India Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1637834

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

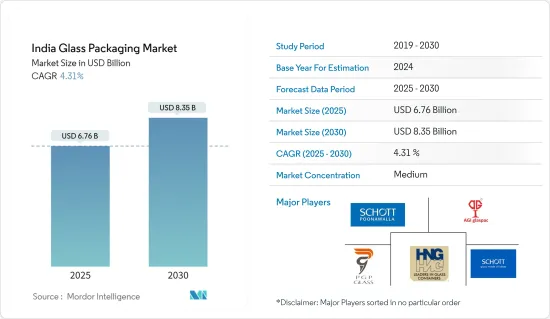

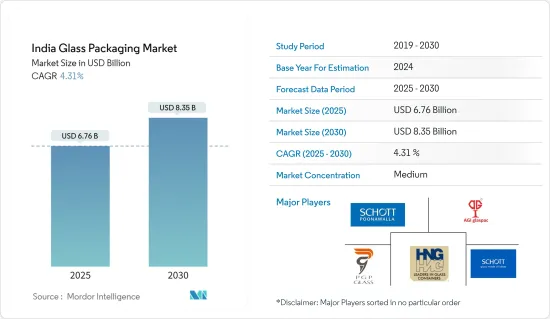

인도의 유리 포장 시장 규모는 2025년 67억 6,000만 달러, 2030년 83억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)중 CAGR은 4.31%에 달할 것으로 예측됩니다.

포장 및 관련 산업의 제조 및 생산은 포장이 GDP에 크게 기여하는 많은 국가에서만 작동합니다. 이 추세는 국내 유리 포장업자에서 제약 산업으로의 초점 전환을 보여주었습니다.

주요 하이라이트

인도는 제약 및 바이오산업의 노동력에서 세계 제2위의 점유율을 차지하고 있습니다. 2021년 인도 경제 조사에 따르면 의약품 시장은 향후 10년간 3배로 성장할 것으로 예상됩니다. 이 나라의 의약품 시장은 2021년에 410억 달러로 예측되며, 2024년에는 650억 달러에 이르고, 2030년에는 1,200-1,300억 달러 규모로 확대됩니다.

비다공성, 불침투성, 환경 친화적, 우수한 미관과 같은 유리병의 특성으로 인해 포장 산업에서의 사용이 점점 증가하고 있습니다. 인도에서는 유리 산업이 잘 확립되어 오랫동안 가내 산업으로 남아있었습니다. 이 부문은 최근 수작업 공정에서 현대 자동화 기법으로 진화하고 있습니다. Hindusthan National Glass &Industries Ltd.에 따르면 인도의 1인당 유리 포장 소비량(1.8kg)은 기타 국가에 비해 훨씬 적습니다.

유리 포장은 재사용이 가능하며 플라스틱 포장을 대체하는 친환경 대체품이기 때문에 소비자의 환경 의식이 높아지면 유리 포장 업계를 견인하고 있습니다. 또한 가처분소득 증가와 소비자 라이프스타일 변화도 시장 성장을 가속할 것으로 예상됩니다.

시장의 주요 과제 중 하나는 알루미늄 캔과 플라스틱 용기와 같은 대체 포장 형태와의 경쟁이 치열 해지고 있다는 것입니다. 알루미늄 캔과 플라스틱 용기는 부피가 큰 유리보다 무게가 가볍고 운반 및 운송 비용이 낮기 때문에 제조업체와 고객 사이에서 인기를 얻고 있습니다. 또한, 유리 포장 산업은 최근 국내에서의 위조 행위를 제한하기 때문에 추적성 향상에 주력하고 있습니다. 각 회사는 용기에 영구적인 각인을 실시해, 위조품 제조업체에 의한 유해한 행위로부터 소비자를 지키고 있습니다.

국내 COVID-19 백신에 대한 최근 투자 동향은 바이알병 성장의 중요한 추진력으로 부상하고 있습니다. 예를 들어, IBEF에 따르면 인도 제약 부문은 각종 백신의 세계 수요의 50% 이상, 미국 제네릭 시장의 약 40%, 영국의 모든 의약품의 25%를 공급하고 있습니다.

인도 유리 포장 시장 동향

큰 수요가 예상되는 유리병/용기

인도에서는 소비자가 환경 친화적이고 건강한 옵션을 강조하고 다른 옵션보다 유리 포장을 선호하기 때문에 유리 포장 솔루션, 특히 병 사용만 증가했습니다. 또한 Hindustan National Glass, Asahi India Glass 등 많은 기업들이 모든 산업 분야에서 유리 패키징 솔루션을 제공합니다.

