ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

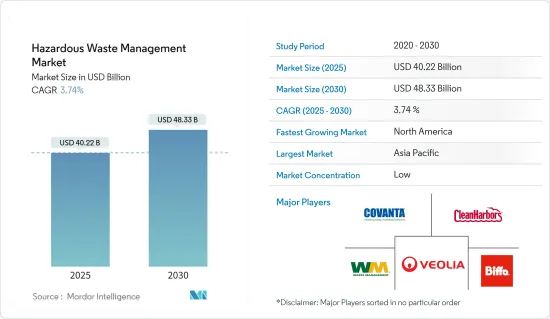

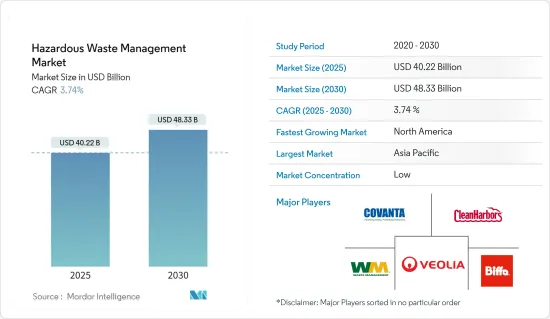

유해 폐기물 관리 시장 규모는 2025년에 402억 2,000만 달러로 추정되며, 예측기간 중(2025-2030년) 연평균 성장율(CAGR)은 3.74%로, 2030년에는 483억 3,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

유해 폐기물 관리에는 사람의 건강이나 환경을 위협하는 물질을 취급, 통제 및 폐기하는 관행과 절차가 포함됩니다. 여기에는 폐기물 수거, 재활용, 처리, 운송, 폐기 및 폐기장 모니터링이 포함됩니다. 주요 목표는 위험을 완화하고 건강과 환경을 보호하는 것입니다.

유해 폐기물 관리 시장은 여러 가지 요인에 의해 움직입니다. 전 세계 정부는 오염과 건강 위험에 대한 우려로 인해 폐기물 처리에 집중하고 있습니다. 이에 따라 폐기물 처리 관행을 관리하고 책임 있는 관리를 장려하기 위해 더 엄격한 규정이 제정되고 있습니다.

기술 발전으로 유해 폐기물 관리가 크게 강화되었습니다. 폐기물 처리 및 폐기 분야의 혁신으로 더욱 효율적이고 친환경적인 방법이 등장했습니다. 주목할 만한 기술로는 증기 멸균 처리, 화학 처리, 오존 처리, 열분해, 전자빔 기술 등이 있습니다. 예를 들어, Pello는 기업이 환경에 미치는 영향을 줄이고 폐기물 수거를 보다 효율적으로 관리할 수 있도록 개발된 새로운 기술입니다. Pello는 여러 가지 방법으로 기업이 이러한 목표를 달성할 수 있도록 지원합니다. 첫째, Pello 시스템은 쓰레기통의 가득 찬 수준을 모니터링하고 쓰레기통의 내용물과 위치에 대한 실시간 정보를 제공합니다.

2023년 4월, 리사이클 트랙 시스템즈(RTS)는 리사이클스마트 솔루션즈를 인수하여 첨단 폐기물 전환, 유기물 포집 및 재활용 관리 기술을 제공하는 캐나다 최고의 독립 공급업체로 입지를 굳혔습니다. 이번 인수에는 사물인터넷(IoT) 플랫폼의 필수 요소인 리사이클 스마트의 최첨단 Pello 폐기물 센서 기술이 포함되었습니다.

