중동 및 북아프리카의 이차 전지 시장 전망 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Middle-East And North Africa Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636569

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

중동 및 북아프리카의 이차 전지 시장 규모는 2025년에 57억 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 8.9%로, 2030년에는 87억 2,000만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기차의 보급 확대, 신재생에너지 도입 확대, 리튬 이온 배터리의 가격 하락이 예측 기간 중 중동 및 북아프리카의 이차 전지 시장을 주도할 것으로 예상됩니다.

반대로 원료 수요 및 공급 불일치는 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

그러나 새로운 배터리 기술의 진보, 혁신적인 배터리 화학, 배터리 재활용의 중요성 증가는 중동과 북아프리카의 이차 배터리 시장에 큰 기회를 제공 할 준비가 되어 있습니다.

아랍에미리트(UAE)은 전기차 판매량의 급증과 재생가능 에너지 도입 증가에 따라 이차 전지 시장에서 현저한 성장을 이루고 있습니다.

중동 및 북아프리카의 이차 전지 시장 동향

리튬 이온 배터리가 급성장

다양한 배터리기술 중 리튬 이온 배터리(LIB)가 중동 및 북아프리카의 이차전지 시장에서 예측 기간 중 가장 급성장하는 부문으로 부상할 전망입니다. LIB는 유리한 용량 대비 중량비로 인해 다른 배터리를 능가하는 인기를 모으고 있습니다. 리튬 이온 배터리의 채택은 뛰어난 성능(긴 수명, 낮은 유지보수 포함), 우수한 보존 가능 기간, 현저한 가격 저하 등의 이점에 의해 더욱 촉진되고 있습니다.

리튬 이온 배터리는 납 배터리와 같은 대체품에 비해 몇 가지 기술적 이점을 자랑합니다. 평균적으로 리튬 이온 이차 전지는 5,000회 이상의 사이클을 제공하며 이는 일반적인 납 배터리의 400-500회와는 대조적입니다. 또한 리튬 이온 배터리는 유지 보수 및 교체 빈도가 적습니다. 또한 방전 사이클을 통해 일정한 전압을 유지하기 때문에 전기 부품의 효율성이 오래 지속됩니다.

최근 이 산업의 주요 업계에서는 연구 개발과 규모의 경제 투자를 강화하고 경쟁을 심화시켜 리튬 이온 배터리의 가격을 인하하고 있습니다. 기술 혁신, 제조 강화, 원료 비용 저하로 리튬 이온 배터리의 부피가중 평균가격은 2013년 780달러/kWh에서 2023년 139달러/kWh로 급락했습니다. 2025년에는 113달러/kWh, 2030년에는 80달러/kWh까지 더욱 하락할 것으로 예측되고 있습니다. 이러한 배터리 비용의 하락 추세는 리튬 이온 배터리를 점점 매력적인 옵션으로 자리매김하고 있습니다.

역사적으로 리튬 이온 배터리의 주요 용도는 휴대폰 및 노트북과 같은 가전 제품이었습니다. 그러나 그 역할은 크게 확대되고 있습니다. 현재 하이브리드 자동차, 배터리 전기자동차(BEV)의 모든 시리즈, 재생 가능 에너지 부문의 배터리 에너지 저장 시스템(BESS)의 전원으로 선호되고 있습니다.

중동과 북아프리카의 리튬 이온 배터리 제조 산업은 아직 초기 단계에 있으며, 중국, 미국, 유럽 등 세계 선두 주자에 는뒤처지고 있지만, 이 부문을 강화하기위한 협조적인 노력이 이루어지고 있습니다. 특히 아랍에미리트(UAE)과 사우디아라비아는 배터리 제조 및 관련 기술에 대한 투자를 추진하고 있습니다. 이 움직임은 경제를 다양화하고, 재생 가능 에너지의 목표를 지원하고, 급증하는 전기자동차 수요에 대응하기 위한 것입니다.

예를 들어, Titan Lithium은 2024년 2월 Khalifa Economic Zones Abu Dhabi(KEZAD) 그룹과 제휴하여 최첨단 리튬 가공 시설 계획을 발표했습니다. KEZAD Al Mamourah의 290,000 평방미터로 퍼지는 이 50억 AED 벤처는 리튬 이온 배터리와 EV 부문에 필수적인 배터리 등급의 탄산 리튬과 수산화 리튬의 생산을 목표로 하고 있습니다.

