북미의 플라스틱 병 및 용기: 시장 점유율 분석, 산업 동향, 통계 및 성장 예측(2025-2030년)

NA Plastic Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1626333

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

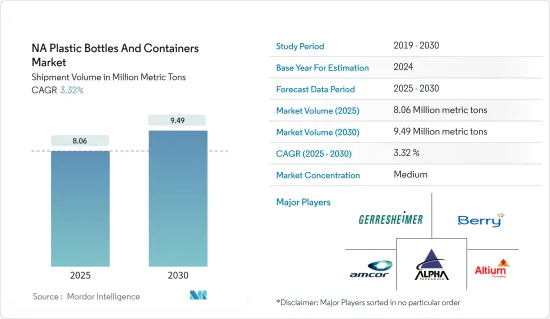

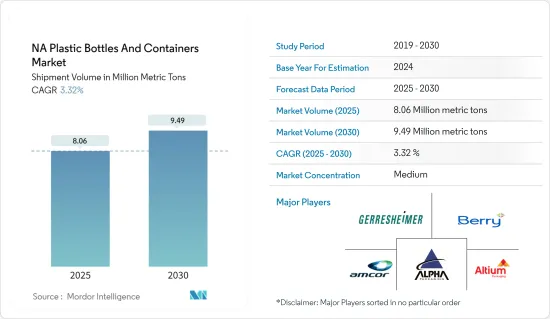

북미의 플라스틱 병 및 용기 시장의 출하량 규모는 예측 기간(2025-2030년) 동안 연평균 3.32%의 연평균 복합 성장률(CAGR)로 2025년 806만 톤에서 2030년 949만 톤으로 성장할 것으로 예상됩니다.

북미의 플라스틱 병 및 용기 시장은 탄탄한 제조 능력과 탄탄한 수출 부문으로 형성되어 있습니다. 포장은 소비재 및 산업용 제품 소비에 있어 매우 중요한 역할을 합니다. 북미에서는 지속 가능하고 편리한 포장 솔루션에 대한 수요가 증가하면서 시장 성장을 견인하고 있습니다.

주요 하이라이트

신흥국들이 부상하는 가운데 미국은 세계 제약 산업에서 지배적인 지위를 유지하고 있습니다. 주요 제약회사의 본거지인 미국은 시장 점유율이 높을 뿐만 아니라 소비자에게 최첨단 제품을 제공합니다. 이러한 탄탄한 제약 산업은 플라스틱 병 및 용기 시장의 혁신과 발전에 박차를 가하고 있습니다.

주요 하이라이트

예를 들어, 미국의 베리 세계(Berry Global)은 2023년 2월 의약품 및 허브 시장을 위한 종합적인 솔루션을 발표했습니다. 베리 헬스케어 번들로 알려진 이 신제품은 20ml에서 1,000ml에 이르는 다양한 28mm 목의 PET 병을 포함하며, 변조 방지 및 어린이 보호 기능이 있는 8가지 유형의 마개가 특징입니다.

화장품에서 스킨케어에 이르기까지 북미 뷰티 및 퍼스널케어 업계는 프리미엄 및 혁신 제품에 대한 수요가 급증하고 있습니다. 이러한 추세는 주요 브랜드들이 제품 라인업을 강화하는 원동력이 되고 있습니다.

개인 위생용품에 대한 수요가 증가하면서 플라스틱 병 및 용기 시장이 크게 성장하고 있습니다. 이러한 급증은 플라스틱 포장의 실용성, 비용 효율성 및 다재다능함에 기인하는 바가 큽니다. 소비자들이 화장품 및 퍼스널케어 제품에서 편리함과 혁신적인 디자인을 선호함에 따라 플라스틱 용기가 최적의 솔루션으로 떠오르고 있습니다. 플라스틱 병은 로션, 크림, 샴푸, 세럼 등 미용 및 퍼스널케어 산업의 다양한 요구를 능숙하게 충족시킬 수 있습니다.

북미에서 기능성 음료 산업이 확대되면서 시장 성장을 견인하고 있습니다. 이는 플라스틱 포장의 편리성과 휴대성, 그리고 이동 중에도 마실 수 있는 음료와 건강 중심 음료에 대한 소비자의 선호도가 높아진 데 기인합니다.

2024년 3월, 미국에 본사를 둔 음료 회사 Roar Organic은 현지 기업으로부터 1,000만 달러의 투자를 받았습니다. 이번 투자는 Roar의 제품 라인업을 확장하는 것을 목표로 하며, Roar가 음료와 분말 형태의 향이 첨가된 비탄산 "기능성" 음료를 출시할 수 있도록 지원할 예정입니다. 이러한 전략적 투자는 향후 몇 년동안 시장 성장을 가속할 것으로 예상됩니다.