유해 폐기물 관리 시장 동향

아시아태평양이 앞으로 수년간 시장을 독점할 전망

중국, 인도, 동남아시아 국가들의 급속한 산업화로 인해 특히 제조, 광업, 전자 등의 산업에서 유해 폐기물 생산이 급증했습니다. 예를 들어, 중국은 1990년대 이후 폐기물 배출량이 3배 가까이 증가했습니다. 이러한 증가는 여러 가지 요인에 기인할 수 있습니다. 지난 수십 년 동안 중국의 도시화율은 꾸준히 상승했습니다. 중국 국가통계국의 데이터에 따르면 2023년에는 인구의 약 66.2%가 도시 지역에 거주할 것으로 예상됩니다.

국제통화기금(IMF)에 따르면 중국의 2023년 GDP가 약 17조 7천억 달러에 달할 것으로 예상되는 중국의 견고한 경제 성장은 산업 폐기물 생산량을 더욱 증가시켰습니다. 광미와 비산재와 같은 전통적인 산업 폐기물의 양은 안정적으로 유지되었지만, 산업 발전과 함께 유해 폐기물 생산량도 급증했습니다. 특히 이러한 유해 부산물은 안전한 처리를 위해 더욱 발전된 처리가 필요합니다. 2024년 3월, 제레 그룹은 그린웰 분산형 유해 폐기물 처리 장비를 도입하면서 중요한 이정표에 도달했습니다. 중앙 집중식 유해 폐기물 처리의 문제를 해결하기 위해 맞춤화된 이 혁신적인 솔루션은 중간 단계를 거치지 않고 현장에서 처리할 수 있습니다.

이 최첨단 장비는 현장 처리를 간소화하고 중간 단계를 제거함으로써 처리 효율성을 크게 향상시키고 폐기물을 줄이며 시스템 내에서 폐수 재활용을 촉진합니다. 이미 유정 현장의 유성 폐기물을 20% 이상 줄이고 기초유 회수율 95%를 달성하는 등 그 효과가 입증된 바 있습니다. 또한, 운영 프레임워크 내에서 폐수의 무방류 재활용을 가능하게 합니다.

지난 수십년동안 아시아태평양은 유해 폐기물 관리에 관한 규제 프레임 워크를 강화하는 데 현저한 진전을 이루었습니다. 각국 정부는 환경 규제를 강화하여 업계가 보다 강력한 폐기물 관리 관행을 채택하도록 강요하고 있습니다. 예를 들어, 2021년 인도 중앙 정부는 “쓰레기 없는 도시”를 구상하는 스와흐 바라트 미션 어반 2.0(SBM-U 2.0)을 출범시켰습니다. 이 미션은 모든 도시 지역 기관이 최소 3단계 인증을 획득하는 것을 목표로 하며, 방문 수거, 원천 분리, 도시 고형 폐기물의 과학적 처리를 강조합니다.

아시아, 특히 중국의 급속한 산업화로 인해 유해 폐기물 발생이 눈에 띄게 증가했지만, 폐기물 처리 기술의 발전과 엄격한 규제 프레임워크는 보다 효율적이고 친환경적인 폐기물 관리 관행으로의 전환을 예고하고 있습니다.

중국과 인도처럼 빠르게 산업화하는 국가에서 유해 폐기물 발생량이 급증하는 것은 첨단 폐기물 관리 솔루션의 필요성을 강조합니다. 중국의 비약적인 경제 성장과 도시화는 유해 폐기물 증가에 직접적으로 기여했으며, 이에 따라 GreenWell 장비와 같은 혁신적인 처리 기술이 필요해졌습니다. 이 기술은 처리 효율을 개선할 뿐만 아니라 폐수 재활용을 통해 환경 지속 가능성도 지원합니다. 또한 아시아태평양 지역에서 규제 프레임워크가 강화되면서 환경 문제를 해결하려는 노력이 증가하고 있으며, 업계가 더 나은 폐기물 관리 관행을 채택해야 한다는 압박이 커지고 있습니다. 이러한 발전은 아시아태평양 지역의 지속 가능한 산업 성장을 향한 긍정적인 추세를 시사합니다.

