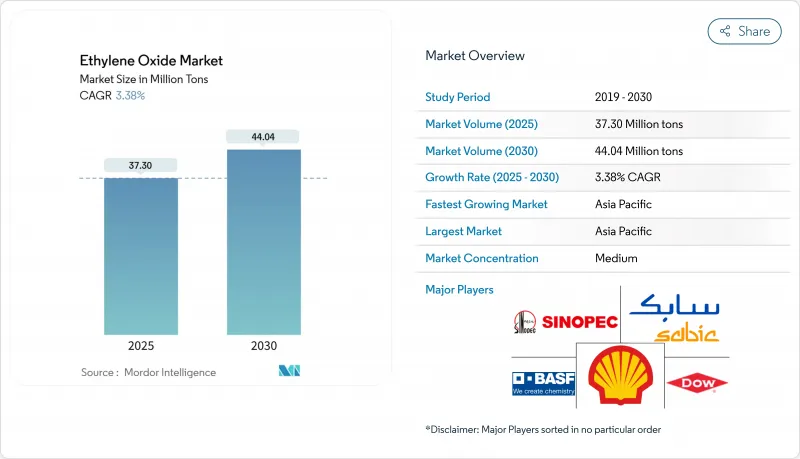

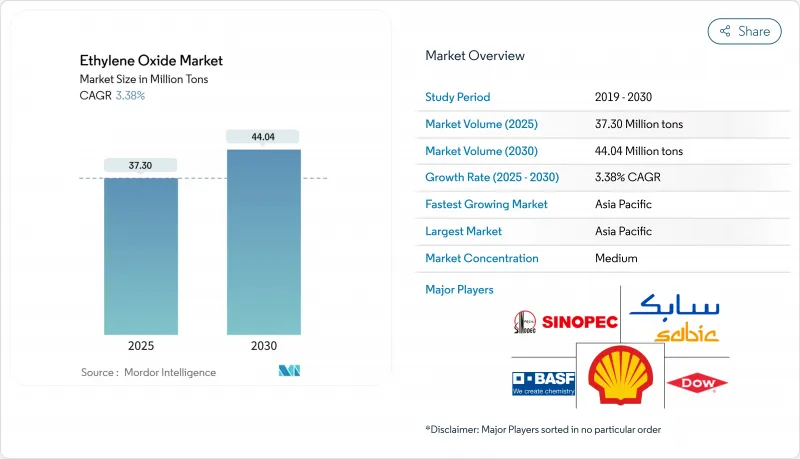

에틸렌옥사이드 시장 규모는 2025년에 3,730만 톤, 2030년에는 4,404만 톤에 이르고, 예측 기간(2025-2030년)의 CAGR은 3.38%를 나타낼 전망입니다.

수요는 화학 중간체로서의 범용성에 기인하고 있고, 폴리에스테르 섬유, PET 수지, 계면활성제, 에탄올아민, 멸균제 등이 소비의 성장을 지지하고 있습니다. 폴리에스테르 기반의 섬유 제품 확대, PET의 경량 식품 및 음료 포장 채택 확대, 의료기기 멸균 시설에 대한 규제 주도 투자가 여전히 중심적인 촉진요인이 되고 있습니다. 바이오에틸렌 원료의 급속한 보급, 배출 억제 기술에 대한 투자 증가, 순환형 경제 구상의 확산은 조달 전략을 재구성하고 새로운 수익원을 개척하고 있습니다. 경쟁력학에서는 공급원료 변동의 균형을 맞추고 강화되는 배출규제를 준수하며 특수유도품을 개발할 수 있는 수직통합형 제조업체가 유리합니다.

PET 포장의 채택이 가속화되고 있는 이유는 브랜드 소유자가 제품의 무결성을 유지하는 가볍고 재활용 가능한 솔루션을 선호하기 때문입니다. 에틸렌옥사이드에서 유래된 모노에틸렌 글리콜은 PET 중합에 사용되는 에틸렌 글리콜 풀의 90% 가까이를 차지하고 있으며, 업스트림 수요에 대한 직접적인 풀쓰루를 야기합니다. 주요 수지 제조업체는 소비자 사용 후 PET를 90% 이상의 수율로 단량체로 해중합하는 화학 리사이클 플랫폼을 지원하고 있으며, 산화 에틸렌의 양을 안정시키면서 순환형 공급 체인을 가능하게 하고 있습니다. 다우와 같은 기업은 2030년까지 연간 수백만 톤 규모의 프로그램을 개발하여 순환형 및 재생 가능한 플라스틱을 공급하고 있습니다. 이러한 노력은 제품 구성이 재활용 등급으로 이동하더라도 장기적인 수요 전망을 강화합니다.

