ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

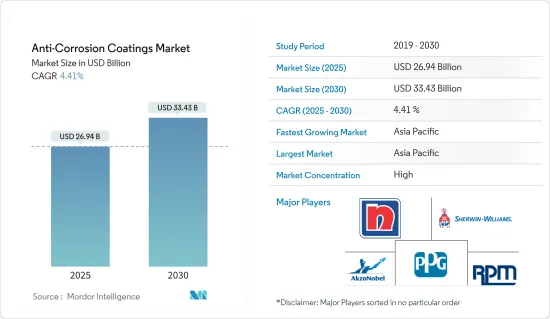

방청 코팅 시장 규모는 2025년에 269억 4,000만 달러로 추정되며 예측 기간(2025-2030년)의 CAGR은 4.41%로, 2030년에는 334억 3,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

COVID-19의 유행은 방청 코팅 부문에 부정적인 영향을 미쳤습니다. 세계 봉쇄와 정부의 엄격한 규칙으로 인해 대부분의 생산 기지가 폐쇄되어 치명적인 타격을 입었습니다. 그럼에도 불구하고 2021년 이후 사업은 회복되어 향후 수년간 크게 상승할 것으로 예상됩니다.

시장을 견인하는 주요 요인은 인프라 산업의 현저한 성장, 해양 산업 수요 증가, 아시아태평양과 북미의 석유 및 가스 활동 확대입니다.

휘발성 유기 화합물(VOC)과 관련된 규정은 조사된 시장의 성장을 방해할 것으로 예상됩니다.

신흥국의 인프라 산업에 대한 대규모 투자와 수성 코팅의 채용 확대는 방청 코팅 시장에 향후 현저한 성장 기회를 가져올 것으로 예상됩니다.

아시아태평양은 예측 기간 동안 이 지역의 다양한 최종 사용자 산업에 대한 투자가 증가하기 때문에 방청 코팅 시장을 독점할 것으로 예상됩니다.

방청 코팅 시장 동향

인프라 산업에서 수요 증가

인프라 부문은 시장의 최대 점유율을 차지하며 가장 빠르게 성장하는 부문으로 추정됩니다. 철도, 교량, 도로가 인프라의 주요 부문으로 기여하고 있습니다. 인구 급증과 인프라 프로젝트 증가가 방청 코팅 수요를 높일 것으로 예상됩니다.

아시아태평양과 북미에는 다양한 소규모 프로젝트가 확산되고 있습니다. 중국은 세계에서 가장 인구가 많은 나라일 뿐만 아니라 철도 이용자 수도 가장 많습니다.

또한 아시아태평양 도로 프로젝트도 방청 코팅의 소비를 늘릴 것으로 예상됩니다. 예를 들어, 도로교통·고속도로성에 의하면 현재 진행중인 바랏말라·파료지나에서는 화물 수송의 대부분을 도로에서 실시하기 위해 전체 길이 약 2만 6,000km의 경제 회랑의 개발이 진행되고 있습니다. 경제 회랑, GQ, NS-EW 회랑의 정비는 8,000km의 인터 회랑과 7,500km의 피더 루트의 건설에 의해 행해지고 있습니다.

인프라 개발에 대해서는 중국 브리핑에 따르면 2021년 말 중국 재정부(MoF)는 잉여유동성이 연초 투자에 박차를 가할 것으로 기대하여 2022년 할당액 중 2,296억 달러를 1분기에 사용하도록 사전 할당했습니다.

2023년 4월 세계 은행의 데이터에 따르면 인프라에 대한 민간 참여(PPI)는 약 917억 달러, 263개 프로젝트에 이르렀으며 2021년부터 23% 증가했습니다. 중저소득 국가에서는 2022년 인프라 투자가 회복된 것으로 확인되었습니다.

미국 운수부(USDoT)와 연방도로국(FHWA)에 따르면 2022-2030년에 걸쳐 약 1,200억 달러가 고속도로 및 교량에 할당되어 그중 약 2,800개의 교량이 이미 착수되고 있습니다. USDOT는 RAISE(Rebuilding American Infrastructure with Sustainability and Equity) 보조금으로 166개 프로젝트에 22억 달러를 투자했습니다. 이를 통해 철도, 항만, 도로, 교량, 복합 일관 운송의 현대화가 촉진되어 저렴하고 안전하며 지속 가능합니다.

