ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

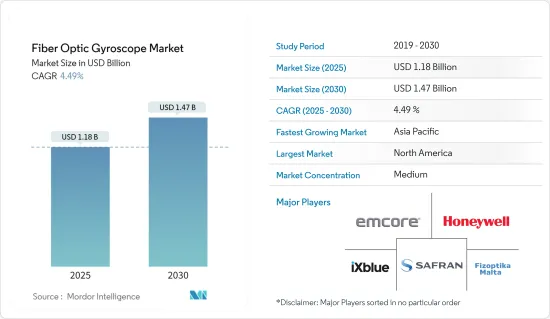

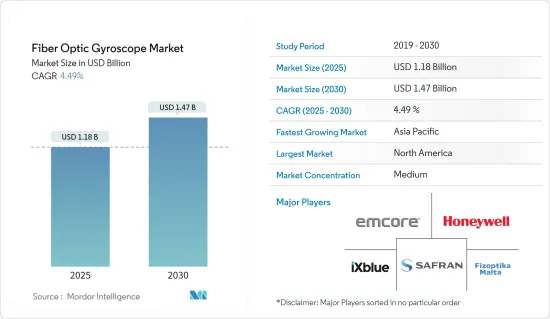

광섬유 자이로스코프 시장 규모는 2025년 11억 8,000만 달러로 추정 및 예측되며, 예측 기간(2025-2030년) 동안 4.49%의 CAGR로 2030년에는 14억 7,000만 달러에 달할 것으로 예상됩니다.

광섬유 자이로스코프는 높은 출력 속도와 다양한 각도에서 각속도를 측정하는 정확도로 유명해 채택이 급증하고 있습니다. 이러한 추세는 특히 비탑승 군용 차량과 공중 모니터링 시스템에서 두드러지게 나타나고 있으며, 항공우주 및 방위 분야에서 자이로스코프에 대한 수요를 증가시키고 있습니다.

항공우주, 국방, 산업 등 다양한 분야에서 광섬유 자이로에 대한 관심이 높아지고 있습니다. 그 배경에는 소형, 경량, 긴 수명, 신뢰성, 저전력 소비, 대량 생산에 대한 적합성 등이 있습니다. 그 결과, 각 부문에서 수요가 증가하여 시장 성장을 촉진하고 있습니다. 세계 각국 정부가 국방력 강화를 위해 군사비를 늘리면서 광섬유 자이로스코프, 특히 원격 차량 유도 등의 용도로 수요가 급증하고 있습니다.

이 시장을 주도하는 것은 국방 및 상업 부문에서 드론과 UAV의 채택이 확대되고 있다는 점입니다. 미국 연방항공청(FAA)의 보고서에 따르면 2023년 미국에서 약 51만 6,800대의 드론이 레크리에이션 비행을 위해 등록될 것으로 예상됩니다. 주목할 점은 이 수치는 등록이 의무화되지 않은 취미용 드론을 제외한 수치라는 점입니다.

광섬유 자이로스코프(FOG) 시장을 강화하는 주요 촉진요인으로는 신흥 경제권과 기존 경제권 모두에서 국방비 지출 증가, 산업 및 가정 내 자동화 도입 급증 등이 있습니다. 이스라엘은 군용 애플리케이션의 선진국인 이스라엘은 텔아비브의 에어로보틱스(Airobotics)가 기업용 자율 솔루션을 선도하며 광섬유 자이로 시장을 주도하고 있습니다. 석유 시추 과정에서 측정에 광섬유 자이로스코프를 사용하고, 원격 조종 차량의 부상과 진화는 시장 성장을 더욱 촉진하고 있습니다.

또한, 소비자 가전 및 산업용 광섬유 자이로스코프(FOG)의 소형화 추세와 제조 비용 절감 노력도 시장 성장에 크게 기여하고 있으며, FOG의 크기와 비용 절감으로 제조업체들은 소비자 가전, 자동차, 항공우주, 산업 자동화 등 다양한 분야로 FOG를 확장하고 있습니다. FOG의 뛰어난 정밀도와 신뢰성은 기존 시장과 신규 시장 모두에서 FOG의 채택을 촉진하고 있습니다. 소형 고성능 센서에 대한 수요가 급증하면서 FOG 시장은 향후 몇 년 동안 크게 성장할 것으로 예상됩니다.

광섬유 자이로스코프에 대한 시장의 큰 수요에도 불구하고, 복잡하고 비싸고 시간이 많이 걸리는 제조 공정이 큰 제약 요인으로 작용하고 있습니다. 이러한 제약은 광섬유 자이로스코프의 보급을 제한하고 시장 성장을 어느 정도 억제하고 있습니다.

