데이터센터 서비스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Data Center Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1637779

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

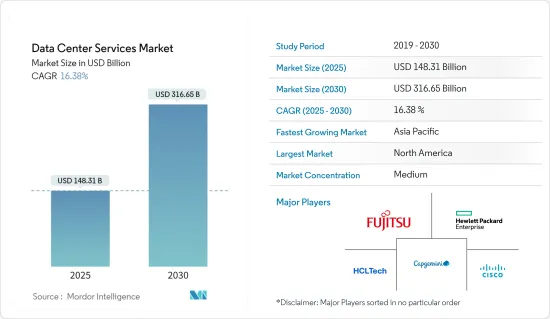

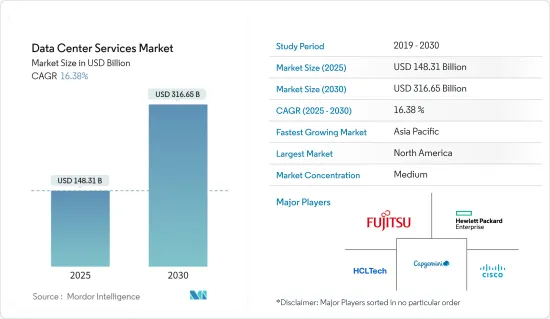

데이터센터 서비스 시장 규모는 2025년 1,483억 1,000만 달러, 2030년 3,166억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 16.38%에 달할 것으로 예측됩니다.

데이터센터 서비스 수요 급증의 주요 요인은 클라우드 컴퓨팅의 보급입니다. 기업 및 기업은 클라우드 서비스에 스토리지, 컴퓨팅 및 용도 요구 사항을 요구하고 있으며 데이터 급증으로 데이터센터의 용량을 확장해야 합니다.

다양한 산업 분야에서 디지털 전환 이니셔티브에 대한 수요가 증가함에 따라 강력한 데이터센터 인프라가 필요합니다. 기업은 점점 디지털 기술을 활용하여 업무 효율성을 높이고 고객 경험을 향상시키고 혁신을 촉진하고 있습니다. 조직은 의사 결정을 위해 엄청난 데이터 세트를 수집하고 분석하는 빅데이터와 애널리틱스에 대한 의존도를 높이고 있습니다. 이러한 추세는 견고한 데이터 스토리지와 데이터 처리 인프라에 대한 필요성을 높이고 있습니다.

2024년 1월, 클라우드 및 커리어 중립 데이터센터 서비스의 세계 공급자인 Digital Realty는 인도에서 최초의 데이터센터를 공개했습니다. 첸나이의 산업 허브에 위치한 10에이커 캠퍼스는 최대 100메가와트의 중요한 IT 부하를 지원하는 능력을 자랑합니다. 이는 회사의 세계, 데이터센터 플랫폼에 있어서 매우 중요한 확장이며, 중요한 세계 시장에서의 디지털 전환 수요 증가에 대응하는 것입니다.

또한, 사물 인터넷(IoT) 증가로 인해 저장, 처리 및 분석이 필요한 엄청난 양의 데이터를 생성하는 연결된 장치가 무수히 존재하고 새로운 수요가 발생하고 있습니다. 인공지능과 머신러닝의 고도화가 진행됨에 따라 방대한 컴퓨팅 능력과 스토리지가 필요해 데이터센터 서비스에 대한 수요를 추진하고 있습니다.

COVID-19 팬데믹으로 촉발된 원격 근무과 디지털 서비스의 급증은 데이터센터의 중요성을 돋보이게 했습니다. 이제 데이터센터는 정보와 용도에 안전하고 안정적으로 액세스하는 데 중요한 허브 역할을 합니다. 또한 엄격한 데이터 보호 규정이 컴플라이언스 기준을 충족하기 위해 데이터센터 서비스에 대한 투자를 강화하도록 기업을 촉구하고 있습니다. 에너지 효율적인 설계 및 냉각 솔루션 강화 등 기술 발전은 데이터센터의 매력과 비용 효율성을 높이고 시장 성장을 가속하고 있습니다.

2024년 4월, American Tower Corporation의 자회사에서 하이브리드 IT 솔루션 제공업체인 CoreSite는 NVIDIA DGX-Ready 데이터센터 프로그램 인증을 받았음을 밝혔습니다. 이 인증을 통해 핵심 사이트는 인공지능(AI), 머신러닝(ML) 및 기타 고밀도 용도에 대한 수요 증가를 활용하려는 조직에 특화된 확장 가능하고 고성능 인프라를 제공할 수 있습니다. CoreSite에서 NVIDIA DGX 인프라를 호스팅하기로 선택한 고객은 로스앤젤레스, 실리콘 밸리, 시카고, 버지니아 북부 등 주요 위치에 있는 NVIDIA AI와 고성능 컴퓨팅을 위해 조정된 고밀도 데이터센터 캠퍼스 네트워크에 액세스할 수 있습니다.

그러나 높은 운영 비용, 에너지 소비 우려, 숙련된 전문가의 제한된 가용성으로 인해 시장 성장이 제한됩니다. 또한 데이터 보안 및 개인 정보 보호 문제, 규제 준수 요구 사항은 시장 확장의 큰 장벽이 되었습니다.

데이터센터 서비스 시장 동향

클라우드 및 호스팅이 데이터센터 서비스 시장에서 큰 점유율을 차지할 전망

클라우드 및 호스팅 서비스에 대한 수요가 증가함에 따라 데이터센터 서비스 시장을 뒷받침하고 있습니다. 이 급성장의 배경에는 확장성이 높은 인프라가 필요합니다. 유연성, 확장성, 비용 효율성이 높고 클라우드로의 전환이 진행됨에 따라 이러한 서비스를 지원하는 신뢰할 수 있는 데이터센터 시설에 대한 수요가 급증하고 있습니다.

수요 증가는 데이터센터 건설 및 확장에 대한 투자를 뒷받침합니다. 이러한 급증은 기술 발전에 박차를 가하고 있을 뿐만 아니라 고성능 컴퓨팅, 스토리지, 네트워킹 솔루션에 대한 필요성도 증가하고 있습니다. 또한 클라우드 기반 서비스로의 전환은 데이터센터 분야의 혁신과 경쟁을 촉진하고 있습니다. 이러한 경쟁이 치열해지면 더욱 견고한 서비스 포트폴리오와 운영 효율성이 향상됩니다.

Cloudscene에 따르면 2024년 3월 현재 미국은 세계에서 가장 많은 데이터센터 수를 자랑하며, 그 수는 5,381로 보고되었습니다. 이어 독일이 521, 영국이 514와 약간 차이가 납니다.

현재 인터넷에 연결된 기기는 수십억대가 가동되고 있으며, 그 수는 증가하고 있습니다. 이러한 장치는 종종 많은 양의 데이터를 생성하며 기록, 처리, 저장, 평가 및 검색이 필요합니다. IoT와 Industry 4.0의 진전에 따라 제조업은 생산성 향상, 비용 절감, 보안 강화, 운영 간소화를 위해 빅데이터와 애널리틱스를 점점 활용하고 있습니다.

데이터 생성이 가속화됨에 따라 적시에 통찰력을 얻는 것이 점점 더 어려워지고 있습니다. 스마트 시티와 지능형 빌딩과 같은 새로운 디지털 분야는 즉시 액세스할 수 있는 풍부한 데이터를 제공합니다. 게다가 퍼블릭 클라우드는 비용 효율적이고 유지보수의 필요성이 적기 때문에 인기가 급상승하고 있습니다. 또한 클라우드 서비스에 쉽게 액세스할 수 있어 중소기업도 인프라 비용을 요구사항에 맞게 조정할 수 있어 효율적으로 규모를 확대할 수 있게 되었습니다.

2024년 5월, 비트코인 마이닝과 집중 컴퓨팅을 위한 그린 데이터센터를 전문으로 하는 기업인 Soluna Holdings Inc.가 새로운 파트너십을 발표했습니다. 전 세계 기업용 GPU 서버 OEM 및 AI Infrastructure-as-a-Service 제공업체와의 제휴 계획을 발표했습니다. Soluna Cloud는 전략적 파트너의 재생 가능 에너지로 실행되는 고성능 데이터센터를 활용하여 서비스를 시작할 예정입니다. 게다가 이번 제휴에 의해 Soluna Cloud의 서비스는 기본적인 인프라로부터, 전략 파트너의 AI 파이프라인 소프트웨어 솔루션 세트에까지 확대할 전망입니다.

북미가 시장에서 큰 점유율을 차지

북미에는 기술 혁신자가 많아 클라우드 컴퓨팅이나 IoT 등 첨단기술 수요를 견인하고 있습니다. 이러한 기술의 복잡한 특성을 고려하면 탄력적인 데이터센터 시설에 대한 요구가 커지고 있습니다. 그 결과, 이 지역에서는 데이터센터 서비스 수요가 급증할 전망입니다.

세계 경제의 중심인 미국은 퍼블릭 클라우드 기반 데이터센터의 확대를 견인하는 입장에 있습니다. 이 나라에서는 IT 산업이 주요 민간 고용주가 되고 있으며, 데이터센터의 보급이 시장 성장을 더욱 뒷받침하고 있습니다. 또한, 하이퍼스케일 플랫폼이 급증함에 따라, 이 나라에서는 하이퍼스케일 플랫폼의 데이터센터 요구에 대응하고 있습니다.

이 지역의 기업은 자체 데이터센터를 건설하는 것보다 코로케이션 데이터센터를 선호합니다. 이 시프트는 코로케이션 시설의 임대가 초래하는 수많은 이점을 실감하는 것이 배경에 있습니다. 인프라 장비는 네트워크 및 연결 장비와 같은 기술의 급속한 통합으로 점점 복잡해지고 있습니다.

시장에서 기존 기업와 신흥 기업 모두 경쟁 기업 간의 격렬한 적대 관계를 볼 수 있습니다. 이러한 시장 진출 기업은 경쟁력을 강화하고 시장 성장을 가속하기 위해 유기적 전략과 무기적 전략을 결합하여 전개하고 있습니다. 예를 들어, 2024년 6월, Oracle과 Google Cloud는 전략적 파트너십을 발표하여 Oracle 클라우드 인프라(OCI)와 Google Cloud 기술을 통합하는 유연성을 고객에게 제공했습니다. 이 제휴는 사용자의 용도 마이그레이션 및 업그레이드를 가속화하기 위한 것입니다. Oracle Interconnect for Google Cloud는 처음에는 전 세계 11개 지역에서 사용할 수 있을 것으로 예상되며, 고객은 클라우드 간 데이터 전송 요금을 부담하지 않고 범용 워크로드를 원활하게 배포할 수 있습니다.

2023년 10월, 안전하고 확장 가능한 데이터센터 솔루션 제공업체인 Flexential은 대규모 GPU 가속 워크로드에 특화된 클라우드 제공업체인 CoreWeave가 데이터센터의 존재를 확대할 것이라고 발표했습니다. CoreWeave의 확장은 오리건 주 힐즈버러와 조지아 주 더글라스빌에 전략적으로 위치한 두 개의 코로케이션 시설로 이전하는 것을 의미합니다. 이 모든 시설은 Flexential의 소유 및 운영하에 있습니다. CoreWeave의 인프라는 머신러닝, AI, VFX, 렌더링, 픽셀 스트리밍에 이르는 프로젝트의 진화하는 요구에 부응하도록 조정되었으며, 고급 컴퓨팅 프레임워크를 선보입니다.

데이터센터 서비스 산업 개요

데이터센터 서비스 시장은 매우 세분화되어 경쟁사 간 적대관계도 치열합니다. 주요 시장 기업은 Fujitsu Ltd, Cisco Systems Inc., Capgemini, HCL Technologies Limited, Hewlett Packard Enterprise Company입니다. 시장 진출 기업은 전략적 파트너십과 제품 혁신을 통해 포트폴리오를 강화하고 지속적인 경쟁력을 추구하고 있습니다.

2024년 5월 북미에서 네트워크 중립 상호 연결과 하이퍼스케일 에지 데이터센터를 제공하는 Cologix는 이 지역에서 네 번째로 가장 큰 데이터센터를 시작하는 데 성공했다고 발표했습니다. 이 확장은 오하이오 주 콜럼버스의 코로케이션 및 상호 연결 서비스에 대한 요구 증가에 대응하기 위해 Cologix의 중요한 단계를 의미합니다.

2024년 2월 세계 인프라 Platform-as-a-Service 기업인 MOD Mission Critical(MOD)은 네트워크 중심의 코로케이션, 클라우드, 관리 서비스를 제공하는 365 Data Centers(365)와의 제휴 확대를 발표했습니다. 이 제휴를 통해 MOD는 분수 코로케이션 및 연결 솔루션을 제공할 수 있으며, 고객은 20개 시장에서 365개의 네트워크 중심 데이터센터에서 제공하는 서비스 및 리소스에 액세스할 수 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

산업 밸류체인 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

시장에 대한 COVID-19의 영향

시장 성장 촉진요인

데이터센터 기술에 대한 지출 증가

확장성에 따른 데이터센터의 복잡화

시장 성장 억제요인

데이터 프라이버시에 대한 우려

제5장 시장 세분화

서비스 유형별

매니지드 호스팅 서비스

코로케이션 서비스

데이터센터 유형별

티어 I 및 티어 II

티어 III

티어 IV

최종 사용자 산업별

BFSI

헬스케어

소매

제조업

IT 및 통신

기타 최종 사용자 산업

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

제6장 경쟁 구도

기업 프로파일

Fujitsu Limited

IBM Corporation

Singapore Telecommunications Limited(Singtel)

Digital Realty Trust Inc.

Cisco Systems Inc.

Equinix Inc.

Hewlett Packard Enterprise Company

Vertiv Co.

Dell Inc.

NTT Communications

Capgemini SE

제7장 투자 분석

제8장 시장의 미래

JHS

영문 목차

영문목차

The Data Center Services Market size is estimated at USD 148.31 billion in 2025, and is expected to reach USD 316.65 billion by 2030, at a CAGR of 16.38% during the forecast period (2025-2030).

The primary driver behind the surge in demand for data center services is the widespread adoption of cloud computing. Businesses and firms are turning to cloud services for their storage, computing, and application requirements, leading to a surge in data volumes that necessitates expanded data center capacity.

The rising demand for digital transformation initiatives in multiple industries is driving the need for robust data center infrastructure. Firms are increasingly turning to digital technologies to boost operations, elevate customer experiences, and foster innovation. Organizations are progressively relying on big data and analytics, collecting and analyzing extensive data sets for decision-making. This trend underscores the growing need for robust data storage and processing infrastructure.

In January 2024, Digital Realty, a global provider of cloud- and carrier-neutral data center services, unveiled its inaugural data center in India. Situated in Chennai's industrial hub, the 10-acre campus boasts the capacity to support up to 100 megawatts of critical IT load. This marks a pivotal expansion for the company's global data center platform, addressing the escalating digital transformation demands in significant global markets.

Moreover, the increase of the Internet of Things (IoT) adds another layer of demand, with countless connected devices generating massive amounts of data that need to be stored, processed, and analyzed. The expanding sophistication of artificial intelligence and machine learning necessitates substantial computational power and storage, thereby driving up the demand for data center services.

The surge in remote work and digital services, catalyzed by the COVID-19 pandemic, underscored the importance of data centers. They now serve as crucial hubs for secure and reliable access to information and applications. Additionally, stringent data protection regulations are nudging businesses to bolster their investments in data center services to meet compliance standards. Technological advancements, including energy-efficient designs and enhanced cooling solutions, are enhancing the appeal and cost-effectiveness of data centers, thereby fuelling market growth.

In April 2024, CoreSite, a subsidiary of American Tower Corporation and a provider of hybrid IT solutions, revealed its certification under the NVIDIA DGX-Ready Data Center program. This certification equips CoreSite to offer scalable, high-performance infrastructure, catering specifically to organizations seeking to leverage the growing appetite for artificial intelligence (AI), machine learning (ML), and other high-density applications. Customers opting to host their NVIDIA DGX infrastructure with CoreSite can gain access to a network of high-density data center campuses in key locations, such as Los Angeles, Silicon Valley, Chicago, and Northern Virginia, tailored for NVIDIA AI and high-performance computing.

However, the growth of the market is restricted by high operational costs, energy consumption concerns, and limited availability of skilled professionals. Additionally, data security and privacy challenges, along with regulatory compliance requirements, pose significant barriers to expansion.

Data Center Services Market Trends

Cloud and Hosting is Expected to Capture a Major Share in the Data Center Services Market

The growing demand for cloud and hosting services is propelling the data center services market. This surge is fuelled by the necessity for enhanced, scalable infrastructure. With businesses increasingly shifting to the cloud for its flexibility, scalability, and cost-effectiveness, the demand for reliable data center facilities has surged to support these services.

The rising demand is driving investments in data center construction and expansion. This surge is not only spurring technological advancements but also amplifying the necessity for high-performance computing, storage, and networking solutions. Furthermore, the transition to cloud-based services is fuelling innovation and competition in the data center sphere. This heightened competition is resulting in more robust service portfolios and greater operational efficiencies.

According to Cloudscene, as of March 2024, the United States boasted the highest number of data centers globally, with a reported count of 5,381. Germany followed with 521, and the United Kingdom closely behind with 514.

Billions of internet-connected devices are in operation today, a number that continues to climb. These devices often produce substantial data volumes, necessitating recording, processing, storage, assessment, and retrieval. As IoT and Industry 4.0 advance, manufacturers increasingly turn to big data and analytics to enhance productivity, cut costs, bolster security, and streamline operations.

As data generation accelerates, capturing timely insights becomes increasingly challenging. Emerging digital arenas, like smart cities and intelligent buildings, provide a wealth of readily accessible data. Furthermore, the public cloud's popularity is surging due to its cost-effectiveness and minimal maintenance requirements. Moreover, the accessibility of cloud services is empowering small and medium enterprises to scale efficiently, as they can tailor their infrastructure expenses to match their requirements.

In May 2024, Soluna Holdings Inc., a company specializing in green data centers for Bitcoin mining and intensive computing, revealed a new partnership. It announced its plan to collaborate with a global enterprise GPU-server OEM and an AI Infrastructure-as-a-Service provider. Soluna Cloud is set to launch its services, tapping into the renewable-powered, high-performance data centers of its strategic partner. Moreover, this partnership is expected to broaden Soluna Cloud's services from basic infrastructure to encompass its strategic partner's full suite of AI pipeline software solutions.

North America Holds a Substantial Share in the Market

North America boasts a surplus of technological innovators, driving demand for advanced technologies such as cloud computing and IoT. Given the intricate nature of these technologies, there is a growing need for resilient data center facilities. Consequently, the region is poised to witness a surge in demand for data center services.

The United States, a significant global economy, is poised to drive the expansion of public cloud-based data centers. With the IT industry governing as the nation's primary private employer, the widespread adoption of data centers further fuels market growth. Furthermore, with the surge in hyper-scale platforms, the country finds itself increasingly catering to the data center needs of its hyper-scale platforms.

Businesses in the region are increasingly favoring colocation data centers over building their own. This shift is driven by the realization of the myriad benefits that come with leasing from a colocation facility. Infrastructure facilities are becoming increasingly complex due to the rapid integration of technologies such as networks and connectivity devices.

The market is witnessing intense competitive rivalry driven by both established and emerging players. These industry participants are deploying a mix of organic and inorganic strategies to enhance their competitive edge and fuel market growth. For instance, in June 2024, Oracle and Google Cloud unveiled a strategic partnership, offering customers the flexibility to integrate Oracle Cloud Infrastructure (OCI) with Google Cloud technologies. This collaboration aims to expedite application migrations and upgrades for users. Oracle Interconnect for Google Cloud is projected to be initially available in 11 global regions for customer onboarding, enabling seamless deployment of general-purpose workloads without incurring cross-cloud data transfer fees.

In October 2023, Flexential, a provider of secure and scalable data center solutions, announced that CoreWeave, a specialized cloud provider focusing on large-scale GPU-accelerated workloads, is set to broaden its data center presence. CoreWeave's expansion would see the company moving into two additional colocation facilities, strategically located in Hillsboro, Oregon, and Douglasville, GA. Notably, both these facilities are under the ownership and operation of Flexential. CoreWeave's infrastructure is tailored to cater to the evolving needs of projects spanning machine learning, AI, VFX, rendering, and pixel streaming, showcasing an advanced computing framework.

Data Center Services Industry Overview

The data center service market is highly fragmented, with high competitive rivalry. The major market players are Fujitsu Ltd, Cisco Systems Inc., Capgemini, HCL Technologies Limited, and Hewlett Packard Enterprise Company. Market players are bolstering their portfolios and pursuing enduring competitive edges through strategic partnerships and product innovations.

May 2024: Cologix, the network-neutral interconnection and hyperscale edge data center provider in North America, announced the successful launch of its fourth and most extensive data center in the region. This expansion signifies a pivotal step in Cologix's dedication to addressing the escalating need for colocation and interconnection services in Columbus, Ohio.

February 2024: Global infrastructure Platform-as-a-Service company MOD Mission Critical (MOD) announced an expansion of its partnership with 365 Data Centers (365), a provider of network-centric colocation, cloud, and managed services. Through this partnership, MOD can provide fractional colocation and connectivity solutions, allowing its clients to access the services and resources offered by 365's network-centric data centers across 20 markets, complemented by an additional 125 nationwide points of presence.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitute Products

4.4 Impact of COVID-19 on the Market

4.5 Market Drivers

4.5.1 Increase in the Expenditure on Data Center Technology

4.5.2 Rising Data Center Complexities Due to Scalability