마찬가지로, 사우디아라비아는 세계의 이차 전지 부문에서 진전을 이루고 있습니다. 2023년 6월 Obeikan Investment Group은 호주의 신흥 기업인 European Lithium과 제휴하여 수산화리튬 정제소를 설립했습니다. 그 다음 달에는 사우디아라비아 국영 광업 기업인 마아덴과 미국의 Ivanhoe Electric이 Arabian Shield의 48,500 평방 킬로미터에서 리튬 및 기타 희귀 금속을 탐사하는 계약을 체결했습니다.

2023년 9월 사우디 투자회사인 에너지캐피탈 그룹은 미국의 첨단 신흥기업인 퓨어 리튬과 협력하여 유전 염수에서 추출한리튬을 사용하는 배터리를 개발했습니다. 초기 투자 5,000만 달러의 이 벤처는 리튬 이온 배터리용 금속의 급증하는 수요에 대응하기 위한 것입니다. 게다가 ERG의 Global Battery Alliance 가입은 리튬 이온 배터리의 지속 가능한 세계 공급망에 대한 노력을 강조합니다. 이러한 정책적 노력은 이 지역의 리튬 이온 배터리 산업에 유망한 궤도를 보여줍니다.

정리하면, 경량 설계, 급속 충전, 충전 주기 연장, 비용 저하, 리튬 이온 배터리 부문의 진보 등의 특성으로 리튬 이온 배터리는 예측 기간 중 중동 및 북아프리카의 이차 전지 시장에서 가장 급성장하는 배터리 기술로 자리매김하고 있습니다.

현저한 성장을 이룬 아랍에미리트(UAE)

예측 기간 동안 아랍에미리트(UAE)의 이차 전지 시장은 크게 성장하고 지역 리더로 자리매김할 것으로 전망됩니다. 이 추세는 급속한 산업화, 신재생에너지에 대한 정부의 지원, 급성장하는 전기자동차(EV) 부문, 기술적 진보, 아랍에미리트(UAE)의 지역 내에서의 전략적 경제적 지위가 뒷받침하고 있습니다. 이러한 요소를 종합하면 아랍에미리트(UAE)에서 이차 전지를 채택하고 혁신을 위한 비옥한 토양을 조성하고 있습니다.

아랍에미리트(UAE)의 급속히 산업화에 따라 신뢰할 수 있는 에너지 저장 솔루션에 대한 수요가 급증하고 다양한 부문에서 이차 전지의 보급이 진행되고 있습니다. 게다가 지속가능성과 재생가능에너지에 힘을 쏟고 있으며, 특히 이산화탄소 배출량을 줄이고 에너지 포트폴리오에서 재생가능에너지가 차지하는 비율을 늘리려고 하기 때문에 중추적인 역할을 할 것으로 보입니다. 이러한 변화는 태양광 발전으로 대표되는 청정 에너지 기술을 지지하는 정부의 지원에 의해 강화되고 있습니다. 이러한 변화는 효율적인 배터리 에너지 저장 시스템(BESS)에 대한 수요를 증가시키고 이차 배터리 시장을 뒷받침하고 있습니다. 예를 들어, 아랍에미리트(UAE)은 야심찬 에너지 목표를 설정하고 있으며, 재생 가능 에너지 용량을 2023년 약 605만kW에서 2030년까지 1420만kW로 현재의 3배 이상으로 끌어올리는 것을 목표로 하고 있습니다. 이 목표는 BESS에 대한 큰 수요를 창출하는 할 것으로 예상됩니다.

최근 몇 년동안 아랍에미리트(UAE)에서는 전기자동차(EV)가 빠르게 확산되고 있습니다. 국제에너지기구(IEA)의 데이터는 이 추세를 잘 보여주고 있습니다. 배터리 전기자동차(BEV)와 플러그인 하이브리드 전기자동차(PHEV)를 포함한 아랍에미리트(UAE)의 EV 판매량은 2023년 약 2만 8,900대로 급증하며 2022년 약 1만 8,900대에서 50% 증가했습니다. 이러한 EV 보급 증가는 이차 전지 시장을 강화할 것으로 예상됩니다.

또한 아랍에미리트(UAE)은 2050년까지 전기자동차와 하이브리드 자동차가 도로를 달리는 모든 차량의 50%를 차지할 것으로 예상했습니다. 기후 변화의 완화와 화석연료에 대한 의존도를 줄이는 것을 목적으로 하는 EV 인프라에의 다액의 투자와 EV 도입의 추진에 의해 고용량, 내구성이 높은 이차 전지 수요가 높아지고 있습니다.