미국에서는 PET와 HDPE가 시장을 독점하고 있습니다. 비용 효율성과 사용 편의성 때문에 플라스틱을 선호하기 때문에 PET 병이 큰 시장 점유율을 차지할 것으로 예상됩니다.

그러나 환경에 대한 인식이 높아짐에 따라 플라스틱 사용의 모멘텀이 약화될 것으로 예상됩니다. 미국과 캐나다에서 눈에 띄는 변화를 볼 수 있는데, 소비자들은 친환경 포장 솔루션에 매력을 느끼고 있습니다. 두 나라 모두 플라스틱과 관련된 환경적 위험성을 인식하고 엄격한 규제를 제정하여 플라스틱의 성장률을 대체 소재에 비해 억제하고 있습니다.

그러나 지속 가능한 플라스틱 병에 대한 수요가 증가함에 따라 특히 재활용 재료 개발 측면에서 시장의 기업들에게 새로운 길을 열어주고 있습니다.

북미의 플라스틱 병 및 용기 시장 동향

음료 포장재에 대한 수요 증가로 폴리에틸렌 테레프탈레이트(PET) 사용 증가

폴리에틸렌 테레프탈레이트(PET)는 수증기, 가스, 희석 된 산, 기름 및 알코올에 대한 견고한 장벽으로 인해 음료 포장재로 선호되며, PET는 보호 특성뿐만 아니라 비산 방지, 적당한 유연성 및 재활용 성이 우수합니다. 내구성과 안정성으로 인해 PET는 개별 음료수 병과 용기를 포함한 식품 등급 제품에 이상적인 선택입니다.

Earth Day Organizer에 따르면, 미국에서는 매분 100만 개의 플라스틱 병이 판매되고 있습니다.

탄산음료(CSD) 분야에서 플라스틱 병의 사용량이 급증하고 있지만, 북미에서는 현재 포화상태에 이르렀다고 합니다. 펩시, 코카콜라, 큐리그 닥터페퍼 등 업계 대기업들은 북미 CSD 부문의 매출이 정체되어 있다고 보고했습니다. 코카콜라의 연례 보고서에 따르면, 이들 3사는 북미 시장 점유율의 80% 이상을 차지하고 있는 것으로 추정됩니다. 이러한 우위는 CSD 부문에서 플라스틱 병에 대한 수요가 앞으로도 지속될 것임을 시사합니다.

2024년 3월, 미국에 본사를 둔 음료 회사 Roar Organic은 현지 기업 Factory LLC로부터 1,000만 달러의 투자를 받아 Ready-to-drink 및 분말 형태의 향이 첨가된 무탄산 "기능성" 음료를 포함한 제품군을 확장할 예정입니다. 투자했습니다. 이러한 투자는 예측 기간 동안 시장에 기회를 가져다 줄 것으로 예상됩니다.

청량음료 포장은 폴리에틸렌 테레프탈레이트(PET) 병이 CO2 보유력이 우수하여 주류로 자리 잡고 있습니다. 그러나 PET 포장의 범용성은 청량음료에 국한되지 않고 과일 주스, 에너지 음료, 스포츠 음료, 와인, 증류주, 맥주와 같은 알코올성 음료에도 적용되고 있습니다. 미국에서는 증류주 판매가 급증하고 있으며, 100% PET 병에 대한 수요가 이 지역 시장 성장을 견인할 것으로 예상됩니다.

화장품 업계에서 플라스틱 포장 채택이 급증할 것

플라스틱은 화장품 포장에 선호되는 재료로 각광받고 있습니다. 플라스틱의 유연성은 디테일한 디자인을 가능하게 하고, 플라스틱의 보호성은 제품의 안전을 보장합니다. 그 결과, 플라스틱 병과 용기는 화장품 산업의 포장을 지배하고 상당한 시장 점유율을 확보했습니다.

포장기계공업협회(PMMI)의 데이터에 따르면 병, 항아리, 콤팩트, 튜브 등 플라스틱 포장은 화장품 및 퍼스널케어 산업에서 61%의 압도적인 점유율을 차지하고 있습니다. 그 중에서도 플라스틱 병이 가장 두드러져 시장의 30%를 차지하고 있습니다.

