아시아태평양의 자동 자재 취급 및 보관 시스템 : 시장 점유율 분석, 산업 동향 및 성장 예측(2025-2030년)

Asia Pacific Automated Material Handling And Storage Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1628851

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

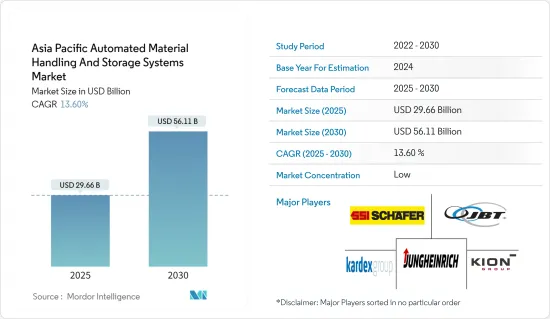

아시아태평양의 자동 자재 취급 및 보관 시스템 시장 규모는 2025년 296억 6,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 13.6%의 연평균 복합 성장률(CAGR)로 2030년에는 561억 1,000만 달러에 달할 것으로 예상됩니다.

재고관리단위(SKU)의 급격한 증가로 인해 도매업체와 유통업체는 정보에 입각한 비즈니스 의사결정을 내리는 것이 점점 더 어려워지고 있습니다. 이러한 딜레마는 보다 효율적인 인력, 장비 및 기술 활용의 절실한 필요성을 강조하고 있습니다. 자동 자재 취급 시스템의 필요성을 높이는 주요 요인으로는 비용 절감, 노동 효율성 향상, 공간 최적화 등이 있습니다.

시장 상황은 제품 유형이 급증하고 더 빈번하고 소량 배송에 대한 수요가 급증하는 것을 목격하고 있습니다. 자동화 된 배송 작업은 조직의 주문 정확도를 크게 향상시켜 종종 몇 퍼센트 포인트의 차이를 만들 수 있습니다. 아시아태평양 시장의 성장을 가속하는 요인은 도시화, 전자상거래의 급증, 기술 제공업체의 존재감입니다. 이들 업체들은 최첨단 솔루션을 제공하고 경쟁력을 유지하기 위해 연구 개발 노력을 강화하고 있습니다.

아시아태평양은 세계 전자상거래 강국으로서의 입지를 공고히 하고 있습니다. 중국, 인도, 인도네시아와 같은 국가에서 빠르게 성장하는 중산층과 모바일 기기에 대한 선호도가 맞물려 이 지역의 소매 전자상거래가 확대되면서 이러한 지위는 더욱 강화되고 있습니다. 특히 중국은 전 세계 소매 전자상거래 매출의 40%라는 놀라운 점유율을 차지하고 있습니다. 아시아태평양의 일부 국가에서는 창고 부지의 가용성이 감소하고 있으며, 이는 다층 시설과 더 높고 좁은 통로로의 전환을 촉진하고 있습니다. 이러한 변화는 첨단 자재 취급 시스템에 대한 수요를 촉진할 태세를 갖추고 있습니다.

자재 취급은 지난 70년 동안 기계와 로봇이 점점 더 많은 개별 작업자를 대체하면서 큰 진화를 거듭해 왔습니다. 이러한 변화는 산업의 형태를 변화시켰을 뿐만 아니라 기업의 성장에 박차를 가하고 있으며, 특히 자동차 산업에서 10배의 성장을 보이고 있습니다. 위스콘신 경제개발공사에 따르면, 인도와 같은 국가들은 자재관리 장비에 대한 투자가 두드러지며, MHE 시장은 인도 건설기계 산업의 약 13%를 차지하고 있습니다. 태국, 필리핀, 베트남 등 동남아시아 국가들은 제조업이 급성장하고 고용이 확대되고 가처분 소득이 증가하고 있습니다. 이러한 소득 증가와 국제 브랜드에 대한 인식이 높아지면서 현지 창고에 대한 수요가 증가하고 있습니다.

인도네시아는 산업 분야에서 로봇 활용이 눈에 띄게 증가하는 등 자동화를 빠르게 받아들이고 있는 국가로 눈에 띕니다. 일본이 공급국과 소비국이라는 두 가지 역할을 담당하고 있기 때문에 인도네시아는 무역 활동의 활성화로 이익을 얻을 수 있으며, 이는 이 지역의 자동화 수요를 더욱 촉진할 수 있습니다.

세계 산업계는 코로나19의 대유행과 그에 따른 가동 중단으로 인해 큰 혼란에 직면했습니다. 이러한 혼란은 공급망 문제, 원자재 부족, 노동력 부족, 가격 변동, 배송 병목 현상으로 이어져 생산 비용을 팽창시키고 예산을 초과할 수 있는 위험에 직면했습니다.

아시아태평양의 자동 자재 취급 및 보관 시스템 시장 동향

조립 라인 부문이 시장의 큰 폭의 성장을 확인합니다.

조립 라인 AGV는 자동차 제조, 마차 제조, 항공우주, 철도 및 기타 산업에서 주요 용도를 찾고 있습니다. 향후 몇 년동안 전기 및 하이브리드 자동차의 생산량 증가는 이러한 AGV에 대한 수요를 촉진할 것으로 보입니다. 이러한 변화는 제조업체의 유연성을 향상시킬 뿐만 아니라 안전하고 비용 효율적인 운영을 보장하면서 시장 변화에 빠르게 대응할 수 있게 해줍니다.

지난 10년간 자동차 산업은 전기차와 하이브리드 자동차의 채택으로 혁명을 일으켰습니다. 이러한 변화는 자동차 생산의 복잡성을 크게 증가시켰습니다. 진화하는 안전 규정 및 산업 표준과 함께 자동차 산업에서 자동화의 필요성이 증가하고 있습니다. 주요 우선순위에는 운송 중 인적 실수로 인한 제품 파손 감소, 워크스테이션 간 섀시 처리 속도 향상, 조립 라인 작업자와의 상호 작용 촉진 등이 포함됩니다. 이러한 요구 사항을 효과적으로 충족하는 조립 라인 AGV는 자동차 산업에서 자동화의 핵심이 되고 있습니다.

또한, 자동차 산업에서는 자동 조립 라인이 엔진과 기어박스에서 연료 시스템과 펌프에 이르기까지 다양한 부품을 생산하기 위해 자동 조립 라인을 활용하고 있습니다. 로봇 공학 및 시각 기술을 활용하여 제조업체는 인체공학적이고 효율적인 제품 라인을 구축하여 신속한 조립을 보장하는 동시에 인력을 위험한 상황으로부터 보호할 수 있습니다. 결과적으로 안전에 대한 우려는 자동차 산업 전반의 자동화를 촉진하고 있습니다.

Automotive Skill Development Council(ASDC)의 보고서 '자동차 부문의 인적 자원 및 기술 요구 사항(2026년)'에 따르면, 인도는 2026년까지 자동차 산업에서 4,508만 명의 인력을 고용할 것으로 예상됩니다. 이러한 인력 수요의 급증은 현재의 기술력에 대한 재평가를 요구하고 있으며, 자동차 설계, 로봇 공학, IoT, AI 등의 분야에서 기술 향상에 대한 필요성을 강조하고 있습니다. 전통적인 역할이 진화함에 따라 산업계는 자동화에 대한 추진력이 증가하고 있습니다.

이러한 수요 증가에 대응하기 위해 많은 시장 진출기업들이 제조 능력을 확장할 뿐만 아니라 새로운 제품 라인을 도입하고 있습니다. 예를 들어, 북미 자동화 엔지니어링 분야에서 유명한 Applied Manufacturing Technologies(AMT)는 2024년 3월 최신 혁신 제품인 ROBiN을 발표했습니다. 로봇 유도 시스템이라는 이름의 ROBiN은 창고 내 자재 취급에 혁명을 일으키고 효율성과 처리량 향상을 약속하는 것을 목표로 합니다. 첨단 자재 취급과 최첨단 자율 이동 로봇(AMR)으로 높은 평가를 받고 있는 AMT의 ROBiN은 업계에 큰 영향을 미칠 준비가 되어 있습니다.

인더스트리 4.0 투자로 자동화 및 자재 취급 수요를 촉진하는 인더스트리 4.0 투자

공항에 대한 투자는 세계 각국이 여행자들이 시간과 돈을 모두 사용할 수 있는 쾌적한 환경을 조성하는 것의 가치를 이해하고 있기 때문에 전 세계적으로 인정받고 있습니다. 체크인부터 탑승까지 모든 규모의 공항에서 널리 사용되는 컨베이어 및 분류 시스템은 프로세스를 효과적으로 간소화하고 전반적인 고객 경험을 향상시킵니다. 현재 많은 공항이 공급업체와 협력하여 자율 로봇을 도입하고 있는데, 이는 수하물 이동 효율을 높일 뿐만 아니라 운영 비용을 절감하기 위한 움직임이기도 합니다. 예를 들어, 물류 자동화 전문 업체인 반더랜드 네덜란드(Vanderlande Dutch)는 최근 홍콩 공항과 협력하여 자율형 수하물 운반 차량 검사 작업을 시작했습니다.

