ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

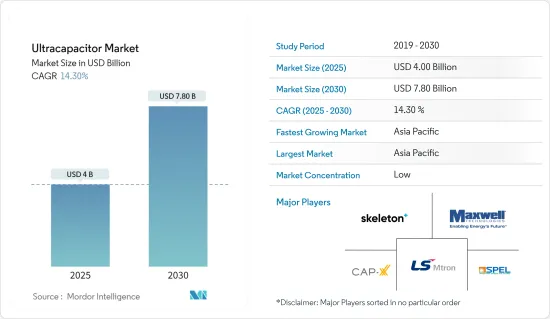

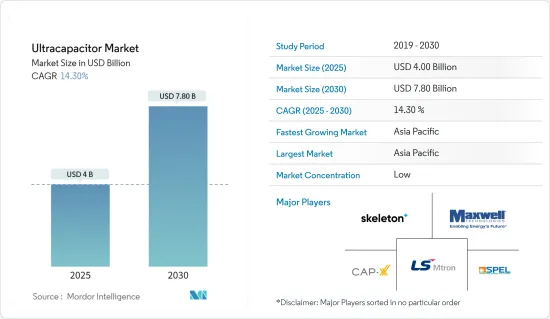

울트라커패시터 시장 규모는 2025년에 40억 달러로 추정되며 예측기간 중(2025-2030년) 연평균 성장율(CAGR)은 14.3%를 나타낼 전망이며, 2030년에는 78억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

자동차 산업이 커패시터 시장을 주도하고 있습니다. 업계가 지속 가능하고 에너지 효율적인 자동차로 전환함에 따라 커패시터는 회생 브레이크, 엔진 시동 정지 시스템, 에너지 회수 시스템 등의 응용 분야에서 점점 더 많이 사용되고 있습니다. 신속한 에너지 공급이 가능한 커패시터는 이러한 용도에서의 효율성을 높이고 있습니다. 게다가 자동차 제조업체는 현재 성능을 최적화하기 위해 배터리와 커패시터를 결합한 하이브리드 에너지 저장 솔루션을 찾고 있습니다.

신재생에너지 프로젝트가 급증함에 따라 효율적인 에너지 저장과 그리드 안정화 솔루션에 대한 수요가 증가하고 있습니다. 울트라커패시터는 전력 생산량이 많을때, 잉여 에너지를 저장하고 발전량이 적을 시기에 그것을 방출함으로써 그리드 안정화를 돕는 매우 중요한 역할을 담당하고 있습니다. 이 기능은 재생 가능 에너지 시스템, 특히 풍력 발전 및 태양광 발전에서 울트라 커패시터의 중요성을 강조합니다.

현재 진행중인 연구 개발 노력은 커패시터의 에너지 밀도를 높이고 기존 배터리와 경쟁 하는 것을 목표로 하고 있습니다. 특히 그래핀이나 카본나노튜브를 이용한 재료혁신은 고출력이나 급속충전을 영향을 주지 않고 저장 용량의 향상을 하는 것입니다. 주목할 만한 사례로는 2023년에 멜버른의 EnyGy는 2023년 최첨단 그래핀 기술을 활용한 울트라커패시터를 발표했습니다.

그러나 슈퍼커패시터는 장기적인 에너지 저장에는 한계가 있습니다. 그 방전 속도는 리튬 이온 배터리를 넘어 매일 10-20%의 자체 방전 손실이 생깁니다. 배터리는 소모될 때까지 거의 일정한 전압을 유지하지만, 커패시터는 충전에 의해 전압이 선형적으로 떨어집니다.

청정 에너지를 요구하는 세계의 움직임과 엄격한 환경 규제는 커패시터 시장에 유리한 분위기를 만들어 냅니다. 이산화탄소 배출량 감축, 전기자동차 및 재생 가능 에너지 도입 촉진을 목적으로 한 시책이 시장 성장을 뒷받침하고 있습니다. 게다가 연구개발, 특히 에너지 저장 기술에 대한 정부와 민간 부문의 투자는 첨단 커패시터의 진화를 가속화하고 있습니다.