미국은 화장품, 퍼스널케어 제품 및 향수의 주요 시장입니다. 미국에는 밀레니얼 세대의 인구가 많아 시장 수요를 뒷받침하고 있습니다. 밀레니얼 세대는 국가의 노동력으로서 탈취제, 향수, 화장품과 같은 퍼스널케어 제품을 우선시하며 외모의 중요성을 강조합니다. 그 결과, 화장품 수요가 급증함에 따라 플라스틱 용기를 포함한 포장재에 대한 수요도 지역 전체에서 동시에 증가하고 있습니다.

지속가능성을 향한 공동의 노력으로 화장품 회사들은 점점 더 친환경 플라스틱 포장 솔루션을 추구하고 있으며, 2020년 8월 미국 로레알은 다른 60개 브랜드, 정부 대표, 소매업체, NGO와 함께 2025년까지 미국 내 모든 플라스틱 포장을 재사용, 재활용, 퇴비화할 것을 약속했습니다. 플라스틱 포장을 재사용, 재활용, 퇴비화할 수 있는 것으로 만들겠다고 약속했습니다.

북미의 플라스틱 병 및 용기 시장 개요

북미의 플라스틱 병 및 용기 시장은 단편화되어 있으며, 여러 회사로 구성되어 있습니다. 시장 점유율은 현재 소수의 대기업이 시장을 독점하고 있습니다. 이들 기업은 해외 고객 기반 확대에 주력하고 있습니다. 이들 기업은 시장 점유율과 수익성을 높이기 위해 전략적 공동 이니셔티브를 활용하고 있습니다.

기타 혜택 :

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter의 Five Forces 분석

공급 기업의 교섭력

구매자/소비자의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

산업 밸류체인 분석

지정학적 동향 업계에 대한 영향 평가

제5장 시장 역학

시장 성장 촉진요인

경량 포장 채택 증가

화장품 업계 플라스틱 포장 채택 급증

시장 성장 억제요인

원재료 가격 변동

플라스틱 사용에 대한 환경 문제 증가

제6장 시장 세분화

소재 유형별

폴리에틸렌 테레프탈레이트(PET)

폴리에틸렌 테레프탈레이트(PET)

저밀도 폴리에틸렌(LDPE)

고밀도 폴리에틸렌(HDPE)

기타 재료 유형

업계별

음료

아로코르 음료

무알코올 음료

식품

화장품

의약품

가정용품

기타 업계별

국가별

미국

캐나다

제7장 경쟁 구도

기업 개요

Alpha Packaging Inc.

Altium Packaging(Loews Corporation)

Gerresheimer AG

Graham Packaging Company LP

Berry Global Group Inc.

Plastipak Holdings Inc.

Amcor Plc

Graham Packaging

AptarGroup Inc.

Comar LLC

제8장 투자 분석

제9장 시장 전망

LSH

영문 목차

영문목차

The NA Plastic Bottles And Containers Market size in terms of shipment volume is expected to grow from 8.06 million metric tons in 2025 to 9.49 million metric tons by 2030, at a CAGR of 3.32% during the forecast period (2025-2030).

Well-established manufacturing capabilities and a resilient export sector mark North America's plastic bottles and containers market landscape. Packaging plays a pivotal role in the consumption of both consumer and industrial products. In North America, the rising demand for sustainable and convenient packaging solutions is propelling the market's growth.

Key Highlights

While several emerging nations are making their mark, the United States remains a dominant player in the global pharmaceutical arena. Home to major pharmaceutical companies, the United States not only commands a significant market share but also provides its consumers with access to cutting-edge products. This robust pharmaceutical landscape is spurring innovations and advancements in the plastic bottles and containers market.

Key Highlights

For example, in February 2023, Berry Global, a US company, unveiled a comprehensive solution tailored for the pharmaceutical and herbal markets. This new offering, known as the Berry Healthcare bundle, includes a diverse range of 28 mm neck PET bottles spanning sizes from 20 ml to 1,000 ml and features eight closures with tamper-evident and child-resistant attributes.

The North American beauty and personal care industry, which includes everything from cosmetics to skincare, is witnessing a surge in demand for premium and innovative products. This trend is driving leading brands to enhance their offerings.

The rising demand for personal care products is significantly boosting the plastic bottles and containers market. This surge is largely due to the practicality, cost-effectiveness, and versatility of plastic packaging. As consumers lean toward convenience and innovative designs in cosmetics and personal care, plastic containers are emerging as the go-to solution. Plastic bottles can adeptly cater to the diverse needs of the beauty and personal care industry, including lotions, creams, shampoos, and serums.

The expanding functional beverage industry in North America is fueling market growth. This can be attributed to the convenience and portability of plastic packaging, resonating with consumers' increasing preference for on-the-go and health-centric beverages.

