아시아태평양의 무균 포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Asia Pacific Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1637898

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

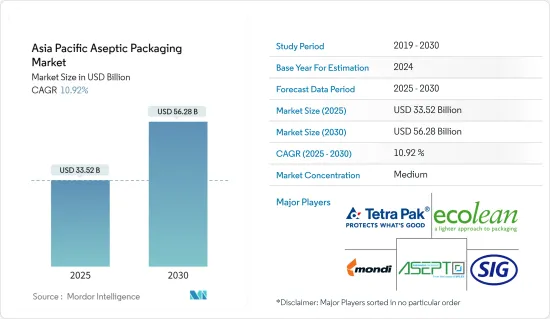

아시아태평양의 무균 포장 시장 규모는 2025년에 335억 2,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 10.92%로, 2030년에는 562억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

아시아태평양의 무균 포장 시장은 주로 인도, 중국, 일본 등의 국가들이 견인하고 있습니다. 가처분 소득 증가와 식품 산업의 성장으로 이 지역의 여러 국가는 무균 포장 솔루션의 채택을 촉구하고 있습니다. 이 추세는 앞으로 몇 년동안 무균 포장 시장에 기회를 가져올 것입니다.

이 지역에서 소비자의 식습관 변화는 즉석식품에 대한 선호도 증가와 편리하면서도 품질 높은 식품에 대한 수요 증가로 이어져 시장 성장을 가속하고 있습니다. 이 변화는 특히 도시 지역에서 두드러지며 시간적인 제약과 바쁜 라이프 스타일은 빠르고 간편한 식사 솔루션의 필요성을 높입니다. 무균 포장 시장의 각 기업은 식품의 안전성을 확보하고 보존 기간을 연장하는 혁신적인 포장 솔루션을 개발함으로써 이러한 소비자 요구의 변화에 대응하고 있습니다.

무균 기술은 기존 방법보다 경제적인 재료를 사용하여 포장 비용을 크게 줄입니다. 이 혁신적인 접근법은 보존료의 필요성을 최소화하고 소비자의 건강과 환경의 지속가능성에 큰 이점을 제공합니다. 게다가, 무균 기술은 소량의 음료를 정밀하게 생산할 수 있게 하고 공급사슬 전반에 걸쳐 폐기물을 줄이는데 도움이 됩니다. 이러한 생산량의 유연성을 통해 기업은 생산량을 수요에 잘 맞출 수 있으므로 전반적인 제조 비용을 낮출 수 있습니다. 이 기술의 효율성은 에너지 소비량과 보관 요건도 향상시켜 음료 업계에서의 비용 대비 효과와 환경면에서의 우위성을 높이고 있습니다.

시장 개척 기업은 또한 진화하는 업계에서 경쟁력을 유지하기 위해 연구 개발에 투자하고 있습니다. 신제품 출시는 시장 동향과 일치하며 수요를 충족시킵니다. 제약 업계에서는 무균 포장 요구가 증가하고 있으며 이는 시장 성장에 기여하고 있습니다. 각국 정부는 헬스케어 분야의 지출을 끌어올리고 있으며, 이는 무균 포장 시장을 더욱 뒷받침하고 있습니다. 이렇듯 제약 산업과 식품 업계의 무균 포장에 대한 수요 증가는 시장 성장을 가속할 것으로 기대됩니다.

예를 들어 SIG는 2023년 4월 인도 팔걸에 두 번째 생산 시설을 개설했습니다. 이 공장은 SIG사의 백 인 박스와 스파우트 파우치 포장을 제조했으며 이전에는 Scholle IPN 및 Bossar 브랜드로 판매했습니다. 뭄바이의 북쪽 90km에 위치한 이 새로운 공장은 팔걸에 있는 SIG의 기존 공장을 보완하는 것으로, 이 공장에서는 부품과 완성품의 포장재를 생산하고 있습니다. 첫 번째 공장에는 블로운 필름 압출기, 사출 성형 셀, 백 인 박스 제조기, 백 인 박스 및 스파우트 파우치 제품에 사용되는 포장 피팅 및 캡금형 제조 설비를 갖추고 있습니다.

