인도의 네트워크 보안 및 사이버 리스크 관리 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

India Network Security And Cyber Risk Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1637918

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

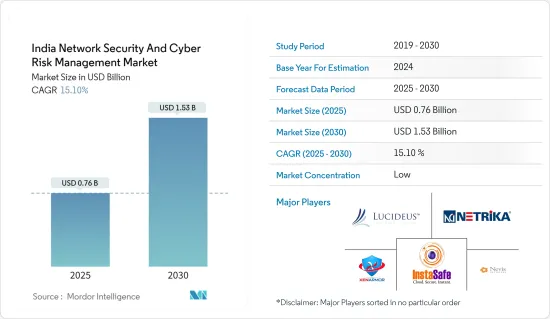

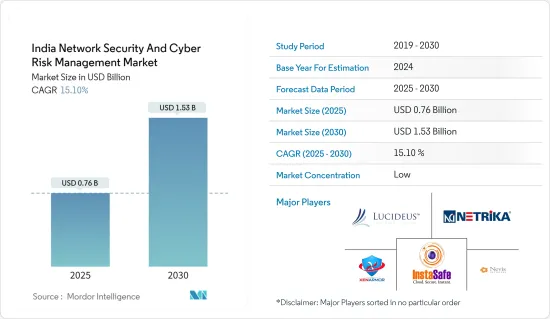

인도의 네트워크 보안 및 사이버 리스크 관리 시장 규모는 2025년 7억 6,000만 달러, 2030년 15억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 15.1%에 이를 것으로 예측됩니다.

과거에, 인도는 주로 정치적 이유로 사이버 공격의 표적이 되어 왔으며, 동향을 보면 보다 고도의 기술이 이용 가능하게 되고, 거래가 복잡화됨에 따라, 시스템의 취약성이 증가하고 있기 때문에 이러한 상황은 점점 현저해질 것으로 보입니다.

주요 하이라이트

인도 산업의 디지털화를 목표로 하는 정부의 이니셔티브가 시장의 주요 견인 요인이 될 것으로 예상됩니다. Make in India', 'Start-Up India', 'Digital India'와 같은 정부 계획은 인도 사이버 보안 시장의 성장을 보완하고 관민 파트너십(PPP) 모델에 대한 연결 핀이 되었습니다.

인도에서는 중요 인프라는 공공 부문과 민간 부문이 소유하고 있으며 사이버 공격으로부터 인프라를 보호하기위한 규범과 프로토콜로 운영됩니다. 그러나 공공 영역과 민간 영역에서 이루어지는 노력을 통합하는 국가 보안 아키텍처는 존재하지 않습니다.

원격근무 동향이 경계가 없는 네트워크 배치로 향하는 중, 클라우드의 도입은 국제적으로 중요한 투자 목표가 되고 있습니다. 이 급속한 디지털화는 데이터 및 개인 정보 보호에 대한 규제 강화, 새로운 기술 스택을 기업 IT에 통합, 클라우드 및 원격 협업 기술의 결과를 가져왔습니다.

이러한 변화와 보드 증가는 세계적인 사이버 보안 수요와 지출을 촉진하고 있습니다. 세계 지식과 경험을 갖춘 인도 IT 서비스와 독창적인 인도 사이버 보안 제품 에코시스템은 고객의 세계 디지털 변화 여행을 보장하는 두 가지 성장 엔진이 되었습니다.

또한 COVID-19는 인도의 디지털 변혁의 길을 가속화했습니다. 처음에는 사업 계속에 중점을 두고 있었지만, 현재는 디지털화의 역학에 현저한 변화가 보입니다. 조직이 새로운 현실에 적응함에 따라 디지털 주도의 조직 전략을 개발하게 되어 사이버 공격의 위험이 증가하고 있습니다.

인도의 네트워크 보안 및 사이버 리스크 관리 시장 동향

침입 감지 및 방어 시스템이 시장을 석권

침입 감지 및 방어 소프트웨어(IDPS)는 네트워크 트래픽을 모니터링하여 공격의 징후를 탐색합니다. 잠재적으로 위험한 활동을 감지하면 공격을 막기 위한 조치를 취합니다. 종종 악성 패킷을 삭제하거나 네트워크 트래픽을 차단하고 연결을 재설정합니다. 또한 IDPS는 일반적으로 잠재적인 악의적인 활동에 대해 보안 관리자에게 경고를 보냅니다.

IDS 또는 IPS를 성공적으로 구축하고 운영하는 두 가지 주요 요인은 배포된 서명과 이를 통과하는 네트워크 트래픽입니다.

시장은 신기하고 저가의 안전한 저전력 침입 감지 및 방지 솔루션을 제공하기 위해 공공기관과 상업조직 모두 연구개발비가 증가한 결과 확대되고 있습니다. 시장 규모는 가정과 상업시설의 안전과 보안에 대한 의식이 높아짐에 따라 확대되고 있습니다.

