아시아태평양의 첨단 건축 자재 시장 전망 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

APAC Advanced Building Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636158

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

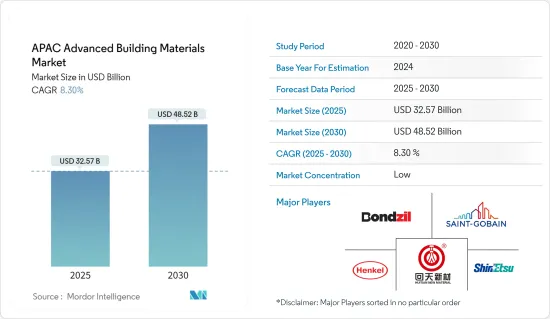

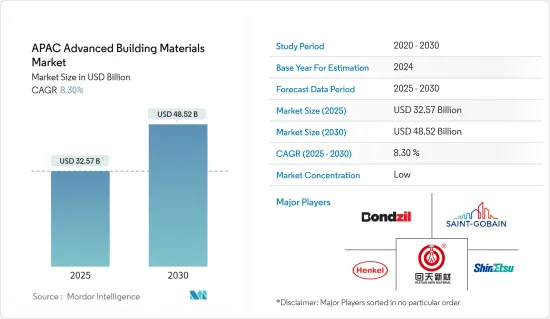

아시아태평양의 첨단 건축 자재 시장 규모는 2025년에 325억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 8.3%로, 2030년에는 485억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

유행은 건축 자재 제조에 영향을 미치고 공급망에 혼란을 가져왔으며, 이동 제한, 국경 폐쇄 등으로 인해 시장이 더욱 확대되지 못했습니다. 또한 팬데믹으로 인해 건설 프로젝트가 지연되어 고급 건축 자재 산업에 더 큰 영향을 미쳤습니다. 이후 제한이 완화되면서 시장은 팬데믹 이전 수준으로 회복되었습니다.

성장하는 건물 건설 및 인프라 부문은 고급 건축 자재 산업의 주요 동력입니다. 이러한 자재는 구조적 강도, 에너지 효율성, 탈탄소화 목표 등을 달성하기 위해 건설 프로젝트에 사용됩니다. 또한 국가가 설정한 탄소중립 목표를 달성하기 위해 대부분의 개발자는 개발 프로젝트에서 친환경 건축 자재를 채택하는 데 관심이 있습니다.

한편, 건설 시간 단축과 비용 효율적인 제품 활용에 대한 필요성이 증가하면서 첨단 건축 자재에 대한 수요가 증가하고 있습니다. 또한 레미콘과 프리캐스트 제품을 활용하면 건물 건설 산업에서 시간을 절약할 수 있습니다.

예를 들어, 2022년 7월, AboitizLand는 미쓰이 스미토모 건설, SMCC Philippines Inc.와 제휴하여 일본의 프리캐스트 콘크리트 기술을 도입하여 주택 프로젝트를 혁신했습니다. 이와 같이 건설 프로젝트 증가와 인프라 부문 투자 증가는 이 지역의 첨단 건축 자재 산업 수요를 촉진할 것으로 예상됩니다.

아시아태평양의 첨단 건축자재 시장 동향

시장의 수요를 주도하는 인프라 개발

아시아태평양 지역은 현재 인프라 개발 프로젝트에서 상당한 성장을 경험하고 있으며, 이는 주로 투자 증가에 힘입은 것입니다. 이러한 투자 급증은 이러한 프로젝트에서 첨단 건축 자재에 대한 수요를 강화하고 있습니다. 예를 들어, 2022년 5월 미국, 인도, 호주는 아시아 태평양 지역 인프라 프로젝트에 500억 달러 이상을 투자할 계획을 발표했습니다.

또한 인도, 중국, 일본과 같은 개발도상국에서는 수많은 인프라 프로젝트가 진행 중이며, 이를 통해 각국의 경제가 더욱 발전하고 있습니다. 2023년 4월, 인도 정부는 7억 4,000만 달러가 넘는 인프라 프로젝트 계획을 발표했습니다. 또한 국가 인프라 파이프라인을 통해 인도 정부는 인도 내 인프라 개발 프로젝트에 1,300억 달러 이상을 배정하는 것을 목표로 하고 있습니다.

한편, 일본은 2023년 5월 인도에 파트나 메트로 철도 건설 프로젝트와 라자스탄 수자원 부문 생활 개선 프로젝트 등 3개 인프라 프로젝트에 8억 6천만 달러 이상을 지원하기로 약속했습니다. 또한, 2022년 중국의 공공 지출은 전년 대비 5% 이상 크게 증가했습니다. 결과적으로 아시아태평양 지역의 인프라 개발 프로젝트에 대한 이러한 투자 증가는 고급 건축 자재에 대한 상당한 수요를 창출하고 있습니다.