In March 2024, Roar Organic, a beverage company based in the United States, secured a USD 10 million investment from a local firm. This funding aims to broaden Roar's product lineup, helping the company introduce flavored, non-carbonated "functional" drinks in both ready-to-drink and powdered formats. Such strategic investments are poised to bolster the market's growth in the coming years.

In the United States, PET and HDPE dominate the market. With manufacturers favoring plastic for its cost-effectiveness and ease of use, PET bottles are expected to hold a significant market share.

However, as environmental awareness grows, the momentum behind plastic usage is expected to decline. A notable shift is evident in the United States and Canada, where consumers are gravitating toward eco-friendly packaging solutions. Recognizing the environmental hazards linked to plastic, both countries have enacted stringent regulations, leading to a tempered growth rate for plastic compared to alternative materials.

Nevertheless, the rising demand for sustainable plastic bottles is opening new avenues for companies in the market, particularly in terms of developing recycled materials.

North America Plastic Bottles & Containers Market Trends

Rising Demand for Beverage Packaging Attributes is Increasing the Usage of Polyethylene Terephthalate (PET)

Polyethylene terephthalate (PET) is a preferred choice for beverage packaging owing to its robust barrier properties against water vapor, gases, dilute acids, oils, and alcohol. Beyond its protective qualities, PET boasts shatter resistance, moderate flexibility, and recyclability. Its durability and steadfastness make PET an ideal choice for food-grade products, including individual drink bottles and containers.

According to Earth Day Organizers, the United States sees a staggering sale of about 1 million plastic bottles every minute, primarily fueled by the region's demand for packaged drinking water.

While the carbonated soft drinks (CSD) segment has seen a surge in plastic bottle usage, it is now reaching saturation in North America. Industry giants, including Pepsi, Coca-Cola, and Keurig Dr Pepper, reported stagnant sales in their North American CSD divisions. Coca-Cola's annual report estimated that these three companies commanded over 80% of the North American market share. This dominance suggests a continued demand for plastic bottles in the CSD segment.

In March 2024, Roar Organic, a United States-based beverage company, attracted a USD 10 million investment from local firm Factory LLC to expand its product range, including flavored, non-carbonated "functional" drinks in ready-to-drink and powdered formats. Such investments are expected to create opportunities for the market during the forecast period.

Soft drink packaging is predominantly led by polyethylene terephthalate (PET) bottles due to PET's superior CO2 retention. However, the versatility of PET packaging is not limited to soft drinks; it also encompasses fruit juices, energy drinks, sports drinks, and a range of alcoholic beverages, including wine, spirits, and beer. With the United States witnessing a surge in spirits sales, the demand for 100% PET bottles is projected to boost the regional market growth.

Plastic Packaging Adoption is Set to Surge in the Cosmetics Industry

Plastic stands out as the preferred material for cosmetics packaging. Its flexibility enables detailed designs, and its protective nature ensures the safety of the products within. Consequently, plastic bottles and containers dominate the cosmetics industry's packaging landscape, securing a substantial market share.

According to data from the Packaging Machinery Manufacturers Institute (PMMI), plastic packaging, including bottles, jars, compacts, and tubes, commanded a dominant 61% share in the cosmetics and personal care industries. Among these, plastic bottles were particularly prominent, accounting for a notable 30% of the market independently.

The United States is a leading market for cosmetics, personal care items, and fragrances. A significant segment of the US millennial population fuels the market demand. As the dominant force in the nation's workforce, millennials prioritize personal care products-like deodorants, perfumes, and cosmetics-underscoring the importance of physical appearance. Consequently, as the demand for cosmetics surges, there is a parallel uptick in the demand for packaging, including plastic containers, across the region.

In a concerted effort toward sustainability, cosmetic companies are increasingly pursuing eco-friendly plastic packaging solutions. Highlighting this dedication, in August 2020, L'Oreal USA, in collaboration with 60 other brands, government representatives, retailers, and NGOs, made a commitment to have all plastic packaging in the US be either reusable, recyclable, or compostable by 2025.

North America Plastic Bottles & Containers Market Overview

The North American plastic bottles and containers market is fragmented and consists of several players. In terms of market share, a few major players currently dominate the market. These players are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions & Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers/Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Assessment of the Impact of Geopolitical Developments on the Industry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Adoption of Lightweight Packaging

5.1.2 Plastic Packaging Adoption Set to Surge in the Cosmetics Industry

5.2 Market Restraints

5.2.1 Fluctuating Raw Materials Prices

5.2.2 Growing Environment Concerns Over the Use of Plastics