ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

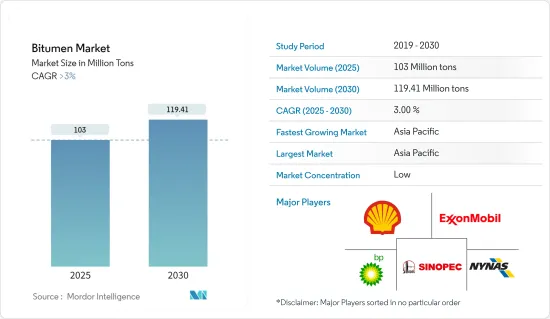

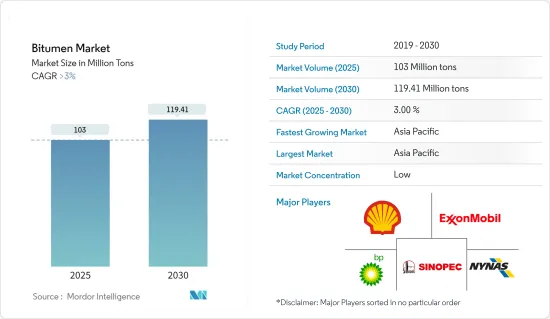

역청 시장 규모는 2025년에 1억 300만 톤으로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 3%를 넘어 2030년에는 1억 1,941만 톤에 달할 것으로 예측됩니다.

COVID-19는 세계 시장의 역청 수요에 부정적인 영향을 미쳤습니다. COVID-19로 인해 많은 건설 프로젝트가 보류되면서 전 세계적으로 아스팔트 사용량이 감소했습니다. 그러나 봉쇄와 제한이 완화되면서 주요 지역에서 건설 활동이 계속되었습니다. 그 이후로 역청 시장은 꾸준히 성장하고 있습니다.

주요 하이라이트

역청 시장의 성장은 도로 건설 및 수리 활동의 증가와 상업용 및 가정용 건축 부문에서 필러, 접착제 또는 실란트로서 역청에 대한 수요가 증가함에 따라 주도되고 있습니다.

반면에 여러 가지 유해한 대기 배출물을 발생시키는 역청의 사용과 같은 환경 문제가 증가하면서 시장 성장에 걸림돌이 되고 있습니다.

고성능 역청 제품 및 도로 인프라 개발을 개선하기 위한 역청 가공에 대한 연구 개발은 향후 역청 시장에 다양한 기회를 창출할 것으로 예상됩니다.

아시아태평양은 역청 시장에서 큰 점유율을 차지하며 예측 기간 동안 가장 높은 연평균 성장율(CAGR)을 나타낼 것으로 예상됩니다.

역청 시장 동향

시장을 독점하는 도로 건설 부문

도로 건설 산업은 전 세계적으로 역청의 최대 소비처 중 하나이며, 전체 역청 소비의 상당 부분을 차지합니다. 도로, 고속도로 및 기타 교통 인프라 포장에 필요한 아스팔트의 엄청난 양이 시장 지배력에 기여하고 있습니다.

역청 기반 아스팔트 도로는 뛰어난 내구성, 유연성, 풍화에 대한 저항성을 갖추고 있어 도로 건설 프로젝트에 매우 적합합니다. 아스팔트 도로는 무거운 교통량, 다양한 기상 조건 및 기타 환경 요인을 견딜 수 있어 장기적인 성능과 비용 효율성을 보장합니다.

컨설팅 및 투자 은행인 FMI Corporation에 따르면 북미의 엔지니어링 및 건설 지출은 2024년 말까지 2% 증가할 것으로 예상됩니다.

또한 미국 인구조사국이 발표한 데이터에 따르면 미국 내 교통용 민간 건설의 가치는 2020년 163억1천만 달러에서 2023년 193억9천만 달러로 증가했습니다.

아시아태평양 개발도상국, 특히 교통 부문은 도시화 증가와 전통적인 부문에서 신흥 2차 산업으로 초점이 이동함에 따라 인프라 프로젝트가 크게 증가할 것으로 예상됩니다. 또한, 경제 번영으로 인해 원자재를 공급하고 소비자에게 판매하는 운송 및 제조업과 같은 소비 부문에 대한 인프라 자금 조달이 증가하고 있습니다.

중국 국가건설공정총공사(CSCEC)는 2020년 4,186킬로미터에서 2022년에 총 4,623킬로미터의 신규 도로 건설에 서명했습니다. 이러한 추세는 아스팔트 시장도 뒷받침합니다.

인도는 NIP에 따라 인프라에 약 1억 달러의 투자 예산을 배정했습니다. 인도는 델리-뭄바이 산업 회랑, 암리차르-콜카타 산업 회랑, 비자그-첸나이 산업 회랑, 벵갈루루-첸나이 산업 회랑, 벵갈루루-뭄바이 산업 회랑 등 여러 산업 회랑 개발을 위한 예산안을 통과시켰습니다. 이 프로젝트들은 2025년 3월까지 완공될 예정으로, 향후 몇 년 동안 역청 수요가 증가할 것으로 예상됩니다.

이러한 모든 요인들에 의해 역청 시장은 예측 기간 동안 세계적으로 성장할 가능성이 높습니다.

아시아태평양이 시장을 독점

인도, 중국 및 기타 동남아시아 국가와 같은 여러 국가의 급속한 산업화와 도시화로 인해 도로, 고속도로, 공항 및 항구를 포함한 인프라 프로젝트에 대한 상당한 투자가 이루어지면서 역청에 대한 수요가 증가하고 있습니다.

아시아태평양 지역의 건설 부문은 아스팔트의 최대 소비처 중 하나로, 주거, 상업 및 산업 건설 프로젝트가 진행되면서 도로 포장, 지붕 및 방수용 아스팔트와 같은 아스팔트 기반 자재에 대한 수요가 증가하고 있습니다.

곧 발표될 중국의 제15차 5개년 계획은 교통, 에너지, 수도 시스템, 도시 개발 분야의 새로운 인프라 프로젝트에 초점을 맞추고 있습니다. 첫 번째 배치에는 중국 북동부와 베이징-톈진-허베이 지역의 고표준 농지 건설을 포함한 약 2,900개의 프로젝트가 포함됩니다.

인도에서는 India Brand Equity Foundation(IBEF)이 발표한 데이터에 따르면 2,000년 4월부터 2023년 3월까지 주택, 인프라, 건설 개발 프로젝트 등 건설 개발에 대한 외국 직접 투자(FDI)는 263억 5,000만 달러에 달했습니다.

인도에서 역청 수요를 증가시킬 것으로 예상되는 예정된 프로젝트에는 델리-뭄바이 산업 회랑, 바라트말라 프로젝트, 구자라트 국제 금융 테크시티(GIFT), 스마트 시티 코치, 나비 뭄바이 국제공항 등이 있습니다.

인도 투자 촉진 및 촉진청이 발표한 자료에 따르면 인도는 2024 회계연도에 1조 4,000억 달러의 예산을 인프라에 배정했습니다. 이 중 24%는 재생 에너지, 18%는 도로 및 고속도로, 17%는 도시 인프라, 12%는 철도에 배정되었습니다.

위의 요인으로 인해 예측 기간 동안 아시아태평양의 역청 수요가 증가할 것으로 예상됩니다.

역청 산업 개요

역청 시장은 세분화되어 있으며 압도적인 점유율을 가진 주요 업체는 존재하지 않습니다. 주요 진출기업(무순서)에는 ExxonMobil, Shell, BP PLC, NYNAS AB, China Petroleum & Chemical Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

도로 건설과 보수 활동 증가

상업 빌딩과 국내 빌딩 건설에 의한 수요

억제요인

환경에 대한 우려

기타 억제요인

산업의 밸류체인 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

원료 분석

제5장 시장 세분화(시장 규모(수량))

제품 유형별

포장 등급

경질 등급

산화 등급

역청 에멀젼

폴리머 개질 역청

기타 제품 유형

용도별

도로 건설

방수

접착제

기타 용도(공업용 도료)

지역별

아시아태평양

중국

인도

일본

한국

인도네시아

태국

말레이시아

베트남

ASEAN 국가

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

러시아

스페인

터키

노르딕

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

BMI Group(Icopal Enterprise ApS)

Bouygues Group

BP PLC

China Petroleum & Chemical Corporation

ENEOS Corporation(JXTG Nippon Oil & Energy Corporation)

Exxon Mobil Corporation

Indian Oil Corporation Ltd

Kraton Corporation

Marathon Oil Company(Marathon Petroleum LP)

NYNAS AB

Shell

Suncor Energy Inc.

제7장 시장 기회와 앞으로의 동향

도로 인프라 개선을 위한 역청 가공에 관한 연구 개발

고성능 역청 제품 개발

HBR

영문 목차

영문목차

The Bitumen Market size is estimated at 103 million tons in 2025, and is expected to reach 119.41 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

COVID-19 adversely influenced the demand for bitumen on the global market. During COVID-19, a large number of construction projects were on hold, reducing the use of bitumen throughout the world. However, as lockdowns and restrictions eased, there was continued construction activity in major regions. Since then, the market has been growing steadily.

Key Highlights

The growth of the bitumen market is driven by increased road construction and repair activities, as well as a growing demand from both commercial and domestic building sectors for bitumen as fillers, adhesives, or sealants.

On the flip side, increasing environmental concerns, such as the utilization of bitumen, which generates several harmful atmospheric emissions, have been hindering the market's growth.

Research and development on bitumen processing to improve the development of high-performance bitumen products and road infrastructure are expected to create various opportunities for the bitumen market in the upcoming years.

Asia-Pacific is expected to hold a significant share of the bitumen market and witness the highest CAGR during the forecast period.

Bitumen Market Trends

Road Construction Segment to Dominate the Market

The road construction industry is one of the largest consumers of bitumen globally, accounting for a significant portion of total bitumen consumption. The sheer volume of bitumen required for paving roads, highways, and other transportation infrastructure contributes to its dominance in the market.

Bitumen-based asphalt pavements offer excellent durability, flexibility, and resistance to weathering, making them well-suited for road construction projects. Asphalt roads can withstand heavy traffic loads, varying weather conditions, and other environmental factors, ensuring long-term performance and cost-effectiveness.

According to the FMI Corporation (a consulting and investment bank), engineering and construction spending in North America is expected to increase by 2% by the end of 2024.

Moreover, according to the data released by the United States Census Bureau, the value of private construction for transportation in the United States increased by USD 16.31 billion in 2020 to USD 19.39 billion in 2023.

Infrastructure projects are expected to increase significantly in developing Asia-Pacific economies, particularly the transport sector, due to increased urbanization and shifting focus from traditional sectors toward emerging secondary industries. In addition, the growing economic prosperity is driving infrastructure financing toward consumer sectors such as transport and manufacturing, where raw materials are provided and sold to consumers.

The China State Construction Engineering Corporation (CSCEC) signed a total of 4,623 kilometers of new road construction in 2022, up from 4,186 kilometers in 2020. This trend also supports the bitumen market.

Under NIP, India allocated an investment budget of ~USD 1000 million for infrastructure. India passed a budget to develop several industrial corridors, including the Delhi-Mumbai Industrial Corridor, Amritsar-Kolkata Industrial Corridor, Vizag-Chennai Industrial Corridor, Bengaluru-Chennai Industrial Corridor, and the Bengaluru-Mumbai Industrial Corridor. These projects are expected to be completed by March 2025, which is expected to increase the demand for bitumen in the coming years.

Owing to all these factors, the bitumen market is likely to grow globally during the forecast period.

Asia-Pacific to Dominate the Market

The rapid industrialization and urbanization in various countries such as India, China, and other Southeast Asian nations have led to significant investments in infrastructure projects, including roads, highways, airports, and ports, driving the demand for bitumen.

The construction sector in Asia-Pacific is one of the largest consumers of bitumen, with ongoing residential, commercial, and industrial construction projects fueling the demand for bitumen-based materials such as asphalt for road paving, roofing, and waterproofing.

China's upcoming 15th Five-Year Plan focuses on new infrastructure projects in transport, energy, water systems, and urban development. The first batch includes about 2,900 projects, including the construction of high-standard farmland in northeast China and the Beijing-Tianjin-Hebei region.

In India, according to the data published by the Indian Brand Equity Foundation (IBEF), foreign direct investment (FDI) in construction development, such as housing, infrastructure, and construction development projects, was valued at USD 26.35 billion between April 2000 and March 2023.

The upcoming projects in India that are assumable to increase the demand for bitumen include the Delhi-Mumbai Industrial Corridor, Bharatmala Project, Gujarat International Finance Tec-City (GIFT), Smart City Kochi, and Navi Mumbai International Airport.

According to the data published by the National Investment Promotion and Facilitation Agency, India has allocated a budget of USD 1.4 trillion for infrastructure for FY 2024. Of this, 24% is for renewable energy, 18% is for roads and highways, 17% is for urban infrastructure, and 12% is for railways.

The factors mentioned above are expected to increase the demand for bitumen in Asia-Pacific during the forecast period.

Bitumen Industry Overview

The bitumen market is fragmented, with no major players having a dominant share. Some of the major players (not in any particular order) include Exxon Mobil Corporation, Shell, BP PLC, NYNAS AB, and China Petroleum & Chemical Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Road Construction and Repair Activities

4.1.2 Demand from Commercial and Domestic Building Constructions

4.2 Restraints

4.2.1 Environmental Concerns

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Feedstock Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Product Type

5.1.1 Paving Grade

5.1.2 Hard Grade

5.1.3 Oxidized Grade

5.1.4 Bitumen Emulsions

5.1.5 Polymer Modified Bitumen

5.1.6 Other Product Types (Emulsified)

5.2 By Application

5.2.1 Road Construction

5.2.2 Waterproofing

5.2.3 Adhesives

5.2.4 Other Applications (Industrial Coatings)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Indonesia

5.3.1.6 Thailand

5.3.1.7 Malaysia

5.3.1.8 Vietnam

5.3.1.9 ASEAN Countries

5.3.1.10 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Russia

5.3.3.6 Spain

5.3.3.7 Turkey

5.3.3.8 NORDIC

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombian

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Nigeria

5.3.5.4 Qatar

5.3.5.5 Egypt

5.3.5.6 UAE

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BMI Group (Icopal Enterprise ApS)

6.4.2 Bouygues Group

6.4.3 BP PLC

6.4.4 China Petroleum & Chemical Corporation

6.4.5 ENEOS Corporation (JXTG Nippon Oil & Energy Corporation)

6.4.6 Exxon Mobil Corporation

6.4.7 Indian Oil Corporation Ltd

6.4.8 Kraton Corporation

6.4.9 Marathon Oil Company (Marathon Petroleum LP)

6.4.10 NYNAS AB

6.4.11 Shell

6.4.12 Suncor Energy Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Research and Development on Bitumen Processing to Improve Road Infrastructure

7.2 Development of High-Performance Bitumen Products