폐기물 처리 유형별 수거, 향후 몇 년간 더욱 주목받게 될 것

유해 폐기물 수거에는 인간의 건강과 환경에 심각한 위험을 초래하는 물질을 수집, 관리, 운반하는 체계적인 절차가 포함됩니다. 이러한 물질은 고유한 특성(인화성, 독성 등) 또는 규제 기관의 특정 지정에 따라 분류됩니다. 적절한 취급 및 폐기 프로토콜을 적용하려면 정확한 식별이 중요합니다.

2024년 7월, 멕시코 환경청 세데마는 소치밀코와 구스타보 마데로의 불법 쓰레기 매립지에서 5,600개가 넘는 타이어를 처리 공장으로 성공적으로 운송했습니다. 이 타이어는 시멘트 생산의 대체 연료로 용도가 변경될 예정입니다. 지오사이클 멕시코와 협력하는 이 움직임은 종종 공공 오염과 산불 위험 증가로 이어지는 부적절한 타이어 폐기로 인한 환경 문제를 해결하기 위한 세데마의 전략의 초석입니다. 세데마는 레시클라트론 프로그램을 통해 타이어 수거를 강화할 계획을 발표하며 화석 연료와 과도한 광물 추출에서 벗어나 총체적인 폐기물 관리에 대한 멕시코의 노력을 보여주었습니다.

2024년 6월, 오타와 시의회는 2035년 용량에 근접한 트레일 로드 매립지에 대한 압력에 대응하기 위해 고형 폐기물 마스터 플랜을 승인했습니다. 이 매립지를 대체하는 데 6억 달러를 초과할 수 있다는 우려가 제기되고 있습니다. 30년에 걸쳐 승인된 이 전략에는 약 50개의 지원이 포함되어 있습니다. 이는 폐기물을 전환하여 매립지의 수명을 2049년까지 연장하는 것을 목표로 합니다. 오타와의 접근 방식은 지속 가능한 폐기물 관리와 장기적인 환경 보호에 대한 헌신을 강조합니다.

효과적인 유해 폐기물 수거를 위해서는 엄격한 규정 준수, 적절한 직원 교육, 폐기물 발생업체, 운송업체, 처리 시설 등 이해관계자 간의 협력이 필요합니다. 이러한 협업은 안전하고 규정을 준수하는 유해 폐기물 관리를 보장합니다.

유해 폐기물 수거 시장은 규제 준수와 혁신적인 폐기물 관리로 인해 진화하고 있습니다. 멕시코에서 세데마의 노력은 폐기물 용도 변경, 환경 위험 감소, 지속 가능성 증진에 대한 적극적인 자세를 보여줍니다. 오타와의 마스터플랜은 폐기물 감소와 자원 관리에 대한 노력을 반영하여 당면한 문제와 미래의 매립지 문제를 모두 해결하고 있습니다. 이러한 사례는 지속 가능성과 공중 보건을 우선시하는 통합 폐기물 관리에 대한 광범위한 추세를 보여줍니다.

유해 폐기물 관리 업계 개요

유해 폐기물 관리 시장은 적당히 세분화되어 있고 경쟁이 치열합니다. Veolia, Biffa, Covanta Holding, Clean Harbors, Suez Group 등은 유해 폐기물 관리 시장의 주요 기업입니다.

또한 시장의 주요 업체들은 시장 입지를 강화하기 위해 새로운 시설을 확장하는 등의 이니셔티브를 취하고 있습니다. 예를 들어, 2022년 5월 트리니다드 토바고 고형 폐기물 관리 회사(SWMCOL)는 폐휴대폰 재활용을 위한 수거 시설을 시작했습니다. 이 새로운 시작은 회사의 프로젝트인 '전자제품 수명 연장 지원'의 일환으로, 전자제품을 줄이고, 재사용하고, 재활용하기 위한 조치입니다.