배터리 수요가 급증함에 따라 아랍에미리트(UAE)에서는 배터리 재활용도 진행되고 있습니다. 2023년 12월 인도 LOHUM Cleantech가 아랍 에미리트 최초의 EV 배터리 재활용 공장 설립 계획을 발표했습니다. 아랍에미리트(UAE)의 에너지 인프라와 중동의 지속가능성과 디지털화 리더인 중동과의 협력을 통한 이 사업은 아랍에미리트(UAE)의 COP28 의제, 2050년까지 탄소 배출 제로 전략, 순환 경제 시책에 합치하고 있습니다. 이 노력 또한 첨단 솔루션을 통해 배기 가스 배출 없는 이동성을 지지합니다.

이 야심찬 프로젝트는 리튬 배터리 재생 및 재활용에 특화된 80,000 평방 피트의 광대한 시설을 특징으로합니다. 이 시설에서는 연간 3,000톤의 리튬 이온 배터리를 재활용하고 15MWh의 배터리용량을 에너지 저장 시스템(ESS)으로 변환할 계획입니다. 이러한 생산량은 예상되는 EV 배터리 관리 요구의 80% 이상을 충족할 것으로 예상됩니다.

배터리 기술의 발전, 특히 솔리드 스테이트 배터리의 출현은 소비자와 기업 모두에게 이차 전지의 효율성, 안전성 및 종합적인 매력을 높여줍니다. 이 추세의 증거로 미국에 본사를 둔 Statevolt는 2024년 4월 2026년까지 아랍에미리트(UAE)에서 고체 배터리 셀을 생산할 목표를 발표했습니다. 이 회사는 라스 알하이마에 32억 달러의 기가팩토리를 건설하고 연간 생산량 40기가와트(GWh)를 목표로 하고 있습니다. 이는 중동 전역에서 급성장하고 있는 배터리 저장과 전기 자동차의 수출 시장을 주시한 것으로, 아프리카와 인도에까지 퍼지고 있습니다.

이러한 움직임으로 아랍에미리트(UAE)은 예측 기간 중 중동과 북아프리카의 이차 전지 시장에서 지배적인 지위를 차지할 것으로 예상됩니다.

중동 및 북아프리카의 이차 전지 산업 개요

중동 맟 북아프리카의 이차 전지 시장은 세분화되고 있습니다. 이 시장의 주요 기업(무순서)에는 Tesla Inc., Exide Industries Ltd., Middle East Battery Company(MEBCO), EnerSys, Panasonic Holdings Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

전기자동차의 보급 확대

신재생에너지 도입 증가

억제요인

원료의 수급 미스매치

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자분석

제5장 시장 세분화

기술

납 배터리

리튬 이온

기타 기술(NiMh, Nicd 등)

용도

자동차용 전지

산업용 전지(동력용, 거치형(텔레콤, UPS, 에너지 저장 시스템(ESS) 등))

휴대용 배터리(가전 제품 등)

기타

지역

아랍에미리트(UAE)

사우디아라비아

이집트

알제리

기타 중동아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Panasonic Holdings Corporation

Tesla Inc.

Saft Groupe SA

Middle East Battery Company(MEBCO)

EnerSys

Exide Industries Ltd

FIAMM Energy Technology SpA

Statevolt

Statron Ltd

Amara Raja Energy & Mobility Limited.

C&D Technologies Inc.

United Batteries Co.