지속가능한 포장과 유통기한의 연장은 식품 및 음료 산업의 소비자에게 매우 중요한 요소입니다. 그 결과, 이 지역의 많은 음식 및 음료 공급업체는 비용 효율성과 환경친화성, 특히 운송 및 현지 보관에 대한 차원에서 무균 포장을 선택합니다. 이 지역의 무균 포장에 대한 높은 수요는 재활용 가능한 골판지와 친환경 소재에서 비롯됩니다. 이 포장 유형은 소량을 선호하고 자주 구매하는 소비자들 사이에서 인기가 있습니다.

이 시장은 고분자 가격 상승으로 인한 비용 압력이 크고 이로 인해 생산비 전체가 상승하고 있습니다. 팬데믹 발생 이후 원재료 비용이 크게 상승했으며 러시아 우크라이나 전쟁은 이 가격 상승을 더욱 악화시켰습니다. 동시에 플라스틱과 플라스틱 제품에 대한 수요는 매년 계속 성장하고 있고 공급은 이 수요 증가를 따라잡지 못하면서 폴리머 가격 상승 추세를 조장하고 있습니다.

아시아태평양의 무균 포장 시장 동향

음료 부문이 큰 점유율을 차지할 전망

아시아태평양 국가에서는 도시화가 급속히 진행되고 있으며 주스와 가향 우유를 포함한 음료 및 천연 제품에 대한 수요가 증가하고 있습니다. 이 지역의 소비자 구매력 증가는 무균 팩 수요를 높이는 중요한 요인이 되었습니다. 특히 팬데믹 후의 건강한 라이프 스타일의 동향과 위생 의식의 고조가 아시아태평양 전역의 무균 팩 시장을 크게 밀어 올리고 있습니다.

포장은 비알코올 음료의 부가가치를 높이고 차별화를 도모하는데 중요한 역할을 하고 있습니다. 이러한 제품에 대한 소비자의 관심이 높아짐에 따라 효과적인 포장 솔루션에 대한 수요가 높아질 것으로 예상됩니다. 비알코올 음료 포장은 취급이나 보관 중 오염과 누출로부터 액체를 보호해야 합니다. 주스와 에너지 음료와 같은 제품의 경우, 무균 포장은 내용물을 외부 요인으로부터 보호합니다. 이 포장은 일반적으로 열가소성 플라스틱, 판지, 알루미늄 포일을 결합하여 제품의 무결성을 보장합니다.

무균 기술은 기존 방법보다 경제적인 재료를 사용하여 포장 비용을 크게 줄입니다. 이 비용 효과는 제품 무결성을 유지하면서 가볍고 얇은 포장 재료를 사용할 수 있기 때문에 발생합니다. 이 기술은 또한 방부제의 필요성을 최소화하고 음료의 화학 첨가물을 줄임으로써 소비자의 건강과 환경에 기여합니다. 무균 가공은 냉장 없이 유통 기한을 연장할 수 있어 보관 및 운송에서 에너지를 절약할 수 있습니다.

게다가 이 기술은 소량의 음료 생산을 가능하게 하고 보다 정밀한 생산을 가능하게 하므로 폐기물 절감으로 이어집니다. 이러한 생산량의 유연성은 과잉 생산 및 재고 보유 비용을 줄이고 전체 생산 비용을 절감합니다. 이러한 요인들이 결합됨에 따라 무균 기술은 생산 공정 최적화와 운영 비용 절감을 목표로 하는 음료 제조업체들에게 매력적인 선택입니다.

음료 패키지 수요는 예측 기간 동안 증가할 것으로 예상됩니다. 다양한 크기의 무균 포장은 음료 보관 및 유통에 널리 사용되며 선적 및 보관에 적합합니다. 소비자가 안전하고 신선한 제품을 선호하기 때문에 이 지역의 무균 포장에 대한 수요가 늘어날 것으로 보입니다.

간편성은 RTD(Ready To Drink) 음료와 건강 복지 카테고리에서 중요한 동향으로 떠오르고 있습니다. 소비자는 음료를 처음부터 준비하는 데 시간이 많이 걸리므로 즉시 마실 수 있는 칵테일을 선호합니다. RTD 음료는 지난 몇 년동안 모든 음료 카테고리 중에서 가장 현저히 성장하였습니다. 소비자는 이러한 음료의 독특한 맛과 집 밖에서 마실 수 있는 편의성에 매력을 느낍니다.

