유럽의 AMH(자동 자재관리) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe AMH - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1629806

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

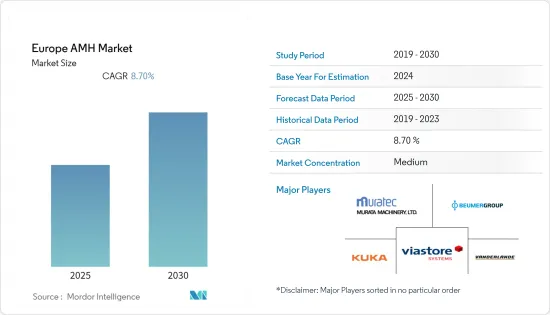

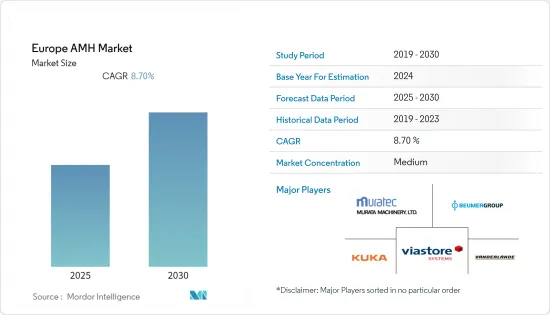

유럽의 AMH(자동 자재관리) 시장, 예측 기간 동안 CAGR 8.7% 기록할 것으로 예상됩니다.

주요 하이라이트

영국과 유럽 전역에서 정치, 경제, 기술 발전은 제조업의 성장에 비례적으로 영향을 미치고 있으며, BREXIT 투표는 모든 산업에 충격을 주었지만 제조업은 긍정적인 영향을 미치고 있습니다.

유럽은 인더스트리 4.0 혁명에 대한 투자 증가로 산업 자동화를 가장 많이 도입한 국가로, CBI 외무부에 따르면 유럽은 전 세계 인더스트리 4.0 투자의 3분의 1 이상을 차지하고 있습니다. 서유럽과 북유럽은 주요 시장이며, 특히 독일은 이 단어를 처음 만들어낸 선두주자입니다.

북유럽은 전통적으로 창고 자동화 분야에서 가장 발전된 시장입니다. 높은 인건비와 공장 내 작업 환경에 대한 특별한 배려로 인해 정교하고 높은 수준의 자동화를 채택하게 되었습니다. 스칸디나비아에서 System Logistics는 창고 관리, 피킹 및 자재 취급 작업을 효율적으로 관리하기 위해 식음료 부문의 중요한 고객들을 지원해 왔습니다.

또한 투자 관리 회사 JLL에 따르면 유럽 전역의 창고에서 사람과 기계가 점점 더 긴밀하게 협력하고 있으며, 효율적이고 숙련 된 인력 부족은 자동화를 더욱 가속화 할 수 있습니다.

COVID-19 봉쇄로 인해 전자 식료품 채널은 더욱 가속화되었습니다. 유럽 주요 시장에서는 2020년 50% 이상의 성장을 기록했으며, 효율적인 전자 식료품 주문 처리 솔루션에 대한 수요가 더욱 증가하고 있습니다. 이에 따라 KNAPP, Ocado, Swisslog, Takeoff Technologies, WITRON과 같은 기술 및 플랫폼 제공업체들은 소프트웨어와 하드웨어를 결합한 자동화 솔루션 포트폴리오를 지속적으로 확장하고 있습니다.

유럽의 AMH(자동 자재관리) 시장 동향

자동차, 큰 폭의 성장세 기록할 전망

유럽연합(EU)은 세계 최대 자동차 생산국 중 하나입니다. 이 부문은 R&D에 대한 민간 투자에서 가장 큰 규모를 자랑합니다. 자동차 산업의 경쟁력을 강화하고 기술 리더십을 유지하기 위해 유럽위원회는 세계 기술 조정을 지원하고 연구개발에 대한 자금 지원을 제안하고 있습니다.

