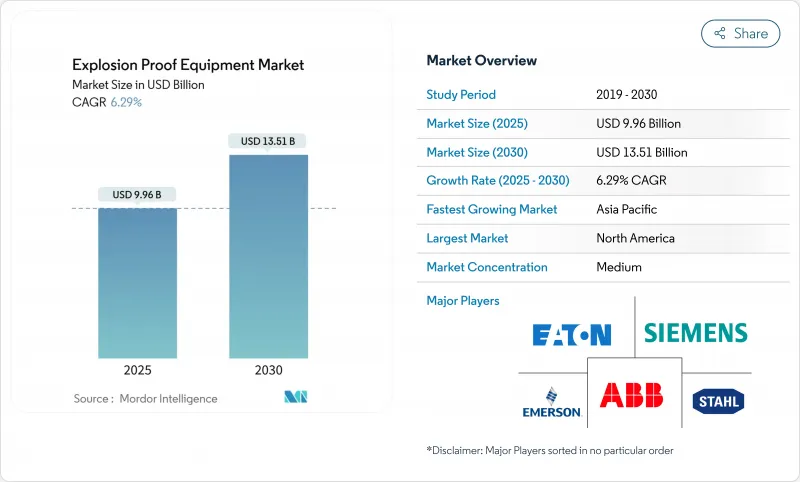

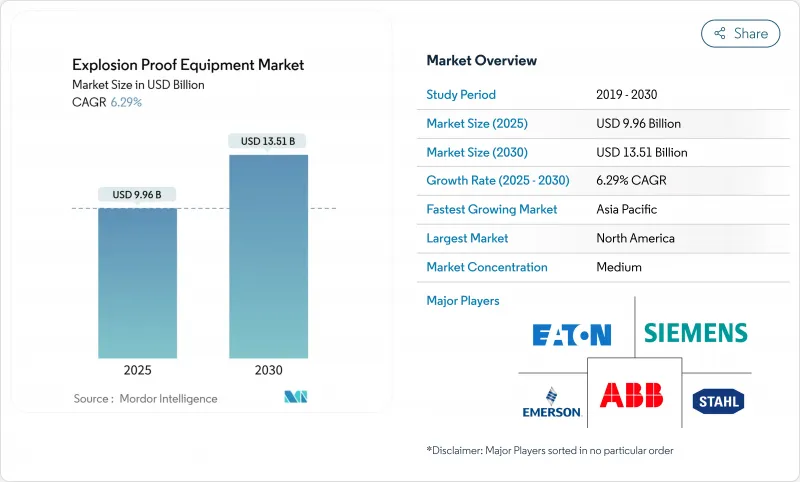

방폭 장비 시장의 2025년 시장 규모는 99억 6,000만 달러로 추정되고, 2030년에는 135억 1,000만 달러에 이를 것으로 예측되며, CAGR 6.29%로 성장할 전망입니다.

확대는 ATEX 및 IECEx 규칙의 보편적인 시행, 그린 수소 플랜트의 신속한 건설, 위험 지역에서의 예지 보전을 촉진하는 IIoT 대응 리노베이션에 대한 지속적인 자본 지출에 의해 지원됩니다. 또한 오프쇼어 및 온쇼어 시설에서 LED 조명으로의 대량 전환과 아시아태평양 전역에서의 리튬 이온 기가팩토리의 출시도 수요에 기여하고 있으며, 각각 방진 구역의 기어가 필요합니다. 북미는 OSHA 규칙과 노후화 설비의 현대화로 규모의 주도권을 유지하고 있지만 아시아태평양은 신흥 수소 회랑, 배터리 공급망, 화학 처리 클러스터 덕분에 가장 빠른 증가량을 창출하고 있습니다. 경쟁 구도는 ABB, 지멘스, 이튼이 밸런스 시트의 강점을 현지 생산 능력으로 재분배하는 반면, 신규 진출기업이 틈새 인증의 격차를 메우기 때문에 적당히 단편화된 채로 남아 있습니다. 눈앞의 역풍으로는 주조품 부족과 중국제 인클로저의 관세가 있으며, 이들은 마진을 압박하고 멀티소싱을 촉진합니다.