네슬레 인디아는 유명 커피 브랜드인 네스카페의 다양한 RTD 음료 출시를 발표했습니다. 이 회사는 180ml 1팩당 30루피로 소매점 및 전자상거래 채널을 통해 RTD 커피 판매를 시작했습니다. 이 제품은 무균 포장을 채택하고 판매 증가에 기여합니다. 매출은 2017년 12억 1,000만 달러에서 2023년에는 22억 6,000만 달러로 증가했습니다. RTD 제품에 대한 수요 증가도 이 지역의 무균 포장 시장을 밀어 올릴 것으로 보입니다.

네슬레 인디아의 RTD 커피는 음료 부문에서 중요한 움직임을 상징합니다. 무균 포장은 이러한 제품의 품질을 유지하고 냉장이 필요없이 유통 기한을 연장하는 데 중요한 역할을 합니다. 이 포장 기술은 실온에서 장기간 보관해도 커피의 신선도와 안전성을 유지합니다.

인도는 예측기간 동안 고성장을 기록할 전망

인도는 유제품 산업에 크게 기여하고 있습니다. 일회용 플라스틱에 대한 규제가 엄격하기 때문에 시장 관계자는 생분해성으로 재사용 가능한 무균 포장을 개발할 수 있는 큰 기회를 얻고 있습니다. 지속가능한 포장 옵션에는 바이오에탄올로 만들어진 폴리에틸렌, 폴리유산, 미세섬유상 셀룰로오스 및 기타 생분해성 재료와 같은 재사용 가능한 재료가 포함됩니다.

인구 증가, 소득 증가, 라이프 스타일 변화가 무균 포장 산업을 견인하고 있습니다. 최종 사용자 분야에서의 성장 전망이 증가함에 따라 무균 포장 수요가 촉진되고 있습니다. 그러나 시장 확대는 대체 포장 옵션, 특히 파우치 포장의 사용 증가에 의해 제한됩니다. 인도는 아시아태평양의 무균 포장 시장에서 큰 점유율을 차지할 것으로 예상되며, 이는 포장 식품에 대한 수요의 급성장과 가처분 소득 증가에 기인하고 있습니다.

인도는 세계에서 가장 큰 우유 소비국이며 다양하고 광범위한 낙농 산업을 자랑합니다. 이 나라의 원유 생산량은 지난 10년간 현저한 성장을 보였으며, 우타르 프라데시와 라자스탄이 큰 공헌을 하고 있습니다. 이 원유 생산량 증가는 원유와 원유를 원료로 하는 제품의 무균성과 품질을 유지하기 위해 필수적인 무균 포장 수요 증가로 이어졌습니다.

인도농업농민복지부의 보고에 의하면, 2023년도의 생유 생산량은 2억 2,600만 톤에 달하고,, 전년의 2억 2,160만 톤으로부터 현저하게 증가했습니다. 그러나 생유 생산량의 성장률은 약간 둔화되어 2023년도의 약 5.8%에서 다음 해에는 3.83%로 감소했습니다.

성장률의 둔화에도 불구하고 원유 생산량의 전체적인 증가 경향은 계속 시장에 큰 영향을 미칩니다. 원유 생산량이 증가함에 따라 신뢰성 있는 무균 포장 솔루션에 대한 요구도 커지고 있습니다. 이 수요 증가는 인도의 활발한 낙농 산업의 진화하는 요구에 부응하기 위해 제조업체가 노력하면서 시장 혁신과 확대를 뒷받침하고 있습니다.

인도의 소비자들은 아침 주스에서 에너지 음료에 이르기까지 음료 선택에 건강과 웰빙을 점점 더 우선시하고 있으며, 소비자는 웰빙이라는 목적에 맞는 기분 전환에 더 많은 지출을 하고자 합니다. 그 결과 음료 분야에서는 비용 효율적인 포장 솔루션에 대한 수요가 높아지고 있습니다. 특히 우유 및 우유음료 업계에서는 제품의 적층이 용이하고 유통기한이 연장되는 등의 이점을 가지는 무균 팩의 채용이 증가하고 있습니다.

