ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

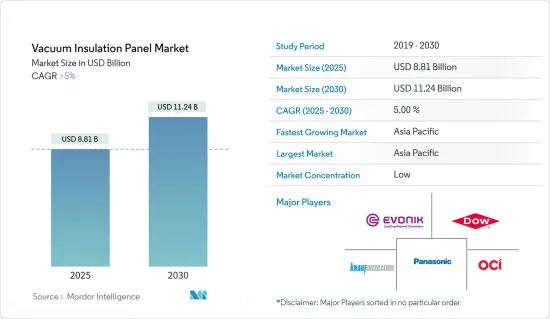

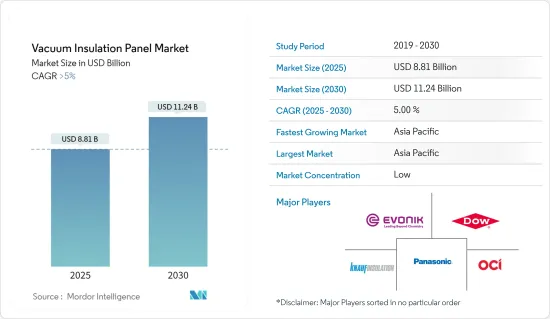

진공 단열 패널 시장 규모는 2025년 88억 1,000만 달러로 추정됩니다. 2030년 112억 4,000만 달러에 이를 것으로 예상되며, 예측기간 중(2025-2030년) CAGR은 5%를 넘을 것으로 추정됩니다.

COVID-19 팬데믹은 봉쇄 및 규제에 의한 제조 시설 및 공장의 운영 중단으로 인해 시장에 악영향을 미쳤습니다. 공급망과 운송의 혼란은 시장에 장애를 가져왔습니다. 그러나 산업은 2021년에 회복을 보였고, 그 결과 조사된 시장 수요는 회복되었습니다.

주요 하이라이트

단기적으로는 건설 산업으로부터의 왕성한 수요와 자동 보관·검색용 진공 단열 패널의 세계적인 도입이 조사 대상 시장의 성장을 가속하는 요인이 되고 있습니다.

반면 비표준 크기에 대한 높은 비용과 패널의 무게는 시장 성장을 방해할 가능성이 높습니다.

그러나 에너지 효율적인 재료를 추진하는 규제가 점점 엄격해지고 있으며, 진공 단열 패널의 비용을 절감하는 자동화 패널을 도입하는 R&D 이니셔티브는 예측 기간 동안 조사한 시장에 기회를 제공할 가능성이 높습니다.

진공 단열 패널 시장 동향

강력한 성장을 이루는 건설 부문

진공 단열 패널(VIP)은 가장 높은 단열 능력을 가진 유망한 단열재 중 하나이며 건설 산업에서 널리 받아 들여지고 있습니다.

진공 단열 패널은 건축 부재의 박형화, 실내 공간 확대 및 토지 이용 최적화, 서비스 수명 후 구성 재료의 재활용 가능성 등 건설 부문의 다른 이점을 제공합니다.

미국 인구조사국에 따르면 미국의 2022년 상업건축액은 1,147억 9,000만 달러로 전년 대비 17.63% 증가했습니다.

또한 아시아태평양, 중동, 아프리카 등 지역에서는 산업 유닛, 병원, 쇼핑몰, 극장, 호텔, IT 부문의 설립을 위해 국내외에서 거액의 투자가 모여 진공 단열 패널 수요에 박차가 걸릴 수 있습니다.

사우디아라비아에서는 부동산 개발 증가, 주택 수요 증가, 사회 경제 인프라 정비를 위한 정부의 이니셔티브이 이 나라의 진공 단열 패널 시장을 견인하고 있습니다. 사우디아라비아의 Majid Al-Hogail 주택상에 따르면, 사우디아라비아은 향후 5년간 30만 호의 주택 건설을 계획하고 있습니다. "비전 2030"에서 사우디아라비아의 중요한 이니셔티브 중 하나가 주택입니다. 향후 수년간, 이 나라의 건설 산업으로부터 진공 단열 패널 시장에 대한 수요가 생길 가능성이 높습니다.