커패시터 시장 동향

자동차 및 운송 부문의 수요 증가

전기자동차와 하이브리드 자동차의 급속한 보급이 커패시터 수요를 크게 증가시키고 있습니다. 기존 배터리와 달리 커패시터는 높은 전력 밀도를 자랑하며 빠른 충전과 방전을 가능하게 합니다. 이 때문에 회생 브레이크나 스타트 및 스톱 시스템 등의 용도에 특히 적합합니다. 슈퍼캡 기술은 회생 제동 테스트 리그에서 광범위하게 활용되고 있으며, 슈퍼커패시터 구현에 따른 도전과 기회를 활용하고 있습니다. 슈퍼커패시터의 뛰어난 전력 밀도와 사이클링 특성은 매우 바람직합니다.

예를 들어, Skeleton Technologies의 슈퍼커패시터는 혼다 CR-V 하이브리드 레이서에 탑재되어 있습니다. 이 데모 차량은 혼다 퍼포먼스 개발의 실력을 나타내는 동시에 혼다의 2023년 인디카 하이브리드 파워 유닛 기술을 발표하고 있습니다. Skeleton의 슈퍼커패시터 덕분에 레이스카는 고출력 성능을 향상시켰습니다. 이 슈퍼 커패시터는 제동 에너지 회수와 가속력 향상을 위한 완벽한 솔루션으로 선전되고 있습니다. 낮은 내부 저항, 높은 순환성, 뛰어난 노화 저항 등 주목할 만한 장점이 있습니다.

KAIST(한국과학기술원) 연구진이 혁신적인 에너지 저장 솔루션을 공개했습니다. 이 새로운 시스템은 슈퍼 커패시터의 장점과 나트륨 이온 배터리 화학의 비용 효율성 및 공급망 이점을 결합한 것입니다. 연구팀은 이 새로운 배터리가 전기 자동차 분야에 큰 파장을 일으킬 것으로 기대하고 있습니다. 연구팀이 개발한 새로운 배터리는 슈퍼커패시터 기술에 적합한 음극과 고급 양극을 통합합니다. 이러한 시너지 효과 덕분에 이 배터리는 인상적인 저장 용량과 빠른 충전-방전 속도를 자랑하며 리튬 이온 배터리의 강력한 경쟁자로 자리매김할 수 있습니다.

미국에서는 주로 세 가지 급속 충전 표준이 지배적입니다. CHAdeMO, 복합 충전 시스템(CCS), 북미 충전 표준(이전에는 Tesla 표준)입니다. 이 중, 급속 충전소의 수에서는 CCS 방식이 리드하고 있습니다. 미국 에너지부의 데이터에 따르면, 2024년에는 CCS 스테이션이 7,315개, CHAdeMO 스테이션이 5,720개, NACS 스테이션이 2,280개가 됩니다. 이 인프라의 확대는 전기자동차에서 커패시터의 사용 확대를 뒷받침합니다.

울트라 커패시터는 에너지 회수 시스템, 특히 전기 버스, 트램, 고속 열차와 같은 대중 교통 부문에서 매우 중요한 역할을 담당합니다. 자동차 산업에서 중요한 과제는 마모 없이 높은 주기를 견디는 부품을 조달하는 것입니다. 울트라커패시터는 이 영역에서 빛을 발해, 열화를 최소한으로 억제하면서 수백만회의 충전 및 방전 주기를 손쉽게 처리합니다. 산업이 전동화, 연비 효율, 지속가능성에 더욱 집중함에 따라 울트라커패시터의 중요성은 증대의 길을 따라가고 있습니다.

아시아태평양이 시장을 견인

중국, 일본, 한국은 혁신적인 에너지 저장 솔루션에 막대한 투자를 하는 자동차 산업에 힘입어 전기 자동차 생산을 주도하고 있습니다. 지속 가능한 교통수단을 향한 강력한 추진력과 더불어 이 지역의 전기차 인프라가 빠르게 확장되면서 시장이 더욱 발전할 것으로 보입니다.