또한 ACEA의 보고서에 따르면 유럽연합(EU)의 인구 1,000명당 자동차 보유량은 569대입니다. 룩셈부르크의 자동차 밀도는 EU에서 가장 높고(인구 1,000명당 694대), 라트비아는 EU 회원국 중 가장 낮으며, OICA는 2020년 유럽 승용차 판매량이 1,416만 대에 달할 것으로 예상했습니다.

영국의 자동차 공급망은 수요 주도형(차량 내 개인화 수준이 높아짐)으로 인해 OEM 공급업체는 유연성이 높은 자동화를 선택할 수밖에 없습니다. 이는 조사 대상 시장 내 자동차 부문의 성장으로 이어지고 있습니다.

자동차 제조 공정의 자동화 채택 증가, 디지털화 및 AI의 출현은 네덜란드 자동차 부문의 디지털화 수요를 촉진하는 주요 요인 중 일부입니다.

독일이 가장 큰 시장 점유율을 차지할 것으로 예상

독일의 자동차 산업은 세계 최대 규모의 제조업입니다. 독일 무역투자청(GTAI)에 따르면, 전 세계에서 생산되는 프리미엄 브랜드 자동차 중 70% 이상이 독일 OEM 생산입니다.

독일은 세계 최고의 자동 자재관리 솔루션 소비국입니다. 국제로봇연맹(IFR)의 최근 추정에 따르면, 독일은 한국, 일본 다음으로 로봇 밀도가 높다(근로자 1만 명당 294대).

자동차 산업뿐만 아니라 우편 및 소포 산업도 AMH의 성공에 기여하고 있습니다. 독일에 본사를 둔 지멘스 우편, 소포 및 공항 물류는 우편물 분류 시스템 세계 시장 리더입니다. 지멘스 기술이 적용된 2만 3,000대 이상의 시스템이 60여 개국에서 안정적으로 우편물을 분류하고 있습니다. 또한, 우편 및 소포 물류, 자동화, 수하물 및 화물 처리 등 공항 물류 분야의 혁신적인 제품과 솔루션을 제공하는 선도적인 기업이기도 합니다.

제약 부문도 자동화를 도입하고 있으며, 완만한 성장이 예상됩니다. 독일 제약 포장 대기업의 전략적 움직임은 병 대 물집, 유리 대 플라스틱 주사기 등 의약품 포장 트렌드에 초점을 맞추고 있으며, 이는 독일 내 포장기계 및 장비에 대한 수요 증가로 이어지고 있습니다.

유럽의 AMH(자동 자재관리) 산업 개요

유럽의 AMH(자동 자재관리) 시장은 경쟁이 치열하고 여러 대기업으로 구성되어 있습니다. 시장 점유율 측면에서 현재 몇몇 대기업이 시장을 독점하고 있습니다. 시장 점유율이 높은 이들 대기업들은 해외로 고객 기반을 확대하는 데 주력하고 있습니다. 이들은 시장 점유율과 수익성을 높이기 위해 전략적 공동 이니셔티브를 활용하고 있습니다. 또한, 이 시장에 진출한 기업들은 제품 역량을 강화하기 위해 유럽의 자동 자재관리 기술 관련 스타트업들을 인수하고 있습니다.

2021년 2월 - 식품 가공, 포장 및 자재 취급 분야의 세계적인 엔지니어링 장비 및 자동화 솔루션 제공업체인 듀라반트(Duravant LLC)가 네덜란드에 본사를 둔 포장기계, 팔레타이저 기계, 스트레치 식품 기계 및 팔레트 운반 시스템의 선두주자인 제조업체인 Votech GS B.V.를 인수했습니다.

2021년 7월 - ABB는 오늘 ASTI Mobile Robotics Group(ASTI)을 인수한다고 발표했습니다. ASTI는 자율 이동 로봇(AMR) 분야의 세계적인 선도기업으로, 자사의 소프트웨어 제품군을 통해 모든 주요 애플리케이션을 구현하는 광범위한 포트폴리오를 보유하고 있습니다. 광범위한 포트폴리오를 보유하고 있습니다. 이번 인수를 통해 ABB는 로봇 및 자동화 분야를 확장하고 차세대 유연한 자동화를 위한 완벽한 포트폴리오를 제공하는 유일한 기업으로 거듭나게 됐습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

COVID-19가 시장에 미치는 영향

시장 성장 촉진요인

창고 애플리케이션의 자동화의 광범위한 채용

자동화에 대한 정부 지원 정책

자동화와 자재관리 수요를 촉진하는 인더스트리 4.0 투자

시장 성장 억제요인

숙련 노동자의 부족

높은 초기 비용

밸류체인/공급망 분석

업계의 매력 - Porter's Five Forces 분석

신규 참여업체의 위협

구매자의 교섭력

공급 기업의 교섭력

대체품의 위협

경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

제품 유형별

하드웨어

소프트웨어

서비스

기기 유형별

이동 로봇

무인운반차(AGV)

자동 지게차

자동 견인/트랙터/예인

유닛 로드

조립 라인

특수 용도

자율 이동 로봇(AMR)

레이저 유도차

자동 창고(ASRS)(ASRS)

고정 통로(스태커 크레인 + 셔틀 시스템)

캐러셀(수평 캐러셀 + 수직 캐러셀)

수직 리프트 모듈

자동 컨베이어

벨트

롤러

팔레트

오버헤드

팔레타이저

기존(하이 레벨 + 로 레벨)

로봇

분류 시스템

최종사용자별

공항

자동차

식품 및 음료

소매/창고/배송센터/물류센터

일반 제조업

의약품

우편·소포

기타 최종사용자

국가별

영국

프랑스

이탈리아

독일

중유럽/동유럽

스페인

기타 유럽

제6장 경쟁 구도

기업 개요

SSI SCHAEFER AG

Daifuku Co. Limited

Kardex Group

Honeywell Intelligrated

Beumer Group GMBH & Co. KG

Vanderlande Industries BV

Murata Machinery Limited

TGW Logistics Group GmbH

KUKA AG

Witron Logistik

Mecalux SA

Viastore Systems GmbH

제7장 투자 분석

제8장 시장 전망

ksm

영문 목차

영문목차

The Europe AMH Market is expected to register a CAGR of 8.7% during the forecast period.

Key Highlights

Throughout the United Kingdom and Europe, political, economic, and technological developments are impacting the growth of the manufacturing industry proportionally. Although the BREXIT vote sent shockwaves across all industries, the manufacturing industry remained positive.

Europe has been the most prominent adopter of industrial automation, owing to increasing investments in the Industry 4.0 revolution. According to the CBI Ministry of Foreign Affairs, Europe accounts for more than one-third of the global Industry 4.0 investments. Western and Northern Europe are its main markets, especially Germany, where the term was originally coined and a frontrunner.

Northern Europe is traditionally the most developed market regarding the use of automation in warehouses. The high labor costs and special attention to the working conditions at the factory have prompted the adoption of sophisticated and advanced automation. In Scandinavia, System Logistics has supported important clients in the food and beverage sector in the efficient management of warehousing, picking, and material handling operations.

Moreover, in warehouses across Europe, man and machine are increasingly working more closely together, and a lack of efficient and skilled manpower could accelerate automation further, according to JLL, an investment management company.

The e-grocery channel accelerated further because of the COVID-19 lockdown. It grew by more than 50% growth in 2020 for key European markets, creating an even stronger need for efficient e-grocery fulfillment solutions. This has encouraged technology and platform providers such as KNAPP, Ocado, Swisslog, Takeoff Technologies, and WITRON to extend their ever-growing portfolio of automation solutions combining software and hardware.

Europe Automated Material Handling (AMH) Market Trends

Automotive is Expected to Register a Significant Growth

The European Union (EU) is among the world's biggest producers of motor vehicles. The sector represents the largest private investor in R&D. To strengthen the automotive industry's competitiveness and preserve its technological leadership, the European Commission supports global technological harmonization and offers to fund R&D.

Moreover, according to an ACEA report, The European Union counts 569 cars per 1,000 inhabitants. Luxembourg has the highest car density in the EU (694 per 1,000 people), and Latvia has the lowest among the EU members. The OICA also suggested that the total sales of passenger vehicles in Europe stood at 14.16 million in 2020.

The demand-driven nature of the automotive supply chain in the United Kingdom (involving increasing levels of personalization within a vehicle) is forcing suppliers of OEMs to opt for automation with greater levels of flexibility. This is leading to the growth of the automotive segment in the market studied.

The increasing adoption of automation in the automotive manufacturing process and the advent of digitization and AI are some of the primary factors driving the demand for digitalization in the automotive sector of the Netherlands.

Germany is Expected to Have the Largest Market Share

The German automotive industry has one of the largest manufacturing sectors in the world. According to the Germany Trade and Investment (GTAI) agency, of all premium brand vehicles produced globally, over 70% are German-OEM manufactured.

Germany is one of the major consumers of automated material handling solutions in the world. According to the recent estimates of the International Federation of Robotics (IFR), Germany has a high robot density (294 units per 10,000 workers), after countries, like South Korea and Japan.

In addition to the automotive industry, the post and parcel industry is also contributing toward the success of AMH in the country. Siemens Postal, Parcel, and Airport Logistics, headquartered in Germany, ranks as a global market leader for mail sorting systems. More than 23,000 systems, using Siemens technology, are reliably sorting mail in more than 60 countries. The company is also a leading provider of innovative products and solutions for mail and parcel logistics, automation, and airport logistics, including baggage and cargo handling.

The pharmaceutical sector is also adopting automation and is expected to record moderate growth. Strategic moves by the German pharmaceutical packaging giants are shedding light on drug packaging trends related to bottles vs. blisters and glass vs. plastic syringes, leading to a growth in the demand for packaging machinery and equipment in Germany.

Europe Automated Material Handling (AMH) Industry Overview

The European automated material handling market is highly competitive and consists of several major players. In terms of market share, few of the major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies are leveraging on strategic collaborative initiatives to increase their market shares and profitability. The companies operating in the market are also acquiring start-ups working on European automated material handling technologies to strengthen their product capabilities.

February 2021 - Duravant LLC, global engineered equipment and automation solutions provider to the food processing, packaging, and material handling sectors, acquired Votech GS B.V., a leading manufacturer of bag filling machines, palletizer machines, stretch hood machines, and pallet transport systems based in The Netherlands.

July 2021 - ABB today announced to acquire ASTI Mobile Robotics Group (ASTI), a leading global autonomous mobile robot (AMR) manufacturer with a broad portfolio across all major applications enabled by the company's software suite. The acquisition will expand ABB's robotics and automation offering, making it the only company to offer a complete portfolio for the next generation of flexible automation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Impact of Covid-19 on the Market

4.3 Market Drivers

4.3.1 Wide Adoption of Automation in Warehouse Applications

4.3.2 Supporting Government Policies for Automation

4.3.3 Industry 4.0 investments driving the demand for automation and material handling

4.4 Market Restraints

4.4.1 Shortage of Skilled Workforce

4.4.2 High Initial Costs

4.5 Value Chain / Supply Chain Analysis

4.6 Industry Attractiveness - Porters Five Forces Analysis

4.6.1 Threat of New Entrants

4.6.2 Bargaining Power of Buyers

4.6.3 Bargaining Power of Suppliers

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Product Type

5.1.1 Hardware

5.1.2 Software

5.1.3 Services

5.2 By Equipment Type

5.2.1 Mobile Robots

5.2.1.1 Automated Guided Vehicle (AGV)

5.2.1.1.1 Automated Forklift

5.2.1.1.2 Automated Tow/Tractor/Tug

5.2.1.1.3 Unit Load

5.2.1.1.4 Assembly Line

5.2.1.1.5 Special Purpose

5.2.1.2 Autonomous Mobile Robots (AMR)

5.2.1.3 Laser Guided Vehicle

5.2.2 Automated Storage and Retrieval System (ASRS)