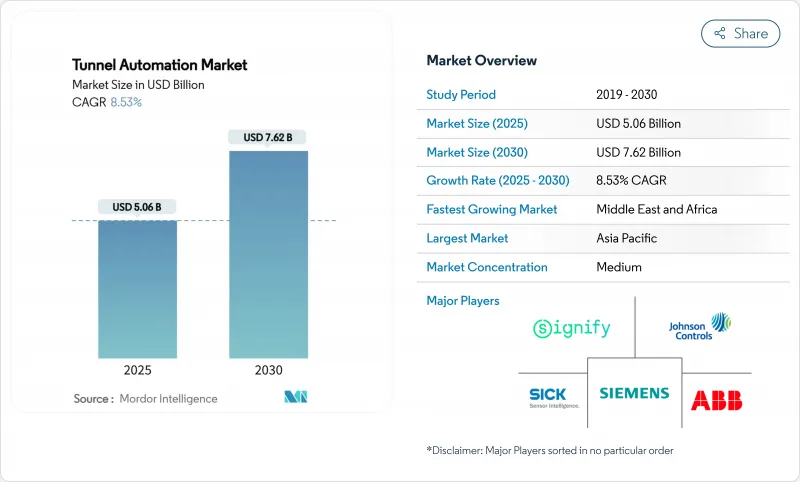

터널 자동화 시장 규모는 2025년에 50억 6,000만 달러에 이르고, 2030년에는 76억 2,000만 달러에 달할 것으로 예상됩니다.

규제 강화, IoT 대응 감시 제어 및 데이터 수집(SCADA) 플랫폼의 보급, 운송 회랑에 대한 공적 자금의 지속적인 투입이 터널 자동화 시장의 성장 궤도를 강화하고 있습니다. 하드웨어 구성 요소는 여전히 필수적이지만 시장은 유지 보수를 간소화하고 실시간 의사 결정을 보장하며 숙련된 노동자 부족을 보완하는 소프트웨어 풍부한 데이터 구동 솔루션으로 빠르게 전환하고 있습니다. 또, 유연한 자금 조달 모델(특히 에너지·퍼포먼스 계약)도, 자본 지출을 보증된 운전 절약으로 바꾸는 것으로 채용을 확대하고 있습니다. 동시에 사이버 보안 및 데이터 프라이버시 기준이 강화됨에 따라 운영자는 연결된 자산 전체에 보안 설계 아키텍처를 통합하도록 요구되고 있습니다.

세계 정책 프레임워크로 인해 터널 자동화 시장의 도입 곡선이 가속화되고 있습니다. 미국의 국가 터널 검사 기준에서는 2년마다 검토가 의무화되고 있으며, 사업자는 자동 안전 시스템의 도입을 강요하고 사실상 강제적인 교환 주기를 형성하고 있습니다. 유럽 횡단 교통망 내의 유사한 지침은 브렌너 기저 터널과 같은 프로젝트에 5,000만 톤의 화물을 도로에서 철도로 이동시킬 수 있는 고급 모니터링을 채택하도록 의무화하고 있습니다. 중국의 감독 기관은 현재 아마야마 승리 터널의 사내 자동화 기술에 의해 입증된 바와 같이 새로운 고속도로 전체에서 지능적인 관리를 요구하고 있습니다. 이러한 지침의 누적 효과는 자본 예산을 일반적인 연기 사이클로부터 보호하는 컴플라이언스 주도의 대규모 지출 풀입니다.

실시간 분석을 통해 운영자는 터널 가동 중지 시간을 최대 40%까지 줄이고 장비 수명을 연장하고 예측 보전 전략과 운영을 일치시킬 수 있습니다. 스페인 솜포트 터널의 지멘스 업그레이드는 SIMATIC WinCC OA와 중복된 S7-1500H PLC를 통합하여 긴급 상황과 자산 관리를 통합했습니다. 첨단 클라우드 플랫폼은 공기 품질 및 장비 데이터 패턴에 머신러닝 알고리즘을 적용하지만 악의적인 행위자의 공격 대상도 확대하고 있습니다. 이 지식 격차를 메우기 위해서는 유지 보수 작업자의 재교육과 운영 기술(OT)과 IT 모범 사례를 일치시키는 사이버 보안 거버넌스 모델의 공식화가 필요합니다.

종합적인 자동화에는 많은 양의 자본이 필요하며 특히 레거시 터널에서는 맞춤형 리노베이션 설계와 단계적 롤아웃이 필요하므로 일정이 최대 2년까지 연장 될 수 있습니다. 미국 연방 정부의 넷 제로 대응 시설의 P100 기준은 기본 사양과 초기 예산을 증가시킵니다. 에너지 성능 계약은 이러한 비용을 부분적으로 상쇄합니다. 존슨 컨트롤스의 580만 달러의 코브 카운티 프로그램은 206만 달러의 광열비 절감을 창출하고 성능 보증이 새로운 자금 조달 경로를 풀 수 있음을 입증합니다. 전문 기술자의 지속적인 부족은 통합 작업의 흐름을 더욱 복잡하게 만듭니다.

