유럽의 이차 전지 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636533

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

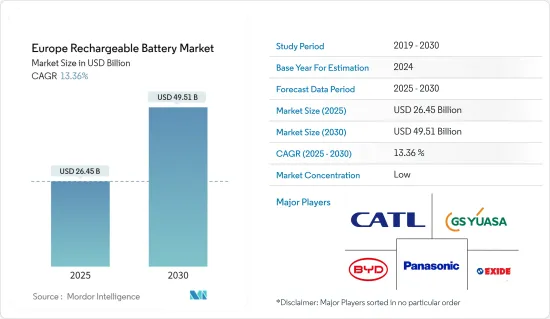

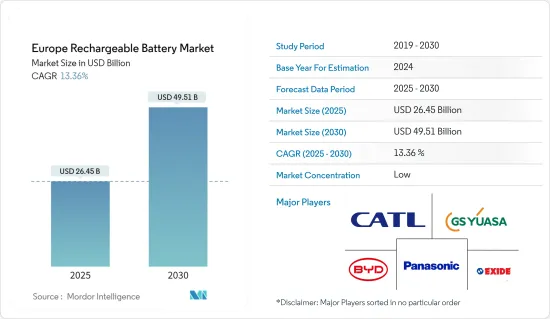

유럽의 이차 전지 시장 규모는 2025년에 264억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장률(CAGR)은 13.36%로, 2030년에는 495억 1,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기차 수요 증가와 재생가능에너지 채택 확대 등의 요인이 예측기간 중 유럽의 이차 전지 시장의 주요 촉진요인이 될 것으로 예상됩니다.

반대로, 배터리 조달에서 큰 공급망의 제약은 예측 기간 동안 유럽의 아차 배터리 시장을 위협할 수 있습니다.

그러나 배터리화학 개발의 지속적인 발전은 보다 효율적인 이차 전지를 생산하고 시장에 많은 미래 기회를 가져오고 있습니다.

독일이 시장을 선도하는 태세를 갖추고 있으며, 급성장하고 있는 소비자용 전자기기 부문와 신속한 재생 가능 에너지 도입이 원동력이 되어 예측 기간 중에 가장 높은 성장을 달성할 것으로 예측되고 있습니다.

유럽의 이차 전지 시장 동향

자동차가 크게 성장

최근 유럽연합(EU)은 온실가스의 배출을 줄이고 보다 청정한 에너지 기술을 지역 전체에 보급하는 것을 목적으로 엄격한 조치를 실시했습니다. 이러한 정책은 또한 운송 부문에서도 전기화 추진을 강조합니다. EU 내 각국도 이러한 노력을 반영하고 전기자동차(EV) 도입을 촉진하기 위한 세제 우대조치와 보조금을 제공하는 시책을 전개하고 있습니다. 그 결과 전기자동차의 주요 부품인 이차 전지 수요 급증이 예상됩니다.

게다가 환경의 지속가능성을 둘러싼 인식의 고조와 화석연료 의존으로부터의 벗어나려는 움직임이 소비자의 기호를 환경친화적인 수송으로 옮겨가고 있습니다. 배출 가스가 없는 전기자동차는 기존의 내연 엔진 차량을 대체할 수 있는 지속 가능한 옵션으로 간주됩니다. 이러한 소비자의 EV 선호 증가는 유럽에서 이차 전지 시장의 성장을 가속할 것으로 예상됩니다.

국제에너지기구(IEA)의 데이터에 따르면 유럽 전역에서 전기차 판매량이 꾸준히 증가하고 있습니다. 2023년 판매량은 약 220만대에 달했으며, 2021년 160만대에서 현저하게 증가하며 성장률은 37.5%를 넘었습니다. 이러한 추세는 전기자동차의 급속한 보급을 뒷받침하는 것으로, 이차 전지 시장을 더욱 활성화시킵니다.

또한 배터리 기술의 지속적인 기술 발전으로 전기자동차의 에너지 밀도 향상, 항속 거리 연장, 충전 시간 단축 등의 기능 강화가 이루어지고 있습니다. 이러한 발전은 특히 새로운 배터리 제조 시설의 설립과 같은 유럽 전역의 투자 증가에 박차를 가하고 있습니다.

예를 들어, 2023년 7월 인도의 유명한 자동차 제조업체인 Tata Motors는 영국에 연간 셀 생산 능력 40GW의 전기자동차 배터리 공장을 건설할 계획을 발표했습니다. 이 시설은 배터리 생산을 현지화함으로써 국내 자동차 산업을 강화하고 장기적인 지속가능성을 확보하기 위함입니다. 타타 모터스와 정부 관계자는 모두 이 공장에 40억 파운드의 대규모 투자를할 것이라고 밝혔습니다.