규제 당국은 2024년 4월에 ATEX 가이드라인을 강화하고, 적합성 평가를 강화하며, 시험량을 전년 대비 40% 증가시켰습니다. 튀르키예와 한국은 IECex에 준거한 법령을 제정하여 이 움직임을 반영하며, 공급업체는 종종 20년간 가동하는 레거시 라인의 업그레이드를 강요받고 있습니다. 다국적 기업은 하나의 인증으로 여러 지역에서의 판매를 가능하게 하고, 사이클 타임을 단축하며, 엔지니어링의 편차를 줄이기 위해 매칭을 환영합니다. 이러한 규제의 엄격화로 정유소, 케미컬 파크, LNG 수출 허브 등의 교환 수요가 가속화되고 있습니다.

수소는 공기 중에서 4-75%의 가연성을 가지므로, 발화 리스크가 높고, 고도의 봉쇄, 검지 및 환기 시스템이 필요합니다. 중국, 호주 및 멕시코 걸프의 기가와트 규모의 전해조는 맞춤형 방염 스위치 기어와 본질 안전 방폭 센서를 조달하고 방폭 장비 시장 내에 전용 조달 채널을 형성하고 있습니다. 수소에 특화된 인증서를 가진 공급업체는 신속하게 선행자 이익을 확보하고 밸류체인 전체에서 포트폴리오를 분리하고 연구개발 제휴를 촉구하고 있습니다.

엔드 투 엔드의 ATEX 및 IECEx 밸리데이션은 개발 예산의 15-25%를 소비하고, 고급 어셈블리에서는 실험실 대기 시간이 6-12개월에 이릅니다. 소규모 기업에서는 복수의 신청 서류를 작성하기 위한 자금 반복에 고생하고 있어 리스크 분담책으로서 M&A나 합작회사의 설립에 박차를 가하고 있습니다. 규격이 진화함에 따라 재인증 사이클은 총이익을 줄이고 가격 조정을 하류로 유도합니다.

2024년 매출의 46%를 방염 격납 용기가 차지했으며, 방폭 장비 시장에서의 중심적 역할을 확인했습니다. 이 설계의 견고한 케이스와 서비스 실적은 특히 성숙한 석유 및 가스 분지에서의 고출력 펌프, 컴프레서, MCC 패널의 보급을 지원하고 있습니다. 그러나 CAGR 7.9%로 성장하는 본질 안전 방폭은 발화 에너지 임계값 이하로 동작하는 저전력 일렉트로닉스, 마이크로센서, 필드버스트폴로지를 이용하고 있습니다. 자산 관리자가 디지털 진단을 강화함에 따라, 본질 안전 방폭 설계는 봉쇄 비율을 꾸준히 감소시키지만, 새로운 센서 노드를 위험 구역으로 전송함으로써 방폭 장비 시장 전체의 규모가 확대됩니다.

가압 및 퍼지된 캐비닛은 대형 프레임 VFD 및 PLC 제품군에 여전히 필수적이며, 방폭 라이닝 및 분리 모듈은 배터리 공장의 특수 먼지 공정을 지원합니다. 에너지 제한 경로로의 전환은 시장이 '봉쇄'에서 '방지'로 축발을 옮기고 있음을 보여주며 세계적인 안전 철학을 반영하고 장기적인 확대를 지원합니다.

존1은 방폭 장비 시장의 2024년 매출의 32%를 차지했으며, 이는 일상 운전에서 증기가 발생하는 산업 프로세스가 널리 존재한다는 것을 반영합니다. 사업자는 유지 보수 사이클 동안 지속성을 보장하기 위해 인증된 조명기구, 케이블 그랜드 및 정션 박스를 선호하고 사용합니다. 그러나 CAGR 8.5%로 예측되는 존0은 지속적인 폭발성 분위기에서 최고급 하드웨어가 요구되는 그린 수소와 심해 드릴링의 설비 투자 우선순위를 모으고 있습니다. 따라서 총 수량이 감소하더라도 제품 믹스의 수익성이 재중시됩니다.

