일본의 플라스틱 포장용 필름 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2024-2029년)

Japan Plastic Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1550323

리서치사:Mordor Intelligence

발행일:2024년 09월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

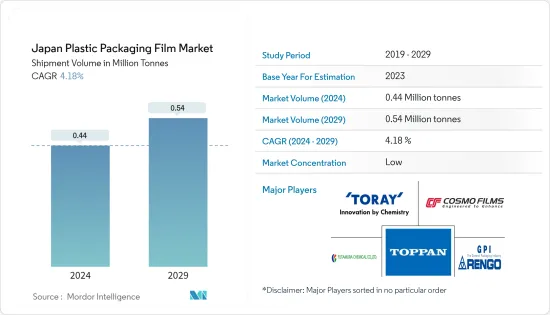

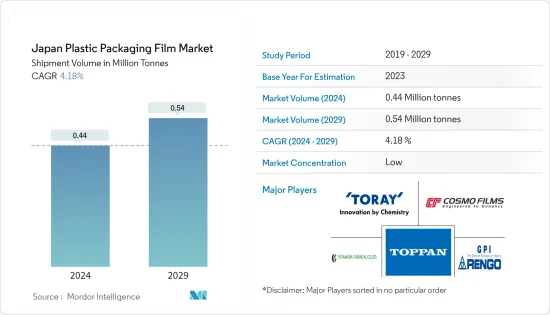

일본의 플라스틱 포장 필름 시장 규모(출하량 기반)는 예측 기간(2024-2029년)의 CAGR 4.18%로, 2024년 44만 톤에서 2029년에는 54만 톤으로 성장할 것으로 예측됩니다.

주요 하이라이트

일본에서는 식품 산업의 성장으로 플라스틱 필름의 판매가 급증하고 있습니다. 이러한 급격한 증가는 주로 필름의 우수한 수분 및 산소 차단 기능 때문입니다. 폴리프로필렌 포장용 필름의 화학적, 물리적 특성이 매력적이기 때문에 식품 및 음료 업계는 점점 더 폴리프로필렌 포장 필름에 매력을 느끼고 있습니다.

일본 산업계에서는 맞춤형 포장 솔루션이 요구되는 경우가 많습니다. 전자, 퍼스널케어, 제약 등 다양한 분야에 맞게 설계된 맞춤형 스트레치 필름은 이러한 다양한 요구에 부응하는 데 도움이 되고 있습니다.

주요 하이라이트

Nipro Corporation에 따르면 지난 수년간 일본의 의약품 포장 관련 매출은 2019년 355억 3,000만엔(2억 2,000만 달러)에서 2023년 517억 5,000만 엔(3억 2,000만 달러)으로 증가했습니다. 이러한 의약품 포장의 지속적인 증가는 앞으로도 계속될 것으로 예상되며, 그 결과 포장 필름과 스트레치 필름 수요를 견인할 것으로 예상됩니다.

또한 주요 상업 중심지에서의 E-Commerce 및 소매 활동이 급증함에 따라 운송 중 상품을 보호하기 위한 안전한 포장 솔루션, 특히 스트레치 필름에 대한 요구가 증가하고 있습니다. 스트레치 필름의 지속적인 기술 발전으로 인해 업계의 광범위한 요구 사항을 충족하도록 조정된 고성능의 다양한 제품이 탄생했습니다.

일본의 포장 산업은 오랫동안 대량의 플라스틱에 의존해 왔기 때문에 지속가능하고 재활용 가능한 포장 필름에 대한 수요가 증가하고 있습니다. 주요 제조업체는 비용 효율성이 높기 때문에 플라스틱 포장을 계속 선호하고 있습니다. 스트레치 필름과 같은 친환경적이고 재활용 가능한 포장재의 인기가 높아지는 것은 소비자의 선택과 규제 요구 사항의 결과입니다.

일본 정부는 2030년까지 플라스틱 포장재 재활용률을 60%, 일회용 플라스틱을 25% 감축하는 것을 목표로 새로운 플라스틱 순환 전략을 수립했습니다. 이 구상은 특히 폴리프로필렌 필름으로 만든 일회용 쇼핑백, 가방, 파우치, 봉지, 주머니에 대한 수요에 영향을 미쳐 시장 성장을 억제할 태세입니다.

