ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

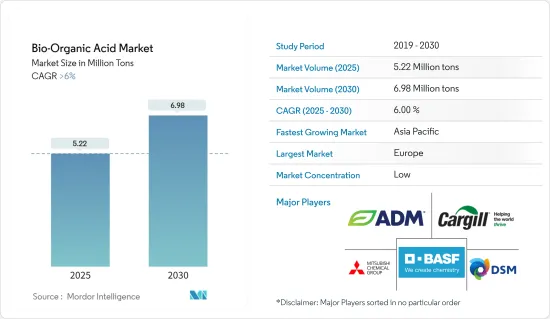

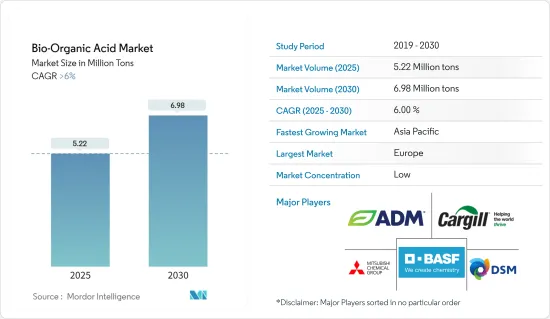

바이오 유기산의 시장 규모는 2025년 522만 톤으로 추정되며, 예측 기간(2025-2030년) 동안 6% 이상의 CAGR을 기록하여 2030년에는 698만 톤에 달할 것으로 예상됩니다.

COVID-19 팬데믹은 전국적인 봉쇄, 엄격한 사회적 거리두기, 공급망 혼란으로 인해 시장에 악영향을 미쳤습니다. 이러한 요인은 식음료, 섬유, 페인트 시장에 부정적인 영향을 미쳤으며, 바이오 유기산 시장에도 영향을 미쳤습니다. 그러나 규제가 해제된 후 시장은 순조롭게 회복되었습니다. 식음료, 섬유, 코팅 최종사용자 산업에서 바이오 유기산 소비가 증가함에 따라 시장은 크게 회복되었습니다.

기존 유기산에 대한 엄격한 규제와 의료용 바이오 기반 폴리머에 대한 수요 증가가 바이오 유기산 시장을 견인할 것으로 예상됩니다.

바이오 기반 화학제품의 높은 제조비용이 시장 성장을 저해할 것으로 예상됩니다.

친환경 제품으로의 전환은 예측 기간 동안 시장에서 기회를 창출할 것으로 예상됩니다.

아시아태평양이 시장을 지배할 것으로 예상됩니다. 또한, 제약, 섬유, 코팅제, 식품 분야에서 바이오 유기산에 대한 수요가 증가함에 따라 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다.

바이오 유기산 시장 동향

시장을 독점하는 식음료 산업

예측 기간 동안 음료 및 식품 최종사용자 산업이 바이오 유기산 시장을 지배할 것으로 예상됩니다. 바이오 유기산과 그 유도체는 음료, 식품, 사료 생산에 자주 사용됩니다. 산성 첨가제는 산도를 조절하는 완충제, 항산화제, 방부제, 향미증진제, 봉쇄제로 작용할 수 있습니다.

북미와 유럽은 세계 최대의 식음료 시장입니다. 미국 인구조사국에 따르면, 미국 소매 및 식품 서비스의 월간 소매 매출은 2023년 11월에 약 7,057억 달러로 9월의 7,049억 달러에 비해 약 7,057억 달러에 달했습니다. 이처럼 식음료 시장의 확대는 미국 바이오 유기산 시장을 견인할 것으로 보입니다.

또한 미국 농무부에 따르면 멕시코는 미국, 브라질에 이어 아메리카에서 세 번째로 큰 식품 가공 산업입니다. 농업시장자문그룹(GCMA)의 데이터에 따르면, 멕시코의 식품 생산량은 2022년 2억 8,700만 톤에서 2023년 2억 9,000만 톤에 달할 것으로 예상됩니다.

FoodDrinkEurope에 따르면 음료 및 식품 부문은 유럽에서 가장 큰 제조업 중 하나이며, 2022년 4분기 음료 및 식품 산업의 매출은 전년 동기 대비 2.3%, 2021년 4분기 대비 19.2% 증가하였다고 합니다. 따라서 음료 및 식품 시장의 매출 성장은 이 지역의 바이오 유기산 시장을 견인할 것으로 예상됩니다.

독일은 유럽 최대의 식음료 시장입니다. 식품 산업은 독일에서 네 번째로 큰 산업 부문입니다. 독일 음료 및 식품 산업 연맹(BVE)의 데이터에 따르면 2022년 독일의 음료 및 식품 가공 총 수입은 207억 달러로 전년 대비 17.9%의 성장률을 기록했습니다. 따라서 음료 및 식품 부문의 성장이 이 지역의 바이오 유기산 시장을 견인할 것으로 예상됩니다.

따라서, 음료 및 식품 최종사용자 산업은 예측 기간 동안 바이오 유기산 시장을 독점할 것으로 예상됩니다.

시장 성장을 주도하는 아시아태평양

아시아태평양은 이 지역의 제약, 섬유, 코팅, 음료 및 식품 최종사용자 산업의 수요 증가로 인해 바이오 유기산 시장을 주도할 것으로 예상됩니다.

중국과 인도는 이 지역에서 가장 큰 식음료 시장입니다. 중국 국가경공업위원회에 따르면, 연간 매출액이 280만 달러 이상인 주요 식품 제조 기업은 2022년에 1조 5,300억 달러 이상의 매출을 기록했으며, 2021년과 비교하면 총 매출은 전년 대비 5.6% 증가하여 식품 산업의 강력한 성장을 보여주었습니다.

IBEF에 따르면 인도의 식품 가공 시장 규모는 2022년 307조 2,000억 달러, 2028년에는 547조 3,000억 달러에 달할 것으로 예상되며, 인도에서도 식음료 부문은 상당한 성장률을 기록할 것으로 예상됩니다. 따라서 식품 가공 시장의 성장으로 인해 인도에서 바이오 기반 유기산의 사용량이 증가할 것으로 예상됩니다.

바이오 유기산에 대한 수요는 제약 부문에서 증가하고 있습니다. 인도는 세계 제약 허브이며 200여 개국에 의약품을 수출하고 있으며, 2022-2023년 상반기 제약산업에 대한 해외직접투자 유입액은 25% 증가했으며, IBEF에 따르면 제약산업 매출은 2024년까지 650억 달러에 달할 것으로 예상됩니다. 따라서 제약 시장의 확대는 현재 연구 시장을 주도할 것입니다.

또한 중국에서는 섬유 산업이 큰 폭의 시장 성장을 기록했습니다. 중국 국가통계국에 따르면 2022년 중국의 섬유 생산량은 전년 동기 235억 미터에 비해 382억 미터에 이르렀고, 12월에는 약 34억 7,000만 미터의 의류용 원단이 중국에서 생산되었습니다. 월간 섬유 생산량은 지속적으로 30억 미터를 초과하고 있습니다.

위의 요인으로 인해 아시아태평양의 바이오 유기산 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

바이오 유기산 산업 개요

바이오 유기산 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 BASF SE, DSM, Mitsubishi Chemical Corporation, Cargill, Incorporated, ADM 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

기존 유기산에 대한 엄격한 규제

의료 용도의 바이오 기반 폴리머 수요 확대

기타 촉진요인

성장 억제요인

바이오 기반 화학제품 제조 비용 상승

기타 성장 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(시장 규모(수량 기준))

원료

바이오매스

옥수수(Corn)

옥수수(Maize)

설탕

기타 원료

제품 유형

바이오 젖산

바이오 아세트산

바이오 아디프산

바이오 아크릴산

바이오 숙신산

기타 제품 유형(바이오 구연산, 바이오 푸마르산 등)

용도 부문

폴리머

의약품

섬유 제품

코팅

식품 및 음료

기타 용도(퍼스널케어, 화학 등)

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

시장 점유율(%)**/순위 분석

주요 기업의 전략

기업 개요

ADM

Abengoa

BASF SE

BioAmber Inc

Braskem

Cargill, Incorporated

Corbion

Cosun

DSM

Genomatica

Gfbio

Mitsubishi Chemical Corporation

NatureWorks LLC

Novozymes

PTT Global Chemical Public Company Limited

제7장 시장 기회와 향후 동향

친환경 제품으로의 이동

기타 기회

ksm

영문 목차

영문목차

The Bio-Organic Acid Market size is estimated at 5.22 million tons in 2025, and is expected to reach 6.98 million tons by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market due to nationwide lockdowns, strict social distancing measures, and disruption in supply chains. These factors negatively affected the food and beverage, textile, and coating markets, thereby affecting the market for bio-organic acids. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of bio-organic acids in food and beverage, textile, and coating end-user industries.

The stringent regulations over conventional organic acids and the growing demand for bio-based polymers in healthcare applications are expected to drive the market for bio-organic acids.

The higher production cost of bio-based chemicals is expected to hinder the growth of the market.