마찬가지로 2023년 12월, Sabesp는 2024년부터 2028년 동안 97억 달러를 투자하겠다는 전략을 발표했습니다. 예상 투자의 대부분은 하수도 서비스에 투자하고 나머지는 상수도 공급 범위 확대, 물 손실 관리 및 기타 운영 업무에 사용할 계획입니다. 또한 인수합병, 전략적 제휴, 신규 프로젝트 출시 등을 통해 사업을 확장하여 고객의 요구를 충족시키고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학과 인사이트

시장 개요

시장 성장 촉진요인

세계 환경 규제의 강화로 규정 준수를 위한 유해 폐기물 관리 및 처리 솔루션 수요가 증가

산업 활동 증가와 도시화가 유해 폐기물 배출량을 증가시켜 폐기물 관리 서비스 수요를 촉진

고도의 재활용 및 폐기물 에너지화 프로세스와 같은 폐기물 처리 기술의 혁신, 효율성 향상 및 환경 영향 감소

시장 성장 억제요인

업계에서의 비용 효율이 높은 폐기물 관리와의 밸런스에 고민

유해 물질 취급은 인간의 건강과 환경을 위협하므로 엄격한 안전 프로토콜과 비상 대응 계획이 필요

시장 기회

신흥 시장에서의 산업화와 도시화가 유해 폐기물 관리 서비스의 성장을 가속

폐기수 처리 기술의 진보에 의해 효율적이고 지속 가능한 솔루션을 제공하는 기업에의 기회를 창출

전략적 제휴에 의한 지식의 공유와 기술 투자 촉진

밸류체인, 서플라이체인 분석

Porter's Five Forces 분석

신규 진입업자의 위협

구매자, 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁의 강도

제5장 시장 세분화

유형별

고체

액체

슬러지

폐기물별

화학제품

바이오메디컬

방사성폐기물

기타 폐기물(부식성, 가연성 등)

지역별

북미

미국

캐나다

유럽

독일

영국

프랑스

러시아

스페인

기타 유럽

아시아태평양

인도

중국

일본

기타 아시아태평양

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

기타 중동

남미

브라질

아르헨티나

기타 남미

제6장 경쟁 구도

기업 프로파일

Suez

Valicor

Veolia

Waste Connections

Waste Management

Republic Services

Biffa

Clean Harbors

Covanta Holding

Daiseki

Hitachi Zosen

Remondis SE & Co. Kg

Urbaser

Biomedical Solutions

기타 기업

제7장 시장의 미래

제8장 부록

활동별 GDP 분포

수입과 수출

HBR

영문 목차

영문목차

The Hazardous Waste Management Market size is estimated at USD 40.22 billion in 2025, and is expected to reach USD 48.33 billion by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

Key Highlights

Hazardous waste management involves practices and procedures to handle, control, and dispose of substances that threaten human health or the environment. It includes waste collection, recycling, treatment, transportation, disposal, and monitoring of disposal sites. The primary objective is to mitigate risks and safeguard health and the environment.

The hazardous waste management market is driven by several factors. Governments worldwide are intensifying their focus on waste disposal due to concerns over pollution and health risks. Consequently, stricter regulations are being enacted to govern waste disposal practices and encourage responsible management.

Technological advancements have significantly bolstered hazardous waste management. Innovations in waste treatment and disposal have ushered in more efficient and eco-friendly methods. Notable technologies include steam autoclave treatment, chemical treatment, ozone treatment, pyrolysis, and electron beam technology. For instance, Pello is a new technology that has been developed to help businesses reduce their environmental impact and manage their waste collection more efficiently. Pello helps companies achieve these goals in a number of different ways. Firstly, the Pello system monitors the fill level of trash cans and provides real-time information on the dumpsters' contents and location.

In April 2023, Recycle Track Systems (RTS) acquired RecycleSmart Solutions, solidifying its position as Canada's premier independent provider of advanced waste diversion, organic capture, and recycling management technology. The acquisition encompassed Recycle Smart's cutting-edge Pello waste sensor technology, an integral part of its Internet of Things (IoT) platform.