일본의 플라스틱 포장 필름 시장 동향

폴리프로필렌(PP) 필름 수요 호조세가 매출 견인

폴리프로필렌 필름은 포장재로 점점 더 선호되고 있습니다. 밀도가 낮아 비용 효율적이며 폴리에틸렌, 폴리염화비닐, 폴리에스테르, 폴리에스테르, 셀로판 등 다양한 포장 용도의 대체 재료로 자리매김하고 있습니다. 이 필름은 식품 및 음료, 의약품, 퍼스널케어, 산업용 제품, 문구, 담배, 섬유에 이르기까지 다양한 산업 분야에 적용되고 있습니다.

일본의 식품 산업은 빠르게 성장하고 있으며, 이는 폴리프로필렌 필름의 판매를 증가시킬 것으로 보입니다. 폴리프로필렌 필름은 뛰어난 수분 및 산소 차단 능력이 뛰어나 식품 및 음료 회사들에게 유력한 선택이 되고 있습니다. 유통기한을 연장하고 습기, 공기 등 외부 요인으로부터 보호할 수 있으므로 기업은 폴리프로필렌 필름을 선호하고 있습니다.

위생에 대한 관심이 높아지면서 일본 소비자들은 특히 주거, 의료, 상업 분야에서 항바이러스 및 항균 제품에 대한 관심이 높아지고 있습니다. 고분자 살생물제를 함유한 폴리프로필렌 포장용 필름은 이러한 추세의 최전선에 있으며, 곰팡이와 박테리아를 포함한 다양한 미생물의 증식을 효과적으로 억제합니다. 이러한 필름에는 활성 항균제가 함유되어 있으며, 항진균 기능이 강화되어 있습니다.

이 시장은 주로 다양한 산업에서 연포장 필름의 채택이 증가함에 따라 성장을 목격하고 있습니다. 또한 특히 다른 플라스틱 식품 포장 필름에 비해 PP 포장 필름의 장점에 대한 인식이 높아짐에 따라 매출이 급증할 것으로 예상됩니다. 특히 일본의 식품 및 음료, 전자제품, 화장품 및 퍼스널케어 시장의 확대는 폴리프로필렌 포장용 필름 수요를 촉진하는 데 매우 중요한 역할을 하고 있습니다.

2024년 4월 일본 재무성 보고서에 따르면 일본의 전자제품 수출액은 2019년 585억 9,000만 달러에서 768억 7,000만 달러로 지난 수년간 지속적으로 증가했습니다. 수출 거래가 증가함에 따라 하이 배리어 PP 필름에 대한 수요도 전체 시장에서 증가할 것으로 예상됩니다.

캔디·제과의 수요로 매출 증가

일본은 아시아 최대 규모의 과자 시장을 자랑합니다. 일본 소비자들은 외국산 과자류를 선호하고 달콤한 과자를 즐겨 먹습니다. 특히 초콜릿과 과자류 동향은 계절에 따라 여러 번 바뀌기 때문에 일본 과자 시장은 역동적이며, 신규 진출기업에게는 매우 큰 기회가 될 수 있습니다.

건강과 웰빙에 대한 관심이 높아지면서 소비자들은 맛과 영양이 균형 잡힌 기호식품을 선호하고, 죄책감 없는 선택을 선호하고 있습니다. 이러한 추세는 제과업계의 기술 혁신에 박차를 가하고 있으며, 소비자들은 지속가능하고 친환경적이며 재활용이 가능한 포장 필름을 과자류에 사용하고자 하는 욕구를 불러일으키고 있습니다.

국내 제과 분야에서는 가볍고, 보호력이 뛰어나고, 시각적으로 매력적인 장벽이 높은 포장에 대한 수요가 증가하고 있으며, 이는 제과 포장 분야의 매출 증가로 이어질 것으로 보입니다. 이러한 패키지의 관능적인 매력은 구매 욕구를 불러일으킬 뿐만 아니라 시장 전망을 크게 향상시킬 수 있습니다.

전일본과자협회가 2024년 4월에 발표한 바에 따르면 2023년 일본의 과자류 생산량은 약 2,000톤에 달했습니다. 일본의 과자류는 스낵, 비스킷, 초콜릿과 함께 전통 일본 과자가 차지하고 있습니다.

Meiji Holdings, Ezaki Glico, Morinaga & Company 등 일본 제과업계의 주요 기업은 오랫동안 제과업계에서 자리를 잡아왔습니다. 주목할 만한 점은 아사히와 같이 과거에는 과자류와 관련이 없던 기업이 과자 제조로 다각화하여 경쟁 분야를 넓혀가고 있다는 점입니다. 이러한 다각화는 일본내 포장용 필름 수요를 증가시킬 것으로 보입니다.

일본의 플라스틱 포장 필름 산업 개요

일본의 플라스틱 포장 필름은 단편화되어 있으며, Toray Advanced Film, Cosmo Films Limited, Futamura Chemical, TOPPAN 등 중등도의 단편화를 보이고 있습니다. 시장은 원자재 및 포장 서비스를 공급하는 대기업과 현지 업체로 구성되어 있습니다. 포장 및 필름 재료의 최신 개발이 시장을 형성하고 있습니다.

2024년 3월 인쇄 및 포장 솔루션 프로바이더로 잘 알려진 TOPPAN(본사: 일본)은 지속가능한 포장을 위한 최첨단 배리어 필름 GL-SP를 발표했습니다. 인도의 TOPPAN Speciality Films(TSF)와의 제휴를 통해 개발된 이 선구적인 제품은 이축연신 폴리프로필렌(BOPP)을 기판으로 사용했습니다.

기타 혜택 :

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

바이어의 교섭력

공급 기업의 교섭력

대체품의 위협

신규 진출업체의 위협

경쟁 기업 간 경쟁 관계

산업 밸류체인 분석

제5장 시장 역학

시장 성장 촉진요인

경량 및 지속가능 포장에 대한 업계 전체의 수요 증가

식품 및 음료와 의약품 부문으로부터 견고한 수요가 성장을 촉진

시장 성장 억제요인

플라스틱 사용에 대한 정부의 엄격한 정책

제6장 시장 세분화

유형별

폴리프로필렌(이축연신 폴리프로필렌(BOPP), 캐스트 폴리프로필렌(CPP))

폴리에틸렌(저밀도 폴리에틸렌(LDPE), 선형 저밀도 폴리에틸렌(LLDPE))

폴리에틸렌 테레프탈레이트(이축연신 폴리에틸렌 테레프탈레이트(BOPET))

폴리스티렌

바이오 기반

PVC, EVOH, PETG, 기타 필름 유형

최종사용자별

식품

제과

냉동식품

신선식품

유제품

건물

육류, 가금육, 어개류

애완동물 사료

기타 식품

헬스케어

퍼스널케어 & 홈케어

산업용 포장

기타 최종사용자

제7장 경쟁 구도

기업 개요

Toray Advanced Film Co. Ltd

Futamura Chemical Co., Ltd.

Cosmo Films Limited

Toppan Packaging Product Co. Ltd.

Rengo Co., Ltd

Kingchuan Packaging

KISCO LTD

Gunze Limited

GSI Creos Corporation

Unitika LTD.

제8장 재활용과 지속가능성 전망

제9장 시장 기회와 향후 동향

KSA

영문 목차

영문목차

The Japan Plastic Packaging Film Market size in terms of shipment volume is expected to grow from 0.44 Million tonnes in 2024 to 0.54 Million tonnes by 2029, at a CAGR of 4.18% during the forecast period (2024-2029).

Key Highlights

The food industry's growth in Japan is poised to boost plastic film sales. This surge is primarily due to the films' exceptional moisture and oxygen barrier capabilities. The food and beverage sectors are increasingly drawn to polypropylene packaging films, enticed by their appealing chemical and physical attributes.

Japanese industries frequently demand bespoke packaging solutions for their distinct products. Tailored stretch films, designed for the electronics, personal care, and pharmaceutical sectors, are instrumental in addressing these varied requirements.

Key Highlights

According to Nipro Corporation, its pharmaceutical packaging-related sales in Japan increased in the past years from JPY 35.53 billion (USD 0.22 billion) in 2019 to JPY 51.75 billion (USD 0.32 billion) in 2023. This constant increase in pharmaceutical packaging is expected to continue in the future, consequently driving the demand for packaging films and stretch films.

Moreover, the surge in e-commerce and retail activities in major commercial hubs has heightened the need for secure packaging solutions, particularly stretch films, to safeguard goods during transit. Ongoing technological advancements in stretch films have resulted in the creation of high-performance variants tailored to meet a wide array of industry requirements.

Japan's packaging industry has long relied on significant amounts of plastic, prompting a growing demand for sustainable and recyclable packaging films. Major manufacturers continue to favor plastic packaging due to its cost-effectiveness. The increasing popularity of environmentally friendly and recyclable packaging materials, such as stretch films, is a result of consumer choices and regulatory requirements.

Japan's government has rolled out a fresh plastic circulation strategy, targeting a 60% recycling rate for plastic packaging and a 25% cut in single-use plastics by 2030. This initiative is poised to temper market growth, particularly impacting the demand for single-use shopping bags, sacks, pouches, and sachets crafted from polypropylene films.

Japan Plastic Packaging Film Market Trends

Strong Demand For Polypropylene (PP) Films Aids the Top-Line

Polypropylene film, an increasingly favored packaging material, is versatile. Its low density makes it cost-effective and positions it as a substitute for a range of materials, such as polyethylene, polyvinyl chloride, polyester, and cellophane, in numerous packaging applications. This film finds applications across various industries, from food and beverages, pharmaceuticals, and personal care to industrial goods, stationery, cigarettes, and textiles.

The burgeoning food industry in Japan is poised to bolster the sales of polypropylene films. These films stand out for their exceptional moisture and oxygen barrier capabilities, making them a prime choice for food and beverage companies. Businesses have been drawn to their products for their capacity to prolong shelf life and shield against external elements like moisture and air.

With a heightened focus on hygiene, Japanese consumers increasingly turn to antiviral and antibacterial products, especially in residential, medical, and commercial settings. Polypropylene packaging films infused with polymeric biocides are at the forefront of this trend, effectively inhibiting the growth of various microorganisms, including fungi and bacteria. These films are engineered with an active antimicrobial agent, bolstering their antifungal capabilities.

The market is witnessing growth primarily due to the rising adoption of flexible packaging films across diverse industries. Moreover, as awareness regarding the advantages of PP packaging films, especially in comparison to other plastic food packaging films, increases, sales are expected to surge. Notably, the expanding food & beverage, electronics, and cosmetics & personal care markets in Japan are playing a pivotal role in driving the demand for polypropylene packaging films.

According to Ministry of Finance Japan report in April 2024, the export value of electronics from Japan have been consistently increasing in the past few years from USD 58.59 billion in 2019 to USD 76.87 billion. With the increasing export trade the demand for hight-barrier PP films are also expected to increase across the market.

Demand From Candy & Confectionery Segments To Boost Sales

Japan boasts one of the largest confectionery markets in Asia. Japanese consumers exhibit a penchant for foreign confectionery, often indulging in sweet treats. Notably, chocolate and sweet confectionery trends shift multiple times within a season, rendering the Japanese confectionery market dynamic and a very significant opportunity for new players.

Amid a surge in health consciousness and a quest for wellness, consumers favor indulgences that strike a balance between taste and nutrition, leaning towards guilt-free options. This trend isn't just fueling innovation in the confectionery sector and driving consumers to seek sustainable, eco-friendly, and recyclable packaging films for their treats.

The country's confectionery sector's growing demand for lightweight, protective, visually appealing, and high-barrier packaging is set to drive up sales in the confectionery packaging segment. The sensory appeal of these packages not only entices purchases but also significantly boosts the market's prospects.

In 2023, Japan produced approximately two thousand metric tons of confectioneries, as reported by the All Nippon Kashi Association in April 2024. The nation's confectionery landscape is dominated by traditional Japanese confectioneries (wagashi), alongside snack foods, biscuits, and chocolates.

Key players in Japan's confectionery sector, such as Meiji Holdings, Ezaki Glico, and Morinaga & Company, have long been established in the industry. Notably, companies like Asahi, traditionally outside the confectionery realm, have diversified into sweet treat production, broadening the competitive field. This diversification is also poised to drive up the demand for packaging films in Japan.

Japan Plastic Packaging Film Industry Overview

Japan plastic film packaging is fragmented, displaying moderate fragmentation with Toray Advanced Film Co. Ltd, Cosmo Films Limited, Futamura Chemical Co., Ltd., TOPPAN Inc, and more. The market comprises major and local players supplying raw materials and packaging services. The latest developments in packaging and film materials are shaping the market.

March 2024: Toppan, a prominent printing and packaging solutions provider headquartered in Japan, has unveiled its latest offering, GL-SP, a cutting-edge barrier film designed for sustainable packaging. Developed in partnership with India's TOPPAN Speciality Films (TSF), this pioneering product uses biaxially oriented polypropylene (BOPP) as its base material.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Buyers

4.2.2 Bargaining Power of Suppliers

4.2.3 Threat of Substitutes

4.2.4 Threat of New Entrants

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand For Light-Weight and Sustainable Packaging Across Industries

5.1.2 Robust Demand From the Food, Beverage and Pharmaceutical Sector Aids Growth

5.2 Market Restraints

5.2.1 Stringent Government Policies Against the Use of Plastic