게다가 제조업 투자를 장려함으로써 인도제품 개발, 제조, 조립을 촉진하는 것을 목적으로 한 'Make in India'와 같은 정부의 대처나 인터넷의 접속성을 향상시키고 국민을 기술면에서 디지털 엠파워먼트 시키기 위해 시작된 'Digital India'와 같은 정부의 캠페인이 국내 IDP 시스템의 성장에 영향을 주고 있습니다.

휴대폰 성장이 시장 성장을 크게 견인

인도에서는 기술에 익숙한 인구가 현저하게 증가하고 있으며 휴대폰은 최초의 디지털 미디어입니다. 인도에는 12억 명의 휴대전화 사용자가 있으며, 그 중 7억 5,000만 명이 스마트폰을 이용하고 있습니다. 향후 5년간 인도는 2위 스마트폰 제조국이 될 것으로 예상됩니다.

인도에서는 스마트폰의 보급에 따라 인터넷 수요도 지속적으로 성장하고 있습니다. IAMAI(The Internet and Mobile Association of India)가 발표한 보고서에 따르면, 국내 액티브 인터넷 사용자는 현재 6억 9,200만 명으로, 농촌의 성장에 견인되어, 2025년에는 9억명에 달할 것으로 추정되고 있습니다.

동시에 인도의 IT 지출은 크게 증가하고 있으며 사물인터넷(IoT), 클라우드 컴퓨팅, 인공지능(AI), 블록체인 등의 기술 이용도 확대되고 있습니다.

Ericsson에 따르면 2022년 인도에서 사용된 스마트폰 계약 수의 주류 기술은 LTE로 약 8억 500만대에 달했습니다. 2024년에는 약 8억 3,860만 계약으로 피크에 이를 것으로 예상되었으며, 3G 연결은 그 시점에서 2,200만으로 추정되었습니다. 5G는 2027년 말 인도 전체 스마트폰 계약 수 11억 3,000만 건 중 약 6억 4,650만 건이 될 것으로 예측됐습니다.

인도의 네트워크 보안 및 사이버 리스크 관리 산업 개요

인도의 네트워크 보안 및 사이버 리스크 관리 시장은 단편화되어 있으며 Lucideus Tech, Instasafe, XenArmor, ArraySheild Technologies, Netrika Consulting India Pvt Ltd.와 같은 대기업이 존재합니다. 이 시장의 기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수와 같은 전략을 채택하고 있습니다.

2023년 2월 - 인도에서 보험 및 위험 관리 서비스를 제공하는 Raghnall Insurance Broking은 모든 규모의 기업을 위해 Business Cyber Shield를 발표했습니다. 이 기술은 완벽한 사이버 보안 솔루션을 제공하는 것을 목표로 합니다. 비즈니스 사이버 쉴드의 소개를 통해 Raghnall는 고객에게 사이버 공격의 위험성 증가와 관련된 위험을 식별, 최소화 및 관리하기 위한 최신 디지털 솔루션을 제공하는 데 전념하고 있음을 나타냅니다.

2023년 1월 - InstaSafe는 인도 및 동남아시아 기술 서비스 및 솔루션 제공업체인 Value InfoSolutions와 제휴하여 인도 및 SAARC 지역을 통해 제품 제공을 확대할 계획을 발표했습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인과 시장 성장 억제요인의 소개

시장 성장 촉진요인

산업 디지털화를 위한 정부의 대처가 시장 성장을 가속

시장 성장 억제요인

국가 안보 인프라의 부재가 시장 성장을 저해

산업 밸류체인 분석

업계의 매력도 - Porter's Five Forces 분석

구매자/소비자의 협상력

공급기업의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

부문별

시큐리티 정보 및 이벤트 관리(SIEM)

보안 웹 게이트웨이(SWG)

아이덴티티 거버넌스와 관리(IGA)

엔터프라이즈 컨텐츠 어웨어 데이터 유출 방지(DLP)

솔루션별

암호화

아이덴티티 액세스 관리(IAM)

데이터 유출 방지(DLP)

침입 감지 시스템/침입 방어 시스템(IDS/IPS)

기타 솔루션

서비스별

네트워크 보안

엔드포인트 보안

무선 보안

클라우드 보안

기타 서비스

업계별

항공우주 및 방위

소매

정부기관

헬스케어

IT&텔레콤

BFSI

제6장 경쟁 구도

기업 프로파일

Lucideus Tech

Instasafe

XenArmor

ArraySheild Technologies

Netrika Consulting India Pvt Ltd.

Aspirantz InfoSec

Cyberoam

Data Resolve Technologies

Mirox Cyber Security & Technology

제7장 투자 분석

제8장 시장 기회와 앞으로의 동향

JHS

영문 목차

영문목차

The India Network Security And Cyber Risk Management Market size is estimated at USD 0.76 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 15.1% during the forecast period (2025-2030).

In the past, India has been targeted through cyber-attacks primarily for political reasons, and trends show that this landscape seems to only gain prominence with the availability of more sophisticated technology and more complex transactions increasing the vulnerability of systems.

Key Highlights

Government initiatives aimed at digitizing Indian industries are expected to be the major driving factor for the market. Government schemes such as 'Make in India,' 'Start-Up India,' and 'Digital India' supplement the growth of Cyber Security market in India and are a linking pin towards Public-Private Partnership (PPP) models.