이러한 개발을 근거로 자동차 산업의 전기자동차 부문은 향후 수년간 크게 성장하게 될 것입니다.

시장을 독점하는 독일

독일은 산업 및 제조의 중심지로서의 지위와 강력한 자동차 산업에 의해 유럽의 이차 전지 시장을 리드할 준비를 갖추고 있습니다. 이 산업은 세계의 에너지 전환에 발맞춰 혁신적인 전기자동차로 방향을 전활하고 있습니다. 유럽의 전기자동차에 대한 수요가 높아짐에 따라 독일 자동차 제조업체는 이차 전지 수요를 크게 늘려 이 부문에서 독일의 리더십을 공고히 할 예정입니다.

게다가 독일은 신재생에너지 발전의 도입에 힘을 쏟고 있기 때문에 이차전지의 요구가 높아지고 있습니다. 신재생에너지원의 간헐적인 특징을 고려하면 에너지 저장 장치가 필수적입니다. 전지 에너지 저장 시스템의 채택이 증가함에 따라, 독일의 재생 가능 에너지 부문은 이차 전지 수요를 더욱 촉진하고 있습니다.

국제에너지기구의 데이터에 따르면 독일의 재생 가능 에너지의 신속한 수용을 강조합니다. 국가의 재생 가능 에너지 설비 용량은 2022년부터 2023년에 걸쳐 약 12% 급증하여 5년간 일관된 평균 성장률 5.6% 이상을 상회할 것으로 전망됩니다.

게다가 독일은 정부와 민간기업 모두에서 엄청난 투자를 통해 전지의 연구개발에 있어 리더가 되고 있습니다. 국내 연구기관과 기업은 에너지 밀도, 충전 속도, 전반적인 효율성 향상에 중점을 두고 배터리 기술의 한계에 도전하고 있습니다.

그 예로, 2024년 5월 독일의 유명한 배터리 공급업체인 Varta는 산업 규모의 나트륨 이온 이차 전지 기술을 개척하기 위한 프로젝트를 시작했습니다. 3년 동안 750만 유로(808만 달러)를 투자하여 셀 화학을 산업 규모로 끌어올리는 것을 목표로 합니다. 목표는 전기자동차 및 거치형 저장장치에 적합한 원형 셀을 한정된 수량으로 생산하는 것입니다. 이 프로젝트는 2027년 중반까지 완료될 예정이며, 기술적, 경제적, 생태학적 철저한 평가를 거치게 됩니다.

이러한 발전을 고려할 때, 예측 기간 동안 유럽의 이차 전지 시장에서 독일의 지배력은 확실하다고 생각됩니다.

유럽의 이차 전지 산업 개요

유럽의 이차 전지 시장은 세분화되어 있습니다. 이 시장의 주요 기업(무순서)에는 BYD, Contemporary Amperex Technology, Exide Industries, Panasonic Corporation, GS Yuasa Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

전기자동차 수요 증가

재생 가능 에너지의 보급 확대

억제요인

공급망의 제약

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형

납산

리튬 이온

기타(NiMh, NiCd 등)

용도

자동차용

산업용 전지

휴대용 전지

기타

지역

독일

프랑스

영국

이탈리아

스페인

노르딕

러시아

터키

기타 유럽

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

BYD Co. Ltd.

LG Chem Ltd.

Contemporary Amperex Technology Co Ltd

Exide Industries

Saft Groupe SA

Samsung SDI Co., Ltd.

Murata Manufacturing Co., Ltd.

Panasonic Corporation

GS Yuasa Corporation

Tesla, Inc.

기타 저명한 기업 일람

시장 랭킹,공유 분석

제7장 시장 기회와 앞으로의 동향

새로운 배터리 화학의 기술적 발전

HBR

영문 목차

영문목차

The Europe Rechargeable Battery Market size is estimated at USD 26.45 billion in 2025, and is expected to reach USD 49.51 billion by 2030, at a CAGR of 13.36% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as increasing demand for electric vehicles and growing adoption of renewable energy are expected to be among the most significant drivers for the Europe rechargeable battery market during the forecast period.

Conversely, high supply chain constraints in battery procurement threaten the European rechargeable battery market during the forecast period.

However, ongoing advancements in battery chemistry development have resulted in more efficient rechargeable batteries, presenting numerous future opportunities for the market.

Germany is poised to lead the market and is projected to achieve the highest growth during the forecast period, driven by a burgeoning consumer electronics segment and swift renewable energy installations.

Europe Rechargeable Battery Market Trends

Automobile to Witness Significant Growth

In recent years, the European Union has implemented stringent measures aimed at curbing greenhouse gas emissions and promoting cleaner energy technologies across the region. These initiatives also emphasize a heightened electrification push within the transportation sector. Individual countries within the EU have mirrored these efforts, rolling out policies that offer tax incentives and subsidies to bolster the adoption of electric vehicle (EV). Consequently, this has led to an anticipated surge in demand for rechargeable batteries, a pivotal component of electric vehicles.

