일본의 상업용 HVAC : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

Japan Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1550330

리서치사:Mordor Intelligence

발행일:2024년 09월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

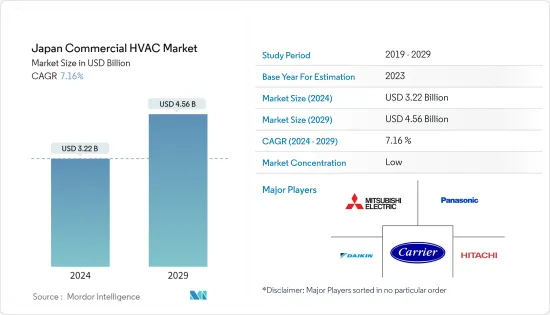

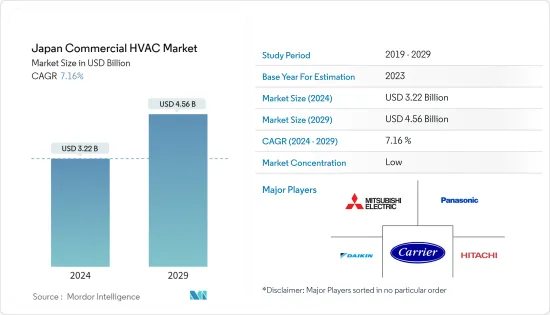

일본의 상업용 HVAC 시장 규모는 2024년 32억 2,000만 달러로 추정되며, 2029년에는 45억 6,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 7.16%의 CAGR로 성장할 것으로 예상됩니다.

주요 하이라이트

HVAC 시스템은 상업용 건물에서 쾌적한 실내 환경을 조성하는 데 필요합니다. 사무실 공간에서 온도를 조절하고 환기시켜 직원들의 생산성과 행복감을 높여줍니다. 또한 습도 관리 부족과 관련된 건강 위험을 줄이는 데 도움이 됩니다.

일본에서는 공해가 증가함에 따라 친환경 건물에 대한 관심이 높아지고 있으며, 일본 시장에서 발자취를 넓히려는 업계 관계자들에게 다양한 투자 전망이 나오고 있습니다.

국제에너지기구(IEA)에 따르면, 일본은 건축 기준을 업데이트하여 2030년까지 모든 신축 건물이 제로 에너지 성능을 달성하고 2050년까지 기존 건물이 이 기준을 충족하도록 의무화하고 있습니다. 건물의 에너지 효율을 높이는 것을 목표로 하는 이 기준은 시장 수요를 자극할 것으로 예상됩니다.

또한 개발도상국의 데이터센터, 창고, 쇼핑센터, 교육기관 및 기타 시설의 증가는 상업용 HVAC 시스템에 대한 수요를 촉진하고 있습니다. 이 나라에서는 데이터센터 건설에 대한 투자가 급증하고 있습니다. 예를 들어, 2024년 4월 ST 텔레미디어 월드 데이터센터(STT GDC)는 일본 내 중요한 디지털 인프라에 대한 수요가 증가함에 따라 도쿄에 두 번째 데이터센터 시설인 'STT 도쿄 2'를 건설할 계획이라고 밝혔습니다. 데이터센터 캠퍼스는 최대 70MW의 IT 용량을 제공하며, STT 도쿄2 프로젝트는 완공 시 최대 38MW의 전력을 생산할 수 있을 것으로 예상하고 있습니다.

에너지 비용 상승으로 인해 에너지 효율이 높은 HVAC 시스템이 점점 더 매력적으로 다가오고 있으며, 잠재적인 비용 절감 효과를 가져다 줄 수 있습니다. 하지만 설치에 따른 막대한 초기 비용이 널리 수용되고 시장 확대를 방해할 수 있습니다.