아시아태평양의 무균 포장 산업 개요

아시아태평양의 무균 포장 시장은 여러 벤더들이 진입하고 있기 때문에 경쟁이 심합니다. 시장은 부분 통합되어 있으며, 각 업체는 주로 시장 확대와 경쟁력 유지를 위해 제품 혁신, 합병, 인수 등 다양한 전략을 채택하고 있습니다. 시장의 주요 기업으로는 Tetra Pak International SA, Asepto(UFlex Ltd), SIG Combibloc Group 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

산업 가치사슬 분석

업계의 매력도 - Porter's Five Forces 분석

구매자의 협상력

공급기업의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

아시아태평양의 무균 포장 시장의 기회

기술 스냅샷

제5장 시장 역학

촉진요인

콜드체인 물류 비용 절감 수요 증가

제품의 장기 보존에 대한 수요 증가

시장의 과제

환경과 재활용에 대한 우려

제조의 복잡화(원재료 비용의 상승 등)와 ROI의 저하

제6장 시장 세분화

제품별

판지

봉투 및 파우치

캔

병

용도별

음료

RTD음료

우유음료

식품

가공식품

과일 및 야채

유제품

의약품 및 의료

기타 용도

국가별

중국

인도

일본

동남아시아

제7장 경쟁 구도

기업 프로파일

Tetra Pak International SA

Ecolean Packaging

SIG Combibloc Group

Mondi PLC

Asepto(UFlex Ltd)

Greatview Aseptic Packaging

Hangzhou Hansin New Packing Material Co. Ltd

제8장 투자 분석

제9장 시장의 미래

CSM

영문 목차

영문목차

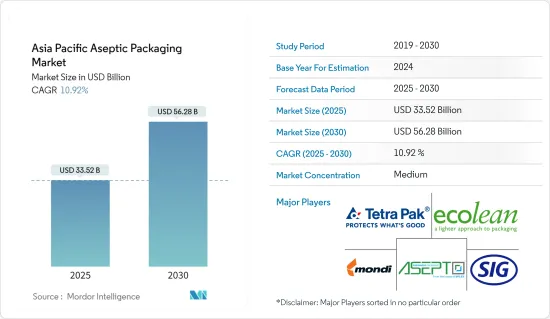

The Asia Pacific Aseptic Packaging Market size is estimated at USD 33.52 billion in 2025, and is expected to reach USD 56.28 billion by 2030, at a CAGR of 10.92% during the forecast period (2025-2030).

Key Highlights

The Asia-Pacific aseptic packaging market is primarily driven by countries such as India, China, and Japan. Increased disposable income and growth in the food and beverage industry have prompted several countries in the region to adopt aseptic packaging solutions. This trend will create opportunities for the aseptic packaging market in the coming years.

Evolving consumer eating habits in the region have led to an increased preference for ready-to-eat meals and a higher demand for convenient, high-quality food products, fostering market growth. This shift is particularly evident in urban areas where time constraints and busy lifestyles are driving the need for quick and easy meal solutions. Players in the aseptic packaging market have responded by developing innovative packaging solutions that ensure food safety and extend shelf life, catering to these changing consumer needs.

Aseptic technology significantly reduces packaging costs using more economical materials than traditional methods. This innovative approach also minimizes the need for preservatives, offering substantial consumer health and environmental sustainability benefits. Furthermore, aseptic technology enables the precision production of smaller beverage quantities, which helps decrease waste throughout the supply chain. This flexibility in production volume lowers overall manufacturing costs, as companies can better match production to demand. The technology's efficiency extends to energy consumption and storage requirements, enhancing its cost-effectiveness and environmental advantages in the beverage industry.

Market players also invest in research and development to stay competitive in evolving industries. New product launches align with market trends and support demand. The pharmaceutical industry's increasing need for aseptic packaging contributes to market growth. Governments across various countries are raising healthcare sector spending, further boosting the aseptic packaging market. Thus, the growing demand for aseptic packaging from the pharmaceutical and food and beverage industries is expected to drive the market's growth.