전기자동차에 그치지 않고 아시아태평양은 신재생에너지 투자에 있어서도 중요한 역할을 담당하고 있습니다. 중국과 인도 등 국가들이 태양광 발전과 풍력 발전 프로젝트를 강화하고 있기 때문에 에너지 저장 솔루션에 대한 수요가 급증하고 있습니다. Carbon Brief의 조사에 따르면 청정 에너지 투자가 전년대비 40% 증가, 2023년에는 총액 8,900억 달러에 달한다고 지적하고 있습니다. 이 성장은 중국 경제 전체의 투자 급증의 전체를 차지합니다. 신속한 충전 및 방전 능력으로 알려진 울트라 커패시터는 이러한 재생 가능 에너지 시스템의 안정화에 매우 중요한 것으로 입증되었습니다.

강력한 제조 거점과 기술 발전으로 잘 알려진 아시아태평양지역은 연구 개발에 중점을 두고 있습니다. 많은 투자를 바탕으로 커패시터의 성능을 향상시킬 뿐만 아니라 소비자 전자 제품에서 산업기계에 이르기까지 다양한 분야에서의 응용을 확대하고 있습니다.

전자제품 제조업에 중요한 도약으로서 인도는 2024년 10월, 케랄라주 카누르에 최초의 슈퍼커패시터 제조 공장을 개장했습니다. 이 시설은 인도 국방, 전기자동차, 심지어 우주 임무를 포함한 다양한 부문을 위한 최고급 슈퍼커패시터를 생산하는 것을 목표로 합니다.

이산화탄소 배출량 감소를 목표로 하고 녹색 에너지 솔루션을 지지하는 정부의 노력은 커패시터의 신속한 도입에 박차를 가하고 있습니다. EV생산과 신재생에너지에 대한 노력을 강화하는 장려금과 보조금으로 커패시터시장의 성장환경이 갖추어지고 있습니다.

커패시터 산업 개요

울트라 커패시터 시장은 기술 혁신과 시장 확대를 우선시하는 기존 다국적 기업과 신흥 기업이 모두 참여하여 치열한 경쟁을 벌이고 있습니다. 이 부문의 주목할만한 진출기업으로는 axwell Technologies, Skeleton Technologies, LS Mtron Ltd, Eaton Corporation 등이 있습니다. 이러한 기업들은 탄탄한 세계 실적, 종합적인 연구개발 능력, 폭넓은 제품 제공을 통해 그 입지를 굳혀 왔습니다.

경쟁은 자동차, 신재생에너지, 산업용도 등의 부문에서 수요가 증가함에 따라 치열해지고 있습니다. 주요 업체들은 R&D 노력을 강화하고, 투자를 확보하고, 자금을 조달하여 시장 입지를 공고히 하고 제품 범위를 넓히고 있습니다. 예를 들어, Skeleton Technologies는 2023년 10월에 1억 800만 유로의 자금을 확보하고 차세대 제품 개발을 급속히 진행하고 슈퍼커패시터 제조를 확대했습니다.

커패시터 시장에서 지속적인 연구 개발은 경쟁 우위를 얻기 위해 가장 중요합니다. 기업은 에너지 밀도를 높이고 비용을 줄이기 위해 탄소나노튜브와 그래핀과 같은 첨단 재료를 연구하고 있습니다. 앞으로 시장은 기술적 혁신, 비용 효율성 및 주요 산업의 역동적인 에너지 수요에 적응하는 데 초점을 맞추고 경쟁 격화를 계획하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 역학

시장 성장 촉진요인

에너지 효율이 높은 솔루션에 대한 수요 증가

전기자동차(EV) 시장의 성장

재생 가능 에너지 시스템의 진보

시장 성장 억제요인

초기 비용의 높이

배터리에 비해 낮은 에너지 밀도

제6장 시장 세분화

유형별

정전 커패시터

슈도 커패시터

하이브리드 커패시터

최종 사용자 산업별

자동차 및 운송

소비자 및 전기

에너지 및 전력

산업용 제조

항공우주 및 방위

기타

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Skeleton Technologies

Maxwell Technologies

CAP-XX

SPEL TECHNOLOGIES PRIVATE LTD.

LS Mtron Co., Ltd.

