ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

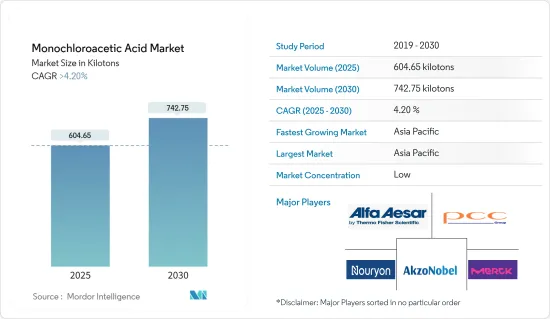

모노클로로아세트산 시장 규모는 2025년에 604.65킬로톤에 이를 것으로 추정되며, 예측 기간(2025-2030년) 동안 4.2% 이상의 CAGR을 기록하여 2030년에는 742.75 킬로톤에 이를 것으로 예상됩니다.

주요 하이라이트

단기적으로는 퍼스널케어 및 제약 산업 수요 증가와 농약 산업 수요 증가가 조사 대상 시장의 성장을 가속하는 주요 요인입니다.

그러나 모노클로로아세트산과 관련된 엄격한 규제는 예측 기간 동안 대상 산업의 성장을 억제할 것으로 예상되는 주요 요인입니다.

시아노아세트산 사용량이 증가함에 따라 조만간 세계 시장에서 유리한 성장 기회가 창출될 가능성이 높습니다.

아시아태평양은 세계 시장을 독점하고 있으며, 가장 큰 소비는 중국과 인도에서 가져왔습니다.

모노클로로아세트산 시장 동향

퍼스널케어 및 제약업계 수요 증가

모노클로로아세트산(MCA)은 퍼스널케어 및 화장품 산업에서 매우 중요한 성분입니다. 주로 양쪽성 계면활성제인 베타 인의 생산에 사용됩니다. 이 베타 인은 발포성으로 유명하며 헤어 샴푸에 광범위하게 사용됩니다.

MCA의 또 다른 유도체 인 티오 글리콜 산(TGA 또는 메르 캅토 아세트산)은 영구 헤어 스타일링 제에 없어서는 안될 필수 성분입니다. 헤어 스타일링뿐만 아니라 티오글리콜산과 그 유도체는 샴푸, 컨디셔너, 헤어 마스크 등 다양한 헤어 케어 제품 생산에 필수적입니다.

국립통계지리연구소(INEGI) 데이터에 따르면 2023년 12월 멕시코의 샴푸, 컨디셔너, 헤어 린스 생산량은 4631만 개로 2022년 12월의 4402만 개보다 5.2% 증가하였습니다.

또한 INEGI의 조사에 따르면, 2023년 12월 멕시코의 샴푸와 컨디셔너의 월별 생산량은 4,625만 개로 전년 대비 4.6% 소폭 증가했습니다.

또한, 가처분 소득 증가, 미용 제품에 대한 인식 증가, 소비 패턴의 진화, 세계화의 영향을 받은 인도, 태국, 베트남 등의 국가에서 소매 상황의 변화는 퍼스널케어 제품 수요를 견인하고 MCA 수요를 증가시킬 것으로 보입니다.

캐나다 통계청에 따르면 캐나다의 화장품 및 향수 매출은 2023년 3 분기에 약 18 억 6 천만 캐나다 달러(약 13 억 8,000만 달러)에 달했습니다. 또한 국제무역국과 미국 상무부에 따르면 캐나다 화장품 시장의 산업 매출은 매년 1.45% 성장하여 2024년에는 18억 달러에 달할 것으로 예상됩니다. 이러한 캐나다의 뷰티 및 퍼스널케어 산업의 부흥은 미국 화장품 수출업체에게 유리한 기회를 가져다 줄 것입니다.

MCA는 퍼스널케어에서의 역할 외에도 이부프로펜/브르펜, 디클로페낙 나트륨, 카페인, 비타민(비타민 B 등), 글리신, N-(P-하이드록시페닐)-글리신(METOL), 말레인산염 등 의약품에서도 중요한 용도를 찾았다, 다양한 의약품 생산에 기여하고 있습니다.

India Brand Equity Foundation(IBEF)에 따르면, 인도는 풍부한 원료 자원과 숙련된 노동력으로 인해 세계 3위, 세계 14위의 의약품 시장으로 성장했습니다.

퍼스널케어 및 제약 부문 모두에서 수요가 증가함에 따라 모노클로로 아세트산 수요는 예측 기간 동안 급증할 것으로 예상됩니다.

아태지역이 시장을 독점

개인 관리, 제약, 농약 등 주요 부문 수요가 증가함에 따라 아시아태평양은 세계 시장 점유율에서 확고한 우위를 점하고 있습니다.

중국과 인도에서는 최근 몇 년동안 모노클로로 아세트산(MCA)에 대한 수요가 눈에 띄게 증가했습니다. 이러한 급증은 주로 퍼스널케어 및 제약 산업 수요 증가에 기인합니다.

중국 국가통계국 데이터에 따르면 2023년 중국 화장품 소매 판매액은 약 4,141억 7,000만 위안(약 584억 2,000만 달러)에 달하고, 전년 대비 5.2%의 소폭 증가를 기록했습니다.

위생과 청결에 대한 관심이 높아지면서 퍼스널케어 제품, 세제, 세탁 비누에 대한 수요가 증가하고 있습니다. 이러한 퍼스널케어 제품 생산에 MCA가 필요하기 때문에 MCA 수요를 증가시킬 가능성이 높습니다.

경제산업성 데이터에 따르면 2023년 일본 헤어 샴푸 매출은 808억 9,000만 엔(약 5억 7,000만 달러)으로 전년 대비 6.6% 감소했습니다.

중국과 인도에서 인구가 급증하면서 아시아태평양의 퍼스널케어 및 제약 부문은 눈에 띄게 상승세를 보이고 있습니다.

IBEF에 따르면, 인도 의약품 시장은 23년도에 전년 대비 5% 증가한 497억 8,000만 달러에 달했습니다. 주목할 만한 점은 의약품이 인도에서 외국인 투자를 유치하는 상위 10개 부문에 포함되었습니다는 점입니다. 인도의 의약품 수출은 200여 개국에 달하며 미국, 서유럽, 일본, 호주 등 까다로운 시장을 아우르고 있습니다. 특히 의약품 수출액은 2023년 4월 22억 6,000만 달러에서 2024년 4월 24억 3,000만 달러로 7.36% 증가했습니다.

따라서 앞서 언급 한 요인을 고려할 때 모노클로로 아세트산에 대한 수요는 예측 기간 동안 아시아태평양에서 급속한 증가를 확인할 것으로 예상됩니다.

모노클로로아세트산 산업 개요

단색 아세트산 시장은 그 특성상 부분적으로 세분화되어 있습니다. 주요 진출기업으로는 Nouryon, Merck KGaA, Alfa Aesar, PCC Group, Akzo Nobel NV 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

성장 억제요인

산업 밸류체인 분석

Porter’s Five Forces

공급 기업의 교섭력

소비자의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(시장 규모(수량))

화학 용도별

글리신

카복시메틸셀룰로오스(CMC)

계면활성제

2,4-디클로로 페녹시 아세트산

티오글리콜산

기타

최종사용자 산업별

퍼스널케어 및 의약품

농약

지질 드릴

염료 및 세제

기타

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

북유럽 국가

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 구도

인수합병(M&A)/합작투자(JV)/협업/협정

시장 점유율(%)**/순위 분석

주요 기업의 전략

기업 개요

Akzo Nobel NV

Alfa Aesar

Anugrah In-Org(P) Limited

CABB Group GmbH

Denak Co. Ltd

Henan HDF Chemical Company Ltd

Merck KGaA

Meridian Chem Bond Pvt. Ltd

Niacet Corporation

Nouryon

PCC Group

Puyang Tiancheng Chemical Co. Ltd

Shandong Minji New Material Technology Co. Ltd

TerraTech Chemicals(I) Pvt. Ltd

제7장 시장 기회와 향후 동향

LSH

영문 목차

영문목차

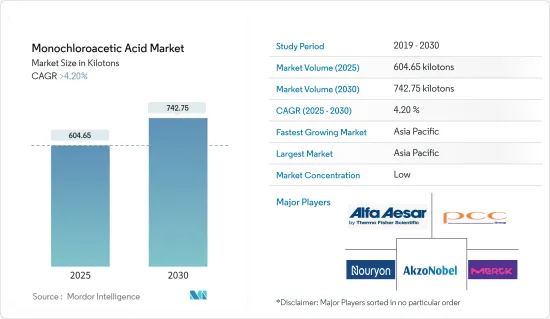

The Monochloroacetic Acid Market size is estimated at 604.65 kilotons in 2025, and is expected to reach 742.75 kilotons by 2030, at a CAGR of greater than 4.2% during the forecast period (2025-2030).

Key Highlights

Over the short term, the increasing demand from the personal care and pharmaceutical industries and the growing demand from the agrochemicals industry are the major factors driving the growth of the market studied.

However, the stringent regulations related to monochloroacetic acid are a key factor anticipated to restrain the growth of the target industry over the forecast period.

Nevertheless, the rising usage of cyanoacetic acid is likely to create lucrative growth opportunities for the global market soon.

Asia-Pacific dominated the market across the world, with the largest consumption coming from China and India.

Monochloroacetic Acid Market Trends

Increasing Demand from Personal Care and Pharmaceuticals Industries

Monochloroacetic acid (MCA) is a pivotal component in the personal care and cosmetic industry. It is primarily utilized in the production of betaines, which are amphoteric surfactants. These betaines, known for their foaming properties, find extensive use in hair shampoos.

Thioglycolic acid (TGA or mercaptoacetic acid), another derivative of MCA, is crucial in permanent hair styling formulations. It's not just limited to hair styling; thioglycolic acid and its derivatives are integral in the production of various hair care products, including shampoos, conditioners, and hair masks.

According to the data from the National Institute of Statistics and Geography (INEGI), in December 2023, Mexico's production volume for shampoos, conditioners, and hair rinses hit 46.31 million units, marking a 5.2% increase from 44.02 million units in December 2022.

INEGI's survey also highlights that the monthly sales volume of shampoos and conditioners in Mexico stood at 46.25 million units in December 2023, showing a modest 4.6% uptick from the previous year.

Additionally, rising disposable incomes, increasing beauty product awareness, evolving consumption patterns, and the changing retail landscape in countries like India, Thailand, and Vietnam, influenced by globalization, are set to drive the demand for personal care products, subsequently boosting the demand for MCA.

As per Statistics Canada, cosmetics and fragrance sales in Canada reached approximately CAD 1.86 billion (~USD 1.38 billion) in the third quarter of 2023. Moreover, according to the International Trade Administration and the US Department of Commerce, the industry revenue for the cosmetics market in Canada is expected to grow by 1.45% annually to reach USD 1.8 billion by 2024. This resurgence in Canada's beauty and personal care industry presents a lucrative opportunity for US cosmetic exporters.

Besides its role in personal care, MCA finds significant use in pharmaceuticals, contributing to the production of various medications, including ibuprofen/brufen, diclofenac sodium, caffeine, vitamins (e.g., vitamin B), glycine, N-(P-hydroxyphenyl)-glycine (METOL), and maleates.

As per the India Brand Equity Foundation (IBEF), India stands as the world's third-largest pharmaceutical market by volume and the fourteenth by value, owing to its rich raw material resources and skilled workforce.

Given the rising demand in both the personal care and pharmaceutical sectors, the demand for monochloroacetic acid is expected to surge during the forecast period.

Asia-Pacific to Dominate the Market

With rising demands from key sectors like personal care, pharmaceuticals, and agrochemicals, Asia-Pacific has firmly established its dominance in the global market share.

China and India have seen a notable uptick in demand for monochloroacetic acid (MCA) in recent years. This surge is predominantly attributed to escalating needs within the personal care and pharmaceutical industries.

As per data from the National Bureau of Statistics of China, in 2023, China's cosmetic retail sales reached approximately CNY 414.17 billion (~USD 58.42 billion), marking a modest 5.2% uptick from the previous year.

The increasing concerns for hygiene and cleanliness have led to the growth in demand for personal care products, detergents, and washing soaps. This is likely to boost the demand for MCA, owing to its requirement in the production of these personal care products.

According to the data from the Ministry of Economy Trade and Industry (METI), Japan's hair shampoo sales were valued at JPY 80.89 billion (~USD 0.57 billion) in 2023, reflecting a 6.6% dip from the year before.

With burgeoning populations in China and India, the personal care and pharmaceutical sectors in Asia-Pacific are on a notable upswing.

As per IBEF, the Indian pharmaceutical market witnessed a 5% Y-o-Y growth in FY23, reaching USD 49.78 billion. Notably, pharmaceuticals rank among the top ten sectors that are drawing foreign investments in India. India's pharmaceutical exports span over 200 countries, encompassing stringent markets like the United States, Western Europe, Japan, and Australia. Specifically, exports of drugs and pharmaceuticals climbed by 7.36%, from USD 2.26 billion in April 2023 to USD 2.43 billion in April 2024.

Therefore, considering the aforementioned factors, the demand for monochloroacetic acid is expected to witness a rapid increase in Asia-Pacific during the forecast period.

Monochloroacetic Acid Industry Overview

The monochloroacetic acid market is partially fragmented in nature. The major players (not in any particular order) include Nouryon, Merck KGaA, Alfa Aesar, PCC Group, and Akzo Nobel NV.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from the Personal Care and Pharmaceutical Industry

4.1.2 Growing Demand from the Agrochemicals Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Regulations To Hinder Market Growth

4.2.2 Other Restraints

4.3 Industry Value-Chain Analysis

4.4 Porter Five Forces

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Chemical Application

5.1.1 Glycine

5.1.2 Carboxymethylcellulose (CMC)

5.1.3 Surfactants

5.1.4 2,4-Dichloro Phenoxy Acetic Acid

5.1.5 Thioglycol Acid

5.1.6 Other Applications

5.2 By End-user Industry

5.2.1 Personal Care and Pharmaceuticals

5.2.2 Agrochemicals

5.2.3 Geological Drillings

5.2.4 Dyes and Detergents

5.2.5 Other End-user Industries

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Nordic Countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Akzo Nobel NV

6.4.2 Alfa Aesar

6.4.3 Anugrah In-Org (P) Limited

6.4.4 CABB Group GmbH

6.4.5 Denak Co. Ltd

6.4.6 Henan HDF Chemical Company Ltd

6.4.7 Merck KGaA

6.4.8 Meridian Chem Bond Pvt. Ltd

6.4.9 Niacet Corporation

6.4.10 Nouryon

6.4.11 PCC Group

6.4.12 Puyang Tiancheng Chemical Co. Ltd

6.4.13 Shandong Minji New Material Technology Co. Ltd