Additionally, heightened awareness surrounding environmental sustainability and a collective move away from fossil fuel reliance has shifted consumer preferences towards eco-friendly transportation. Electric vehicles, with their zero direct emissions, are increasingly viewed as a sustainable alternative to traditional internal combustion engine vehicles. This rising consumer inclination towards EVs is poised to propel the rechargeable battery market's growth in Europe.

Data from the International Energy Agency highlights a consistent uptick in electric vehicle sales across Europe. In 2023, sales reached approximately 2.2 million units, a notable increase from 1.6 million units in 2021, marking a growth rate exceeding 37.5%. Such momentum underscores the burgeoning traction of electric vehicles, further fueling the rechargeable battery market.

Moreover, ongoing technological advancements in battery technology have ushered in enhancements like improved energy density, extended ranges, and expedited charging times for electric vehicles. These advancements have catalyzed increased investments across Europe, particularly in establishing new battery manufacturing facilities.

For example, in July 2023, Tata Motors, a prominent Indian automobile manufacturer, unveiled plans for a 40 GW annual cell production capacity electric vehicle battery plant in Britain. This facility is poised to fortify the domestic car industry by localizing battery production, ensuring long-term sustainability. Both Tata Motors and government officials disclosed a hefty investment of GBP 4 Billion for the factory.

Given these developments, the electric vehicle segment of the automobile industry is set for substantial growth in the coming years.

Germany to Dominate the Market

Germany is poised to lead the European rechargeable battery market, bolstered by its status as an industrial and manufacturing hub and a strong automobile industry. This industry is pivoting towards innovative electric vehicles, aligning with the global energy transition. As Europe's appetite for electric vehicles grows, German automakers are set to significantly boost the demand for rechargeable batteries, solidifying Germany's leadership in this segment.

Furthermore, Germany's dedication to incorporating renewable energy into its power generation amplifies its need for rechargeable batteries. Given the intermittent nature of renewable sources, energy storage becomes crucial to harness their full potential. With the rising adoption of battery energy storage systems, Germany's renewable energy sector is poised to further fuel the demand for rechargeable batteries.

Data from the International Renewable Energy Agency highlights Germany's swift embrace of renewables: the nation's installed renewable energy capacity surged by about 12% from 2022 to 2023, outpacing a consistent five-year average growth rate of over 5.6%.

Moreover, Germany is a leader in battery R&D, due to substantial investments from both government and private entities. Domestic research institutions and companies are pushing the envelope in battery technologies, emphasizing enhancements in energy density, charging speed, and overall efficiency.

As an illustration, in May 2024, Varta, a prominent German battery supplier, launched a project aimed at pioneering industrial-scale rechargeable sodium-ion battery technology. With a three-year investment of EUR 7.5 million (USD 8.08 million), the initiative seeks to elevate cell chemistry to an industrial scale. The goal is to produce a limited batch of round cells, tailored for electric vehicles and stationary storage. Set to wrap up by mid-2027, the project will undergo a thorough technical, economic, and ecological evaluation.

Given these developments, Germany's dominance in the European rechargeable battery market appears assured during the forecast period.

Europe Rechargeable Battery Industry Overview

The Europe Rechargeable Battery Market is fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Ltd., Exide Industries, Panasonic Corporation, and GS Yuasa Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Demand for Electric Vehicles

4.5.1.2 Growing Renewable Energy Penetration

4.5.2 Restraints

4.5.2.1 Supply Chain Constraints

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lead Acid

5.1.2 Lithium-Ion

5.1.3 Others (NiMh, NiCd, etc.)

5.2 Applications

5.2.1 Automobiles

5.2.2 Industrial Batteries

5.2.3 Portable Batteries

5.2.4 Other Applications

5.3 Geography

5.3.1 Germany

5.3.2 France

5.3.3 United Kingdom

5.3.4 Italy

5.3.5 Spain

5.3.6 NORDIC

5.3.7 Russia

5.3.8 Turkey

5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BYD Co. Ltd.

6.3.2 LG Chem Ltd.

6.3.3 Contemporary Amperex Technology Co Ltd

6.3.4 Exide Industries

6.3.5 Saft Groupe SA

6.3.6 Samsung SDI Co., Ltd.

6.3.7 Murata Manufacturing Co., Ltd.

6.3.8 Panasonic Corporation

6.3.9 GS Yuasa Corporation

6.3.10 Tesla, Inc.

6.4 List of Other Prominent Companies

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Advancements in New Battery Chemistry