Chloride Egypt SAE

기타 저명한 기업 일람

시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

새로운 배터리 기술과 선진 배터리 화학의 개발의 진전

HBR

영문 목차

영문목차

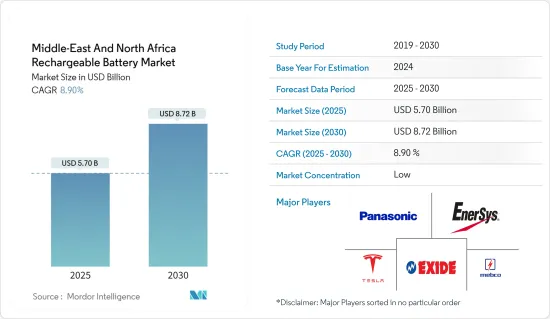

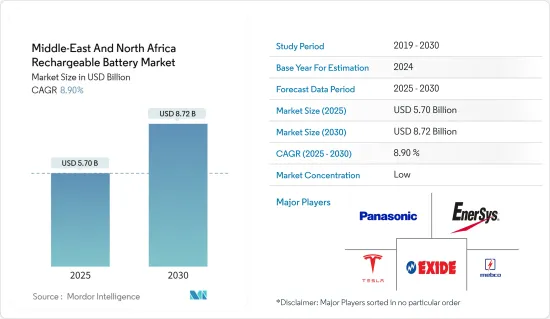

The Middle-East And North Africa Rechargeable Battery Market size is estimated at USD 5.70 billion in 2025, and is expected to reach USD 8.72 billion by 2030, at a CAGR of 8.9% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing adoption of electric vehicles, rising adoption of renewable energy, and declining lithium-ion battery prices are expected to drive the Middle East and North Africa rechargeable battery market during the forecast period.

Conversely, a mismatch between the demand and supply of raw materials is anticipated to impede the market's growth during the forecast period.

However, advancements in new battery technologies, innovative battery chemistries, and an increasing emphasis on battery recycling are poised to offer substantial opportunities for the rechargeable battery market in the Middle East and North Africa.

The United Arab Emirates is set to experience notable growth in the rechargeable battery market, driven by surging electric vehicle sales and a growing adoption of renewable energy in the region.

Middle-East And North Africa Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

Among various battery technologies, lithium-ion batteries (LIBs) are poised to emerge as the fastest-growing segment in the rechargeable battery market of the Middle East and North Africa during the forecast period. LIBs are outpacing other battery types in popularity due to their favorable capacity-to-weight ratio. Their adoption is further fueled by advantages like superior performance (including extended life and low maintenance), an impressive shelf life, and a notable decrease in prices.

Li-ion batteries boast several technical advantages over alternatives like lead-acid batteries. On average, rechargeable Li-ion batteries offer over 5,000 cycles, a stark contrast to the 400-500 cycles typical of lead-acid batteries. Moreover, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for electrical components.

In recent years, major industry players have ramped up investments in R&D and economies of scale, intensifying competition and driving down lithium-ion battery prices. Thanks to technological innovations, manufacturing enhancements, and falling raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further dip to around USD 113/kWh by 2025 and an ambitious USD 80/kWh by 2030. Such trends in declining battery costs position lithium-ion batteries as an increasingly attractive option.

Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. Yet, their role has expanded significantly. Today, they're the preferred power source for hybrids, the entire range of battery electric vehicles (BEVs), and battery energy storage systems (BESS) in the renewable energy sector.

While the Middle East and North Africa's lithium-ion battery manufacturing industry is still in its nascent stages, trailing behind global frontrunners like China, the United States, and Europe, there's a concerted effort to bolster this sector. Countries, especially the UAE and Saudi Arabia, are channeling investments into battery manufacturing and related technologies. This move aims to diversify their economies, support renewable energy goals, and cater to the surging demand for electric vehicles.

For instance, in February 2024, Titan Lithium, in partnership with Khalifa Economic Zones Abu Dhabi (KEZAD) Group, unveiled plans for a state-of-the-art lithium processing facility. This AED 5 billion venture, sprawling over 290,000 square meters in KEZAD Al Mamourah, aims to produce battery-grade lithium carbonate and hydroxide, essential for the lithium-ion battery and EV sectors.

Similarly, Saudi Arabia is making strides in the global rechargeable battery arena. In June 2023, Obeikan Investment Group teamed up with Australian startup European Lithium to establish a lithium hydroxide refinery. The following month, Saudi state mining giant Ma'aden and US-based Ivanhoe Electric struck a deal to explore 48,500 sq km of the Arabian Shield for lithium and other rare metals.

In September 2023, Energy Capital Group, a Saudi investment firm, collaborated with US tech startup Pure Lithium to pioneer batteries using lithium sourced from oilfield brines. With an initial investment of USD 50 million, this venture aims to address the burgeoning demand for lithium-ion battery metals. Additionally, ERG's membership in the Global Battery Alliance underscores its commitment to a sustainable global supply chain for lithium-ion batteries. Such initiatives signal a promising trajectory for the region's lithium-ion battery industry.

In summary, attributes like lightweight design, rapid charging, extended charging cycles, decreasing costs, and advancements in the lithium-ion battery sector position it as the fastest-growing battery technology in the Middle East and North Africa's rechargeable battery market during the forecast period.

United Arab Emirates to Witness Significant Growth

During the forecast period, the rechargeable battery market in the United Arab Emirates (UAE) is poised for substantial growth, positioning it as a regional leader. This momentum is fueled by rapid industrialization, government backing for renewable energy, a burgeoning electric vehicle (EV) sector, technological strides, and the UAE's strategic economic stature in the region. Collectively, these elements foster a fertile ground for the adoption and innovation of rechargeable batteries in the UAE.

As the UAE industrializes swiftly, the demand for dependable energy storage solutions surges, driving the uptake of rechargeable batteries across diverse sectors. Moreover, the UAE's dedication to sustainability and renewable energy is set to play a pivotal role, especially as the nation seeks to curtail its carbon emissions and amplify the proportion of renewables in its energy portfolio. This shift is bolstered by governmental initiatives championing clean energy technologies, notably solar power. Such efforts amplify the demand for efficient battery energy storage systems (BESS), thereby propelling the rechargeable battery market. Illustratively, the UAE has set ambitious energy targets, aiming to elevate its renewable energy capacity from approximately 6.05 GW in 2023 to a robust 14.2 GW by 2030, more than tripling its current capacity. This ambitious goal is poised to generate a substantial demand for BESS.

In recent years, the UAE has witnessed a swift embrace of electric vehicles (EVs). Data from the International Energy Agency (IEA) highlights this trend: EV sales in the UAE, encompassing both Battery Electric Vehicles (BEV) and Plug-in Hybrid Electric Vehicles (PHEV), surged to roughly 28,900 units in 2023, marking a 50% increase from 2022's tally of about 18,900 units. Such a rising tide in EV adoption is anticipated to bolster the rechargeable battery market.

Moreover, the UAE envisions electric and hybrid vehicles constituting 50% of all vehicles on its roads by 2050. With substantial investments in EV infrastructure and a push for EV adoption-aimed at mitigating climate change and reducing fossil fuel dependence-the demand for high-capacity, durable rechargeable batteries is escalating.

In tandem with the surging battery demand, the UAE is making strides in battery recycling. A notable development occurred in December 2023, when LOHUM Cleantech, an Indian firm, unveiled plans to establish the UAE's inaugural EV Battery Recycling plant. This venture, in collaboration with the UAE's Ministry of Energy & Infrastructure and BEEAH-a leader in sustainability and digitalization in the Middle East-aligns with the UAE's COP28 agenda, its Net Zero by 2050 Strategic Initiative, and its Circular Economy Policy. The initiative also champions emissions-free mobility with forward-thinking solutions.

The ambitious project will feature an expansive 80,000 sq ft facility dedicated to refurbishing and recycling lithium batteries. Annually, this facility is set to recycle 3,000 tons of lithium-ion batteries and convert 15MWh of battery capacity into Energy Storage Systems (ESS). Such output is projected to satisfy over 80% of the anticipated EV battery management needs.

Advancements in battery technology, particularly the emergence of solid-state batteries, are boosting the efficiency, safety, and overall appeal of rechargeable batteries for both consumers and businesses. A testament to this trend, in April 2024, US-based Statevolt announced its intent to produce solid-state battery cells in the UAE by 2026. The company is laying the groundwork for a USD 3.2 billion gigafactory in Ras Al Khaimah, targeting an annual output of 40 gigawatt-hours (GWh). This initiative eyes the burgeoning export markets for battery storage and electric mobility across the Middle East, extending to Africa and India.

Given these dynamics, the United Arab Emirates (UAE) is set to emerge as a dominant player in the rechargeable battery landscape of the Middle-East and North Africa during the forecast period.

Middle-East And North Africa Rechargeable Battery Industry Overview

The Middle-East and North Africa rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Tesla Inc., Exide Industries Ltd., Middle East Battery Company (MEBCO), EnerSys and Panasonic Holdings Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Adoption of Electric Vehicles

4.5.1.2 Growing Renewable Energy Installation

4.5.2 Restraints

4.5.2.1 Demand-Supply Mismatch of Raw Materials

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Technology

5.1.1 Lead-Acid

5.1.2 Lithium-Ion

5.1.3 Other Technologies (NiMh, Nicd, etc.)

5.2 Application

5.2.1 Automotive Batteries

5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)