The shifting focus towards eco-friendly products is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for bio-organic acids in pharmaceuticals, textiles, coatings, and food products applications.

Bio-Organic Acid Market Trends

Food and Beverage Industry to Dominate The Market

The food and Beverage end-user industry is expected to dominate the market for bio-organic acid during the forecast period. Bio-organic acids and their derivatives are frequently used in beverage, food, and feed production. Acidic additives may act as buffers to regulate acidity, antioxidants, preservatives, flavor enhancers, and sequestrants.

North America and Europe are the largest markets for food and beverages across the globe. According to the U.S. Census Bureau, monthly retail sales from U.S. retail and food services were valued at around USD 705.7 billion in November 2023, as compared to USD 704.9 billion in September. Thus, the increasing market for food and beverage products will drive the market for bio-organic acids in the country.

Furthermore, according to the USDA, Mexico is the third-largest food processing industry in the Americas, after the United States and Brazil. According to data from the Agricultural Markets Advisory Group (GCMA), the country's food production is anticipated to reach 290 million tons in 2023, growing from 287 million tons in 2022.

The food and beverage sector is one of the largest manufacturing industries in Europe. According to FoodDrinkEurope, the food and beverage industry turnover increased by 2.3% in Q4 2022, compared to the previous quarter, and increased by 19.2% Y-o-Y compared to Q4 2021. Thus, the growth in food and beverage market turnover is expected to drive the market for bio-organic acid in the region.

Germany is the largest market for food and beverage products in Europe. The food industry represents the fourth-largest industrial sector in the country. According to data from the Federation of German Food and Drink Industries (BVE), in 2022, the total revenue of food and beverage processing in the country reached USD 20.7 billion, at a growth rate of 17.9% as compared to the previous year. Thus, the growth in the food and beverage sector is expected to drive the market for bio-organic acids in the region.

Thus, the food and beverage end-user industry is expected to dominate the market for bio-organic acid during the forecast period.

Asia-Pacific Region to Dominate the Market Growth

The Asia-Pacific region is expected to dominate the market for bio-organic acid due to rising demand from pharmaceuticals, textiles, coatings, food and beverage end-user industries in the region.

China and India are the largest food and beverage markets in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry.

Similarly, in India, the food and beverage sector is expected to register a significant growth rate. According to IBEF, Indian food processing market size reached USD 307.2 trillion in 2022 and is expected to reach USD 547.3 trillion by 2028. Thus, the growth in food processing markets will increase the usage of bio-based organic acids in the country.

The demand for bio-organic acids is increasing in the pharmaceutical sector. India is a global pharmaceutical hub, exporting pharmaceuticals to over 200 countries. In the first half of 2022-2023, foreign direct investment inflows into the pharmaceutical industry increased by 25%. According to IBEF, the pharmaceutical industry revenue is expected to reach USD 65 billion by 2024. Thus, the increasing market for pharmaceuticals will drive the current studied market.

Furthermore, in China, the textile industry registered significant market growth. According to the National Bureau of Statistics of China, China's textile production volume accounted for 38.2 billion meters in 2022, compared to 23.5 billion meters during the same period in the previous year. In December, approximately 3.47 billion meters of clothing fabric were produced in China. Monthly textile production volume was consistently above three billion meters.

Owing to the above-mentioned factors, the market for bio-organic acid in the Asia-Pacific region is projected to grow significantly during the forecast period.

Bio-Organic Acid Industry Overview

The bio-organic acid market is fragmented in nature. Some of the major players in the market (not in any particular order) include BASF SE, DSM, Mitsubishi Chemical Corporation, Cargill, Incorporated, and ADM, amongst others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Stringent Regulations Over Conventional Organic Acids

4.1.2 Growing Demand for Bio-based Polymer in Healthcare Applications

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Higher Production Cost of Bio-based Chemicals

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Raw Material

5.1.1 Biomass

5.1.2 Corn

5.1.3 Maize

5.1.4 Sugar

5.1.5 Other Raw Materials

5.2 Product Type

5.2.1 Bio Lactic Acid

5.2.2 Bio Acetic Acid

5.2.3 Bio Adipic Acid

5.2.4 Bio Acrylic Acid

5.2.5 Bio Succinic Acid

5.2.6 Other Product Types (Bio Citric Acid, Bio Fumaric Acid, etc.)

5.3 Application

5.3.1 Polymers

5.3.2 Pharmaceuticals

5.3.3 Textile

5.3.4 Coatings

5.3.5 Food and Beverage

5.3.6 Other Applications (Personal Care, Chemicals, etc.)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements