액티브 광케이블(AOC) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2024년)

Global Active Optical Cables (AOC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1549899

리서치사:Mordor Intelligence

발행일:2024년 09월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

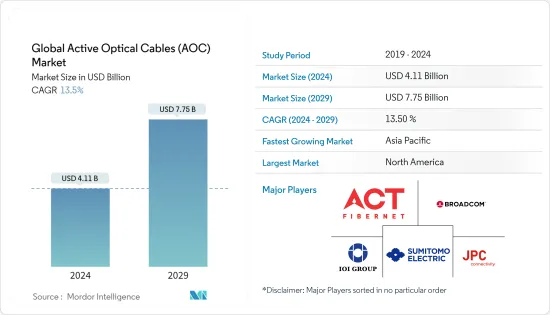

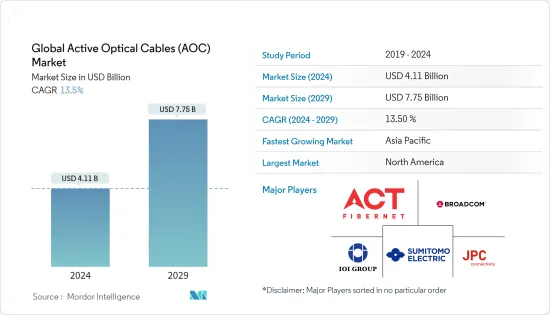

세계의 액티브 광케이블(AOC) 시장 규모는 2024년 41억 1,000만 달러로 추정되며, 2029년에는 77억 5,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 13.5%의 CAGR로 성장할 것으로 예상됩니다.

현재 액티브 광케이블 시장은 강력한 성장세를 보이고 있으며, 클라우드 기반 서비스, 디지털화, 5G, 데이터센터 및 기타 용도의 대규모 도입으로 인해 더욱 성장할 것으로 예상됩니다.

주요 하이라이트

액티브 광케이블(AOC) 시장은 데이터센터, 통신, 가전 등 다양한 애플리케이션에서 고속 데이터 전송에 대한 요구가 증가하고 있는 것이 주요 요인으로 작용하고 있습니다. 다양한 애플리케이션을 통한 데이터 수요 증가는 AOC 시장 수요를 견인할 것으로 예상됩니다.

데이터센터 시장은 클라우드 기술의 대규모 적용, 디지털화, AI/ML에 대한 수요 증가로 인해 빠르게 성장하고 있습니다. 통신 서비스 제공 업체인 Cloudscene에 따르면 2023년 12월 현재 전 세계에는 약 10,978개의 데이터센터가 있으며, 그 수는 빠르게 증가하고 있습니다. 데이터센터는 견고하고 빠른 인터넷 연결이 필요합니다. 따라서 데이터센터 시장의 성장은 AOC 시장도 견인할 것으로 예상됩니다.

5G의 도입은 디지털 업무 강화에 필수적인 효율적인 통신에 대한 수요 증가에 대응하기 위한 것으로, 5G의 광대역 파장은 빠른 데이터 전송을 가능케 하지만 3G나 4G에 비해 신호 도달 거리가 제한되어 있습니다. 따라서 견고한 5G 네트워크는 신호 전송을 위한 고속 케이블에 의존하는 셀 타워를 촘촘히 배치해야 하기 때문에 AOC 시장에 대한 수요가 증가하고 있습니다.

GSMA는 2029년까지 5G 연결이 전체 모바일 연결의 절반 이상(51%)을 차지하고 10년 후에는 56%까지 증가하여 5G가 주요 연결 기술로 자리 잡을 것으로 예상하고 있으며, 5G는 지금까지의 모든 모바일 세대를 뛰어넘어 2023년 말까지 1,600억 연결을 넘어설 것으로 예상하고 있습니다. 까지 16억 연결을 넘어설 것이며, 2030년에는 55억 연결에 도달할 것으로 예상됩니다. 이에 따라 5G의 급속한 확장에 따라 세계의 액티브 광케이블 시장은 가까운 미래에 큰 성장을 이룰 것으로 예상됩니다.

광전송의 보안에 대한 우려와 민감한 데이터 애플리케이션의 잠재적 취약성은 AOC의 보급을 방해할 수 있습니다. 또한 AOC는 기존 구리 케이블에 비해 유지보수 및 수리에 큰 어려움을 초래하는 경우가 많으며, 특히 신속한 서비스 개입이 필요한 분야에서는 더욱 그렇습니다.

세계의 액티브 광케이블(AOC) 시장 동향

데이터센터 내 액티브 광케이블 수요 증가로 시장 견인

세계의 액티브 광케이블(AOC) 시장은 업계 전반의 고속 데이터 전송 수요 급증에 힘입어 최근 몇 년 동안 큰 폭의 성장세를 보이고 있습니다. 기술의 발전과 함께 효율적이고 신뢰할 수 있는 연결 솔루션의 중요성이 그 어느 때보다 높아지고 있습니다. 액티브 광케이블(AOC)은 레이저, 포토다이오드 등의 능동 소자를 케이블 어셈블리에 직접 통합한 고속 케이블 솔루션으로 각광받고 있습니다. 이러한 구성요소는 광섬유 케이블을 통한 광신호 전송을 촉진하는 매우 중요한 역할을 합니다. 데이터센터 영역에서 '200G AOC'라는 용어는 특히 초당 200기가비트(Gbps)의 데이터 속도를 지원하도록 설계된 케이블을 가리킵니다.

또한, 200G AOC는 방대한 연산 능력을 필요로 하는 고성능 컴퓨팅(HPC) 환경에서 프로세서와 스토리지 유닛 간의 빠른 데이터 교환을 촉진합니다. 기업들은 고성능 컴퓨팅을 병렬 처리에 활용하여 AI 및 데이터 분석과 같은 고도의 프로그램 실행을 지원하고 있습니다. 특히 AI와 머신러닝을 중시하는 데이터센터는 HPC를 통해 큰 이점을 얻을 수 있습니다.

Flexera State of the Cloud Report 2023에 따르면, 72%의 기업이 하이브리드 클라우드를 채택하고 있으며, 조직 내 클라우드 컴퓨팅의 부상은 데이터센터 시장을 크게 견인하고 있습니다. 그러나 이러한 전환은 기존의 프라이빗 및 퍼블릭 클라우드 인프라를 넘어서는 경우가 많습니다.

AOC(Active Optical Cable)는 데이터센터의 케이블 랙과 스위치를 연결하는 데 매우 중요한 역할을 하며, 스위치와 서버 간의 원활한 통신을 가능하게 합니다. 일반적으로 데이터센터는 먼저 스위치를 설치한 후 구조화된 케이블을 도입하고 마지막으로 네트워크 액세스에 적합한 상호 연결 제품을 선택하는데, 10G의 경우 90미터 이하, 40G의 경우 10미터 이하로 정의되는 단거리에서는 구리 케이블이 가장 비용 효율적인 선택입니다. 10G의 경우 500m 미만, 40G의 경우 150m 미만의 중거리에서는 다중 모드 VCSEL(수직 공진기면 발광 레이저) 트랜시버가 선호되며, 종종 AOC로 보완됩니다.

인도의 데이터센터 시장은 크게 성장하여 2025년 46억 달러 규모에 이를 것으로 예상됩니다. 이러한 성장에는 국내 인터넷 사용자 수 증가, 클라우드 컴퓨팅에 대한 수요 증가, 정부의 디지털화 추진 노력, 디지털 서비스 제공업체들의 현지화 전환 등의 요인이 작용했습니다. 특히 인도의 데이터센터 부문은 신흥국 시장과 비교해 시장 개척 단계와 운영 단계에서 비용 측면에서 큰 우위를 점하고 있다는 점을 주목할 필요가 있습니다. 현재 데이터센터의 주요 거점은 주로 뭄바이, 벵갈루루, 첸나이, 델리(NCR), 하이데라바드, 푸네에 있으며, 캘커타, 케랄라, 아메다바드에도 새로운 데이터센터가 생겨나고 있습니다. 데이터센터 투자가 확대됨에 따라 인도 전역에서 IT, 전기, 기계, 일반 건축을 아우르는 부수적인 인프라 서비스 수요도 증가하고 있습니다.

북미가 큰 비중을 차지

북미는 세계 최대의 데이터센터 시장으로, 현재 하이퍼스케일 데이터센터 건설이 눈에 띄게 증가하고 있습니다. 클라우드 서비스에 대한 수요 증가와 디지털 혁신의 진행이 주요 요인으로, 클라우즈씬(Cloudscene)이 발표한 2024년 3월 기준 최신 데이터에 따르면 미국이 5,381개의 데이터센터를 보유해 세계 선두를 달리고 있습니다. 독일이 521개, 영국이 514개로 근소한 차이로 뒤를 이었습니다. 역사적으로 구리 케이블은 서버, 라우터, 스위치 간의 네트워크 연결에 사용되어 왔습니다. 데이터센터가 확장됨에 따라 이 지역의 액티브 구리 케이블에 대한 수요는 지속적으로 증가하고 있습니다.

미국에서는 새로운 데이터센터에 대한 수요가 여전히 강하고 매주 새로운 프로젝트가 발표되고 있으며, 2024년 3월 아마존은 버윅 원자력발전소에 인접한 데이터센터를 인수하기 위해 6억 5,000만 달러의 거액을 투자할 계획을 밝혔습니다. 이 계획은 세일럼 타운십에 위치한 서스케하나 증기 발전소를 운영하는 탈렌 에너지(Talen Energy)가 확인한 것으로, 아마존의 웹 서비스 부문이 새로운 데이터센터 개발을 주도할 예정입니다.