존2의 프로젝트는 특히 레거시 설정에서 마이그레이션하는 식품, 식음료 및 음료 공장에서 낮은 사양의 기어를 대량으로 생산합니다. 더스트 존21과 22는 배터리의 양극과 음극 먼지가 널리 알려진 화재 사고 후에 시각화되어 OEM에 미립자 위협에 대한 설계를 강제하고 먼지 정격 제품의 방폭 장비 시장 점유율을 에스컬레이션하기 위해 가속화됩니다.

방폭 장비 시장은 보호 방법별(폭발 격리, 폭발 방지, 기타), 존별(존0, 존20, 존1, 기타), 최종 사용자별(제약, 화학, 석유화학, 기타), 시스템별(전원 시스템, 자재관리, 기타), 지역별로 세분화되어 있습니다. 시장 규모 및 예측은 금액(달러)으로 제공됩니다.

북미는 2024년에 35%의 매출을 차지했으며, NEC 500-516조와 멕시코 걸프를 따라 석유화학 허브에서 경상적인 턴어라운드 프로그램에 활력을 얻습니다. 미국 정유 회사는 중기 개보수를 추진하고 캐나다는 겨울 SAGD 장치에 저온 인증 인클로저를 장착합니다. 높은 IIoT 도입과 LED 리노베이션이 지역의 평균 판매 가격을 상승시키고 방폭 장비 시장의 견조한 EBIT 마진을 유지합니다.

아시아태평양은 CAGR 7.6%로 성장하여 리튬 이온 기가팩토리, 육상 화학 콤비나트, 해상 LNG 트레인이 건설되어 방폭 장비 시장 규모를 확대하고 있습니다. 중국은 배터리 파크에 더스트 존을 배치하고, 인도는 제약 및 특수 화학제품에 PLI 장려금을 투입하며, 일본은 맞춤형 클래스 I 공압 장비가 필요한 수소 계곡을 개척하고 있습니다. 각 지역공급업체는 IECEx 라인을 신속하게 개발하고 리드 타임을 단축하여 지역 서비스 노드를 구축합니다.

유럽은 독일의 ATEX에 관한 전문 지식과 EU 지령 2014/34/EU에 적합하면서 플랜트의 수명을 연장하는 탄소 중립에 대한 투자에 의해 견조를 유지하고 있습니다. 영국 브렉시트 후 정책의 연속성은 ABB의 3,500만 달러의 연구개발 및 공장 업그레이드를 뒷받침하고, 지역의 능력에 대한 호의적인 감정을 보여줍니다. 중동 및 아프리카는 그린필드의 석유화학과 LNG의 메가 프로젝트에 의존하고 있으며, 남미는 브라질의 에탄올과 석유화학의 회랑에 기세가 모여 있습니다.

The explosion proof equipment market is valued at USD 9.96 billion in 2025 and is forecast to reach USD 13.51 billion by 2030, advancing at a 6.29% CAGR.

Expansion is underpinned by the universal enforcement of ATEX and IECEx rules, a quick build-out of green-hydrogen plants, and sustained capital spending on IIoT-ready retrofits that boost predictive maintenance in hazardous areas. Demand also benefits from the mass conversion to LED lighting in offshore and on-shore facilities and the ramp-up of lithium-ion gigafactories across Asia-Pacific, each requiring dust-zone-rated gear . North America preserves scale leadership through OSHA rules and ageing-asset modernization, whereas Asia-Pacific generates the fastest incremental volumes thanks to emerging hydrogen corridors, battery supply chains, and chemical processing clusters. The competitive landscape remains moderately fragmented as ABB, Siemens, and Eaton redeploy balance-sheet strength into local capacity while newcomers fill niche certification gaps. Near-term headwinds include casting shortages and tariffs on Chinese enclosures, which compress margins and encourage multi-sourcing

Regulators tightened ATEX guidelines in April 2024, intensifying conformity assessments and escalating testing volumes by 40% year-on-year. Turkey and South Korea mirrored the move through IECEx-aligned statutes, forcing suppliers to upgrade legacy lines that often run for 20 years. Multinationals welcome harmonization because one certificate now unlocks multi-region sales, compressing cycle times and lowering engineering variance. This regulatory rigor accelerates replacement demand across refineries, chemical parks, and LNG export hubs as managers rush to stay audit-ready.

Hydrogen's flammability range of 4-75% in air heightens ignition risk, mandating advanced containment, detection, and ventilation systems. Gigawatt-scale electrolyzer farms in China, Australia, and the Gulf are sourcing bespoke flame-proof switchgear and intrinsically safe sensors, creating a dedicated procurement channel inside the explosion proof equipment market. Suppliers with hydrogen-specific certificates secure early-mover margins, prompting portfolio carve-outs and R&D alliances across the value chain.

End-to-end ATEX and IECEx validation can consume 15-25% of development budgets, while lab queues stretch to 6-12 months for sophisticated assemblies. Smaller firms struggle to finance multiple dossiers, spurring M&A and joint-venture formations as a risk-sharing tactic. As standards evolve, recertification cycles shave gross margins, nudging price adjustments downstream.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flame-proof containment captured 46% of 2024 revenue, confirming its anchor role in the explosion proof equipment market. The design's rugged housings and service record underpin uptake in high-power pumps, compressors, and MCC panels, especially in mature oil & gas basins. However, intrinsic safety, growing 7.9% CAGR, exploits lower-power electronics, micro-sensors, and field-bus topologies that operate below ignition energy thresholds. As asset managers elevate digital diagnostics, intrinsic-safety designs will steadily dilute containment's percentage but enlarge the overall explosion proof equipment market size by funneling new sensor nodes into hazardous areas.

Pressurized and purged cabinets remain essential for large-frame VFDs and PLC suites, while explosion prevention linings and segregation modules serve specialty dust processes in battery plants. The shift towards energy-limiting pathways illustrates the market's pivot from 'contain' to 'prevent,' mirroring global safety philosophies and supporting long-term expansion.

Zone 1 retained 32% of 2024 revenue in the explosion proof equipment market, reflecting widespread industrial processes where vapors appear in routine operation. Operators favour certified luminaires, cable glands, and junction boxes to secure continuity during maintenance cycles. Yet Zone 0, forecast at 8.5% CAGR, garners capex priority within green hydrogen and deep-sea drilling where continuous explosive atmospheres demand the highest-grade hardware. This re-weights product-mix profitability even if total unit counts remain thinner.

Zone 2 projects generate high volumes for lower-spec gear, particularly across food, feed, and beverage plants transitioning from legacy setups. Dust Zones 21 and 22 accelerate as battery cathode and anode powders gain visibility after widely publicized fire events, compelling OEMs to design for fine particulate threats and escalating the explosion proof equipment market share for dust-rated products.

The Explosion Proof Equipment Market Segmented by Method of Protection (Explosion Segregation, Explosion Prevention, and More), by Zone (Zone 0, Zone 20, Zone 1, and More), by End-User (Pharmaceutical, Chemical and Petrochemical, and More), by System (Power Supply System, Material Handling, and More), and by Geography. The Market Size and Forecasts are Provided in Terms of Value (USD).

North America controlled 35% revenue in 2024, galvanized by NEC Articles 500-516 and recurring turnaround programs in petrochemical hubs along the Gulf Coast . United States refiners push mid-cycle revamps, while Canada outfits winterized SAGD units with low-temperature certified enclosures. High IIoT uptake plus LED retrofits elevate the regional average selling price, preserving robust EBIT margins within the explosion proof equipment market.

Asia-Pacific advances at 7.6% CAGR, building lithium-ion gigafactories, onshore chemical complexes, and offshore LNG trains that collectively swell the explosion proof equipment market size . China spearheads dust-zone deployments across battery parks, India channels PLI incentives into pharma and specialty chemicals, and Japan scales hydrogen valleys requiring bespoke Class I pneumatics. Regional suppliers fast-track IECEx lines, compressing lead times and embedding local service nodes.

Europe remains steady, anchored by Germany's ATEX expertise and the bloc's carbon-neutrality investments that extend plant life while aligning with Directive 2014/34/EU. The United Kingdom's policy continuity post-Brexit encourages ABB's USD 35 million R&D and factory upgrade, signalling positive sentiment for regional capabilities. Middle East and Africa rely on greenfield petrochemical and LNG megaprojects, whereas South America's momentum clusters around Brazil's ethanol and petrochemical corridor, together extending the global footprint of the explosion proof equipment market.