중국의 건설 부문이 시장 성장을 주도

중국 건설 산업은 팬데믹 위기에도 불구하고 제14차 5개년 계획(2021-2025년)에 명시된 인프라에 대한 막대한 투자에 힘입어 상당한 성장을 경험하고 있습니다. 이 계획은 5개 부문에 걸쳐 20개의 정량적 목표로 구성되어 있습니다. 중국 정부는 2023년까지 전국적으로 다양한 인프라 프로젝트에 1조 1,000억 달러 이상을 배정하여 중국 내 첨단 건축 자재 제조 공장의 개발을 더욱 촉진할 계획입니다.

또한 2022년 중국 정부는 건물과 관련된 오염을 억제하기 위한 친환경 건설 프로젝트에 140억 달러 이상을 배정했습니다. 탄소 순배출 제로 목표를 달성하기 위해 중국 정부는 특히 건물 관련 오염을 완화하는 데 7억 8천만 달러 이상을 배정했습니다.

게다가, 문화유산 보존을 위한 노력의 일환으로 전국적으로 수많은 박물관을 건립하고 있습니다. 예를 들어, 베이징시 문화유산국은 2023년 2월까지 베이징에 460개 이상의 박물관을 건립하고, 이미 215개 이상의 박물관이 등록되었습니다. 이러한 지속적인 투자와 프로젝트 확대로 인해 중국의 건설 생산량은 전년 대비 6% 이상 증가했으며, 이에 따라 첨단 건축 자재 제조업체에 대한 수요도 증가하고 있습니다.

아시아태평양의 첨단 건축 자재 산업 개요

이 보고서는 아시아 태평양 첨단 건축 자재 시장에서 활동하는 저명한 업체들을 다룹니다. 이 시장은 경쟁이 치열하고 세분화되어 있으며, 상당한 점유율을 차지하고 있는 플레이어는 없습니다. 경쟁력을 유지하기 위해 주요 업체들은 제품 제공을 강화하고, 지리적 입지를 확장하고, 인수합병에 지속적으로 참여하기 위해 끊임없이 노력하고 있습니다. 시장의 주요 기업으로는 Huitian, Bondzil, Saint-Gobain Group, Henkel Balti OU, Shin-Etsu Chemical Industry 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

분석 방법

조사 단계

제3장 주요 요약

제4장 시장 인사이트

현재의 시장 시나리오

기술 동향에 대한 통찰

업계의 밸류체인, 공급망 분석

시장에 관한 정부 규제와 주요 지원

시장 역학

성장 촉진요인

인프라 개발을 위한 정부 지출 증가

공기 단축과 비용 효율적인 제품에 대한 요구

억제요인

초기 투자 높이

기회

업계의 매력 - Porter's Five Forces 분석

신규 참가업체의 위협

구매자, 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

COVID-19가 시장에 미치는 영향

제5장 시장 세분화

용도별

빌딩 건설

인프라

유형별

그린 소재

첨단 기술

재료별

첨단 시멘트, 콘크리트

집성재

구조용 단열 패널

실링재

기타 재료

국가별

중국

인도

일본

한국

호주

기타 아시아태평양

제6장 경쟁 구도

시장 집중도 개요

기업 프로파일

China National Building Material Group Corporatio

Henkel Balti OU

China Lesso

Huitian

Zamil Steel Buildings India Private Limited

Kingspan Jindal

Bondzil

Ultratech Cement Limited

Arto Precast Concrete

Saint-Gobain Group

BASF SE

DuPont

Sika AG

신에츠 케미컬(주)

제7장 시장 기회와 앞으로의 동향

제8장 부록

HBR

영문 목차

영문목차

The APAC Advanced Building Materials Market size is estimated at USD 32.57 billion in 2025, and is expected to reach USD 48.52 billion by 2030, at a CAGR of 8.3% during the forecast period (2025-2030).

Key Highlights

The pandemic had impacted building materials manufacturing and disrupted the supply chain, further preventing the market from expanding due to restrictions, border closures, etc. Additionally, the pandemic caused delays in construction projects, further affecting the advanced building materials industry. Later, after easing restrictions, the market recovered when compared to pre-pandemic levels.

The growing building construction and infrastructure sectors are the major drivers of the advanced building materials industry. These materials are employed in construction projects to achieve structural strength, energy efficiency, decarbonization goals, etc. In addition, to meet net-zero goals set by the country, most of the developers are interested in adopting green building materials in development projects.

Meanwhile, in April 2023, the Confederation of Real Estate Developers Association of India (Credai) partnered with the Indian Green Building Council (IGBC) to build over 1,000 certified green projects across India in the next two years, and 4,000 projects by 2030, these projects, in turn, bolsters the utilization of advanced building materials.

Furthermore, the increasing need for construction time reduction and utilization of cost-effective products is driving the demand for advanced construction materials. In addition, the utilization of ready-mix concrete and precast products saves time in the building construction industry.

For instance, in July 2022, AboitizLand partnered with Sumitomo Mitsui Construction Co. Ltd., SMCC Philippines Inc., to innovate its residential projects with the introduction of Japanese precast concrete technology. Thus, the growing construction projects and increasing investments in the infrastructure sector are expected to drive the demand for the advanced building materials industry in the region.

APAC Advanced Building Materials Market Trends

Infrastructure developments driving the market demand

The Asia-Pacific region is currently experiencing significant growth in infrastructure development projects, primarily driven by increased investments. This surge in investment is, in turn, bolstering the demand for advanced building materials within these projects. For example, in May 2022, the United States, India, and Australia announced plans to invest over USD 50 billion in infrastructure projects across the Asia-Pacific region.

Moreover, developing countries such as India, China, and Japan are undergoing numerous infrastructure projects, which are further propelling their respective economies. In April 2023, the Indian government revealed plans for infrastructure projects exceeding USD 740 million. Additionally, through the National Infrastructure Pipeline, the government aims to allocate more than USD 1,300 billion to infrastructure development projects in India.

Meanwhile, in May 2023, Japan committed to funding India with over USD 860 million for three infrastructure projects, including the Patna Metro Rail Construction Project and the Rajasthan Water Sector Livelihood Improvement Project. Furthermore, Chinese public expenditure in 2022 witnessed a substantial growth of over 5% compared to the previous year. Consequently, these increasing investments in infrastructure development projects across the Asia Pacific region are generating a significant demand for advanced building materials.

China construction sector is driving market growth

The Chinese construction industry is experiencing significant growth despite the pandemic crisis, fueled by substantial investments in infrastructure as outlined in the 14th Five-Year Plan (spanning from 2021 to 2025). This plan comprises 20 quantitative targets across five categories. The Chinese government has allocated over USD 1.1 trillion for diverse infrastructure projects nationwide by 2023, further boosting the development of advanced building materials manufacturing plants in the country.

Additionally, in 2022, the Chinese government earmarked more than USD 14 billion for green construction projects aimed at curbing pollution associated with buildings. To achieve net-zero carbon emission goals, the government allocated over USD 780 million specifically to mitigate building-related pollution.

Furthermore, efforts to preserve cultural heritage involve the construction of numerous museums nationwide. For example, the Beijing Municipal Cultural Heritage Bureau planned to build over 460 museums in the city by February 2023, with more than 215 museums already registered. These continuous investments and expanding projects have driven the country's construction output to grow by over 6% compared to the previous year, thereby generating increased demand for manufacturers of advanced construction materials.

APAC Advanced Building Materials Industry Overview

The report covers prominent players operating in the Asia-Pacific advanced building material market. The market is highly competitive and fragmented, with no players occupying a significant share. To remain competitive, the major players are constantly working to enhance their product offerings, expanding their geographical presence, and constantly being involved in mergers and acquisitions. Some of the major players in the market include Huitian, Bondzil, Saint-Gobain Group, Henkel Balti OU, Shin-Etsu Chemical Co., Ltd, etc.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Current Market Scenario

4.2 Insights on Technological Trends

4.3 Industry Value Chain/Supply Chain Analysis

4.4 Spotlight on Government Regulations and Key Initiatives in the Market

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increase in government expenditures for infrastructural development

4.5.1.2 Need for reduced construction time and cost-effective products

4.5.2 Restraints

4.5.2.1 High initial investments

4.5.3 Opportunities

4.6 Industry Attractiveness - Porter's Five Forces Analysis

4.6.1 Threat of New Entrants

4.6.2 Bargaining Power of Buyers/Consumers

4.6.3 Bargaining Power of Suppliers

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

5.1 By Application

5.1.1 Building Construction

5.1.2 Infrastructure

5.2 By Type

5.2.1 Green Materials

5.2.2 Technically Advanced

5.3 By Material

5.3.1 Advanced Cement And Concrete

5.3.2 Cross-Laminated Timber

5.3.3 Structural Insulated Panel

5.3.4 Sealants

5.3.5 Other Materials

5.4 By Country

5.4.1 China

5.4.2 India

5.4.3 Japan

5.4.4 South Korea

5.4.5 Australia

5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 China National Building Material Group Corporatio