지정학적 문제와 경제 상황의 변화를 포함한 거시경제적 요인은 시장 형성에 매우 중요한 역할을 합니다. 예를 들어, 경제가 호황인 지역에서는 첨단 군 및 방위 시스템에 더 많은 예산이 할당되기 때문에 이러한 솔루션의 채택이 확대될 것입니다. 전쟁과 같은 지정학적 이슈는 시장 성장을 더욱 촉진합니다.

광섬유 자이로스코프 시장 동향

시장을 장악하고 있는 항공우주 및 항공 부문

광섬유 자이로스코프의 주요 최종사용자인 항공우주 산업은 비행 제어, 지상 감지 및 동적 세계 포지셔닝 시스템(GPS) 추적에 이러한 장치를 광범위하게 채택하고 있습니다. 특히 아시아태평양의 항공 부문에 대한 투자 추세와 함께 이러한 추세는 광섬유 자이로스코프에 대한 수요를 강화할 것입니다.

예를 들어, 인도는 세계에서 가장 큰 항공 시장으로 빠르게 자리매김하고 있습니다. 지난 1년 동안 Air India, Indigo, Akasa Air를 포함한 인도의 주요 항공사들은 총 1,100대 이상의 항공기를 주문했으며, 이는 세계 역사상 가장 큰 규모의 민간항공기 주문입니다.

마찬가지로 세계 시장도 이러한 추세를 반영하고 있습니다. 민간항공기 제조 대기업인 보잉(Boeing)은 2023년부터 2042년까지 전 세계 민간항공기가 약 4만 2,595대의 신규 납품을 맞이할 것으로 예상하고 있습니다. 광섬유 자이로(FOG)는 항공기 항법 시스템, 항공기 운동 모니터링, 각속도 및 속도 등의 측정 기준에서 중요한 역할을 담당하고 있으며, 이러한 사례가 시장 성장을 촉진할 것으로 보입니다.

특히 FOG는 우주 로켓 및 관련 시스템에서 중요한 역할을 하기 때문입니다. 또한 SpaceX와 Blue Origin과 같이 우주여행을 현실화하려는 비전을 가진 비상장 기업의 출현은 조사 대상 시장 기회를 더욱 확대할 것입니다.

Jonathan Space Report에 따르면, 2023년에는 지구 궤도를 도는 약 9,115개의 활동 중인 위성이 확인되어 전년 대비 35% 급증할 것으로 예상됩니다. 자이로스코프는 우주선이나 발사체에서 매우 중요한 역할을 하는데, 방향과 각도의 움직임을 감지할 수 있습니다. 이 기능을 통해 우주선의 초기 위치에서 움직임을 정확하게 제어하고 추적할 수 있습니다. 그 결과 인공위성 발사가 증가하여 이 시장의 성장을 촉진하는 환경이 조성되었습니다.

아시아태평양은 괄목할만한 성장률을 보임

향후 몇 년 동안 아시아태평양은 여러 신흥 경제국의 국방 예산 증가로 인해 상당한 시장 성장을 보일 것입니다. 특히 중국과 일본이 이 지역의 광섬유 자이로스코프 수요를 주도하고 있습니다. 이러한 성장에는 항공우주 및 방위 부문의 R&D 활동 증가, 빠른 산업화, 센서, 드론 및 무인 해양 선박을 강화하기 위한 대규모 투자 등의 요인이 기여하고 있습니다.

중국은 자동차 산업의 제조 거점으로 부상하고 있으며, 무인 자동차의 새로운 개발 계획과 함께 광섬유 자이로 채택에 박차를 가하고 있습니다. 중국, 일본, 한국과 같은 국가들의 규제 강화는 기업의 투자를 더욱 자극하고 있습니다. 그 결과, 최종사용자 기업들은 다양한 모니터링 시스템에서 방위 측정을 우선순위로 삼고 있으며, 시장 확대가 두드러지게 나타나고 있습니다.

최근 몇 년 동안 인도는 군사 및 방산 제품의 주요 지출 국가로 부상하여 FOG에 유리한 시장으로 부상하고 있습니다. 예를 들어, 2024년 2월 미국 국무부는 제너럴 아토믹스의 MQ-9B 드론을 인도에 39억 달러 규모의 잠재적 거래를 승인했습니다. 이 계약은 워싱턴과 뉴델리의 국방 및 안보 협력 강화를 강조합니다. 인도군에 제안된 패키지는 31대의 스카이 가디언 무인항공기, 310개의 소구경 폭탄, 170개의 헬파이어 미사일을 포함합니다. 이 패키지에는 해상 수송에 특화된 Sea Guardian용 레이더와 대잠 장비도 포함되어 있습니다.

인도는 항공우주 및 방위 산업에서 괄목할 만한 발전을 이루며 조사 대상 시장에서 기회를 창출하고 있습니다. 예를 들어, 최근 인도 최초의 민간 UAV 제조 시설인 Adani-Elbit Advanced Systems India Ltd는 이스라엘에 20대 이상의 Hermes 900 중고도 및 장시간 비행(MALE) UAV를 성공적으로 납품했습니다. 하이데라바드에 본사를 둔 이 합작회사는 인도의 Adani Defence and Aerospace와 이스라엘의 Elbit Systems가 합작하여 설립한 회사로, 이스라엘 밖에서 이 UAV를 제조한 최초의 회사입니다.

다른 국가들도 비슷한 추세를 목격하고 있습니다. 예를 들어, 중국은 UAV 역량을 적극적으로 강화하고 있습니다. 중국 민간항공국(CAAC)에 따르면 중국은 2023년 말까지 전년 대비 32.2% 증가한 127만 대의 드론을 등록할 것으로 예상됩니다. 결과적으로 이러한 추세와 발전은 예측 기간 동안 이 지역에서 조사된 시장의 성장을 촉진할 것입니다.

광섬유 자이로스코프 산업 개요

광섬유 자이로스코프 시장 경쟁은 중간 정도이며, 몇몇 주요 기업들이 선두에 서 있습니다. 이들 진입 기업 중 일부 기업은 현재 시장 점유율에서 지배적인 위치를 차지하고 있습니다. 무인 자동차의 급속한 부상과 지속적인 기술 발전은 시장 공급업체에게 매력적인 기회를 제공하고 있습니다. 기존 업체들 간의 경쟁은 완만하지만, 각 업체들은 혁신 전략을 통해 시장 수요를 자극하고 있습니다. 그러나 복잡하고 시간이 많이 소요되는 제조 공정, 막대한 투자, 낮은 비용 효율성 등의 문제로 인해 신규 업체들이 광섬유 자이로스코프 제조를 주저하고 있습니다. 주요 시장 진입 기업으로는 Emcore, Honeywell, Safran 등이 있습니다.

2024년 6월, Exail은 Rheinmetall과 독일 육군의 Caracal 4X4 차량에 1004대의 Advans Ursa 관성 항법 시스템(INS)을 납품하기로 합의하는 중요한 계약을 체결했습니다. 엑스자일의 첨단 광섬유 자이로스코프(FOG) 기술을 활용한 Advans Ursa는 전술 항법용으로 특별히 설계된 컴팩트하고 예산 친화적인 INS로 눈에 띕니다. 이 시스템은 가혹한 조건에서도 정확하고 신뢰할 수 있는 내비게이션 데이터를 보장합니다. 그 결과, 카라칼 차량은 GNSS 신호가 전혀 없는 상황에서도 시간이나 거리에 관계없이 제약 없이 자신 있게 항해할 수 있습니다.

2024년 6월, Inertial Labs는 최신 제품인 INS-FI를 발표했습니다. 이 GPS 보조 관성 항법 시스템(INS)은 전술 등급 광섬유 자이로스코프(FOG) 기술을 활용하여 시장에서 가장 정교하고 신뢰할 수 있는 INS 솔루션 중 하나로 자리매김하고 있습니다. GPS, GALILEO, GLONASS, QZSS, NAVIC, BEIDOU를 포함한 모든 별자리와 호환되는 멀티 밴드 GNSS 수신기를 자랑합니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 강도

산업 밸류체인 분석

거시경제 동향이 광섬유 자이로스코프 시장에 미치는 영향

제5장 시장 역학

마커 드라이버

방위와 민간 용도에서 무인 차량의 급성장

세계의 방위비 확대

시장 성장 억제요인

시장 수요 과제가 되고 있는 복잡성의 상당한 상승

첨단 미세전자기계 시스템용 자이로스코프에 대한 수요 증가

제6장 시장 세분화

코일 유형별

플랜지 형태

허브형

자립형

검출축별

1축

2축

3축

디바이스별

자이로 컴퍼스

관성측정장치

관성 항법 시스템

최종 이용 산업별

항공우주

로봇공학

자동차(자율주행차)

방위

산업

기타

지역별

북미

유럽

아시아태평양

호주·뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 개요

EMCORE Corporation

Honeywell International Inc.

