aerospace, Automotive and Shipbuilding, Chemical Processing, Power and Desalination, Medical and Dental Implants, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Asia-Pacific commanded 41.35% of the titanium alloy market in 2024, anchored by China's 60% share of global metal output. However, the region's aerospace certification gap curtails immediate penetration into high-value jet programs. India collaborates with HAL and DRDO on indigenous sponge capacity, while Australian miners explore downstream alloying to capture margin farther along the value chain. These initiatives collectively support robust volume gains, although quality hurdles remain.

The Middle East and Africa region, expanding at a 5.94% CAGR, benefits from Saudi Arabia's USD 46 billion mining strategy, which aims to lift mining GDP share to 75 billion by 2030 and position the kingdom as a neutral titanium supplier. North American consumption stays high despite minimal sponge output. Cumberland County, North Carolina, secured a USD 867 million plant to rebuild domestic capacity with hydrogen-assisted reduction that could supply 10,000 tons annually once fully operational. In Canada, Quebec's hydro-powered ilmenite operations explore vertically integrating into low-carbon sponge.

Across the Atlantic, European OEMs juggle sanction compliance and production continuity, prompting joint-venture discussions with Kazakh and Japanese suppliers; the EU's Critical Raw Materials Act expedites permitting for sponge projects in Norway and Spain. South America remains largely a raw-ore exporter, but Brazil's state development bank signals interest in co-financing downstream alloy plants near existing ilmenite mines. Overall, shifting supply footprints continue to reshape the titanium alloy market.