IOXUS

Nippon Chemi-Con Corporation

Shanghai Aowei Technology Development Co., Ltd

KEMET Corporation

Eaton Corporation

Yunasko

VINATech Co., Ltd

SECH

제8장 투자 분석

제9장 시장의 미래

HBR

영문 목차

영문목차

The Ultracapacitor Market size is estimated at USD 4.00 billion in 2025, and is expected to reach USD 7.80 billion by 2030, at a CAGR of 14.3% during the forecast period (2025-2030).

Key Highlights

The automotive sector drives the ultracapacitor market. As the industry shifts towards sustainable and energy-efficient vehicles, ultracapacitors are increasingly used in applications like regenerative braking, engine start-stop systems, and energy recovery systems. Their capability to deliver quick energy bursts enhances their effectiveness in these roles. Furthermore, automakers are now exploring hybrid energy storage solutions, merging batteries with ultracapacitors for optimized performance.

With the surge in renewable energy projects, the demand for efficient energy storage and grid stability solutions has intensified. Ultracapacitors play a pivotal role by storing excess energy during peak production and releasing it during low generation periods, thus aiding grid stabilization. This functionality underscores their importance in renewable energy systems, particularly in wind and solar power.

Ongoing research and development efforts aim to boost the energy density of ultracapacitors, allowing them to rival conventional batteries. Material innovations, especially with graphene and carbon nanotubes, promise enhanced storage capacity without compromising on high power output and rapid charging. A notable example is EnyGy, a Melbourne-based company, which in 2023 unveiled an ultracapacitor leveraging cutting-edge graphene technology.

However, supercapacitors have limitations in long-term energy storage. Their discharge rate surpasses that of lithium-ion batteries, leading to a self-discharge loss of 10-20 percent daily. While batteries maintain a near-constant voltage until depleted, capacitors experience a linear decline in voltage with charge.

Global pushes for cleaner energy and stringent environmental regulations have created a conducive atmosphere for the ultracapacitor market. Policies aimed at reducing carbon emissions and promoting electric vehicles and renewable energy adoption have bolstered market growth. Moreover, both government and private sector investments in research and development, particularly in energy storage technologies, have accelerated the evolution of advanced ultracapacitors.

Ultracapacitor Market Trends

Automotive and Transportation Sector Experiencing Demand

The swift rise in the adoption of electric and hybrid vehicles has significantly driven up the demand for ultracapacitors. Unlike conventional batteries, ultracapacitors boast a high power density, enabling rapid charging and discharging. This makes them particularly suited for applications like regenerative braking and start-stop systems. Supercap technologies are being extensively utilized in regenerative braking test rigs, capitalizing on the challenges and opportunities presented by supercapacitor implementation. Their remarkable power density and cycling characteristics make them highly desirable.

For example, Skeleton Technologies' supercapacitors are featured in the Honda CR-V Hybrid Racer. This demonstration vehicle highlights the prowess of Honda Performance Development and showcases Honda's 2023 IndyCar hybrid power unit technology. Thanks to Skeleton's supercapacitors, the race car enjoys enhanced high-power performance. These supercapacitors are touted as the perfect solution for braking energy recovery and boosting acceleration. They come with notable advantages: low internal resistance, high cyclability, and excellent aging resistance.

Researchers at KAIST (Korea Advanced Institute of Science and Technology) have unveiled an innovative energy storage solution. This new system merges the strengths of supercapacitors with the cost-effectiveness and supply chain benefits of sodium-ion battery chemistry. The research team envisions their creation making waves in the electric vehicle sector. Their novel battery integrates an advanced anode with a cathode tailored for supercapacitor technology. This synergy enables the battery to boast both impressive storage capacities and swift charge-discharge rates, positioning it as a formidable contender against lithium-ion batteries.

In the U.S., three primary fast-charging standards dominate: CHAdeMO, Combined Charging System (CCS), and the North American Charging Standard (previously Tesla's standard). Among these, the CCS method leads in the number of fast-charging stations. Data from the U.S. Department of Energy reveals that in 2024, there were 7,315 CCS stations, 5,720 CHAdeMO stations, and 2,280 NACS stations. This expanding infrastructure bolsters the growing use of ultracapacitors in electric vehicles.