In India, Critical infrastructure is owned by both Public Sector and Private sector, operating with their norms and protocols for protecting their infrastructure from cyber-attacks. But there is no national security architecture that unifies the efforts taking place in the public sphere and the private sphere.

As the trend of remote working is driving into a borderless network arrangement, cloud adoption has become a critical investment goal internationally. This fast digitization has resulted in a greater regulatory focus on data and privacy, integration of new technology stacks into company IT, and cloud and remote collaboration technologies.

These changes and increased board are driving global cybersecurity demand and spending. Indian IT services, with their worldwide knowledge and experience, and the creative Indian cybersecurity product ecosystem have been the twin growth engines ensuring customers' global digital transformative journeys.

Moreover, COVID-19 accelerated the country's digital transformation path. Initially, the emphasis was on business continuity, but there is now a noticeable shift in the dynamics of digitalization. As organizations adjust to the new reality, they are developing digitally led organizational strategies, which has increased the risk of cyber attacks.

India Network Security And Cyber Risk Management Market Trends

Intrusion Detection and Prevention System to Dominate the Market

An Intrusion Detection and Prevention Software (IDPS) monitors network traffic for signs of a possible attack. When it detects potentially dangerous activity, it takes action to stop the attack. Often this takes the form of dropping malicious packets, blocking network traffic or resetting connections. The IDPS also usually sends an alert to security administrators about the potential malicious activity.

The two main contributors to the successful deployment and operation of an IDS or IPS are the deployed signatures and the network traffic that flows through it.

The market is expanding as a result of rising R&D expenditures by both public and commercial organisations to provide novel and affordable secured low-power intrusion detection and prevention solutions. The market size is increased by rising awareness of home and commercial safety and security.

Moreover, government initiatives like 'Make in India', which aims to promote the development, manufacture, and assembly of products made in India by incentivizing dedicated investments into manufacturing, and government campaigns like 'Digital India,' which was launched to ensure increased Internet connectivity and make the nation digitally empowered in terms of technology, have been influencing the growth of the IDP system in the country.

Growth in Mobile Phones to Significantly Drive the Market Growth

India has seen a tremendous growth in tech savvy population, with mobile phones being the first digital medium. In India, there are 1.2 billion mobile customers, 750 million of whom use smartphones. The nation is anticipated to be the second-largest smartphone manufacturer in the coming five years.

With the growing number of smartphones in India, the demand for the Internet is continuously growing in the country. According to the report published by IAMAI (The Internet and Mobile Association of India), there are currently 692 million active internet users in the country, and the number is estimated to hit 900 million by 2025, led by growth in rural areas.

At the same time, there has been substantial growth in IT spending in India and a scaling up in the use of technologies such as the Internet of Things (IoT), Cloud Computing, Artificial Intelligence (AI), and BlockChain.

According to Ericsson, In 2022, the dominant technology of smartphone subscriptions used in India was LTE, which had reached nearly 805 million. It was expected to peak in 2024 at around 838.6 million subscriptions, with 3G connections estimated at 22 million by that point. 5G was forecasted to be about 646.5 million of all 1.13 billion smartphone subscriptions in India at the end of 2027.

India Network Security And Cyber Risk Management Industry Overview

India Network Security And Cyber Risk Management Market is fragmented, with the presence of major players like Lucideus Tech, Instasafe, XenArmor, ArraySheild Technologies, and Netrika Consulting India Pvt Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

February 2023 - Raghnall Insurance Broking, a supplier of insurance and risk management services in India, announced the launch of Business Cyber Shield for companies of all sizes. This technology is intended to offer complete cybersecurity solutions. With the introduction of Business Cyber Shield, Raghnall demonstrates its dedication to giving its clients access to the most up-to-date digital solutions for identifying, minimizing, and managing the risks connected with the rising danger of cyber-attacks.

January 2023 - InstaSafe announced plans to expand its product offerings through India and the SAARC region by partnering with Value InfoSolutions, a technology services and solutions provider in India and Southeast Asia.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Introduction to Market Drivers and Restraints

4.3 Market Drivers

4.3.1 Government Initiatives Towards Digitizing Industries is Driving the Market Growth

4.4 Market Restraints

4.4.1 Absence of National Security Infrastructure is Discouraging the Market Growth

4.5 Industry Value Chain Analysis

4.6 Industry Attractiveness - Porter's Five Forces Analysis

4.6.1 Bargaining Power of Buyers/Consumers

4.6.2 Bargaining Power of Suppliers

4.6.3 Threat of New Entrants

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Segment

5.1.1 Security Information and Event Management (SIEM)

5.1.2 Security Web Gateway (SWG)

5.1.3 Identity Governance and Administration (IGA)

5.1.4 Enterprise Content-Aware Data Loss Prevention (DLP)

5.2 By Solution

5.2.1 Encryption

5.2.2 Identity and Access Management (IAM)

5.2.3 Data Loss Protection (DLP)

5.2.4 Intrusion Detection System/Intrusion Prevention System (IDS/IPS)