For instance, SIG inaugurated its second production facility in Palghar, India, in April 2023. This plant manufactures SIG's bag-in-box and spouted pouch packaging, previously marketed under the Scholle IPN and Bossar brands. Located 90 km north of Mumbai, the new facility complements SIG's existing plant in Palghar, which produces components and finished packaging. The first plant has blown film extruders, injection molding cells, bag-in-box manufacturing machines, and a mold-making facility for packaging fitments and closures that are used in bag-in-box and spouted pouch products.

Sustainable packaging and extended shelf life are crucial factors for consumers in the food and beverage industry. Consequently, many food and beverage vendors in the region opt for aseptic packaging, driven by cost efficiency and environmental considerations, particularly regarding transportation and storage in local conditions. The region's high demand for aseptic packaging is attributed to its use of recyclable cardboard and environmentally friendly materials. This packaging type is prevalent among consumers who prefer smaller quantities and make frequent purchases.

The market is experiencing significant cost pressures due to rising polymer prices, which have increased the overall production expenses. Raw material costs have risen substantially since the onset of the pandemic. The Russia-Ukraine War further exacerbated this price escalation. Concurrently, the demand for plastics and plastic products continues to grow annually. The supply has not kept pace with this increasing demand, contributing to the upward trend in polymer prices.

Asia Pacific Aseptic Packaging Market Trends

The Beverages Segment is Expected to Hold a Significant Share

Rapid urbanization in Asia-Pacific countries fuels the rising demand for beverages and natural products, including juices and flavored milk. The growing purchasing power of consumers in the region is a crucial factor contributing to the demand for aseptic cartons. The rising trend of healthier lifestyles and heightened awareness of hygiene, particularly in the aftermath of the pandemic, has significantly boosted the market for aseptic cartons across Asia-Pacific.

Packaging plays a vital role in adding value and differentiating non-alcoholic beverages. As consumer interest in these products grows, the demand for effective packaging solutions is expected to increase. Packaging for non-alcoholic beverages must protect liquids from contamination and leakage during handling and storage. Aseptic packaging shields the contents from external elements for products such as juices and energy drinks. This packaging typically combines thermoplastics, paperboard, and aluminum foil to ensure product integrity.

Aseptic technology significantly reduces packaging costs using more economical materials than traditional methods. This cost-effectiveness stems from the ability to use lighter, thinner packaging materials that still maintain product integrity. The technology also minimizes the need for preservatives, benefiting consumer health and the environment by reducing beverage chemical additives. Aseptic processing allows extended shelf life without refrigeration, which can lead to energy savings in storage and transportation.

Additionally, this technology enables the production of smaller beverage quantities, which helps decrease waste by allowing for more precise production runs. This flexibility in production volume lowers overall production costs by reducing overproduction and inventory-holding expenses. Combining these factors makes aseptic technology an attractive option for beverage manufacturers looking to optimize their production processes and reduce operational costs.

The demand for beverage packaging is expected to increase during the forecast period. Aseptic packaging, available in various sizes, is widely used for storing and distributing beverages, making it suitable for shipping and storage. The demand for aseptic packaging in this region will likely grow as consumers increasingly prefer safe and fresh products.

Convenience has emerged as a significant trend in ready-to-drink beverages and health and well-being categories. Consumers prefer ready-to-drink cocktails due to the time-consuming nature of preparing beverages from scratch. The rise of ready-to-drink options has been a notable development across all beverage categories in recent years. Consumers are attracted to these drinks for their unique flavors and convenience outside the home.

Nestle India Ltd announced the launch of a range of ready-to-drink variants of its renowned coffee brand, Nescafe. The company commenced the sale of ready-to-drink coffee for INR 30 per pack of 180 ml at retail outlets and through its e-commerce channel. This product uses aseptic packaging, which helps the company increase sales. Sales increased to USD 2.26 billion in 2023 from USD 1.21 billion in 2017. The rise in the demand for ready-to-drink products will also boost the aseptic packaging market in the region.