작년 인도의 용기용 유리 제조업체인 Sunrise Glass는 240TPD의 설비 능력을 갖춘 새로운 용광로를 증설했습니다. 이 회사는 현재 두 개의 용광로를 운영하고 있으며 총 380TPD의 설비 능력을 보유하고 있습니다. 이 회사는 이 난로에는 AIS 10 트리플 고브(TG) 엠하트 머신 3대가 있는 4개의 라인이 있다고 말합니다. 모든 라인에 EVM(검사기)이 설치됩니다. 이 생산 능력이 확대됨에 따라 회사는 주류 제조업체를 중심으로 식품 병을 미국과 유럽에 수출하고 있습니다.

다국적 제약 유리 제조 업체는 인도 제약 유리 제조 업체와 함께 지난 3년동안 설계 능력을 강화하는 데 투자했습니다. 또한 세계 주요 제약 유리 제조 업체인 Gerresheimer, SGD Pharma 및 Schott는 인도 사업에 자본 투자를 실시했습니다. 다른 기업들의 이러한 노력은 최근 몇 년동안 이루어졌으며 국내 유리병 수요를 추진할 것으로 예상됩니다.

식음료, 식품 가공, 퍼스널케어, 의약품의 각 최종 사용자 산업에 대한 엄청난 투자로 인도의 병 및 용기용 유리 산업에 큰 비즈니스 기회가 생겨나고 있습니다. 수량 베이스에서는 주류가 최대의 하위 부문이며, 식음료, 의약용 유리, 화장품·향수가 이에 이어집니다.

음료 분야는 큰 수요가 예상됩니다.

유리병 및 용기는 화학적 불활성, 무균성, 비투과성을 유지할 수 있기 때문에 알코올 및 비알코올 음료 산업에서 주로 사용되고 있습니다. 유리는 음료에 함유된 화학물질과 반응하지 않기 때문에 이러한 음료의 향기, 강도, 풍미를 유지해, 우수한 포장 옵션이 되기 때문에 맥주 등의 음료가 큰 시장 점유율을 차지하고 있습니다. 이러한 이유로 맥주 수송량의 대부분은 유리병으로 수송되고 있으며, 이 동향은 조사 기간 동안에도 계속될 것으로 예상됩니다. 맥주는 자외선에 노출되면 부패하기 쉬운 내용물을 저장하기 위해 어두운 색의 유리 병으로 포장됩니다.

국내에서는 음료 최종 사용자가 시장 수요를 견인하고 있습니다. ASSOCHAM에 따르면 인도의 음료 분야에서 유리와 단단한 플라스틱은 포장의 약 3 분의 2를 차지합니다. 그러나 환경 문제에 대한 관심이 높아짐에 따라 유리 포장의 범위가 확대되고 있습니다. 음료, 특히 알코올 음료의 RTD(Ready to Drink) 분야에서 유리 포장의 사용 증가는 인도의 음료 포장 업계의 현재 동향입니다. 유리 포장 산업은 주로 국내 알코올 음료 소비 증가로 뒷받침됩니다.

또한 ICRIER(인도국제경제관계연구평의회)에 따르면 향후 10년간 인도에서 알코올 음료 소비 성장률의 70% 이상은 중저소득층과 고소득층이 견인하게 되어 제품의 프리미엄화 경향이 강해지고 있습니다.

청량 음료는 비 알코올 음료 사업을 지원하는 가장 중요한 공헌자입니다. 인도의 콜라 매출 점유율은 유리병이 35%를 차지합니다. 음료 제조업체인 Coca-Cola India Pvt. Ltd.는 재활용 유리병을 다시 추진하고 있습니다. 작년, 일부 주에서 10루피(0.15달러)의 가격대(200ml)로 전개된 병은 Coca-Cola, Thums Up, Sprite 등 동사의 히트 상품 브랜드로 판매되고 있습니다. 일부 시장에서는 유리병이 음료 매출의 30%를 차지하게 되었습니다(출처: 코카콜라).

많은 음료들이 유리병을 사용할 것으로 예상되며, 특히 선도적인 제조업체들은 유리병으로 꾸며져 있습니다. 사용자의 주요 이점은 주스 및 기타 음료 포장 용기로 유리 병을 사용하는 경우 용기 재료에서 거의 용출되지 않는다는 것입니다.

인도의 유리 포장 산업 개요

인도의 유리 포장 시장은 여러 기업의 경쟁으로 시장이 적당하게 통합되었습니다. Schott Kaisha Pvt Ltd., AGI glaspac., Piramal Glass Limited, Borosil Glass Works Limited, Haldyn Glass Limited 등 시장 기업들은 시장 점유율을 더욱 확대하기 위해 제품 혁신, 파트너십, M&A 등의 전략을 채택하고 있습니다. 시장에서 중요한 진전은 다음과 같습니다.