Hazardous Waste Management Market Trends

Asia-Pacific Expected to Dominate the Market Over the Coming Years

Rapid industrialization in countries like China, India, and Southeast Asian nations has driven a surge in hazardous waste production, notably in industries such as manufacturing, mining, and electronics. China, for instance, has witnessed a nearly threefold increase in waste output since the 1990s. This rise can be attributed to multiple factors. Over the past few decades, China's urbanization rate has steadily climbed. By 2023, data from the National Bureau of Statistics of China revealed that approximately 66.2% of the population was residing in urban areas.

China's robust economic growth, evidenced by its 2023 GDP of roughly USD 17.7 trillion, as per the International Monetary Fund (IMF), further bolstered industrial waste production. While the volume of conventional industrial waste, such as tailings and fly ash, has remained stable, hazardous waste production has surged in tandem with industrial progress. Notably, these hazardous by-products necessitate more advanced treatment for safe disposal. A significant milestone was reached in March 2024 when Jereh Group introduced its GreenWell distributed hazardous waste treatment equipment. This innovative solution, tailored to address challenges in centralized hazardous waste disposal, allows for on-site treatment, bypassing the need for intermediary steps.

By streamlining on-site treatment and eliminating intermediary steps, this state-of-the-art equipment significantly enhances processing efficiency, reduces waste, and facilitates wastewater recycling within the system. Impressively, it has already demonstrated its efficacy, cutting oily waste at well sites by over 20% and achieving an outstanding 95% recovery rate for basic oil. Furthermore, it enables zero-discharge recycling of wastewater within its operational framework.

Over the past few decades, Asia-Pacific has made notable strides in enhancing its regulatory frameworks for managing hazardous waste. Governments have intensified environmental regulations, compelling industries to adopt more robust waste management practices. For instance, in 2021, the Central Government of India launched the Swachh Bharat Mission Urban 2.0 (SBM-U 2.0), envisioning "Garbage Free Cities." The mission targets all urban local bodies to secure at least a 3-star certification, emphasizing door-to-door collection, source segregation, and scientific processing of municipal solid waste.

While rapid industrialization in Asia, particularly in China, has led to a notable uptick in hazardous waste generation, advancements in waste treatment technology and stringent regulatory frameworks are heralding a shift toward more efficient and eco-friendly waste management practices.

The surge in hazardous waste production in rapidly industrializing countries like China and India underscores the critical need for advanced waste management solutions. China's significant economic growth and urbanization have directly contributed to increased hazardous waste, necessitating innovative treatment technologies like the GreenWell equipment. This technology not only improves processing efficiency but also supports environmental sustainability through wastewater recycling. Additionally, the strengthening of regulatory frameworks across the Asia-Pacific indicates a growing commitment to addressing environmental challenges, compelling industries to adopt better waste management practices. These developments suggest a positive trend toward more sustainable industrial growth in the region.

By Disposal Type, Collection Gaining More Traction Over the Coming Years

Hazardous waste collection involves structured procedures to gather, manage, and transport materials that pose significant risks to human health and the environment. These materials are classified based on inherent traits (flammable, toxic, etc.) or specific designations by regulatory bodies. Accurate identification is crucial for applying proper handling and disposal protocols.

In July 2024, Sedema, Mexico's Secretariat of the Environment, successfully transported over 5,600 tires from illegal dumps in Xochimilco and Gustavo Madero to a treatment plant. These tires will be repurposed as an alternative fuel in cement production. Partnering with Geocycle Mexico, this move is a cornerstone in Sedema's strategy to combat environmental challenges from improper tire disposal, which often leads to public pollution and heightened wildfire risks. Sedema announced plans to bolster its tire collection via the Reciclatron Program, showcasing Mexico's commitment to holistic waste management and a shift away from fossil fuels and excessive mineral extraction.

In June 2024, Ottawa's city council greenlit a Solid Waste Master Plan, responding to mounting pressures on the Trail Road Landfill, nearing its 2035 capacity. Concerns arise as replacing it could exceed USD 600 million. The endorsed strategy, spanning three decades, includes nearly 50 initiatives. These aim to divert waste, extending the landfill's life to 2049. Ottawa's approach highlights its dedication to sustainable waste management and long-term environmental stewardship.

Effective hazardous waste collection demands strict regulatory compliance, proper personnel training, and collaboration among stakeholders, including waste generators, transporters, and disposal facilities. This collaboration ensures safe and compliant hazardous waste management.

The hazardous waste collection market is evolving, driven by regulatory compliance and innovative waste management. Sedema's initiative in Mexico showcases a proactive stance on repurposing waste, reducing environmental risks, and promoting sustainability. Ottawa's Master Plan mirrors a commitment to waste reduction and resource management, addressing both immediate and future landfill concerns. These cases underscore a broader trend toward integrated waste management, prioritizing sustainability and public health.

Hazardous Waste Management Industry Overview

The hazardous waste management market is moderately fragmented and competitive. Veolia, Biffa, Covanta Holding, Clean Harbors, and Suez Group are among the key players in the hazardous waste management market.

Moreover, key players in the market are taking initiatives such as expanding new facilities to strengthen their market presence. For instance, in May 2022, The Trinidad and Tobago Solid Waste Management Company (SWMCOL) launched collection sites for recycling old mobile phones. The new launch was a part of the company's project, 'Helping Electronics Live Longer,' which is a measure to reduce, reuse, and recycle.

Similarly, in December 2023, Sabesp announced a strategy to invest USD 9.7 billion in its operations over 2024-28. The majority of the company's expected investments will be in sewerage services, while the rest will be spent on expanding water supply coverage, controlling water losses, and other operational tasks. In addition, players are expanding their businesses through mergers, acquisitions, strategic partnerships, and new project launches to meet customer needs.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Stringent Global Environmental Regulations Drive Demand for Compliant Hazardous Waste Management and Disposal Solutions

4.2.2 Increased Industrial Activities and Urbanization Driving up Hazardous Waste Production, Fueling Demand for Waste Management Services

4.2.3 Innovations in Waste Treatment Technologies, such as Advanced Recycling and Waste-to-Energy Processes, Enhance Efficiency and Reduce Environmental Impact

4.3 Market Restraints

4.3.1 Industries Under Economic Pressure Often Struggle to Balance Cost-efficient Waste Management

4.3.2 Handling Hazardous Materials Risks Human Health and the Environment, Requiring Strict Safety Protocols and Emergency Response Plans

4.4 Market Opportunities

4.4.1 Industrialization and Urbanization in Emerging Markets are Driving Growth in Hazardous Waste Management Services

4.4.2 Advancements in Waste Treatment Technologies Create Opportunities for Companies Offering Efficient and Sustainable Solutions

4.4.3 Strategic Collaborations can Enhance Knowledge Sharing and Technology Investments

4.5 Value Chain/Supply Chain Analysis

4.6 Porter's Five Forces Analysis

4.6.1 Threat of New Entrants

4.6.2 Bargaining Power of Buyers/Consumers

4.6.3 Bargaining Power of Suppliers

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Type

5.1.1 Solid

5.1.2 Liquid

5.1.3 Sludge

5.2 By Waste

5.2.1 Chemicals

5.2.2 Biomedical

5.2.3 Radioactive

5.2.4 Other Waste (Corrosive, Flammable, etc.)

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Russia

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 India

5.3.3.2 China

5.3.3.3 Japan

5.3.3.4 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 United Arab Emirates

5.3.4.2 Saudi Arabia

5.3.4.3 Rest of Middle East

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Overview (Market Concentration & Major Players)