인도와 중국은 국내 항공 연결 증가와 1인당 GDP 증가에 힘입어 지역 항공 정세에서 매우 중요한 진입자로 부상하고 있으며, ICAO는 아시아태평양에서만 국내 항공 노선의 70%를 차지한다고 지적했습니다.

예측에 따르면 향후 몇 년동안 중국 항공 시장은 강력한 성장 궤도를 그릴 것입니다. 특히 중국 3대 항공사인 중국국제항공, 중국남방항공, 중국동방항공은 세계 순위 상승을 목표로 야심찬 장비 확충 목표를 세우고 있습니다. 또한 상하이와 베이징의 주요 공항은 대규모 확장 계획을 적극적으로 추진하고 있습니다.

Chinese Tourism Outbound Research Institute에 따르면, 중국 출국자 수는 2030년까지 약 4억 명에 달하고, 전 세계 출국자 수의 4분의 1을 차지할 것으로 예상됩니다. 이러한 급격한 증가에 대응하기 위해 공항들은 첨단 시스템을 도입해야 하며, 이러한 움직임은 예측 기간 동안 시장 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

반대로, 코로나19 사태를 계기로 많은 공항들이 승객 검사와 바이러스 차단을 위해 로봇을 도입하고 있습니다. 예를 들어, 한국 인천공항의 스마트 공항 팀은 로봇공학과 자율주행 차량을 활용하여 거동이 불편한 승객(PRM)의 경험을 개선하고 있습니다.

아시아태평양의 자동 자재 취급 및 저장 시스템 산업 개요

아시아태평양의 자동 자재 취급 및 보관 시스템 시장은 많은 기업들이 이 부문에 진입하고 있어 경쟁이 치열합니다. 이러한 경쟁을 형성하는 주요 요인으로는 높은 진입장벽, 기업 집중화, 시장 침투율 증가 등이 있습니다. 주요 시장 진출기업으로는 Kardex Group, KION Group, JBT Corporation, Jungheinrich AG, Daifuku, BEUMER Group GmbH & Co.KG 등이 있습니다.

2024년 2월, 세계적인 신발 및 의류 브랜드인 Skechers USA는 자동 보관 및 검색 시스템(ASRS) 선도 기업인 하이로보틱스(High Robotics)와 파트너십을 맺고 도쿄 미나토구에 최신 물류 센터를 개설했습니다. 스케쳐스는 하이로보틱스의 최첨단 자동 창고 기술을 활용하여 창고 운영을 강화하고 주문 처리 속도를 높이며 정확한 주문 처리를 실현할 수 있게 되었습니다.

2024년 1월, 후지쯔(Fujitsu Limited)와 YE DIGITAL CORPORATION은 일본 물류 산업의 노동력 부족 문제를 해결하고 지속가능한 공급망을 강화하기 위한 협력을 발표했습니다. 이번 파트너십은 물류센터 효율화로 유명한 후지쯔의 WMS 서비스와 YE DIGITAL의 WES MMLogiStation을 활용한 창고 업무 자동화에 초점을 맞추었습니다. 신규 물류센터 건설 및 기존 물류센터의 업무 개혁 등의 계획 지원도 함께 진행하여 자동화 설비 도입을 촉진합니다. 시설 관리의 효율화를 통해 운영의 자동화를 촉진하고 물류센터 전체의 성과를 향상시키는 것을 목표로 하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

산업 밸류체인 분석

산업의 매력 - Porter의 Five Forces 분석

공급 기업의 교섭력

소비자의 교섭력

신규 진출업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

COVID-19산업 에코시스템에 대한 영향

시장 성장 촉진요인

시장 성장 억제요인

제5장 시장 세분화

제품 유형

하드웨어

소프트웨어

서비스

기기 유형

이동 로봇

무인운반차(AGV)

자동 지게차

자동 촉진/트랙터/태그

유닛 로드

조립 라인

특수용도

자율 이동 로봇(AMR)

자동 보관 및 검색 시스템(ASRS)