2022년 8월 - 소다 재 제조업체 Nirma는 가장 유명한 Hindustan National Glass Limited(HNGL)를 인수하는 165억 루피(2억 600만 달러) 계획을 제출했습니다. 아프리카에 본사를 둔 병 제조업체인 Madhvani Group과 용기 유리 제조업체인 AGI Greenpac도 각각 다른 결의 계획을 제출했습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

애널리스트에 의한 3개월간의 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

업계 밸류체인 분석

COVID-19의 업계에 대한 영향 평가

무역 시나리오 분석

제5장 시장 역학

시장 성장 촉진요인

국민의 환경 의식 고조

국내에서의 음료 소비 증가

시장 성장 억제요인

알루미늄이나 플라스틱 등의 대체 포장 옵션

제6장 시장 세분화

제품별

병/용기

바이알

앰풀

주사기/카트리지

최종 사용자 업계별

식품

음료(청량음료, 우유, 알코올 음료, 기타 음료 유형)

화장품, 향수, 퍼스널케어

의약품

제7장 경쟁 구도

기업 프로파일

Schott Kaisha Pvt Ltd(SCHOTT AG)

AGI Glaspac(HSIL Ltd)

Piramal Glass Limited

Hindustan National Glass & Industries Limited(HNGIL)

Schott Poonawalla Private Limited

Gerresheimer AG

Borosil Glass Works Limited(Klasspack Pvt. Ltd.)

Haldyn Glass Limited(HGL)

Sunrise Glass Industries Private Limited

Ajanta Bottle Pvt Ltd

GM Overseas

Empire Industries Limited-Vitrum Glass

제8장 투자 분석

제9장 시장 전망

JHS

영문 목차

영문목차

The India Glass Packaging Market size is estimated at USD 6.76 billion in 2025, and is expected to reach USD 8.35 billion by 2030, at a CAGR of 4.31% during the forecast period (2025-2030).

The manufacturing and production of packaging and relatable industries are only functional in many countries where packaging contributes significantly to GDP. The trend witnessed a shift of focus from glass packagers in the country to the pharmaceutical industry.

Key Highlights

India contributes the second-largest share of the pharmaceutical and biotech workforce worldwide. According to the Indian Economic Survey of 2021, the pharmaceutical market is expected to grow three times in the next decade. The country's pharmaceutical market was projected at USD 41 billion in 2021 and will reach USD 65 billion by 2024 and further expand to around USD 120-130 billion by 2030.

Glass bottle characteristics, such as being non-porous, impermeable, eco-friendly, and aesthetically pleasing, lead to ever-increasing use in the packaging industry. In India, the glass industry is well established and has remained a cottage industry for a long time. The sector is recently evolving from hand-working processes to modern automation methods. According to the Hindusthan National Glass & Industries Ltd, Indian per capita consumption of glass packaging (1.8 kg) is much lower than other nations.

The glass packaging industry is also driven by the growing environmental awareness among consumers, with glass packaging being reusable and an environmentally friendly alternative to plastic packaging. The increasing disposable incomes and changing consumers' lifestyles are also expected to drive the market's growth.

One of the main challenges for the market is the increased competition from alternative forms of packaging, such as aluminum cans and plastic containers. The items are lighter in weight than the bulky glass, gaining popularity among manufacturers and customers because of the lower cost involved in their carriage and transportation. Moreover, the glass packaging industry is recently concentrating on increasing traceability to restrict counterfeit activities in the country. The companies are mentioned using permanent engravings on containers, protecting consumers from harmful practices by spurious product manufacturers.

The recent investing trend in vaccines for COVID-19 in the country is emerging as a significant driver for the vials growth. For instance, according to IBEF, the Indian pharmaceutical sector supplies more than 50% of the global demand for various vaccines, around 40% of the generic market for the United States, and 25% of all medicines for the United Kingdom.

India Glass Packaging Market Trends

Glass Bottles/Containers Expected to Witness Significant Demand

In India, only the usage of glass packaging solutions, especially bottles, is increasing as consumers emphasize eco-friendly and healthy options and prefer glass packaging over other options. Also, the country comprises many companies, including Hindustan National Glass and Asahi India Glass, offering glass packaging solutions across industries.

Last year, India's container glass producer Sunrise Glass added a new furnace with an installed capacity of 240 TPD. The company currently operates two furnaces with a combined installed of 380 TPD. The company stated that the stove would have four lines with three AIS 10 triple gob (TG) Emhart Machines. All the lines will have EVM (Inspection Machines). With this capacity expansion, the company focuses on catering to significant liquor clients and exports to the USA and Europe for food-grade jars.

