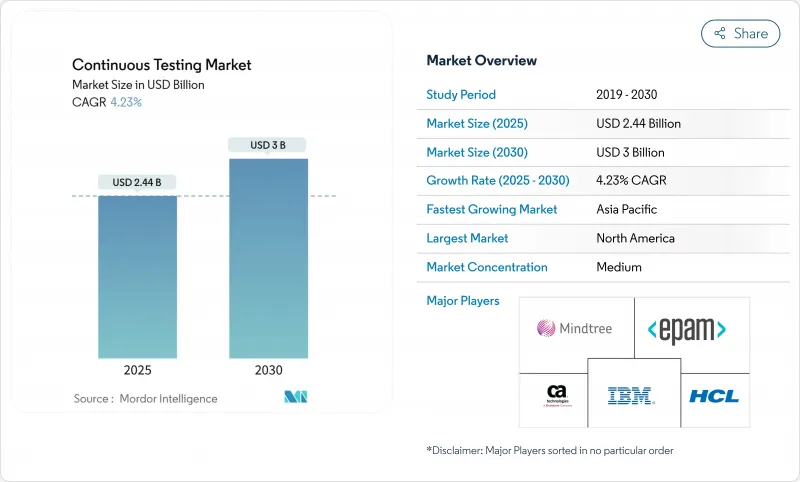

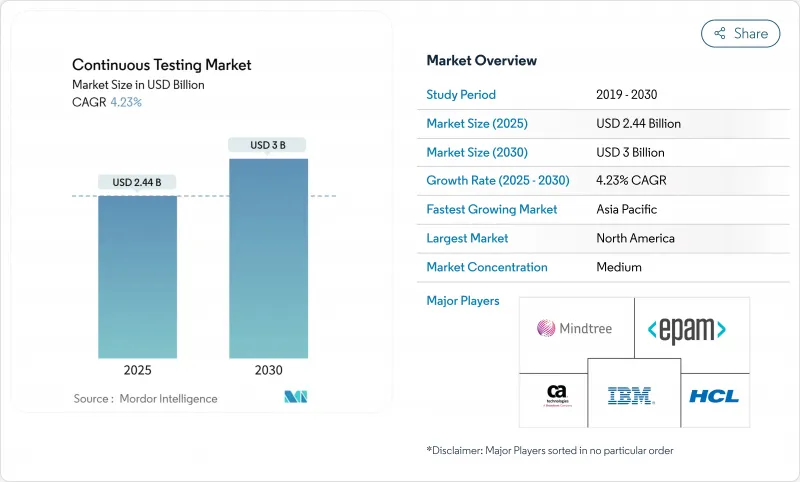

지속적 테스트 시장 규모는 2025년에 24억 4,000만 달러로 추정되고, 2030년에는 30억 달러에 이를 전망이며, CAGR 4.2%로 확대될 것으로 예측됩니다.

그 배경에는 지속적 테스트 시장이 전통적인 품질 보증 워크플로우에서 AI가 지원하는 컴플라이언스 중심 에코시스템으로 전환하고 있는 것이 있습니다. 68% 이상의 기업이 품질 엔지니어링 프로세스에 생성형 AI를 통합하고 있습니다. DevOps 채용 기업의 약 절반만이 테스트 자동화의 완전한 통합을 실현하고 있음에도 불구하고, CAGR 20.1%로 성장하는 DevOps를 배경으로 그 기세는 더욱 강해지고 있습니다. 기술 부족이 테스트 환경 오케스트레이션의 외부화를 추진하는 동안 관리 서비스 파트너십이 활발한 반면, 기능 테스트 및 보안 테스트의 조합은 유럽의 새로운 사이버 탄력성 법(Cyber Resilience Act) 마일스톤에 따라 재조정되었습니다. 지리적 리더십은 북미에 있지만 아시아태평양의 CAGR은 5.0%로 제조업, 은행, 소매업의 디지털화가 급속히 진행됨에 따라 그 차이는 줄어들고 있습니다.

DevOps의 사례는 현재 주류이지만, 지속적 테스트에는 여전히 부족한 기술이 필요하기 때문에 테스트 격차가 커지고 있습니다. DevOps와 지속적 테스트를 결합한 기업은 AI가 생성하는 테스트 케이스가 감사 추적을 유지하면서 릴리스 사이클을 단축하는 규제가 있는 은행 환경에서 20%의 생산성 향상을 보고합니다. 테스트 커버리지의 책임이 개발 팀 전체로 이동하는 품질 엔지니어링 모델로 전환함에 따라 기존 QA 기능의 역할이 줄어들고 있습니다. 분석가는 2027년까지 모든 테스트 워크플로우의 90%가 자동화될 것으로 예상하고 있으며, AI 보증 엔지니어 및 모델 트레이너에 대한 수요가 증가하고 있습니다. Nationwide Building Society와 같은 조직은 애자일 증분 초기에 테스트를 통합한 결과, 보다 신속한 변화 전달 및 높은 고객 만족도 점수를 얻은 결과를 보여줍니다.

디지털 채널로의 급속한 전환으로 기업은 이전의 속도로 소프트웨어를 출시해야 하며, 종종 품질 가드 레일이 늘어나고 있습니다. 라틴아메리카의 기업들은 완전한 회귀주기 없이 코드가 푸시됨으로써 결함 유출이 증가한다는 것을 경험하고 있습니다. 한 세계 체인에서는 하루 1만 건의 주문을 '파이브나인' 가동률로 지원하면서 전환을 4.5포인트 개선했습니다. 제조업의 리더은 스마트 팩토리의 경쟁력이 소프트웨어의 품질에 달려 있다고 말하고 있지만, AI의 시험 운용이 확장할 수 없는 경우, 야망은 종종 정체되어 개념 실증과 기업 전개의 교량을 할 수 있는 플랫폼 레벨에서 테스트 프레임워크의 필요성이 부각되고 있습니다.

미국의 노동 시장 데이터에 따르면 QA의 결원은 2032년까지 17% 증가할 전망이며, 이대로 직무가 수행되지 않으면 연간 1,620억 달러의 생산고가 위험에 노출될 가능성이 있습니다. CI/CD 파이프라인, 클라우드 인프라, AI 주도 테스트 자동화를 통합할 수 있는 전문가의 부족은 심각합니다. 인력 부족을 보완하기 위해 기업은 관리 서비스와 무선 테스트 플랫폼을 조달하여 기술력이 낮은 직원의 진입 장벽을 낮추고 있습니다. 자동화를 통해 반복적인 작업은 제거되지만 AI 모델의 큐레이션, 바이어스 감사, 데이터 유출에 대한 파이프라인 보호가 가능한 아키텍트에 대한 수요는 증가하고 있습니다.

매니지드 서비스는 2024년에 지속적 테스트 시장의 67.8%를 차지하였고, 2030년까지 CAGR 5.8%로 성장이 예측됩니다. 외부 파트너에 대한 의존도가 증가하고 있는 이유는 규제 기준의 엄격화에 대응해야 하는 복잡한 AI 대응 테스트 에스테이트를 실행하기 위한 사내 용량이 제한되어 있기 때문입니다. 프로바이더는 기존의 수작업에 의한 테스트 담당자가 아니라 AI 보증 엔지니어나 모델 거버너를 채용하여 포지션을 바꾸고 있습니다. 권고 및 전문 서비스 라인은 아웃소싱 문제를 보완하고 품질 엔지니어링 및 CloudOps 매칭을 위한 문화적 전환을 통해 고객을 안내합니다.

관리형 서비스 모델은 현재 기본 테스트 실행에 그치지 않고 전반적인 품질 인텔리전스로 확장되고 있으며 공급자는 릴리스 속도, 위험 분석 및 에너지 효율적인 테스트 스케줄링을 보장합니다. 호주 및 뉴질랜드에서 클라우드 마이그레이션 및 데이터 현대화 워크스트림을 번들하는 기업은 하이브리드 워크로드를 다루기 위해 전문가를 재고용하고 있습니다. 이러한 폭이 넓어짐에 따라 기존 기업은 성장이 가속되어도 점유율을 유지할 수 있으며, 매니지드 서비스는 지속적 테스트 시장의 구조적인 지주가 되고 있습니다.

웹 애플리케이션은 2024년 기준에서 58.2%의 점유율을 차지했으며, 가장 큰 인터페이스 등급이었지만, 모바일 테스트는 2030년까지 연평균 복합 성장률(CAGR)로 최고 5.5%를 기록하는 기세입니다. 스마트폰 주도의 상거래는 2027년까지 세계 소매 매출의 대부분을 차지할 것으로 예측되고 있으며, 분산 장치의 조경에는 엄격한 성능과 사용성이 요구됩니다. 기업은 클라우드 호스트 디바이스 팜, 네트워크 조건 에뮬레이션, AI 기반 비주얼 검증을 채택하여 수천 개의 모바일 기기 순열에 걸쳐 브랜드 일관성을 유지하고 있습니다.

브라우저의 표준은 블록체인과 에지 서비스를 융합시킨 분산형 Web 4.0 구조로 진화하고 있으며, 상태의 지속성과 API 레이어의 내결함성에 대한 새로운 접근이 요구되고 있습니다. 데스크톱 테스트는 레거시 비즈니스 프로세스 플랫폼에 여전히 중요하지만 자본 배분은 낮습니다. 전반적으로 인터페이스의 다양화는 교차 채널 테스트 데이터, 성과물 및 분석을 단일 유리 페인으로 관리할 수 있는 통합 오케스트레이션의 필요성을 강화합니다.

지속적 테스트 시장 보고서는 서비스 유형별(관리 서비스 및 전문 서비스), 인터페이스별(웹, 데스크톱, 모바일), 전개 모드별(온프레미스 및 클라우드), 테스트 유형별(기능 테스트, 성능 및 부하 테스트 등), 조직 규모별(대기업 및 중소기업), 업계별(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 기타), 지역별로 분류됩니다.

북미는 2024년 매출의 26.5%를 차지했으며, DevOps의 조기 도입, 견고한 클라우드 인프라, 품질 엔지니어링 플랫폼에 대한 왕성한 벤처 자금으로부터 혜택을 누리고 있습니다. 일반 AI의 채택은 널리 퍼져 있으며 96%의 기업이 테스트 생성 및 최적화 워크플로우에서 AI를 시험적으로 도입하거나 확장하고 있습니다. 기술 리더십에도 불구하고 이 지역은 심각한 인력 부족으로 고통받고 있으며, 관리 서비스 계약 및 자동화 툴체인에 대한 의존도가 높아지고 있습니다. 미국 은행은 위험 기반 회귀 팩을 권장하는 AI 에이전트를 통합한 결과 2자리 생산성 향상을 보고했습니다.

아시아태평양은 가장 급속히 확대되고 있는 지역으로, 2030년까지 CAGR 5.0%로 성장이 예측되고 있습니다. 중국, 인도, 동남아시아 국가들은 스마트 제조 및 핀테크 생태계에 자본을 주입하고 지속적인 품질 자동화를 위한 그린필드 기회를 창출하고 있습니다. 호주 및 뉴질랜드에서는 기업이 SAP S/4HANA 업그레이드, API 근대화, 부서별 컴플라이언스 보고서 작성 등의 전문 지식을 요구하기 때문에 외부 위탁 테스트가 부활하고 있습니다. 이 지역에서는 2033년까지 380만 명의 제조업 종업원이 새로 필요할 것으로 예상되고 있으며, 확장 가능하고 오버헤드가 적은 테스트 프레임워크에 대한 수요가 높아지고 있습니다.

유럽은 지속적 테스트를 사실상 의무화하는 규제 환경에 의해 형성된 중진 상태로 남아 있습니다. 2024년에 채택된 사이버 탄력성 법(Cyber Resilience Act)과 2025년에 발효된 디지털 오퍼레이션 탄력성 법(Digital Operational Resilience Act)은 각각 제조업체와 금융기관에 지속적인 보안 검증을 실증할 것을 의무화하고 있습니다. 독일, 프랑스, 영국은 수작업을 최소화하면서 CRA와 DORA 지표를 모두 충족할 수 있는 AI를 활용한 컴플라이언스 자동화에 대한 기업 지출을 선도하고 있습니다. EU 제조물 책임 지침의 개정과 같은 보완적인 법률은 소프트웨어 결함에 대한 책임을 강화하고 품질을 엔지니어링의 뒷받침이 아니라 이사회 수준의 책임으로 취급하는 지속적 테스트와 시장 침투를 촉진합니다.

The continuous testing market size is valued at USD 2.44 billion in 2025 and is forecast to reach USD 3 billion by 2030, expanding at a 4.2% CAGR.

Behind the measured headline rate, the continuous testing market is shifting from traditional quality-assurance workflows to AI-supported, compliance-centric ecosystems. More than 68% of enterprises have already embedded generative AI into quality-engineering processes. Momentum is reinforced by a wider DevOps backdrop growing at a 20.1% CAGR, although only about half of DevOps adopters have achieved full test-automation integration, signalling untapped headroom inside existing pipelines. Managed service partnerships are thriving as skill shortages drive externalisation of test-environment orchestration, while the functional-to-security testing mix is recalibrating in response to new European Cyber Resilience Act milestones. Geographic leadership remains with North America, yet Asia-Pacific's 5.0% CAGR trajectory suggests a narrowing gap as manufacturers, banks, and retailers digitise at speed.

DevOps practices are now mainstream, yet sizeable testing gaps persist because continuous testing requires skills that remain scarce. Enterprises that combine DevOps with continuous testing report productivity gains of 20% in regulated banking environments where AI-generated test cases compress release cycles while maintaining audit trails. The role of the traditional QA function is shrinking as companies transition toward quality-engineering models in which responsibility for test coverage shifts to the entire development squad. Analysts expect 90% of all testing workflows to become automated by 2027, elevating demand for AI-assurance engineers and model trainers. Organisations such as Nationwide Building Society illustrate the payoff, citing faster change delivery and higher customer-satisfaction scores after embedding testing earlier in agile increments.

A rapid pivot to digital channels has forced enterprises to release software at unprecedented speed, often stretching quality guardrails. Latin American firms have experienced heightened defect leakage when code is pushed without complete regression cycles. Retailers are scaling AI-guided user-acceptance testing to safeguard 24/7 e-commerce uptime, with one global chain improving conversion by 4.5 percentage points while supporting 10,000 daily orders at "five-nine" availability. Manufacturing leaders say smart-factory competitiveness hinges on software quality, yet ambitions frequently stall when AI pilots cannot be scaled, underscoring the need for platform-level testing frameworks capable of bridging proof-of-concept and enterprise rollout.

U.S. labour-market data show QA vacancies on course to grow 17% through 2032, potentially placing USD 162 billion of annual output at risk if roles remain unfilled. The gap is acute for specialists who can weave CI/CD pipelines, cloud infrastructure and AI-driven test automation into a cohesive fabric. To offset shortages, enterprises are procuring managed services and codeless test platforms that lower entry barriers for less technical staff. Automation eliminates repetitive tasks but raises demand for architects able to curate AI models, audit bias and safeguard pipelines against data exposure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Managed services captured 67.8% of the continuous testing market in 2024 and are forecast to grow at a 5.8% CAGR through 2030. Heightened reliance on external partners stems from limited in-house capacity to run complex, AI-enabled test estates that must meet tightening regulatory standards. Providers are repositioning, hiring AI-assurance engineers and model governors rather than traditional manual testers. Advisory and professional-services lines complement outsourcing deals, guiding clients through cultural shifts toward quality engineering and CloudOps alignment.

The managed-services model now extends beyond basic test execution to holistic quality intelligence, with providers guaranteeing release velocity, risk analytics, and energy-efficient test scheduling. Renewed demand is visible in Australia and New Zealand, where enterprises bundling cloud migration and data-modernisation workstreams are re-engaging specialists to maintain coverage across hybrid workloads. Such breadth enables incumbents to defend their share even as growth accelerates, making managed services the structural anchor of the continuous testing market.

Web applications remained the largest interface class with a 58.2% share in 2024, but mobile testing is on track for the highest 5.5% CAGR to 2030. Smartphone-led commerce, forecast to comprise a dominant slice of global retail sales by 2027, places rigorous performance and usability demands on distributed device landscapes. Enterprises are adopting cloud-hosted device farms, network-condition emulation, and AI-based visual validation to uphold brand consistency across thousands of handset permutations.

Web testing is hardly static; browser standards are evolving toward decentralized Web 4.0 constructs that blend blockchain and edge services, which in turn mandate new approaches to state persistence and API-layer fault tolerance. Desktop testing remains relevant for legacy business-process platforms, yet receives lower capital allocation. Overall, interface diversification is reinforcing the need for unified orchestration that can manage cross-channel test data, artefacts, and analytics inside a single pane of glass.

The Continuous Testing Market Report is Segmented by Service Type (Managed Services and Professional Services), Interface (Web, Desktop, and Mobile), Deployment Type (On-Premise and Cloud), Testing Type (Functional Testing, Performance and Load Testing, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (BFSI, IT and Telecom, and More) and Geography.

North America accounted for 26.5% revenue in 2024, benefiting from early DevOps uptake, robust cloud infrastructure, and strong venture funding into quality-engineering platforms. Generative AI adoption is widespread, with 96% of enterprises piloting or scaling AI in test generation and optimisation workflows. Despite technology leadership, the region contends with acute talent shortages, prompting higher reliance on managed-service engagements and automated toolchains. U.S. banks report double-digit productivity gains after embedding AI agents that recommend risk-based regression packs, balancing rapid feature delivery against strict regulatory demands.

Asia-Pacific is the fastest-expanding theatre, registering a projected 5.0% CAGR to 2030. China, India, and Southeast Asian nations are channelling capital into smart manufacturing and fintech ecosystems, creating greenfield opportunities for continuous quality automation. Australia and New Zealand showcase a resurgence in outsourced testing as enterprises hunt for expertise that spans SAP S/4HANA upgrades, API modernisation, and sector-specific compliance reporting. An expected 3.8 million additional manufacturing employees will be required across the region by 2033, magnifying demand for scalable, low-overhead testing frameworks.

Europe remains a heavyweight, shaped by a regulatory environment that effectively mandates continuous testing. The Cyber Resilience Act, adopted in 2024, and the Digital Operational Resilience Act, effective in 2025, oblige manufacturers and financial institutions, respectively, to demonstrate ongoing security validation. Germany, France, and the United Kingdom spearhead enterprise spending on AI-enabled compliance automation that can satisfy both CRA and DORA metrics while minimizing manual effort. Complementary legislation such as the revised EU Product Liability Directive heightens liability for software defects, encouraging continuous testing and market penetration that treats quality as a board-level responsibility rather than an engineering afterthought.