고정 통로

카르셀

수직 리프트 모듈

자동 컨베이어

벨트

롤러

팰릿

오버헤드

팔렛타이즈

기존

로봇

구분 시스템

최종사용자 산업

공항

자동차

식품 및 음료

소매/창고/배송센터/물류센터

일반 제조업

의약품

우편 및 소포

일렉트로믹스 및 반도체 제조

기타

국가명

중국

일본

인도네시아

인도

호주

태국

한국

싱가포르

말레이시아

대만

기타 아시아태평양

제6장 경쟁 구도

기업 개요

Daifuku Co. Ltd

Kardex Group

KION Group

JBT Corporation

Jungheinrich AG

SSI Schaefer AG

VisionNav Robotics

System Logistics

BEUMER Group GmbH & Co. KG

Interroll Group

Witron Logistik

Kuka AG

Honeywell Intelligrated Inc.

Murata Machinery Ltd

Toyota Industries Corporation

제7장 투자 분석

제8장 시장 기회와 향후 동향

LSH

영문 목차

영문목차

The Asia Pacific Automated Material Handling And Storage Systems Market size is estimated at USD 29.66 billion in 2025, and is expected to reach USD 56.11 billion by 2030, at a CAGR of 13.6% during the forecast period (2025-2030).

With the rapid growth in stock-keeping units (SKUs), wholesalers and distributors are finding it difficult to make informed decisions about operations. This dilemma underscores the pressing need for more efficient labor, equipment, and technology utilization. Key factors driving the need for automated material-handling systems include cost savings, enhanced labor efficiency, and space optimization.

The market landscape is witnessing a surge in product variety and a demand for more frequent, smaller deliveries. Automated distribution operations can significantly boost an organization's order accuracy, often by several percentage points. The Asia-Pacific market's growth is propelled by urbanization, surging e-commerce sales, and a robust technology provider presence. These providers are intensifying their R&D efforts to offer cutting-edge solutions and maintain a competitive edge.

Asia-Pacific has cemented its position as a global e-commerce powerhouse. This status has been bolstered by the region's expanding retail e-commerce, driven by a burgeoning middle-income group in countries like China, India, and Indonesia, coupled with a fondness for mobile devices. Notably, China commands a staggering 40% share of global retail e-commerce sales. In several Asia-Pacific nations, the availability of warehouse land is dwindling, prompting a shift toward multi-story facilities and taller, narrower aisles. These adaptations are poised to fuel the demand for advanced material handling systems.

Material handling has witnessed a profound evolution over the past seven decades, with machines and robots increasingly replacing individual workers. This transformation has not only reshaped the industry but also fueled the growth of enterprises, notably in the automotive industry, which has seen a tenfold expansion. Countries like India are significantly investing in material handling equipment, with the MHE market, as per the Wisconsin Economic Development Corporation, capturing around 13% of the country's construction equipment industry. Southeast Asian nations, including Thailand, the Philippines, and Vietnam, are witnessing a surge in manufacturing establishments, bolstering employment and, subsequently, disposable incomes. This rise in income, coupled with a growing awareness of international brands, is spurring demand for local warehouses.

Indonesia stands out as a nation swiftly embracing automation, with a notable uptick in robotic usage for industrial applications. Given Japan's dual role as both a supplier and a consumer, Indonesia stands to benefit from heightened trade activities, further propelling the region's automation demand.

The global industrial landscape faced significant disruptions due to the COVID-19 pandemic and ensuing lockdowns. These disruptions spanned supply chain challenges, raw material shortages, labor scarcities, fluctuating prices, and shipping bottlenecks, all of which threatened to inflate production costs and exceed budgets.

APAC Automated Material Handling & Storage Systems Market Trends

Assembly Line Segment to Witness Significant Growth in the Market

Assembly-line AGVs find their primary application in industries like automobile manufacturing, coach-building, aerospace, and railways. The rising production of electric and hybrid vehicles is set to drive the demand for these AGVs in the coming years. This shift not only enhances manufacturers' flexibility but also enables them to swiftly adapt to market changes, all while ensuring safe and cost-effective operations.

The automotive industry witnessed a revolution in the past decade with the introduction of electric and hybrid vehicles. This transformation has significantly increased the complexity of automobile production. Coupled with evolving safety regulations and industry standards, there is a growing need for automation in the automotive industry. Key priorities include reducing product damage, often caused by human error during transit, improving the speed of chassis handling between workstations, and facilitating interaction with assembly-line workers. Assembly line AGVs, meeting these requirements effectively, have become the cornerstone of automation in the automotive industry.