Institution of Civil Engineers(ICE)의 조사에 따르면 세계 건설 산업은 2030년까지 8조 달러에 이를 것으로 예상되며, 주로 중국, 인도, 미국이 견인하고 있습니다.

게다가 에너지 효율적인 구조를 의무화하는 건축 기준법이나 시책이 증가하고 있는 것도, 건설 부문에 의한 환경 친화적으로 에너지 절약으로 이어지는 재료의 사용 증가를 촉진하고 있습니다.

그러므로 건설 산업에서의 상기 동향은 예측 기간 동안 진공 단열 패널 시장의 성장을 가속할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

아시아태평양이 세계 시장 점유율을 독점. 인도, 중국, 필리핀, 베트남, 인도네시아에서는 주택과 상업시설의 건설 활동에 대한 투자가 증가하고 있으며, 시장은 향후 몇 년동안 성장할 것으로 예상됩니다.

2011-2022년까지 중국의 건설 생산액은 이 산업의 성장이 진행되고 있음을 나타냅니다. 예를 들어 중국국가통계국에 따르면 2022년 중국의 건설생산액은 피크 때 약 27조 6,300억 위안(4조 1,000억 달러)에 달할 전망입니다.

가계 소득 증가율 상승과 농촌에서 도시로의 인구이동으로 중국에서는 주택건설 수요가 증가할 것으로 예상됩니다. 공공 부문과 민간부문 모두에서 저렴한 주택을 중시하게 되면 주택건설 부문 개발에 박차가 걸릴 것으로 예상됩니다.

중국에서는 현재 개발 중 또는 계획 중인 공항 건설 프로젝트가 몇 가지 있습니다. 예를 들어 신강 위구르 자치구는 현대적인 공항 네트워크 시스템을 형성하기 위해 8개 공항을 새로 건설할 계획입니다. 신장공항그룹은 2023-2025년에 걸쳐 바얀브라크, 발콜, 우스, 호복살, 치에모에 공항을 건설할 계획을 발표했습니다.

게다가 2021년 건설산업에서 새로 체결된 계약액은 1,345억 위안(195억 2,000만 달러)으로 전년 동기 대비 2.5% 증가, 성장률은 7.1% 축소되었습니다. 중국은 2022년 1월 제14차 5개년 계획(2021-2025년) 기간 중에 건설산업을 발전시킬 계획을 발표하고 보다 환경친화적이고 보다 스마트하고 보다 안전한 길을 걷는 일본 경제 기둥을 세웠습니다. 그러므로 건설의 계약 증가는 진공 단열 패널 시장에 긍정적으로 작용할 것으로 예상됩니다.

또한 인도에서는 정부가 2022년 1월 국내 21곳의 그린필드 공항 개발을 승인했습니다. 국내 최대의 공항은 우타르 프라데시의 가우탐 부다 나가르 지구에 건설됩니다. 민간 항공성은 향후 몇 년동안 인도 전역에 21개의 공항을 추가로 건설할 의향입니다.

또한 인도공항공단(AAI)은 향후 4-5년 사이에 3억 3,800만 달러로 신공항 건설과 많은 기존 공항의 확대·개량을 계획하고 있습니다. 이는 기존 터미널의 확대·변경, 신터미널의 건설, 기존 활주로, 기술 블록, 앞치마, 공항 내비게이션 서비스의 관제탑의 확대·강화로 구성됩니다.

또한 2025년까지 델리, 벵갈루루, 하이데라바드 등 3개의 PPP(관민 파트너십) 공항이 확대 계획에 3,000억 루피(38억 1,000만 달러)를 투자할 예정입니다. 따라서 진공 단열 패널 시장에 상승 수요가 발생합니다.

인도에서는 정부가 27개 산업 클러스터 개발에 1,205억 달러를 투자한다는 목표를 세우고 있으며, 국내 상업 건설이 활발해질 것으로 기대되고 있습니다.