에톡실레이트와 에탄올아민이 배합된 계면활성제나 세제는 특히 경수지역에서 우수한 세정 효율을 발휘합니다. 친환경 성분을 추구하는 소비자의 선호도는 Nouryon과 같은 제조업체에게 ISCC PLUS 체계에 의한 녹색 산화 에틸렌 유도체의 인증을 촉구하고 있습니다. 알킬 페놀에서 지방 알코올 에톡실레이트로의 전환은 성능을 유지하면서 오는 생분해성 규제에 대응합니다. 유럽과 북미의 생산 능력 증강은 프라이빗 브랜드의 세정제가 소매점의 선반에 늘어서게 되어, 이 수요 증가를 받아들이기 위한 것입니다.

에틸렌옥사이드은 발암성이 있다고 분류되어 있기 때문에 EPA는 2025년 1월 노동자의 노출 한도를 2028년까지 0.5ppm에서 2035년까지 0.1ppm으로 낮추는 잠정 결정을 내렸습니다. 이를 준수하기 위해서는 비용이 많이 드는 기술 관리, 개인 모니터링 및 장비 업데이트가 필요합니다. 일부 건강 관리 장비 제조업체는 감마선 조사, 기화 과산화수소, 이산화질소와 같은 대체 멸균 방법의 인증을 가속화하고 있습니다. 이러한 대체품이 특정 부피를 침식하는 반면, 산화 에틸렌은 복잡한 루멘을 갖는 열에 민감한 장치에 필수적인 것으로 변하지 않습니다.

2024년 에틸렌옥사이드 시장은 아시아태평양에서 폴리에스테르 섬유와 PET 수지의 생산량이 확대됨에 따라 에틸렌글리콜이 75.57%의 점유율을 획득하여 그 기반을 형성했습니다. 업스트림 공급 중단으로 인해 가격 변동이 재발했고 아시아 구매자는 종합 제조업체와 장기 계약을 확보하게 되었습니다. 이와 병행하여 브랜드 소유자가 보다 저탄소 패키징을 요구하게 되어 바이오MEG의 파일럿 생산이 활발해지고 있습니다.

에탄올아민의 공헌량은 적지만, 2030년까지의 CAGR은 3.69%를 나타내고, 농약, 가스 처리, 퍼스널케어 수요가 견인합니다. BASF의 앤트워프에서의 디보틀 네킹은 세계의 알킬 에탄올아민 생산 능력을 30% 가까이 끌어올려 연간 14만 톤 이상으로 이 부문의 전략적 가치를 명확히 했습니다. 라틴아메리카와 아시아에서 글리포세이트 제초제의 생산량 증가는 모노에탄올아민의 풀쓰루를 유지하고, 트리에탄올아민은 CO2 포집용제에 새로운 기회를 발견합니다. 강하의 강력한 다각화로 인해이 유도체 클래스는 단일 산업의 순환성으로부터 보호됩니다.

PET 수지와 폴리에스테르 섬유는 2024년 에틸렌옥사이드 수요의 28.19%를 흡수했습니다. PET와 관련된 산화 에틸렌 시장 규모는 음료 제조업체가 유리와 금속에서 경량 PET 병으로 전환함에 따라 꾸준히 성장할 것으로 예측됩니다. 디메틸카보네이트를 이용한 메탄올리시스 등의 혁신적인 해중합 경로로 테레프탈산디메틸의 수율이 90%를 넘어 고순도의 재생 PET 스트림이 열리고 있습니다. 예측 기간 동안 버진 PET 수요는 선진국에서는 완만해지지만, 재활용 인프라가 미정비된 급성장 경제권에서는 확대됩니다.

멸균과 훈증은 CAGR 3.81%에서 가장 빠르게 성장하는 용도입니다. 약 50,000 유형의 의료기기가 에틸렌옥사이드 멸균에 의존하고 있으며, 감마선이나 전자선을 견딜 수 없는 열가용성 폴리머를 보존하고 있습니다. 배출 규제가 엄격해지더라도, 다른 방법으로는 복잡한 포장을 관통할 수 없거나 요구되는 멸균 보증 수준을 달성하지 못하는 경우가 많기 때문에 수요는 지속되고 있습니다. 촉매 산화 장치와 지속적인 방출 모니터링에 대한 투자는 컴플라이언스를 준수하는 운영을 가능하게 하고, 이 틈새 분야에서의 성장을 지속하고 있습니다.

산화 에틸렌 시장 보고서는 유도체(에틸렌 글리콜, 에톡 실레이트, 에탄올 아민 등), 응용(폴리 에스테르 섬유 및 PET 수지, 계면 활성제 및 세제, 기타), 최종 사용자 산업(자동차, 농약, 음식 및 기타,), 원료(석유 기반 에틸렌 및 바이오 에틸렌), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카

아시아태평양은 2024년에도 최대의 에틸렌옥사이드 시장으로 지속되어 세계 수요의 51.09%를 공급하고, 2030년까지의 CAGR은 3.82%로 지역을 선도해 확대하고 있습니다. 중국은 BASF의 Zhanjiang Verbund 컴플렉스가 2025년에 스타트업할 예정이며, 생산 능력 증강의 축이 되고 있습니다. 인도의 생산은 정부의 제조 장려책에 의해 지원되고 현지에서 폴리에스테르 섬유의 확대와 함께 성장합니다. 지역 정부는 환경 규제를 강화하지만 고급 삭감 시설을 갖춘 통합 컴플렉스는 경쟁력을 유지합니다.

북미는 셰일 옥사이드를 기반으로 하는 에탄의 경제성에서 혜택을 받으며, 에틸렌의 현금 비용은 세계에서 가장 낮은 수준에 있습니다. 의료기기의 멸균이 집중됨에 따라 국내 소비가 증가하고 INEOS가 2024년에 LyondellBasell의 Bayport 유닛을 인수함으로써 최대 단일 시장 공급이 통합됩니다. 미국 환경보호청(EPA)의 배기 가스 규제 대응은 촉매 스크러버와 실시간 모니터링에 대한 투자를 가속화하고 세계 기술 벤치마크를 확립합니다.

유럽은 에너지 가격 상승과 CO2 목표 강화에 직면해 2023년부터 2024년까지 1,100만 톤의 지역화학 생산 능력 폐쇄를 촉진합니다. 저탄소 에틸렌과 에틸렌옥사이드 유도체를 공급하기 위한 2024년 클라리언트-OMV 협정과 같은 협력 관계는 수입품으로부터 시장 점유율을 보호하기 위한 것입니다. 동유럽은 파이프라인 가스에 접근하고 확립된 폴리에스테르 강하 자산을 통해 선택적 경쟁력을 유지합니다.

중동에서는 사우디아라비아에 본사를 둔 생산자가 아시아 수출 시장을 목표로 통합 컴플렉스에서 유리한 원료를 활용하고 있습니다. 아프리카에서는 국내 생산이 제한적이지만 세제 및 농약 제제에 안정적인 수입이 있습니다. 남미는 브라질에서 바이오에틸렌 프로젝트를 추진하고 향후 10년간 아대륙을 저탄소 유도품의 순수출국으로 만들 가능성이 있습니다.

The Ethylene Oxide Market size is estimated at 37.30 Million tons in 2025, and is expected to reach 44.04 Million tons by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

Demand stems from its versatility as a chemical intermediate, with polyester fibers, PET resins, surfactants, ethanolamines, and sterilants underpinning consumption growth. Expansion of polyester-based textiles, wider adoption of PET for lightweight food and beverage packaging, and regulatory-driven investments in medical device sterilization facilities remain the core drivers. Rapid uptake of bio-ethylene feedstock, rising investment in emission-control technology, and the spread of circular-economy initiatives are reshaping sourcing strategies and opening new revenue pools. Competitive dynamics favor vertically integrated producers that can balance feedstock volatility, comply with tightening emission limits, and develop specialty derivatives.

PET packaging adoption is accelerating because brand owners favor lightweight, recyclable solutions that preserve product integrity. Monoethylene glycol derived from ethylene oxide constitutes nearly 90% of the ethylene glycol pool used for PET polymerization, causing direct pull-through on upstream demand. Large resin producers are backing chemical-recycling platforms that depolymerize post-consumer PET into monomers with yields above 90%, enabling circular supply chains while keeping ethylene oxide volumes steady. Companies such as Dow have earmarked multi-million-metric-ton programs to deliver circular and renewable plastics annually by 2030. These initiatives strengthen long-term demand visibility even as the product mix shifts toward recycled grades.

Surfactants and detergents formulated with ethoxylates and ethanolamines deliver superior cleaning efficiency, especially in hard-water regions. Consumer preference for eco-friendly ingredients is prompting producers such as Nouryon to certify green ethylene oxide derivatives under the ISCC PLUS scheme. Switching from alkylphenol to fatty-alcohol ethoxylates aligns with forthcoming biodegradability regulations while sustaining performance. Capacity additions in Europe and North America are timed to capture this demand uptick as private-label cleaning brands gain retail shelf space.

Ethylene oxide is classified as carcinogenic, prompting the EPA's January 2025 interim decision that cuts worker exposure limits from 0.5 ppm by 2028 down to 0.1 ppm by 2035. Compliance demands costly engineering controls, personal monitoring, and capital upgrades. Some healthcare device makers are accelerating the qualification of alternative sterilization methods, including gamma radiation, vaporized hydrogen peroxide, and nitrogen dioxide. While these substitutes will erode specific volumes, ethylene oxide remains indispensable for heat-sensitive devices with intricate lumens.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ethylene glycols formed the bedrock of the ethylene oxide market in 2024, capturing 75.57% share as polyester fiber and PET resin output scaled in Asia-Pacific. Price volatility has returned following upstream supply disruptions, pushing Asia-based buyers to secure long-term contracts with integrated producers. In parallel, bio-MEG pilots are gaining traction as brand owners seek lower-carbon packaging options.

Ethanolamines contribute a smaller volume but post the highest 3.69% CAGR to 2030, driven by agrochemicals, gas treatment, and personal-care demand. BASF's Antwerp debottlenecking raised global alkyl ethanolamine capacity by nearly 30% to more than 140,000 t per year, underscoring the segment's strategic value. Rising glyphosate herbicide volumes in Latin America and Asia sustain monoethanolamine pull-through, while triethanolamine sees new opportunities in CO2 capture solvents. Strong downstream diversification shields this derivative class from single-industry cyclicality.

PET resins and polyester fibers absorbed 28.19% of ethylene oxide demand in 2024. The ethylene oxide market size linked to PET is expected to grow steadily as beverage companies transition from glass and metal to lightweight PET bottles. Innovative depolymerization pathways such as dimethyl-carbonate-aided methanolysis enable greater than 90% dimethyl terephthalate yields, opening high-purity recycled PET streams. Over the forecast horizon, virgin demand moderates in developed regions yet expands in fast-growing economies where recycling infrastructure remains nascent.

Sterilization and fumigation ranked as the fastest-growing application at 3.81% CAGR. Approximately 50,000 distinct medical devices rely on ethylene oxide sterilization, preserving thermolabile polymers that cannot withstand gamma or electron-beam radiation. Even with stringent emissions limits, demand persists because alternative modalities often fail to penetrate complex packaging or achieve required sterility assurance levels. Investment in catalytic oxidation units and continuous emissions monitoring allows compliant operations, sustaining growth in this niche.

The Ethylene Oxide Market Report is Segmented by Derivative (Ethylene Glycols, Ethoxylates, Ethanolamines, and More), Application (Polyester Fiber and PET Resins, Surfactants and Detergents, and More), End-User Industry (Automotive, Agrochemicals, Food and Beverage, and More), Feedstock (Petro-Based Ethylene and Bio-Ethylene), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Asia-Pacific remained the largest ethylene oxide market in 2024, supplying 51.09% of global demand and expanding at a region-leading 3.82% CAGR to 2030. China anchors capacity additions with BASF's Zhanjiang Verbund complex slated for start-up in 2025. India's production grows alongside local polyester fiber expansion, supported by government manufacturing incentives. Regional governments tighten environmental norms, but integrated complexes with advanced abatement maintain competitiveness.

North America benefits from shale-based ethane economics that yield some of the world's lowest ethylene cash costs. Medical device sterilization concentration elevates domestic consumption, and INEOS's 2024 acquisition of LyondellBasell's Bayport unit consolidates supply in the largest single market. Compliance with EPA emission rules accelerates investment in catalytic scrubbers and real-time monitoring, setting a global technology benchmark.

Europe confronts high energy prices and more stringent CO2 targets, prompting 11 million tons of regional chemical capacity closures during 2023-2024. Collaborations such as the 2024 Clariant-OMV agreement to supply lower-carbon ethylene and ethylene oxide derivatives aim to defend market share against imports. Eastern Europe retains selective competitiveness through access to pipeline gas and established downstream polyester assets.

The Middle East leverages advantaged feedstock at integrated complexes, with Saudi-based producers targeting export markets in Asia. Africa sees limited local production but steady imports for detergent and agrochemical formulations. South America advances bio-ethylene projects in Brazil, positioning the subcontinent as a potential net exporter of low-carbon derivatives over the next decade.