Furthermore, in the automotive industry, automated assembly lines are utilized to craft various parts, ranging from engines and gearboxes to fuel systems and pumps. Leveraging robotics and vision technology, manufacturers can create ergonomic and efficient product lines, safeguarding their workforce from hazardous conditions while ensuring swift assembly. Consequently, safety concerns are propelling automation across the automotive landscape.

According to a report by the Automotive Skill Development Council (ASDC), titled 'Human Resource and Skills Requirements in the Automotive Sector (2026),' India is projected to employ 45.08 million individuals in the automobile industry by 2026. This surge in the workforce demands a reevaluation of the current skill set, emphasizing the need for upskilling in areas like automotive design, robotics, IoT, and AI. As traditional roles evolve, the industry is witnessing a heightened push toward automation.

To cater to this escalating demand, numerous market players are not only expanding their manufacturing capacities but also introducing new product lines. For instance, in March 2024, Applied Manufacturing Technologies (AMT), a prominent name in North America's automation engineering, unveiled its latest innovation, ROBiN. Termed the Robotic Induction System, ROBiN aims to revolutionize material handling in warehousing, promising heightened efficiency and throughput. With a strong reputation in advanced material handling and cutting-edge autonomous mobile robots (AMRs), AMT's ROBiN is poised to make a significant impact in the industry.

Industry 4.0 Investments Driving Demand for Automation and Material Handling

Airport investments are gaining global recognition as nations understand the value of creating welcoming environments that encourage travelers to spend both time and money. From check-in to boarding, conveyors and sortation systems, prevalent in airports of all sizes, effectively streamline the process, enhancing the overall customer experience. Many airports are now collaborating with vendors to introduce autonomous robots, a move that not only boosts luggage transfer efficiency but also trims operational costs. For example, Vanderlande Dutch, a logistics automation specialist, recently partnered with Hong Kong Airport to trial autonomous baggage handling vehicles.

India and China, driven by increasing domestic air connectivity and rising per capita GDP, stand out as pivotal players in the regional aviation landscape. Highlighting this, the ICAO notes that the Asia-Pacific region alone accounted for 70% of domestic air travel.

Projections indicate a robust growth trajectory for the Chinese aviation market in the coming years. Notably, China's top three airlines-Air China, China Southern, and China Eastern-have set ambitious fleet expansion goals, aiming to elevate their global rankings. Furthermore, major airports in Shanghai and Beijing are actively pursuing extensive expansion initiatives.

According to the Chinese Tourism Outbound Research Institute, Chinese outbound visits are set to reach around 400 million by 2030, potentially constituting a quarter of all global outbound travelers. To accommodate this surge, airports must deploy advanced systems, a move that is expected to drive market growth positively throughout the forecast period.

Conversely, the pandemic prompted many airports to deploy robots for passenger screening and virus containment. For instance, South Korea's Incheon Airport's Smart Airport team has been leveraging robotics and automated vehicles to enhance the experience for passengers with reduced mobility (PRMs).

APAC Automated Material Handling & Storage Systems Industry Overview

The Asia-Pacific market for automated material handling and storage systems is fiercely competitive, primarily due to the significant number of players in the arena. Key factors shaping this competition include high exit barriers, increasing firm concentration, and rising market penetration rates. Some of the key players operating in the market are Kardex Group, KION Group, JBT Corporation, Jungheinrich AG, Daifuku Co. Ltd, and BEUMER Group GmbH & Co. KG.

In February 2024, Skechers USA, a prominent global footwear and apparel brand, partnered with Hai Robotics, a top player in automated storage and retrieval systems (ASRS), to inaugurate its latest distribution hub in Minato City, Tokyo, Japan. By leveraging Hai's cutting-edge automated goods-to-person technology, Skechers is enhancing its warehouse operations, accelerating fulfillment, and ensuring precise order processing.

In January 2024, Fujitsu Limited and YE DIGITAL CORPORATION announced a collaboration aimed at tackling labor shortages and bolstering sustainable supply chains in Japan's logistics industry. The partnership focuses on leveraging Fujitsu's WMS services, known for enhancing distribution center efficiency, alongside YE DIGITAL's WES MMLogiStation, which is designed to automate warehouse operations. Fujitsu will not only provide its WMS services but also offer planning support for constructing new distribution centers and transforming operations at existing ones, aiming to ease the adoption of automated facilities. By streamlining facility management, the companies aim to drive operational automation and enhance overall distribution center performance.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis