ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

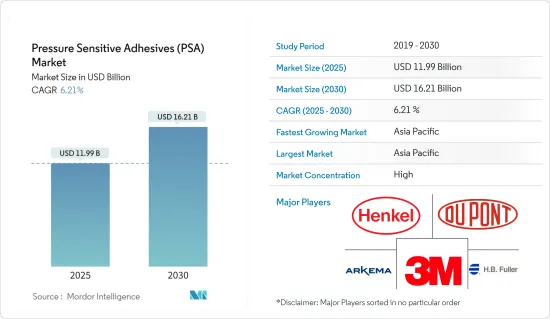

감압 접착제(PSA) 시장 규모는 2025년 119억 9,000만 달러, 2030년 162억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)중 CAGR은 6.21%에 달할 것으로 예측됩니다.

COVID-19의 발생으로 2020년에는 세계 봉쇄, 제조 활동 및 공급망의 혼란, 생산 정지가 발생하여 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 상황이 회복되기 시작하여 시장의 성장 궤도가 회복되었습니다.

주요 하이라이트

시장을 견인하는 주요 요인은 저렴한 비용으로 유연한 패키징 개발이 진행되고 있으며 경화 시간이 짧은 감압 접착제(PSA)의 사용이 증가하고 있다는 것입니다.

반면 VOC 배출에 대한 엄격한 환경 규제와 UV 경화형 접착제와 같은 대체품의 사용 증가가 시장 성장을 방해할 것으로 예상됩니다.

테이프 분야는 시장을 독점하고 있으며 예측 기간 동안에도 성장이 예상됩니다. 이는 포장, 의료, 운송과 같은 최종 사용자 산업이 성장하고 있기 때문입니다.

바이오의 감압 접착제(PSA)의 채용과 나노기술을 기반으로 한 기능성 감압 접착제(PSA)의 개발은 향후의 기회가 될 것 같습니다.

아시아태평양은 세계 시장을 독점하고 중국과 인도 등 국가에 의한 소비가 가장 많습니다.

감압 접착제(PSA) 시장 동향

포장 산업이 시장을 독점

접착제는 제품 패키지가 소비자에게 도달할 때까지 온전함을 보장합니다. 패키징 작업은 여러 신제품과 제품이 급증함에 따라 점점 복잡해지는 패키징 수요를 해결하기 위해 신뢰할 수 있는 접착제가 필요합니다.

감압 접착제(PSA)는 특히 포장 산업에 몇 가지 장점을 제공합니다 :

신속한 재작업: 재가공 및 재포장은 비용을 증가시킵니다. PSA는 제품이 표준을 준수하고 선반에 정렬되도록 적시에 방법을 제공합니다. 감압 접착제(PSA)는 스틱 풀보다 안전하며 기존 테이프보다 눈에 띄지 않습니다. 스틱 접착제와 달리 감압 접착제(PSA)는 적용 시 열을 필요로 하지 않습니다. 열이 없기 때문에 화상의 걱정이 없으며 공장에서 일하는 사람들의 안전성이 향상됩니다. 게다가 PSA는 패키징 그래픽의 방해가 되지 않고 브랜드 이미지를 손상시키지 않고 필요한 접착력을 제공합니다. 감압 접착제(PSA)는 브랜드의 영향을 유지하고 최대화하는 눈에 띄지 않는 패키징 솔루션입니다.

즉시 접착: 감압 접착제(PSA)를 적용하면 경화될 때까지 기다릴 필요가 없으므로 시간을 절약할 수 있습니다. 감압 접착제(PSA)를 적용하면 접착과 동시에 기판이 압축됩니다. 순간적으로 접착할 수 있기 때문에 처리 속도가 향상되고 생산성도 향상됩니다.

브랜드 이미지 유지 : 브랜드 이미지는 패키지의 모양에 크게 의존합니다. PSA는 패키징에 손상을 주거나 잔류물을 남기지 않고 깨끗하게 벗겨내는 접착제를 제공합니다. 브랜드 이미지의 유지는 소비자에게 호소로 이어집니다.

게다가 지난 몇 년동안 패키징 업계는 제조업과 산업 부문이 유연한 패키징에 적응하는 전환기를 맞이했습니다.

가벼워 취급하기 쉽고, 장소를 차지하지 않고, 보존 기간이 길고, 수송이 용이하고, 파손되기 어렵고, 인쇄 적성이 뛰어난 등의 이점이 있기 때문에 패키징이 보급되었습니다.

전자상거래, 전자소매, 식품의 온라인 주문 및 택배 서비스 증가 추세에 따라 포장재료, 특히 연포장 수요가 증가하고 있으며, 예측 기간 동안 UV 경화형 접착제 수요를 견인할 가능성이 높습니다. 독일에서는 2022년 종이 포장 산업이 이전에 비해 크게 성장했습니다.

인도 포장 산업 협회(PIAI)에 따르면 인도 포장 산업은 예측 기간 동안 22%의 성장이 예상됩니다. 또한 인도의 포장 시장은 2025년까지 2,048억 1,000만 달러에 이를 것으로 예상됩니다.

연포장은 저소득 남미, 아프리카, 아시아태평양 국가의 식품 포장 용도로 사용됩니다. 신흥국에서는 연포장의 인기와 수요가 높아지고 있으며, 지속적인 경기 확대와 식음료 산업의 가속이 수요를 지지하고 있습니다.

독일에서는 2022년 종이 포장 산업이 크게 성장했으며, 이는 다양한 최종 사용자 산업을 위한 비화석 기반 포장에 대한 수요가 증가하고 있기 때문입니다.

이러한 요인으로 인해 예측 기간 동안 감압 접착제(PSA) 시장 수요가 증가할 것으로 보입니다.

아시아태평양이 시장을 독점할 전망

세계 수요의 40% 이상을 차지하는 아시아태평양은 감압 접착제(PSA)에 있어서 가장 유망한 시장이며, 조만간 지배하게 될 것으로 보입니다. 이 지배는 이 지역의 테이프 및 라벨 수요 증가로 인한 것입니다.

중국, 인도, 일본, 한국은 감압 접착제(PSA) 수요의 80% 이상을 차지합니다.

중국은 접착제 제품(테이프, 라벨 등)의 주요 수출국 중 하나입니다. 많은 고객에게 중요한 것은 제품 품질, 공급업체가 제공하는 제품군, 접착제 사용량 및 낭비를 줄이는 것입니다. 따라서 현재 감압 접착제(PSA)의 중국 시장은 국제 기업이 지배하고 있습니다. 같은 요인은 국내 주요 시장 점유율을 얻기 위해 R & D에 투자하는 현지 제조업체를 뒷받침하고 있습니다.

중국은 1인당 소득 증가와 전자상거래 대기업의 대두로 세계 최대의 패키징 소비국이 되고 있습니다. 인도 플라스틱 산업 협회에 따르면 인도의 포장 산업은 세계 5위로 연간 약 22-25%의 성장률을 보이고 있습니다. 고도로 숙련된 노동력과 저렴한 인건비로 포장·가공 식품의 비용은 유럽보다 40% 낮게 억제할 수 있습니다. 인구 증가와 포장 수요 증가가 시장을 견인할 것으로 예상됩니다.

게다가 중국의 포장산업은 경제 확대와 구매력이 높은 중간층의 상승으로 최근 몇 년간 지속적으로 급성장하고 있습니다. 식품 포장은 포장 업계의 주요 기업이며 중국 시장 점유율의 약 60%를 차지합니다. Interpak에 따르면 중국의 식품 포장 카테고리에서 포장 총량은 2023년에 4,470억 개에 이를 것으로 예상되며, 포장 업계의 감압 접착제(PSA)에 대한 수요 증가가 나타났습니다.

인도의 감압 접착제(PSA) 시장은 높은 성장률이 예상됩니다. 그 용도는 투명 라벨과 필름 라벨, FMCG(Fast-Moving Consumer Goods) 제조업체용 수축 랩 라벨, 플렉서블 라벨, 멀티 컬러 랩 어라운드 라벨로 증가했습니다. 감압 접착제(PSA) 시장은 여전히 초기 성장 단계에 있으며 미래의 성장 전망은 더 높습니다.

아시아태평양의 큰 성장과 함께 큰 시장 규모는 감압 접착제(PSA) 시장의 확대에 기여하고 있습니다.

감압 접착제(PSA) 산업 개요

감압 접착제(PSA) 시장은 통합되어 있습니다. 주요 기업 7개사에서 60% 가까이를 차지하고 있습니다. 주요 기업(순부동)은 3M, Arkema, DuPont, HB Fuller, Henkel AG&Co.KGaA입니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

저비용 연포장 개발 증가

경화 시간이 짧은 PSA의 사용 증가

기타 촉진요인

억제요인

VOC 배출에 관한 엄격한 환경 규제

UV 경화형 접착제와 같은 대체품의 사용 증가

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

기술별

수성

용제계

핫멜트

방사선

수지별

아크릴

실리콘

엘라스토머

기타 수지

용도별

테이프

라벨

그래픽

기타 용도

최종 사용자 산업별

포장

목공 및 건구

의료

상업 그래픽

운수

일렉트로닉스

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Arkema Group(Bostik SA)

Ashland Inc.

Avery Dennison Corp.

DuPont

Franklin International

HB Fuller Co.

Helmitin Adhesives

Henkel AG & Co. KGaA

Huntsman Corporation

Illinois Tool Works Inc.

Jowat AG

Mapei SPA

Master Bond

Pidilite Industries Ltd

Sika AG

Tesa SE(A Beiersdorf Company)

Wacker Chemie AG

제7장 시장 기회와 앞으로의 동향

바이오 베이스의 감압 접착제(PSA)의 채용

나노기술에 근거한 기능성 감압 접착제(PSA)의 개발

JHS

영문 목차

영문목차

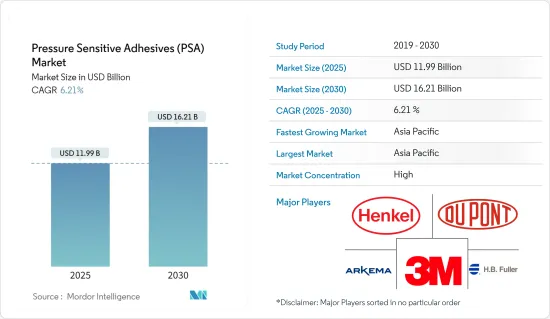

The Pressure Sensitive Adhesives Market size is estimated at USD 11.99 billion in 2025, and is expected to reach USD 16.21 billion by 2030, at a CAGR of 6.21% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

The major factor driving the market studied is the increasing development of low-cost, flexible packaging and increasing usage of pressure-sensitive adhesives because of lesser curing time.

On the flip side, stringent environmental regulations regarding VOC emissions and increasing usage of substitutes like UV-cured adhesives are expected to hinder the studied market's growth.

The tapes segment dominated the market and is expected to grow during the forecast period. It is owing to the growing end-user industries, such as packaging, medical, and transportation.

Adopting bio-based pressure-sensitive adhesives and developing nanotechnology-based functional pressure-sensitive adhesives is likely an opportunity in the future.

Asia-Pacific dominated the global market, with the largest consumption from countries such as China and India.

Pressure Sensitive Adhesives Market Trends

Packaging Industry to Dominate the Market

Adhesives ensure the product packaging remains intact until it reaches the consumer. Packaging operations require a reliable adhesive to meet the increasingly complex packaging demands as there is an increase in several new products and product proliferation.

Pressure-sensitive adhesives (PSAs) specifically offer several advantages for the packaging industry:

Quick reworks: Reworking or repackaging increases costs. PSAs offer a timely way to make products compliant and shelf-ready. Pressure-sensitive adhesives are safer than glue sticks and more discrete than traditional tape. Unlike glue sticks, pressure-sensitive adhesives do not require heat during application. The absence of heat eliminates burns and increases safety among plant workers. Additionally, PSAs are less intrusive on packaging graphics, providing the required adhesion without sacrificing the brand image. Pressure-sensitive adhesives are less visible packaging solutions that preserve and maximize the brand's impact.

Instant bond: Applying pressure-sensitive adhesives is time-saving, as waiting until they cure is unnecessary. When applied, they compress the substrate right when adhesion occurs. Instant bonding increases the processing speed, as well as improves production.

Maintaining brand image: Brand image relies heavily on the packaging appearance. PSAs provide a bond that removes cleanly without damaging the packaging or leaving behind residue. Preserving brand image adds to your consumer appeal.

Furthermore, in the last few years, the packaging industry is experiencing a transition where the manufacturing and industrial sector is adapting to flexible packaging.

The benefits, such as being lightweight, easy to handle, less space-consuming, longer shelf life, easy transit, damage resistance, and better printability, made packaging popular.

With the growing trend of e-commerce, e-retail, and online food orders and delivery services, the demand for packaging materials, especially flexible packaging, is increasing, likely to drive the demand for UV-curable adhesives during the forecast period. In Germany, the paper packaging industry grew significantly in 2022 compared to previous years.

According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025.

Flexible packaging is used in food packaging applications in low-income South America, Africa, and Asia-Pacific countries. The popularity and demand for flexible packaging are rising in emerging economies, and the demand is supported by continued economic expansion and an acceleration in the food and beverage industry.

The paper packaging industry grew significantly in Germany in 2022 because of the increasing demand for non-fossil-based packaging for different end-user industries.

Such factors will likely increase the demand for the pressure-sensitive adhesives market over the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

With over 40% of the global demand, Asia-Pacific is the most promising market for pressure-sensitive adhesives, which will likely dominate soon. This domination can be attributed to the region's growing demand for tapes and labels.

China, India, Japan, and South Korea account for over 80% of the demand for pressure-sensitive adhesives.

China is one of the major exporters of adhesive products (tapes, labels, etc.). The factors concerning most of its customers are the product quality, the product range offered by the vendor, and reducing the dosage and wastage of adhesives. Therefore, international players currently dominate the Chinese market for pressure-sensitive adhesives. The same factor encourages local producers to invest in R&D to acquire a major national market share.

China is the world's largest packaging consumer globally, owing to growing per capita income and rising e-commerce giants. India's packaging industry is the fifth-largest globally, growing at about 22-25% per year, according to the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

Furthermore, the Chinese packaging industry grew rapidly and consistently in recent years, owing to the expanding economy and rising middle class with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for roughly 60% of the total market share in China. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023, indicating an increased demand for pressure-sensitive adhesives from the packaging industry.

The pressure-sensitive adhesives market in India is expected to grow at a higher rate. Its usage increased with transparent and film labels, shrink-wrap labels for fast-moving consumer goods (FMCG) manufacturers, flexible labels, and multicolor wrap-around labels. The pressure-sensitive adhesives market is still in its early growth stage, with a higher scope of growth in the future.

The large market size, coupled with the huge growth of Asia-Pacific, is instrumental in expanding the pressure-sensitive adhesives market.

Pressure Sensitive Adhesives Industry Overview

The pressure-sensitive adhesives market is consolidated. The top seven players account for almost 60%. The major companies (not in any particular order) include 3M, Arkema, DuPont, HB Fuller, and Henkel AG & Co. KGaA.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Development of Low-cost Flexible Packaging

4.1.2 Increasing Usage of PSA Because of Lesser Curing Time