Multinational pharmaceutical glass producers, along with Indian pharmaceutical glass producers, have invested in increasing designed capacity over the last three years. In addition, leading global pharmaceutical glass producers Gerresheimer, SGD Pharma, and Schott have invested capital in Indian operations. Such initiatives by other players are estimated to take place in recent years and will fuel the demand for glass bottles in the country.

Considerable investments in the beverages, food processing, personal care, and pharmaceutical end-user industries have created enormous opportunities for the country's bottles/container glass industry. Alcoholic beverages are the largest sub-segment for bottles/container glass consumption on a volume basis, followed by food, pharmaceutical glass, and cosmetics & perfumery.

Beverage Sector Expected to Witness Significant Demand

Glass bottles and containers are majorly used in the alcoholic and non-alcoholic beverage industries due to their ability to maintain chemical inertness, sterility, and non-permeability. Drinks such as beer account for a significant market share, as glass does not react with the chemicals present in drinks and, therefore, preserves the aroma, strength, and flavor of these beverages, making them a good packaging option. Due to this reason, most beer volume is transported in glass bottles, and this trend is expected to continue over the study period. Beer is packaged in dark-colored glass bottles to preserve the contents, which are prone to spoilage when exposed to UV light.

The beverage end-user vertical is driving the market demand in the country. According to ASSOCHAM, glass and rigid plastics constitute about two-thirds of packaging in India's beverage sector. However, the industry's glass packaging scope is expanding due to growing environmental concerns. Increasing glass packaging usage for Beverages, especially for the alcoholic Ready to Drink (RTD) segment, is a current trend in the Beverage packaging industry of India. The glass packaging industry is primarily boosted by increasing alcoholic beverage consumption in the country.

Moreover, ICRIER (Indian Council for Research on International Economic Relations) said over 70% of the growth in alcoholic beverage consumption in India in the next decade would be driven by the lower middle and upper middle-income groups, and there is a growing trend toward product premiumization.

Soft drinks are the most significant contributor on which the business of non-alcoholic drinks rests. Glass bottles retain a 35% share of sales for Coke in India. Beverage maker Coca-Cola India Pvt. Ltd. is again promoting returnable glass bottles. The bottles rolled out last year at INR 10 (USD 0.15) price point (200 ml) in select states are available across the company's top-selling brands, such as Coca-Cola, Thums Up, and Sprite. In some markets, glass bottles now make up 30% of beverage sales (source: Coca-Cola).

Many beverages are expected to use glass bottles, particularly those from large manufacturers that have been decorated with glass bottles. The main advantage for the user is that there is almost no dissolution from container materials when glass bottles are used as packaging containers for juice or other drinks.

India Glass Packaging Industry Overview

The India Glass Packaging Market is competitive owing to multiple players, which led the market to be moderately consolidated. Players in the market, such as Schott Kaisha Pvt Ltd., AGI glaspac., Piramal Glass Limited, Borosil Glass Works Limited, and Haldyn Glass Limited are adopting strategies like product innovation, partnerships, and mergers and acquisitions to increase their market share further. Some of the critical advancements in the market are:

August 2022 - Soda ash producer Nirma submitted an INR 16,500 million (USD 206 million) plan to acquire one of the most prominent Hindustan National Glass Limited (HNGL). Africa-based bottle maker Madhvani Group and container glass producer AGI Greenpac have also submitted separate resolution plans for the company.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Assessment of Impact of COVID-19 on the Industry

4.5 Trade Scenario Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Environmental Awareness Among the Population

5.1.2 Increasing Beverage Consumption in the Country

5.2 Market Restraints

5.2.1 Alternative Packaging Options such as Aluminum and Plastic

6 MARKET SEGMENTATION

6.1 By Product ( Revenue in USD Billion and Volume in Million Metric Tones)

6.1.1 Bottles/Containers

6.1.2 Vials

6.1.3 Ampoules

6.1.4 Syringe/Cartridges

6.2 By End-user Vertical ( Revenue in USD Billion and Volume in Million Metric Tones)

6.2.1 Food

6.2.2 Beverage (Soft Drinks, Milk, Alcoholic Beverages, Other Beverage Types)

6.2.3 Cosmetics, Perfumery and Personal Care

6.2.4 Pharmaceuticals

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Schott Kaisha Pvt Ltd (SCHOTT AG)

7.1.2 AGI Glaspac (HSIL Ltd)

7.1.3 Piramal Glass Limited

7.1.4 Hindustan National Glass & Industries Limited (HNGIL)

7.1.5 Schott Poonawalla Private Limited

7.1.6 Gerresheimer AG

7.1.7 Borosil Glass Works Limited (Klasspack Pvt. Ltd.)