석유 및 가스 산업용 가스 압축기 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Oil And Gas Industry Gas Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1637776

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

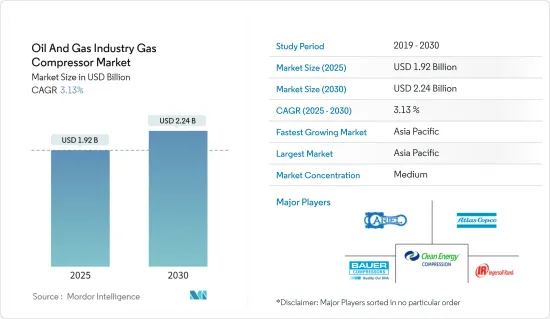

석유 및 가스산업용 가스 압축기 시장 규모는 2025년 19억 2,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 3.13%로, 2030년에는 22억 4,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

장기적으로는 다양한 용도에서의 천연가스 소비량의 성장이 시장을 크게 견인하고 있으며, 가스 생산·공급 프로젝트 증가나 현재의 시나리오에서의 합리적인 천연가스 가격이 업스트림 부문에 좋은 영향을 줍니다.

한편, 에너지 부문에서의 재생가능 에너지의 보급 확대는 천연 가스 소비에 엄격한 경쟁을 초래하여, 많은 용도에서 가스 압축기 전개의 성장을 방해하고 있습니다.

천연가스 확인 매장량 증가, 특히 최근 상황에 있는 오프쇼어 가스전은 가스 압축기 시장에 큰 기회를 가져왔습니다. 아주 최근 러시아 그룹인 Lukoil이 멕시코 앞바다에서 발견한 석유 및 가스전이 그 예입니다. 향후 새롭게 생산되는 유전은 개더링 라인용 가스 압축기의 배치 확대로 이어질 것으로 예상됩니다.

석유 및 가스 압축기 시장 동향

중류부문이 시장을 독점할 전망

석유 및 가스 산업의 중류에서 사용되는 가스 압축기는 가스 송전 파이프라인 네트워크 내 또는 압축 가스 저장 장치 중 하나에 배치됩니다. 파이프라인을 통해 흐르는 가스는 유속과 파이프의 길이에 따라 증가하는 압력 손실을 겪습니다. 따라서 50-100마일마다 가스를 재압축하여 압력 손실을 보완하기 위한 컴프레서 스테이션이 필요합니다.

천연가스 소비량은 지난 10년간 지속적으로 증가세를 보였으며, 2022년 소비량은 약 3조 9,413억 입방미터입니다. 많은 국가에서 정부가 보다 깨끗한 에너지 생성 방법을 추진하고 있기 때문에 수요는 향후 수년간 확대될 것으로 예상됩니다. 앞으로 몇 년동안 많은 파이프라인과 LNG 프로젝트가 많은 중류 기업의 달성된 프로젝트 목록에 추가될 예정입니다.

예를 들어, 아델피아 게이트웨이 프로젝트는 미국 연방 에너지 규제위원회(FERC)로부터 제2기 프로젝트의 건설 승인을 받았습니다. 이 프로젝트에는 기존 84마일의 석유 파이프라인을 필라델피아 지역에서 배급하기 위한 가스 공급 파이프라인으로 전환하는 작업이 포함되어 있습니다. 개발자인 Adelphia Gateway LLC는 2023년 말까지 파이프라인에서 최초의 가스를 공급할 전망입니다.

게다가 2023년 2월, 인도의 국영 탄화수소 대기업인 석유·천연가스 공사는 이 회사의 주요 서해안 유전에서 생산에 중요한 프로젝트인 대규모 파이프라인 교환 프로젝트를 시작했습니다. 이 4억 4,600만 달러의 프로젝트는 서해안을 따라 4만 평방 킬로미터에 이르는 ONGC 유전에서 석유 및 가스의 안정적인 공급을 보장합니다. 석유 및 가스산업에서 컴프레서는 천연가스의 압력을 높이고 생산현장에서 천연가스 수송을 가능하게 하는 중요한 역할을 담당하고 있기 때문에 이러한 프로젝트는 나아가 산업 전체에서 컴프레서의 이용을 홍보하게 됩니다.

이러한 개발은 예측 기간 동안 석유 및 가스 산업의 가스 압축기 시장에 긍정적인 영향을 미칠 것입니다.

아시아태평양이 시장 성장을 지배할 전망

아시아태평양은 수송과 산업 부문의 소비 증가로 인해 가까운 미래에 가스 수요 증가의 절반을 차지할 수 있습니다. 발전산업 및 기타 용도의 천연가스 수요에 대응하기 위해 이 지역에서는 주로 인도나 중국 등의 국가에서 파이프라인망의 확대를 볼 수 있습니다.

중국의 LNG와 파이프라인에 의한 천연가스 수입은 2022년 기록적인 수준에 이르렀으며 LNG 수입량은 지난 10년간 16.6% 이상 증가했습니다. 수입의 급증은 국내 파이프라인 인프라의 확대로 이어집니다. 또한 인도는 2023년까지 3만 4,384km의 새로운 파이프라인을 가동할 예정입니다.

2023년 3월, Aramco와 합작 파트너인 Panjin Xincheng Industrial Group과 NORINCO Group은 중국 북동부에서 대규모 통합 정유소와 석유화학 콤플렉스 건설을 시작할 계획을 발표했습니다. 이 복합단지은 일당 30만 배럴 정유소와 연산 165만톤의 에틸렌과 200만톤의 파라크실렌을 생산하는 석유화학 플랜트를 겸비할 예정입니다. 건설은 프로젝트가 행정허가를 확보한 후 2023년 2분기에 시작될 예정입니다. 2026년까지 완전 가동을 시작할 예정입니다.

또한 CNG 급유소의 네트워크가 급속히 확대되고 있는 것도 아시아태평양의 가스 압축기 시장의 개척으로 이어지고 있습니다. 예를 들어 인도 정부는 2023년 4월, 2030년까지 전국에 약 1만 7,700개의 CNG 스테이션을 설치하는 목표를 정했다고 발표했습니다.

이러한 신흥국 시장의 개척으로 가스 압축기 시장은 조사 기간 동안 아시아태평양에서 가장 번영할 것으로 예상됩니다.

석유 및 가스 압축기 산업 개요

석유 및 가스 산업의 가스 압축기 시장은 반고체화되고 있습니다. 주요 기업(순부동)에는 Atlas Copco AB, Ariel Corporation, Bauer Compressor Inc., Clean Energy Fuels Corp., Ingersoll Rand PLC 등이 있습니다.

Atlas Copco AB는 연구개발 주력, 시장개척 확대, 업무효율 향상, 보다 우수한 가치를 제공하는 지속가능한 신제품 및 솔루션 개발, 에너지 효율 개선 등 많은 전략을 채택하고 있습니다. 예를 들어 Atlas Copco는 2023년 2월 차세대 GA 및 GA 고정 속도 스마트 산업용 에어컨 프레서를 발표했습니다. 이러한 기술 혁신은 다양한 제품 포트폴리오를 통해 산업 고객의 변화하는 요구에 더 잘 대응할 수 있습니다. 이러한 새로운 유형의 압축기는 천연 가스 처리 및 수소 제조와 같은 청정 에너지 용도에도 사용할 수 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2028년까지 시장 규모와 수요 예측(단위:달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

다양한 용도에서의 천연 가스 소비의 성장

억제요인

에너지 부문에서의 재생 가능 에너지의 보급 확대

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

유형

레시프로

스크류

용도

업스트림

다운스트림

미드스트림

지역

북미

미국

캐나다

멕시코

유럽

독일

프랑스

스페인

영국

기타 유럽

아시아태평양

중국

인도

말레이시아

인도네시아

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

나이지리아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Ariel Corporation

Atlas Corporation AB

Bauer Compressors Inc.

Burckhardt Compression Holding AG

Clean Energy Fuels Corp.

General Electric Company

HMS Group

Howden Group Ltd

Ingersoll Rand PLC

Siemens AG

제7장 시장 기회와 앞으로의 동향

천연가스 확인 매장량 증가, 특히 해양가스전 증가

JHS

영문 목차

영문목차

The Oil And Gas Industry Gas Compressor Market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Key Highlights

Over the long term, the market is largely driven by the growth in natural gas consumption for various applications, which has led to more gas production and transmission projects and reasonable natural gas prices in the current scenario, which has a positive impact on the upstream sector.

On the other hand, the growing penetration of renewables in the energy sector offers stiff competition to natural gas consumption and thus impedes the growth of gas compressor deployment in numerous applications.

Nevertheless, the increase in natural gas proved reserves, particularly offshore gas fields in the recent picture, places a tremendous opportunity for the gas compressor market. The very recent Russian group's Lukoil's oil and gas field discovery off the coast of Mexico is an example of the same. The new upcoming producing fields will lead to a greater deployment of gas compressors for gathering lines.

Oil and Gas Compressor Market Trends

Midstream Sector Expected to Dominate the Market

The gas compressors used in the midstream oil and gas industry are deployed either within the gas transmission pipeline network or at the compressed gas storage units. Gas flowing in pipelines suffers from pressure losses that increase with flow velocity and the length of the pipe. Therefore, every 50 to 100 miles, a compressor station is necessary to recompress the gas and compensate for the pressure losses.

Natural gas consumption continuously showed an advancing trend over the last 10 years, with around 3941.3 billion cubic meters of consumption in 2022. The demand is expected to grow in the coming years due to the government's push for cleaner methods of energy generation in many countries. A number of pipeline and LNG projects are about to be added to the list of accomplished projects of many midstream companies in the coming years.

For instance, the Adelphia Gateway Project received approval for the construction of the second phase of the project from the Federal Energy Regulatory Commission (FERC), United States. The project includes the conversion of an existing 84-mile oil pipeline to a gas supply pipeline for distribution in the Philadelphia region. The developer, Adelphia Gateway LLC, is expected to be able to supply the first gas from the pipeline by the end of 2023.

Furthermore, in February 2023, Oil and Natural Gas Corporation, India's state-owned hydrocarbon giant, initiated a big-buck pipeline replacement project, a crucial project for the company's production from key west coast fields. The USD 446 million project will ensure a stable supply of oil and gas from ONGC wells covering an area of 40,000 square kilometers along the western coast. Since compressors play a crucial role in the oil and gas industry in increasing the pressure of natural gas and allowing natural gas transportation from the production site, this kind of project will, in turn, promote the usage of compressors across the industry.

Such developments will inevitably have a positive impact on the gas compressor market in the oil and gas industry during the forecast period.

Asia-Pacific Expected to Dominate Market Growth

Asia-Pacific can account for half of the incremental gas demand in the near future due to increased consumption in the transport and industrial sectors. To serve the natural gas demand for the power generation industry and other applications, the region has witnessed an expansion in the pipeline network, mainly in countries like India and China.

China's LNG and pipeline imports of natural gas reached record levels in 2022, with an increment of more than 16.6% in LNG imports during the last decade, whereas the gas pipeline monthly imports approached a peak level of 4 million metric tons. The surge in imports will lead to an expansion of the supporting pipeline infrastructure in the country. Moreover, India is expected to bring 34,384 km of new pipelines online by 2023.

In March 2023, Aramco and joint venture partners Panjin Xincheng Industrial Group and NORINCO Group announced plans to start the construction of a significant integrated refinery and petrochemical complex in northeast China. The complex is going to have combination of a 300,000 barrels per day refinery and a petrochemical plant with an annual production capacity of 1.65 million tons of ethylene and 2 million metric tons of paraxylene. Construction is expected to start in the second quarter of 2023 after the project has secured administrative approvals. It is expected to be fully operational by 2026.

Also, the rapidly growing network of CNG fueling stations has led to the development of the gas compressor market in the Asia-Pacific region. For example, in April 2023, the government of India announced the target has been fixed to establish around 17,700 CNG stations across the country by 2030.

Owing to such developments, the gas compressor market is expected to flourish to the greatest extent in the Asia-Pacific region during the study period.

Oil and Gas Compressor Industry Overview

The oil and gas industry's gas compressor market is semi-consolidated. Some of the major companies (in no particular order) include Atlas Copco AB, Ariel Corporation, Bauer Compressor Inc., Clean Energy Fuels Corp., and Ingersoll Rand PLC, among others.

Atlas Copco AB has adopted many strategies like focus on research and development, increase market coverage, increase operational efficiency, develop new sustainable products and solutions offering better value and improved energy efficiency. As an example, in February 2023, the company launched its next generation GA and GA+fixed speed smart industrial air compressors,. Such technological innovations would enable the company to better respond to the changing needs of the industrial customers with diversified product portfolio. These new type of compressors can also be used for clean energy applications like natural gas processing, and hydrogen production.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growth in Natural Gas Consumption for Various Applications

4.5.2 Restraints

4.5.2.1 Growing Penetration of Renewables in the Energy Sector

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Reciprocating

5.1.2 Screw

5.2 Application

5.2.1 Upstream

5.2.2 Downstream

5.2.3 Midstream

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 France

5.3.2.3 Spain

5.3.2.4 United Kingdom

5.3.2.5 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Malaysia

5.3.3.4 Indonesia

5.3.3.5 Rest of Asia-Pacifc

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East & Africa

5.3.5.1 Saudi Arabia

5.3.5.2 United Arab Emirated

5.3.5.3 Nigeria

5.3.5.4 South Africa

5.3.5.5 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Ariel Corporation

6.3.2 Atlas Corporation AB

6.3.3 Bauer Compressors Inc.

6.3.4 Burckhardt Compression Holding AG

6.3.5 Clean Energy Fuels Corp.

6.3.6 General Electric Company

6.3.7 HMS Group

6.3.8 Howden Group Ltd

6.3.9 Ingersoll Rand PLC

6.3.10 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increase in Natural Gas Proved Reserves, Particularly Offshore Gas Fields