앞서 언급한 요인들로 인해 예측 기간 동안 방청 코팅 수요가 증가할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

아시아태평양에서는 중국, 일본, 한국이 조선 산업을 선도하고 있지만 베트남, 인도, 필리핀에 새로운 해운 허브가 출현하고 있습니다.

호주 및 뉴질랜드는 모두 섬나라이며, 호주 해안선과 수로의 지리적 규모로부터 레저용, 상업용, 방어용의 선박이 많이 건조되고 있습니다.

중국은 세계 유수의 원유 수출입국입니다. 이 때문에 석유 및 가스 부문과 관련된 확대 활동에 영향을 미치는 변화가 있으며 중국의 방청 코팅 시장에 큰 영향을 줄 가능성이 높습니다.

미국 에너지 정보국에 따르면 중국은 2022년, 2030년과 2060년 기후 목표인 탄소 배출량의 피크와 탄소 중립을 각각 달성하기 위해 저탄소와 탄소 중립 노력을 우선시했습니다. 이 계획에서는 천연가스의 연간 생산량을 8조 1,000억 입방피트(Tcf)로, 발전설비 용량을 3.0테라와트(TW)로 증가시키는 목표를 내걸고 있습니다.

방청 코팅은 인프라 용도와 세계 개발에서도 중요한 역할을 담당하고 있으며, 인프라 투자 증가가 방청 코팅 수요를 밀어 올리고 있습니다. 아시아개발은행(ADB)에 따르면 아시아태평양이 성장세를 유지하고 기후 변화에 대응하고 빈곤을 없애기 위해서는 2030년까지 연간 1조 7,000억 달러를 인프라 개발에 투자해야 한다고 합니다.

따라서, 상기 요인이 예측 기간 동안 방청 코팅 시장을 견인할 것으로 예상됩니다.

방청 코팅 산업 개요

방청 코팅 시장은 통합되어 있으며 주요 기업으로는 PPG Industries, Inc., Akzo Nobel NV, Nippon Paint Holdings, RPM International Inc., Sherwin-Williams Company 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

인프라 산업의 현저한 성장

해양산업에서의 수요 증가

아시아태평양과 북미의 석유 및 가스 활동 확대

억제요인

휘발성 유기화합물(VOC) 관련 정부규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(규모별)

수지 유형별

에폭시

알키드

폴리에스테르

폴리우레탄

비닐에스테르

기타

기술별

수성

용매성

분말

UV 경화

최종 사용자 산업별

석유 및 가스

해양

전력

인프라

산업

항공우주 및 방위

운수

기타

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작사업, 제휴, 협정

시장 점유율 분석**/랭킹 분석

주요 기업의 전략

기업 프로파일

Akzo Nobel NV

Axalta Coating Systems, LLC

BASF SE

HB Fuller Company

Hempel A/S

Jotun

Kansai Paint Co.,Ltd

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

RPM International Inc.

Sika AG

The Sherwin-Williams Company

제7장 시장 기회와 앞으로의 동향

신흥국의 인프라 산업에 대한 대규모 투자

수성 코팅의 채용 증가

KTH

영문 목차

영문목차

The Anti-Corrosion Coatings Market size is estimated at USD 26.94 billion in 2025, and is expected to reach USD 33.43 billion by 2030, at a CAGR of 4.41% during the forecast period (2025-2030).

Key Highlights

The COVID-19 pandemic had a negative impact on the anti-corrosion coatings sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

Major factors driving the market are significant growth in the infrastructure industry, an increase in demand from the marine industry, and expansion of oil and gas activities in Asia-Pacific and North America.

Regulations related to volatile organic compounds (VOCs) and is expected to hinder the growth of the market studied.

Significant investments in the infrastructure industry in emerging economies and increased adoption of water-borne coatings are expected to provide remarkable growth opportunities in the anti-corrosion coatings market in the future.

Asia-Pacific region is expected to dominate the anti-corrosion coatings markets due to the increase in investments in various end-user industries in the region during the forecast period.

Anti-Corrosion Coatings Market Trends

Increasing Demand from the Infrastructure Industry

The infrastructure segment accounts for the largest share of the market and is also estimated to be the fastest-growing segment. Rails, bridges, and roads contributed as the major segments of the infrastructure. The rapid increase in population and growth in infrastructure projects are expected to boost the demand for anti-corrosion coatings.

There are various small-scale projects spread across Asia-Pacific and North America. Apart from being the most populous nation in the world, China also has the largest number of railroad passengers.