따라서 아시아태평양 국가의 이러한 투자와 계획된 프로젝트는 모두 이 지역의 건설 활동을 뒷받침하고 있으며 예측 기간 동안 진공 단열 패널 수요를 촉진할 것으로 예상됩니다.

진공 단열 패널 산업 개요

진공 단열 패널 시장은 세분화되어 있습니다. 이 시장의 주요 기업에는 Evonik Industries AG, Panasonic Corporation, Dow, Knauf Insulation, OCI Company Ltd 등이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건설 산업으로부터의 왕성한 수요

진공 단열 패널의 자동 보관·검색에 채용

기타 촉진요인

억제요인

비표준 사이즈에 대한 VIP의 고비용

진공 단열 패널의 무거운 중량

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(규모별)

핵심 재료

실리카

유리 섬유

기타 핵심 재료

구조 유형

평면

특수 모양

용도

건축

냉각·냉동 장치

물류

기타

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

AVERY DENNISON CORPORATION

Chuzhou Yinxing Electric Co. Ltd

Csafe

Dow

Etex Group

Evonik Industries AG

KCC CORPORATION

Kevothermal

Kingspan Group

Knauf Insulation

Morgan Advanced Materials

Panasonic Corporation of North America

Recticel Insulation

TURNA doo

Vaku-Isotherm GmbH

Va-Q-Tec AG

제7장 시장 기회와 앞으로의 동향

자동화 패널 도입을 향한 연구 개발 이니셔티브

지속 가능한 건축용 진공 단열 패널

KTH

영문 목차

영문목차

The Vacuum Insulation Panel Market size is estimated at USD 8.81 billion in 2025, and is expected to reach USD 11.24 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market due to the shutdown of manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

Over the short term, robust demand from the construction industry and the adoption of vacuum insulation panels for automated storage and retrieval worldwide are factors driving the studied market's growth.

On the flip side, the high cost for non-standard sizes and the heavy weight of the panels will likely hinder the studied market's growth.

However, increasingly stringent regulations promoting energy-efficient materials and R&D initiatives to introduce automated panels to reduce vacuum insulation panel costs will likely provide opportunities for the market studied during the forecast period.

Vacuum Insulation Panel Market Trends

Construction Segment to Witness Strong Growth

Vacuum insulation panels (VIPs) are one of the most promising insulation materials with the highest thermal insulating capacity and are widely accepted in the construction industry.

Vacuum insulation panels also offer other advantages in the construction sector, like the reduced thickness of building components, increased indoor space and land use optimization, and recyclability of constitutive materials after their service life.

According to the US Census Bureau, the value of commercial construction in the United States amounted to USD 114.79 billion in 2022, which showed an increase of 17.63% compared to the previous year.

Additionally, regions like Asia-Pacific, the Middle East, and Africa are attracting huge domestic and foreign investments for setting up industrial units, hospitals, malls, theaters, hotels, and the IT sector, which may add to the demand for vacuum insulation panels.

In Saudi Arabia, the growing number of real estate developments, increasing demand for residential property, and governmental initiatives to develop socio-economic infrastructure drive the vacuum insulation panel market in the country. According to Majid Al-Hogail, the Saudi Housing Minister, the Kingdom of Saudi Arabia plans to construct 300,000 extra housing units over the next five years. One of Saudi Arabia's significant initiatives under Vision 2030 is housing. It will likely create demand for the vacuum insulation panel market from the country's construction industry in the upcoming years.

According to a study by the Institution of Civil Engineers (ICE), the global construction industry is expected to reach USD 8 trillion by 2030, primarily driven by China, India, and the United States.

Furthermore, the rising number of building codes and policies mandating energy-efficient structures is further facilitating an increase in the construction sector's usage of eco-friendly and energy-conserving materials.

Hence, the trends above in the construction industry are expected to drive the growth of the vacuum insulation panel market during the forecast period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region dominated the global market share. With growing investments in residential and commercial construction activities in India, China, the Philippines, Vietnam, and Indonesia, the market is expected to grow in the coming years.