일본의 상업용 HVAC 시장은 단편화되어 있으며, 다수의 기업이 작은 시장 점유율을 차지하고 있습니다. 상업용 HVAC 시장에 진출한 주요 기업들은 고객 수요 증가에 대응하기 위해 신제품 개발, 전략적 제휴, 인수, 사업 확장에 주력하고 있으며, 이는 시장 성장을 더욱 촉진하고 있습니다.

예를 들어, 다이킨공업은 2023년 8월 이바라키현 츠쿠바미라이시에 토지를 매입해 에어컨 전용 공장을 신설할 계획을 발표했습니다. 이 계산된 결정은 회사의 국내 생산능력을 강화하고 일본 시장에서의 입지를 강화하려는 목표를 더욱 강화하기 위한 것입니다.

또한, 일본 내 공공건축물의 확대가 시장 성장을 뒷받침할 것으로 보입니다. 예를 들어, 2024년 6월, 씨티는 일본 내 씨티 상업은행(CCB)의 도입을 발표했습니다. 이 이니셔티브는 시티가 목표한 클러스터 내 전략적 성장 시장에 CCB를 설립하고 대폭적인 확장을 촉진하기 위한 계획의 핵심 요소입니다.

또한, 일본의 상업용 HVAC 산업은 정부의 규제와 에너지 효율이 높은 장비의 사용을 촉진하기 위한 새로운 시도와 같은 거시경제적 요소의 영향을 크게 받고 있습니다. 예를 들어, 일본은 2030년까지 온실 가스(GHG) 배출량을 46% 감축하는 목표를 세웠으며, 추가로 50% 감축을 달성하겠다는 야심찬 목표를 가지고 있습니다.

일본의 상업용 HVAC 시장 동향

HVAC 장비가 큰 시장 점유율을 차지

단일 분할 시스템은 소규모 상업용 건물에서 선호되는 HVAC 시스템입니다. 비용 효율적이고 각 방의 온도를 정확하게 제어할 수 있습니다.

상업용 공간의 VRF 시스템은 냉난방에 필요한 양의 냉매를 효율적으로 순환시킵니다. 이러한 첨단 공조 시스템을 통해 기업은 건물 내 여러 공조 구역을 동시에 관리할 수 있습니다.

또한, 공기 처리 장치(AHU)는 외부 환경과 실내 공기로부터 공기를 수집하고 오염 물질을 필터링하여 상업용 건물의 온도와 습도를 조절합니다. AHU는 설계 및 작동 방식에 따라 기존 매장용 공조 장치보다 효율적이며, AHU는 상업용 건물 내 비용을 낮추고 에너지 사용량을 줄일 수 있습니다.

일본에서는 관광객 증가로 인한 숙박업 부문의 확대가 상업용 HVAC 시스템에 대한 수요를 증가시킬 것으로 보입니다. 일본에서는 여행객들이 시티 호텔, 비즈니스 호텔, 리조트 호텔, 료칸, 단체 숙박시설 등 다양한 휴가용 숙박시설을 선택할 수 있습니다. 일본 후생노동성에 따르면 2023년 3월 말 기준 일본의 호텔 및 여관 등록 수는 약 90,700개소로 전년 대비 크게 증가했습니다.

일본의 인바운드 관광은 빠르게 성장하고 있으며, 시장은 국내 여행 활동을 우선시하고 있습니다. 최근 몇 년 동안 숙박객 수는 계속 증가하고 있지만, 숙박객 중 외국인이 차지하는 비율은 5분의 1에 불과합니다.

상업용 건물 부문이 큰 시장 점유율을 차지

상업용 건물 부문은 오피스 빌딩, 소매점, 쇼룸, 창고 등의 인프라를 구성합니다. 냉난방 시스템은 거주자에게 쾌적한 환경을 제공하기 때문에 모든 상업용 건물에 필수적입니다.

상업용 HVAC 시스템은 난방, 환기 및 공조 요소를 포함하는 복잡한 시스템입니다. 우수한 실내 공기질, 에너지 효율성 및 거주자 만족도를 보장하기 위해 대규모 건물의 특정 요구 사항을 충족하도록 조정됩니다.

상업용 HVAC 시스템은 세 가지 주요 시스템 기능을 조정하여 실내 온도를 효과적으로 조절하고 습도 수준을 제어하며 공기 질을 유지합니다. 에어컨은 냉매를 사용하여 실내 공간을 냉각시키고 제습을 돕습니다. 난방 시스템은 물, 라디에이터 코일 또는 가스를 사용하여 실내 온도를 높입니다. 환기 시스템은 여과 시스템으로 공기를 정화하고 팬으로 적절한 공기 순환을 보장합니다.

일본 내 오피스 공간의 확대는 예측 기간 동안 HVAC 서비스 및 장비의 수요를 견인할 것으로 보입니다. 일본 국토교통성에 따르면 2023년 일본에서 약 9,580개의 오피스 건설 프로젝트가 시작될 예정입니다. 이는 전년과 비슷한 수준이며, 오피스 건축 면적은 전년과 동일합니다.

또한, 대형 소매업체들이 일본 내 입지를 확대하면서 상업용 HVAC 시스템 및 서비스에 대한 높은 수요가 발생하고 있습니다. 효율적인 HVAC 시스템은 소매 공간의 공기질을 개선하여 큰 이점을 제공합니다. 이는 오염물질, 알레르겐, 불쾌한 냄새를 제거하여 궁극적으로 쇼핑 경험을 개선하고 고객과 직원 모두의 건강을 보장하는 것을 포함합니다.

이케아는 2024년 1월, 북관동에 새로운 매장을 오픈할 계획을 밝혔습니다. 이케아 마에바시 매장은 인구 700만 명 이상의 지역을 아우르며 지역사회의 요구에 부응할 수 있는 전략적 입지를 갖추고 있으며, 이케아 마에바시 매장은 지속가능성에 대한 이케아의 헌신을 보여주며, 일본에서 가장 친환경적인 이케아 매장이 될 예정입니다.

일본의 상업용 HVAC 산업 개요

일본의 상업용 HVAC 시장은 여러 기업으로 구성된 단편적인 시장입니다. 시장에 진입한 기업들은 신제품 도입, 사업 확장, 전략적 M&A, 제휴, 협력 관계 체결을 통해 시장에서의 입지를 강화하기 위해 끊임없이 노력하고 있습니다. 주요 기업으로는 Carrier Corporation, 다이킨공업 주식회사, 미쓰비시 전기 주식회사, Hitachi 주식회사, 파나소닉 주식회사 등이 있습니다.

2024년 5월, Midea는 EVOX G3 히트 펌프 시스템을 출시했으며, 이 새로운 EVOX 시리즈는 EVOX G3 히트 펌프와 EVOX G3 공기조화장치(AHU)로 구성되며, Midea EVOX G3 히트 펌프는 1.5톤에서 5톤까지 다양한 크기로 제공됩니다. 톤에서 5톤까지 다양한 크기로 제공되며, EVI(Enhanced Vapor Injection) 기술과 다층 열교환기를 탑재하여 혹독한 기상 조건에서도 보조 열이 필요 없는 안정적인 보온을 보장합니다.

2024년 3월, 파나소닉(Panasonic Corporation)은 환경 친화적인 자연 냉매를 사용하여 공동주택, 상점, 사무실 및 기타 경상업 시설용으로 설계된 새로운 상업용 공기 대 물(A2W) 히트 펌프 3종을 발표했습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 강도

업계 밸류체인 분석

COVID-19의 부작용과 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

국내의 상업 건축 증가

에너지 효율적 기기에 대한 수요 증가

시장 과제

에너지 효율적 시스템의 높은 초기 비용

제6장 시장 세분화

부품 유형별

HVAC 기기

난방 기기

공조·환기 기기

HVAC 서비스

최종 이용 산업별

호스피탈리티

상업 빌딩

공공시설

기타

제7장 경쟁 상황

기업 개요

Johnson Controls International PLC

Midea Group Co., Ltd.