Moreover, road projects in Asia-pacific are also expected to increase the consumption of anti-corrosion coatings. For instance, according to the Ministry of Road Transport and Highways, the ongoing Bharatmala Pariyojna is developing around 26,000 km length of Economic Corridors in order to carry most of the freight traffic on roads. The improvement of Economic Corridors, GQ, and NS-EW Corridoors has been done by building 8.000 km of Inter Corridors and 7,500 km of Feeder Routes.

For infrastructure development, according to China Briefings, At the end of 2021, China's Ministry of Finance (MoF) pre-allocated USD 229.6 billion of the 2022 quota to be used in the first quarter in the hopes that the extra liquidity would spur investment at the beginning of the year, with higher quotas allocated to provinces and regions with higher capital needs.

In April 2023, World Bank data stated that private participation in infrastructure (PPI) reached around USD 91.7 billion with around 263 projects, which accounts for 23% growth from 2021. It is observed in low and middle-income countries, the investment in infrastructure has rebounded in 2022.

According to the US Department of Transportation (USDoT) and Federal Highway Administration (FHWA), in the years 2022 and 2030, around USD 120 billion has been allocated for highways and bridges, of which nearly 2,800 bridges have already been launched. USDOT invested USD 2.2 billion for 166 projects in Rebuilding American Infrastructure with Sustainability and Equity (RAISE) grants. It will facilitate the modernization of rail, ports, roads, bridges, and intermodal transportation to be more affordable, safer, and sustainable.

The aforementioned factors are expected to increase the demand for anti-corrosion coatings in the forecast period.

Asia-Pacific Region to Dominate the Market

In Asia-Pacific, though China, Japan, and South Korea lead the shipbuilding industry, new shipping hubs are appearing in Vietnam, India, and the Philippines.

Australia and New Zealand are both island nations, and the geographical scale of Australia's coastline and waterways has resulted in a large number of recreational, commercial, and defense vessels.

China is the leading importer and exporter of crude oil in the world. Thus, any changes affecting the expansion activities related to the oil and gas sector are likely to have a significant impact on the anti-corrosion coatings market in China.

According to US Energy Information Administration, in 2022, China has prioritized low-carbon and carbon-neutral initiatives in order to meet the country's 2030 and 2060 climate targets of peak carbon emissions and carbon neutrality, respectively. The plan has set a goal for natural gas annual production to increase to 8.1 trillion cubic feet (Tcf) and installed generation capacity to increase to 3.0 terawatts (TW).

Anti-corrosion coatings also play a significant role in infrastructure applications and global development, and an increase in investment in infrastructure is boosting the demand for anti-corrosion coatings. According to the Asian Development Bank (ADB), if Asia- Pacific has to maintain its growth momentum, respond to climate change, and remove poverty, then the region has to invest USD 1.7 trillion per year by 2030 in infrastructure development.

Thus, the above-mentioned factors are expected to drive the anti-corrosion coatings market in the forecast period.

Anti-Corrosion Coatings Industry Overview

The anti-corrosion coatings market is consolidated and the major companies include PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., and the Sherwin-Williams Company.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Significant Growth in the Infrastructure Industry

4.1.2 Increase in Demand from the Marine Industry

4.1.3 Expansion of Oil and Gas Activities in Asia-Pacific and North America

4.2 Restraints

4.2.1 Government Regulations Related to Volatile Organic Compounds (VOCs)

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Resin Type

5.1.1 Epoxy

5.1.2 Alkyds

5.1.3 Polyester

5.1.4 Polyurethane

5.1.5 Vinyl Ester

5.1.6 Other Resin Types

5.2 By Technology

5.2.1 Water-borne

5.2.2 Solvent-borne

5.2.3 Powder

5.2.4 UV-cured

5.3 By End-user Industry

5.3.1 Oil and Gas

5.3.2 Marine

5.3.3 Power

5.3.4 Infrastructure

5.3.5 Industrial

5.3.6 Aerospace and Defense

5.3.7 Transportation

5.3.8 Other End-user Industries

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle East & Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Analysis**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Akzo Nobel N.V.

6.4.2 Axalta Coating Systems, LLC

6.4.3 BASF SE

6.4.4 H.B. Fuller Company

6.4.5 Hempel A/S

6.4.6 Jotun

6.4.7 Kansai Paint Co.,Ltd

6.4.8 Nippon Paint Holdings Co., Ltd.

6.4.9 PPG Industries, Inc.

6.4.10 RPM International Inc.

6.4.11 Sika AG

6.4.12 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Significant Investments in the Infrastructure Industry in the Emerging Economies