The output value of construction in China from 2011 to 2022 indicates progressive growth in the industry. For instance, according to the National Bureau of Statistics of China, in 2022, the construction output value in China peaked at around CNY 27.63 trillion (USD 4.10 trillion).

Rising household income rates and population migration from rural to urban areas are expected to increase demand for residential construction in China. Increased emphasis on both public and private sector affordable housing would fuel development in the residential construction sector.

There are currently several airport construction projects in China, either in the development or planning stage. For instance, the Xinjiang Uygur autonomous region plans to construct eight new airports to form a modern airport network system. Xinjiang Airport Group announced its plan to build airports in Bayanbulak, Barkol, Wusu, Hoboksar, and Qiemo from 2023 to 2025.

Moreover, in 2021, the value of newly signed contracts in the construction industry was CNY 134.5 billion (USD 19.52 billion), an increase of 2.5% year-on-year, and the growth rate narrowed by 7.1% compared with the same period last year. In January 2022, China unveiled plans to develop its construction industry during the 14th Five-Year Plan (2021-2025), paving a pillar of the country's economy on a greener, smarter, and safer path. Therefore, increasing contracts from construction is expected to include an upside for the vacuum insulation panel market.

Moreover, in India, the government approved the development of 21 greenfield airports in the country in January 2022. The country's largest airport will be built in Uttar Pradesh's Gautam Buddha Nagar area. The Ministry of Civil Aviation intends to build 21 additional airports across India in the next few years.

Furthermore, in the next four to five years, the Airports Authority of India (AAI) plans to create new airports and expand and upgrade many existing airports for USD 338 million. It comprises the expansion and alteration of existing terminals, the construction of new terminals, and the expansion or strengthening of existing runways, technical blocks, aprons, and the control towers of the Airport Navigation Services.

In addition, by 2025, three PPP (Public-Private Partnership) airports in Delhi, Bengaluru, and Hyderabad will invest INR 30,000 crore (USD 3810 million) in expansion plans. Therefore, creating an upside demand for the vacuum insulation panel market.

In India, the government's target for investing USD 120.5 billion in developing 27 industrial clusters is expected to boost commercial construction in the country.

Hence, all such investments and planned projects in the Asia-Pacific countries are boosting construction activities in the region, which are anticipated to drive the demand for vacuum insulation panels during the forecast period.

Vacuum Insulation Panel Industry Overview

The vacuum insulation panel market is fragmented in nature. The major players in this market (not in any particular order) include Evonik Industries AG, Panasonic Corporation, Dow, Knauf Insulation, and OCI Company Ltd, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Robust Demand from Construction Industry

4.1.2 Adoption of Vacuum Insulation Panel for Automated Storage and Retrieval

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Cost of VIPs for Non-standard Sizes

4.2.2 Heavy Weight of Vacuum Insulation Panels

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Core Material

5.1.1 Silica

5.1.2 Fiberglass

5.1.3 Other Core Materials

5.2 Structure Type

5.2.1 Flat

5.2.2 Special Shape

5.3 Application

5.3.1 Construction

5.3.2 Cooling and Freezing Devices

5.3.3 Logistics

5.3.4 Other Applications

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 AVERY DENNISON CORPORATION

6.4.2 Chuzhou Yinxing Electric Co. Ltd

6.4.3 Csafe

6.4.4 Dow

6.4.5 Etex Group

6.4.6 Evonik Industries AG

6.4.7 KCC CORPORATION

6.4.8 Kevothermal

6.4.9 Kingspan Group

6.4.10 Knauf Insulation

6.4.11 Morgan Advanced Materials

6.4.12 Panasonic Corporation of North America

6.4.13 Recticel Insulation

6.4.14 TURNA d.o.o

6.4.15 Vaku -Isotherm GmbH

6.4.16 Va-Q-Tec AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 R&D Initiatives to Introduce Automated Panels

7.2 Vacuum Insulated Panels for Sustainable Buildings