2024년 터널 자동화 시장의 46.4%는 하드웨어가 차지하며, 이는 센서, 컨트롤러 및 전력 인프라의 기본적인 필요성을 반영했습니다. 그러나 소프트웨어는 예지보전과 자율적 의사결정을 촉진하는 AI 대응 애널리틱스에 힘입어 CAGR 9.8%로 다른 모든 제품을 능가합니다.

헬렌크네히트의 커넥티드 플랫폼은 TBM의 성능을 전 세계적으로 추적하고 다운타임을 줄이는 실시간 인사이트를 제공함으로써 이러한 전환을 설명합니다. 설치, 교정, 수명주기 관리 등의 서비스가 포트폴리오를 구성하고 운영자가 전문 지식을 아웃소싱함에 따라 경상 수익 점유율이 증가하고 있습니다.

조명과 전원 시스템의 점유율은 38.5%로 에너지 효율적인 LED와 스마트 전원 제어의 중요성을 강조하고 있습니다. 안전·화재 감지 센서는 사고 방지 규제의 엄격화에 따라 CAGR 9.4%로 성장을 견인할 것으로 예측됩니다.

아시아에서 가장 긴 도로 터널에 설치된 ABB의 가변 속도 환기 드라이브는 에너지 비용을 줄이면서 공기 품질 관리를 강화하는 구성 요소 통합의 예입니다. 멀티 파라미터 센서의 보급으로 이전에는 불가능했던 실시간 구조 건전성 모니터링이 가능합니다.

아시아태평양이 터널 자동화 시장에서 42.5%의 점유율을 차지하고 있는 것은 끊임없는 설비 투자, 국가가 추진하는 산업 정책, 인더스트리 4.0 규범의 광범위한 수용에 기인합니다. 중국 규모의 이점은 건설 사이클의 단축을 가능하게 하고, 신강 위구르 자치구의 아마야마 승리 터널에서 입증된 바와 같이 대규모 자동화를 통해 프로젝트 리드 타임을 거의 절반으로 단축하고 있습니다. 싱가포르의 창이 프로젝트는 항공 인프라와 최첨단 터널 시스템의 통합에서 지역의 숙련도를 강조하는 것이며, 호주 자율 TBM은 기술적 성숙도를 확인합니다. 관민 파트너십은 표준이며 사업자의 인센티브를 장기적인 에너지와 안전 목표에 부합시키는 것입니다.

중동은 CAGR 10.9% 전망으로 급속한 상승을 계속하고 있습니다. 사우디아라비아의 '비전 2030'은 로봇 제조, 인공지능 모니터링, 탄소 중립 목표가 집약된 대규모 스마트 시티 회랑을 조성하고 있습니다. 카타르 철도 건설과 아랍에미리트(UAE) 지하철망은 IoT 센서를 사전 설치한 모듈식 터널 포장를 도입하여 현장 설정을 줄였습니다. 경쟁 조달의 틀에서는 턴키로 완전히 통합된 생태계를 제공할 수 있는 공급업체가 우선합니다.

유럽은 엄격한 컴플라이언스 체제와 국경을 넘어선 거대한 프로젝트에 힘입어 신중한 성장을 유지하고 있습니다. 블렌너 기저 터널은 모달 이동을 목적으로 EU의 공동 출자를 받고 독일의 SudLink 전력 링크는 헬렌 쿠네히트의 TBM을 사용하여 송전망을 탈탄소화하는 전선관을 부설하고 있습니다. 브라운필드 리노베이션이 주류이며, 특히 LED 교체는 60%의 에너지 절약을 달성했습니다.

The tunnel automation market size reached USD 5.06 billion in 2025 and is projected to attain USD 7.62 billion by 2030, reflecting an 8.53% CAGR and underscoring the rising demand for integrated, safety-compliant infrastructure upgrades around the world.

Intensifying regulatory mandates, widespread adoption of IoT-enabled supervisory control and data acquisition (SCADA) platforms, and sustained public-sector funding for transportation corridors are reinforcing the growth trajectory of the tunnel automation market. Hardware components remain indispensable, yet the market is rapidly pivoting toward software-rich, data-driven solutions that streamline maintenance, ensure real-time decision-making, and offset skilled labor shortages. Flexible financing models-especially energy-performance contracting-are also expanding adoption by converting capital expenditure into guaranteed operational savings. At the same time, heightened cyber-security and data-privacy standards are prompting operators to embed secure-by-design architectures across connected assets.

Worldwide policy frameworks are accelerating the adoption curve of tunnel automation market deployments. The US National Tunnel Inspection Standards require biennial reviews and force operators to introduce automated safety systems, effectively creating a mandatory replacement cycle. Comparable directives within the Trans-European Transport Network compel projects like the Brenner Base Tunnel to employ advanced monitoring that can shift 50 million tonnes of freight from road to rail.Legislated targets for energy savings add an environmental dimension by encouraging LED lighting retrofits and high-efficiency ventilation. China's oversight bodies now require intelligent management across new expressways, as demonstrated by the Tianshan Shengli Tunnel's in-house automation technology. The cumulative effect of these mandates is a sizeable, compliance-driven spending pool that shields capital budgets from typical deferment cycles.

Real-time analytics allow operators to reduce tunnel downtime by up to 40%, extending equipment life and aligning operations with predictive maintenance strategies. Siemens' upgrades at Spain's Somport Tunnel merged SIMATIC WinCC OA with redundant S7-1500H PLCs, delivering unified emergency and asset management. Advanced cloud platforms apply machine-learning algorithms to patterns in air-quality and equipment data, yet also widen the attack surface for malicious actors. Bridging this knowledge gap requires reskilling maintenance crews and formalizing cyber-security governance models that align operational technology (OT) with IT best practices.

Comprehensive automation requires significant capital, especially where legacy tunnels demand bespoke retrofit designs and phased rollouts that can stretch timelines by up to two years. US federal P100 standards for net-zero-ready facilities increase baseline specifications and thus initial budgets. Energy-performance contracts partly offset these costs; Johnson Controls' USD 5.8 million Cobb County program generated USD 2.06 million in utility savings, proving that guaranteed performance can unlock new funding channels. Persistent shortages of specialist technicians further complicate integration workstreams.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware accounted for 46.4% of the tunnel automation market in 2024, reflecting the foundational need for sensors, controllers, and power infrastructure. Software, however, is set to outpace all other offerings with a 9.8% CAGR, propelled by AI-enabled analytics that facilitate predictive maintenance and autonomous decision-making.

Herrenknecht's Connected platform illustrates the transition by tracking TBM performance globally and providing real-time insights that cut downtime. Services-installation, calibration, and lifecycle management-round out the portfolio and embody a rising share of recurring revenue as operators outsource expertise.

Lighting and power supply systems dominated with 38.5% share, emphasizing the importance of energy-efficient LEDs and smart power controls. Safety and fire-detection sensors are forecast to lead growth at 9.4% CAGR, aligned with stricter incident-prevention regulations.

ABB's variable-speed ventilation drives inside Asia's longest road tunnel exemplify component integration that enhances air-quality management while cutting energy costs ABB. The rising proliferation of multi-parameter sensors enables real-time structural health monitoring that was previously unattainable.

The Global Tunnel Automation Market Report is Segmented by Offering (Hardware, Software, Services), Component (Lighting and Power Supply, Signalization and Control, and More), Automation Level (Semi-Automated, Fully-Automated), Application (Traffic Management and SCADA, and More), Tunnel Type (Roadways and Highways, Railways and Metros, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's 42.5% hold on the tunnel automation market stems from relentless capital investment, state-backed industrial policies, and the widespread embrace of Industry 4.0 norms. China's scale advantage enables shorter construction cycles, cutting project lead-times nearly in half through extensive automation, as demonstrated in Xinjiang's Tianshan Shengli tunnel. Singapore's Changi project underscores regional proficiency in integrating aviation infrastructure with state-of-the-art tunnel systems, while Australia's autonomous TBMs confirm technical maturity. Public-private partnerships are standard, aligning operator incentives with long-run energy and safety objectives.

The Middle East is on a rapid ascent with a 10.9% CAGR outlook. Saudi Arabia's Vision 2030 subsidizes large-scale, smart-city corridors where robotic fabrication, AI-assisted monitoring, and carbon-neutral targets converge. Qatar's rail build-out and the UAE's metro networks deploy modular tunnel packages that are pre-fitted with IoT sensors, reducing on-site configuration. Competitive procurement frameworks prioritize vendors that can deliver turnkey, fully integrated ecosystems.

Europe sustains measured growth supported by strict compliance regimes and cross-border megaprojects. The Brenner Base Tunnel attracts EU co-funding for modal-shift objectives, while Germany's SudLink electricity link uses Herrenknecht TBMs to lay power conduits that decarbonize the grid. Brownfield retrofits dominate, particularly LED replacements that achieve documented 60% energy savings.