Daikin Industries, Ltd.

Robert Bosch GmbH

Carrier Corporation

Valliant Group

LG Electronics Inc.

Lennox International Inc.

Mitsubishi Electric Corporation

Panasonic Corporation

Hitachi Ltd.

Danfoss A/S

제8장 투자 분석

제9장 시장 전망

ksm

영문 목차

영문목차

The Japan Commercial HVAC Market size is estimated at USD 3.22 billion in 2024, and is expected to reach USD 4.56 billion by 2029, growing at a CAGR of 7.16% during the forecast period (2024-2029).

Key Highlights

HVAC systems are necessary for creating comfortable indoor environments in commercial buildings. In office spaces, they regulate temperatures, provide ventilation, and boost employee productivity and well-being. Furthermore, they assist in reducing health risks related to poor humidity control.

Increasing levels of pollution in Japan have led the country to focus on eco-friendly buildings, presenting various investment prospects for industry players aiming to grow their footprint in the Japanese market.

According to the International Energy Agency (IEA), Japan has updated its building standards, mandating that all new buildings achieve zero-energy performance by 2030 and existing structures meet this criterion by 2050. These standards, aimed at enhancing energy efficiency in buildings, are projected to stimulate market demand.

Moreover, the increasing number of data centers, warehouses, shopping centers, educational institutions, and other facilities in developing nations is fueling the demand for commercial HVAC systems. The country is experiencing a surge in investments in the construction of data centers. For instance, in April 2024, ST Telemedia Global Data Centres (STT GDC) revealed plans to begin construction on its second data center facility in Tokyo, STT Tokyo 2, in response to the growing need for critical digital infrastructure in the country. The data center campus is expected to offer a maximum of 70 MW of IT capacity, and the STT Tokyo 2 project is expected to generate up to 38 MW upon completion.

Energy-efficient HVAC systems are increasingly attractive in the country because of the escalating energy costs, providing potential savings. Nevertheless, the substantial upfront expenses linked to installation could hinder widespread acceptance and market expansion.

The commercial HVAC market in Japan is fragmented, with a large number of players occupying a small market share. Key market players operating in the commercial HVAC market are focusing on new product development, strategic partnerships, acquisition, and expansion to meet the growing demand from customers, further supporting market growth.

For instance, in August 2023, Daikin Industries, Ltd announced plans to acquire land in Tsukubamirai City, Ibaraki Prefecture, Japan, with the intention of establishing a new manufacturing plant dedicated to air conditioners. This calculated decision is set to bolster the company's domestic production capacity and further its objective of strengthening its position within the Japanese market.

Furthermore, the rising expansion of public buildings in the country will support market growth. For instance, in June 2024, Citi revealed the introduction of Citi Commercial Bank (CCB) in Japan. This initiative is a crucial component of Citi's plan to establish CCB in strategic growth markets within targeted clusters to facilitate significant expansion.

Additionally, the commercial HVAC industry in Japan is significantly influenced by macroeconomic elements like governmental regulations and fresh endeavors aimed at promoting the use of energy-efficient equipment. For instance, Japan has set a target to reduce its greenhouse gas (GHG) emissions by 46% by 2030, with a further ambition to achieve a 50% reduction.

Japan Commercial HVAC Market Trends

HVAC Equipment Holds the Significant Market Share

The single split system is the preferred HVAC system for small commercial buildings. It is cost-effective and allows for precise control over the temperature in each room.

VRF systems in commercial space efficiently circulate the precise amount of refrigerant required for heating or cooling purposes. These advanced air conditioning systems enable businesses to manage multiple air conditioning zones within their premises simultaneously.