KVH Industries Inc.

Safran Colibrys SA

iXBlue SAS

Northrop Grumman LITEF GmbH

Cielo inertial Solutions Ltd

Fizoptika Malta

NEDAERO

Optolink LLC

Advanced Navigation

제8장 투자 분석

제9장 시장 전망

ksm

영문 목차

영문목차

The Fiber Optic Gyroscope Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.47 billion by 2030, at a CAGR of 4.49% during the forecast period (2025-2030).

Fiber optic gyroscopes, known for their high output rates and precision in measuring angular velocity across diverse angles, are witnessing a surge in adoption. This trend is particularly evident in uncrewed military vehicles and airborne surveillance systems, driving up the demand for these gyroscopes in the aerospace and defense sectors.

Various sectors, including aerospace, defense, and industrial domains, are increasingly turning to fiber optic gyroscopes. This is attributed to their compact size, lightweight nature, longevity, reliability, low power consumption, and suitability for mass production. As a result, this heightened demand across sectors propels the market's growth. With governments worldwide ramping up military expenditures to bolster their defense capabilities, there is a corresponding surge in demand for fiber optic gyroscopes, especially in applications like remotely operated vehicle guidance.

The market is driven by the growing adoption of drones and UAVs across defense and commercial sectors. The Federal Aviation Administration (FAA) reported that in 2023, approximately 516.8 thousand drones were registered for recreational flying in the United States. Notably, this count excludes hobbyist drones, which are not required to be registered.

Key drivers bolstering the fiber optics gyroscope (FOG) market include heightened defense spending in both emerging and established economies, alongside a surge in automation adoption across industries and households. Israel, a frontrunner in military application advancements, showcases its prowess with Tel Aviv's Airobotics spearheading autonomous solutions for enterprises, propelling the fiber optic gyroscope market. Using fiber optic gyroscopes for measurement during oil drilling processes and the rising prominence and evolution of remotely operated vehicles further fuel the market's growth.

The market's growth is also being significantly driven by the trend of miniaturizing fiber optic gyroscopes (FOGs) for consumer electronics and industrial applications, alongside efforts to cut manufacturing costs. By reducing the size and cost of FOGs, manufacturers are broadening their applications to sectors like consumer electronics, automotive, aerospace, and industrial automation. This broadened application is spurring greater adoption of FOGs in new and established markets due to their superior precision and reliability. With the surging demand for compact, high-performance sensors, the FOG market is set for substantial growth in the years ahead.

Despite significant demand for fiber optic gyroscopes in the market, their complicated, costly, and time-consuming manufacturing process poses a considerable constraint. This limitation restricts the widespread adoption of fiber optic gyroscopes and curtails the market's growth to some degree.

Macroeconomic factors, including shifting geopolitical issues and economic conditions, are pivotal in shaping the market. For example, regions enjoying robust economic health typically allocate greater budgets to advanced military and defense systems, thereby broadening the adoption of these solutions. Geopolitical challenges, such as wars, further drive the growth of the market studied.

Fiber Optic Gyroscope Market Trends

Aerospace and Aviation Segment to Dominate the Market

The aerospace and aviation industry, a major end-user of fiber optic gyroscopes, extensively employs these devices in flight control, ground detection, and dynamic global positioning system (GPS) tracking. Coupled with rising investments in the aviation sector, particularly in the Asia-Pacific region, this trend is set to bolster the demand for fiber optic gyroscopes.

For instance, India is rapidly establishing itself as one of the world's largest aviation markets. Over the past year, leading Indian airlines, including Air India, Indigo, and Akasa Air, collectively placed orders for more than 1,100 aircraft, marking one of the largest commercial aircraft orders in global history.

Similarly, the global market mirrors this trend. Boeing, a leading name in commercial aircraft manufacturing, projects that from 2023 to 2042, the global commercial fleet will welcome approximately 42,595 new aircraft deliveries. Given the prominent role of fiber optic gyroscopes (FOGs) in aircraft navigation systems, monitoring motion in aviation, and capturing metrics like angular velocity and speed, such instances are poised to propel the growth of the market.

As countries like India ramp up their space missions, the growing activities in the space exploration sector are set to boost the market studied, especially since FOGs play a crucial role in space rockets and related systems. Moreover, the emergence of private companies like SpaceX and Blue Origin, with their vision of making space travel a reality, further amplifies the opportunities in the market studied.

As reported by Jonathan Space Report, 2023 witnessed approximately 9,115 active satellites orbiting Earth, marking a 35% surge from the prior year's count. Gyroscopes play a pivotal role in space vehicles and launch rockets, enabling them to detect orientation and angular motion. This capability allows precise control and tracking of the craft's movement from its initial position. Consequently, the uptick in satellite launches fosters a conducive environment for the growth of the market studied.

Asia-Pacific to Witness a Significant Growth Rate

In the coming years, the Asia-Pacific is set to witness significant market growth, driven by rising defense budgets in several emerging economies. Notably, China and Japan are leading the demand for fiber optic gyroscopes in the region. Contributing to this growth are factors such as heightened R&D activities in the aerospace and defense segment, swift industrialization, and substantial investments to enhance sensors, drones, and unmanned maritime vessels.

China's emergence as a manufacturing hub for the automobile industry, coupled with its new development plans for driverless vehicles, is spurring the adoption of fiber optic gyroscopes. The tightening of regulations in countries like China, Japan, and South Korea has further incentivized corporate investments. As a result, end-user companies increasingly prioritize orientation measurement in various monitoring systems, underscoring the market's expansion.

In recent years, India has emerged as a leading spender on military and defense products, making it a lucrative market for FOGs. For example, in February 2024, the US State Department approved a potential USD 3.9 billion deal for General Atomics MQ-9B drones to India. This deal underscores the strengthening of defense and security cooperation between Washington and New Delhi. The proposed package for the Indian military encompasses 31 SkyGuardian unmanned aerial vehicles, 310 Small Diameter Bombs, and 170 Hellfire missiles. The package includes radars and anti-submarine equipment for the maritime-focused SeaGuardian variant.

India is making notable strides in aerospace and defense production, driving opportunities in the studied market. For instance, recently, Adani-Elbit Advanced Systems India Ltd, India's inaugural private UAV manufacturing facility, successfully delivered over 20 Hermes 900 medium-altitude, long-endurance (MALE) UAVs to Israel. This joint venture, based in Hyderabad and formed between India's Adani Defence and Aerospace and Israel's Elbit Systems, proudly stands as the first entity to produce these UAVs outside of Israel.

Other countries are witnessing similar trends. For example, China is actively bolstering its UAV capabilities. According to the Civil Aviation Administration of China (CAAC), by the end of 2023, China boasted 1.27 million registered drones, marking a 32.2% increase from the prior year. Consequently, these trends and advancements are poised to fuel the growth of the market studied in the region during the forecast period.

Fiber Optic Gyroscope Industry Overview

The fiber optic gyroscope market features a moderate level of competition, with several key players at the forefront. A select few of these players currently hold a dominant position in terms of market share. The swift ascent of unmanned vehicles, coupled with ongoing technological advancements, presents enticing opportunities for market vendors. While the competitive rivalry among established players remains moderate, companies are leveraging innovation strategies to drive market demand. However, challenges such as intricate and time-intensive manufacturing processes, substantial investments, and a low cost-benefit ratio have deterred new entrants from producing fiber optic gyroscopes. Some key market players include Emcore, Honeywell, and Safran.

June 2024: Exail clinched a significant deal with Rheinmetall, agreeing to deliver 1004 units of its Advans Ursa inertial navigation systems (INS) for the German Army's Caracal 4X4 vehicles. Leveraging Exail's advanced Fiber-Optic Gyroscope (FOG) technology, the Advans Ursa stands out as a compact and budget-friendly INS specifically designed for tactical navigation. This system ensures accurate and dependable navigation data, even in challenging conditions. As a result, Caracal vehicles can confidently navigate without any constraints, regardless of time or distance, even in scenarios where GNSS signals are entirely absent.

June 2024: Inertial Labs has unveiled its newest offering, the INS-FI. This GPS-assisted Inertial Navigation System (INS) leverages Tactical-grade Fiber Optic Gyroscope (FOG) technology, positioning it as one of the market's most sophisticated and dependable INS solutions. It boasts a multi-band GNSS receiver compatible with all constellations, including GPS, GALILEO, GLONASS, QZSS, NAVIC, and BEIDOU.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of Macroeconomic Trends on the Fiber Optic Gyroscope Market

5 MARKET DYNAMICS

5.1 Marker Drivers

5.1.1 Rapid Growth of Unmanned Vehicle in Defense and Civilian Applications

5.1.2 Expanding Defense Expenditure Globally

5.2 Market Restraints

5.2.1 Substantial Rise in Complexity Challenging the Market Demand

5.2.2 Increasing Demand for Advanced Microelectromechanical Systems Gyroscopes