Nestle India Ltd's introduction of ready-to-drink coffee variants represented a significant move in the beverages segment. Aseptic packaging plays a crucial role in preserving the quality and extending the shelf life of such products without the need for refrigeration. This packaging technology ensures that the coffee remains fresh and safe for consumption, even when stored at room temperature for extended periods.

India is Expected to Record High Growth During the Forecast Period

India has made significant contributions to the dairy industry. Due to strict regulations on single-use plastics, market players have substantial opportunities to develop biodegradable and reusable aseptic packages. Sustainable packaging options include reusable materials such as polyethylene made from bioethanol, polylactic acid, micro-fibrillated cellulose, and other biodegradable materials.

Population growth, rising incomes, and lifestyle changes drive the aseptic packaging industry. Increasing growth prospects in end-user segments are fueling the demand for aseptic packaging. However, the market's expansion is constrained by the increased use of alternative packaging options, particularly pouch packaging. India is expected to hold a significant share of the Asia-Pacific aseptic packaging market, propelled by the rapidly growing demand for packaged food products and increasing disposable incomes.

India is the world's largest milk consumer, boasting a diverse and expansive dairy industry. Milk production in the country has shown significant growth over the past decade, with Uttar Pradesh and Rajasthan emerging as substantial contributors. This increase in milk production led to a corresponding rise in the demand for aseptic packaging, essential for maintaining the sterility and quality of milk and milk-based products.

The Ministry of Agriculture and Farmers Welfare (India) reported that milk production reached an impressive 226 million metric tons in fiscal year 2023, a notable increase from the previous year's 221.6 million tons. However, the growth rate in milk production experienced a slight deceleration, decreasing from approximately 5.8% in the fiscal year 2023 to 3.83% in the following year.

Despite this minor slowdown in growth rate, the overall upward trend in milk production continues to impact the market substantially. As milk production volumes increase, so does the need for reliable, sterile packaging solutions. This growing demand drives innovation and expansion in the market as manufacturers strive to meet the evolving needs of India's thriving dairy industry.

Indian consumers are increasingly prioritizing health and wellness in their beverage choices, from morning juices to energy drinks, with consumers willing to spend more on refreshments that align with wellness goals. Consequently, there is a growing demand for cost-effective packaging solutions in the beverages segment. The milk and dairy beverage industries are particularly driving increased adoption of aseptic cartons, which offer advantages such as easy product stacking and extended shelf life.

Asia Pacific Aseptic Packaging Industry Overview

The Asia-Pacific aseptic packaging market is highly competitive due to multiple vendors operating in it. The market is semi-consolidated, with the players adopting various strategies, such as product innovations, mergers, and acquisitions, primarily to expand their reach and stay competitive. Some of the major players in the market include Tetra Pak International SA, Asepto (UFlex Ltd), and SIG Combibloc Group.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Buyers

4.3.2 Bargaining Power of Suppliers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Opportunities in the Asia Pacific Aseptic Packaging Market

4.5 Technology Snapshot

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand to Reduce Cost of Cold Chain Logistics

5.1.2 Increasing Demand for Longer Shelf Life of Products

5.2 Market Challenges

5.2.1 Concerns over Environment and Recycling

5.2.2 Manufacturing Complications( for example increasing cost of raw materials) & Lower ROI

6 MARKET SEGMENTATION

6.1 By Product

6.1.1 Cartons

6.1.2 Bags and Pouches

6.1.3 Cans

6.1.4 Bottles

6.2 By Applications

6.2.1 Beverage

6.2.1.1 Ready-to-drink Beverages

6.2.1.2 Dairy-based Beverages

6.2.2 Food

6.2.2.1 Processed Foods

6.2.2.2 Fruits and Vegetables

6.2.2.3 Dairy Products

6.2.3 Pharmaceutical & Medical

6.2.4 Other Applications

6.3 By Country

6.3.1 China

6.3.2 India

6.3.3 Japan

6.3.4 South East Asia

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Tetra Pak International SA

7.1.2 Ecolean Packaging

7.1.3 SIG Combibloc Group

7.1.4 Mondi PLC

7.1.5 Asepto (UFlex Ltd)

7.1.6 Greatview Aseptic Packaging

7.1.7 Hangzhou Hansin New Packing Material Co. Ltd