Moreover, Air Handling Units (AHUs) collect air from the external environment and indoor air, filter out contaminants, and regulate the temperature and humidity in the commercial building. The treated air is then circulated back into the atmosphere. Because of their design and operation, AHUs are more efficient than traditional retail air conditioning units. They can potentially lower costs and decrease energy usage within commercial establishments.

The rising expansion of the hospitality sector in Japan due to growing tourism will propel the demand for commercial HVAC systems in the country. In Japan, travelers can choose from various holiday accommodations, including city hotels, business hotels, resorts, ryokan, and group lodgings. According to the Ministry of Health, Labour and Welfare of Japan, as of the end of March 2023, Japan had seen a surge in the number of registered hotels and inns, totaling around 90,700 establishments, which was a significant increase compared to the previous year.

Despite Japan's rapid growth in inbound tourism, the market prioritizes domestic travel activities. Although the number of lodging guests has continuously increased in recent years, foreign nationals account for only one-fifth of overnight guests.

Commercial Building Segment Holds the Significant Market Share

The commercial building segment compromises infrastructures, such as office buildings, retail, showrooms, and warehouses, among others. Heating and cooling systems are essential to any commercial building, as they provide occupants with a comfortable environment.

Commercial HVAC systems are intricate, including elements for heating, ventilation, and air conditioning. They are tailored to meet large buildings' particular requirements to guarantee excellent indoor air quality, energy efficiency, and occupant satisfaction.

Commercial HVAC systems effectively regulate indoor temperature, control humidity levels, and maintain air quality by coordinating the functions of three key systems. Air conditioning units cool indoor spaces by utilizing refrigerants, which also help in dehumidifying the air. Heating systems raise indoor temperatures using water, radiator coils, or gas. Ventilation systems clean the air with filtration systems and ensure proper air circulation with fans.

The rising expansion of office space in the country will drive the demand for HVAC services and equipment during the projected timeline. According to the Ministry of Land, Infrastructure, Transport, and Tourism, approximately 9,580 office construction projects commenced in Japan in 2023. The floor area of these office constructions remained consistent with the previous year.

Moreover, leading retail players are expanding their presence in the country, thus creating high demand for commercial HVAC systems and services. An efficient HVAC system offers a significant benefit by enhancing the air quality in the retail space. This involves removing pollutants, allergens, and unpleasant odors, ultimately improving the shopping experience and ensuring the well-being of both customers and employees.

In January 2024, IKEA revealed plans to open a new store in the northern Kanto region of Japan. This store has been strategically located to serve the needs of the local communities, encompassing an area with a population of more than seven million individuals. Demonstrating IKEA's dedication to sustainability, IKEA Maebashi is set to become Japan's most environmentally friendly IKEA store, boasting the smallest operational climate impact.

Japan Commercial HVAC Industry Overview

The Japanese commercial HVAC market is fragmented and consists of several players. Companies in the market continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions, partnerships, and collaborations. Some of the major players include Carrier Corporation, Daikin Industries Ltd, Mitsubishi Electric Corporation, Hitachi Ltd, Panasonic Corporation, and many more.

In May 2024, Midea has introduced the EVOX G3 heat pump system. This new iteration of the EVOX series consists of the EVOX G3 Heat Pump and EVOX G3 Air Handling Unit (AHU). Available in sizes ranging from 1.5-ton to 5-ton units, the Midea EVOX G3 heat pumps are equipped with Enhanced Vapor Injection (EVI) technology and a multi-layer heat exchanger, guaranteeing reliable warmth without the need for auxiliary heat, even in extreme weather conditions.

In March 2024, Panasonic Corporation unveiled three new commercial air-to-water (A2W) heat pump models that utilize eco-friendly natural refrigerants designed for use in multi-dwelling units, stores, offices, and other light commercial properties.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Commercial Construction in the country

5.1.2 Increasing Demand For Energy Efficient Devices

5.2 Market Challenges

5.2.1 High Initial Cost of Energy Efficient Systems