Ultracapacitors are carving out a pivotal role in energy recovery systems, especially in public transport realms like electric buses, trams, and high-speed trains. A key challenge in the automotive industry is sourcing components that can endure high-cycle usage without substantial wear. Ultracapacitors shine in this domain, effortlessly handling millions of charge and discharge cycles with minimal degradation. As the industry leans more towards electrification, fuel efficiency, and sustainability, the significance of ultracapacitors is poised to grow.

Asia-Pacific Region is Driving the Market

China, Japan, and South Korea lead the charge in electric vehicle production, bolstered by their established automotive industries that heavily invest in innovative energy storage solutions. The region's rapid expansion of EV infrastructure, coupled with a strong push towards sustainable transportation, is set to propel the market further.

Beyond electric vehicles, the Asia-Pacific region is a significant player in renewable energy investments. With countries like China and India intensifying their solar and wind energy projects, the demand for energy storage solutions has surged. Research from Carbon Brief highlights this trend, noting a 40% year-on-year rise in clean-energy investments, totaling USD 890 billion in 2023. This growth accounted for the entirety of the investment surge across China's economy. Ultracapacitors, known for their swift charging and discharging capabilities, are proving to be pivotal in stabilizing these renewable energy systems.

The Asia-Pacific region, renowned for its strong manufacturing base and technological advancements, is channeling its focus on research and development. Backed by substantial investments, this emphasis has not only enhanced ultracapacitor performance but also broadened their applications across diverse sectors, from consumer electronics to industrial machinery.

In a significant leap for electronics manufacturing, India inaugurated its first supercapacitor manufacturing plant in Kannur, Kerala in October 2024. This facility aims to produce top-tier supercapacitors for various sectors, including the Indian defense, electric vehicles, and even space missions.

Government initiatives, targeting a reduction in carbon emissions and championing green energy solutions, have catalyzed the swift adoption of ultracapacitors. With incentives and subsidies bolstering EV production and renewable energy initiatives, the environment is ripe for the ultracapacitor market's growth.

Ultracapacitor Industry Overview

The ultracapacitor market is fiercely competitive, featuring both established multinational corporations and emerging players that prioritize technological innovation and market expansion. Notable players in this arena include Maxwell Technologies, Skeleton Technologies, LS Mtron Ltd, and Eaton Corporation. These companies have cemented their positions through a robust global footprint, comprehensive R&D capabilities, and a wide array of product offerings.

Competition intensifies with rising demand from sectors like automotive, renewable energy, and industrial applications. Major players are bolstering their R&D efforts, securing investments, and raising funds to solidify their market positions and broaden their product ranges. For example, in October 2023, Skeleton Technologies secured EUR 108M in funding, aimed at fast-tracking the development of next-gen products and expanding supercapacitor manufacturing.

In the ultracapacitor market, continuous R&D is paramount for gaining a competitive edge. Companies are delving into advanced materials, such as carbon nanotubes and graphene, to boost energy density and cut costs. Looking ahead, the market is poised for heightened competition, focusing on technological breakthroughs, cost efficiency, and adapting to the dynamic energy demands of key industries.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 An Assessment of Impact of Macroeconomic Trends on The Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand for Energy-Efficient Solutions

5.1.2 Growing Electric Vehicle (EV) Market

5.1.3 Advancements in Renewable Energy Systems

5.2 Market Restraints

5.2.1 High Initial Cost

5.2.2 Lower Energy Density Compared to Battery

6 MARKET SEGMENTATION

6.1 By Type

6.1.1 Electrostatic Ultracapacitors

6.1.2 Pseudocapacitors

6.1.3 Hybrid Capacitors

6.2 By End User Vertical

6.2.1 Automotive and Transportation

6.2.2 Consumer Electronics

6.2.3 Energy and Power

6.2.4 Industrial Manufacturing

6.2.5 Aerospace and Defense

6.2.6 Others

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia

6.3.4 Australia and New Zealand

6.3.5 Latin America

6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Skeleton Technologies

7.1.2 Maxwell Technologies

7.1.3 CAP-XX

7.1.4 SPEL TECHNOLOGIES PRIVATE LTD.

7.1.5 LS Mtron Co., Ltd.

7.1.6 IOXUS

7.1.7 Nippon Chemi-Con Corporation

7.1.8 Shanghai Aowei Technology Development Co., Ltd