미국 내 초고속 인터넷의 개척도 세계 AOC 시장을 견인하는 큰 요인입니다. 미국 농무부(USDA)는 사업자들의 네트워크 구축을 지원하기 위해 총 9,700만 달러를 지원하기로 약속했습니다. 이 네트워크는 2027년까지 미국 정부가 설정한 목표인 100Mbps의 다운로드 속도와 20Mbps의 업로드 속도에 미치지 못하거나, 2027년까지 미국 전역의 모든 가구에 연결이 부족한 지역을 대상으로 합니다. 이번 노력으로 11개 주에 걸쳐 22,000명의 가입자에게 서비스를 강화할 예정입니다.

그린시티의 노스이스트 미주리 유선전화회사(North East Missouri Rural Telephone Company)는 6개 교환국을 구리선에서 파이버투더프리미스(Fiber-to-the-Premise) 기술로 전환하기 위해 1,370만 달러의 융자를 받았습니다. 이 프로젝트는 1,063명의 가입자에게 더 나은 서비스를 제공하기 위해 약 500 루트 마일의 광섬유를 설치하게 됩니다.

2023년 10월, 미국 연방통신위원회(FCC)는 지방의 광대역 인프라를 강화하기 위해 약 182억 8,000만 달러의 대규모 투자를 시작했습니다. 이 자금은 2024년 1월부터 15년간의 프로그램에 배정되었으며, 70만 곳 이상에 100/20Mbps 광대역 배치를 목표로 하고 있습니다. 또한, 44개 주에 걸쳐 약 200만 곳의 기존 서비스를 업그레이드하는 것을 목표로 하고 있습니다. 이 야심찬 광대역 확대는 AOC 시장에 큰 영향을 미칠 것으로 보입니다.

세계의 액티브 광케이블(AOC) 산업 개요

액티브 광케이블(AOC) 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 ACT, Broadcom Inc., Sumitomo Electric, JPC Connectivity 등이 있습니다. 이 시장의 기업들은 서비스 제공을 강화하고 지속가능한 경쟁 우위를 확보하기 위해 제휴, 계약, 혁신, 인수 등의 전략을 채택하고 있습니다.

2024년 1월 광섬유 솔루션 분야의 선도기업인 OFS가 최신 혁신 제품인 LaserWave Dual-Band OM4 멀티 모드 광섬유를 발표했습니다. 이미 높은 평가를 받고 있는 OM4 및 OM5 제품군에 추가된 이 멀티 모드 광섬유는 대역폭, 감쇠 및 형상 측면에서 새로운 기준을 제시하는 LaserWave Dual-Band OM4는 양방향(BiDi) 애플리케이션을 위해 세심하게 제작된 프리미엄급이면서 양방향(Bi-Di) 애플리케이션을 위해 세심하게 제작된 프리미엄급이지만 비용 효율적인 파이버로 돋보입니다. 이 광섬유는 고밀도, 저전력 멀티 모드 링크를 강화하기 위해 설계되었습니다. 또한 850nm 및 910nm 파장에서 OM5와 동등한 성능을 발휘할 수 있어 양방향 전송에 필수적입니다. 이는 800G-SR4.2 및 1.6T-SR8.2를 포함한 테라비트 BiDi 이더넷과 같은 최첨단 애플리케이션에 필수적인 지표인 일관된 100미터 도달거리를 보장합니다.

2024년 1월 Telstra International은 Trans Pacific Networks(TPN)와 제휴하여 미국과 싱가포르를 직접 연결하는 최초의 해저 케이블인 Echo 케이블 시스템을 도입함. 에코 케이블의 첫 번째 구간은 괌과 미국을 연결하는 전용 광섬유 회선으로 2024년 중반에 개통될 예정이며, 이후 구간은 2025년에 개통될 예정입니다. 완공되면 캘리포니아, 자카르타, 싱가포르, 괌을 완벽하게 연결하게 됩니다. 텔스트라는 이 시스템이 새로운 경로를 개척할 뿐만 아니라 저지연, 고속, 견고한 내결함성을 특징으로 하는 네트워크 인프라를 약속한다고 강조했습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

거시경제 시나리오 분석(경기후퇴, 러시아·우크라이나 위기 등)

COVID-19 팬데믹의 영향과 회복 평가

제5장 시장 역학

시장 성장 촉진요인

광네트워크 고속화를 향한 통신 분야 변화

광대역화 요구 상승

데이터센터의 액티브 광케이블 수요 증가

디지털화와 5G 접속 높은 보급률

시장 과제

막대한 초기 비용과 네트워크 보안 파이버 해킹

소비 전력에 대한 우려

기술적 전문 지식의 부족

가격과 기술 사양 분석

직접 연결 케이블(액티브 및 패시브) 대액티브 광케이블에 관한 기술 인사이트

세계 무역 분석

AOC 가장 일반적인 폼팩터 사양에 관한 주요 인사이트

AOC 각종 프로토콜 유형에 관한 인사이트

제6장 시장 세분화

용도별

데이터센터

통신

고성능 컴퓨팅(HPC)

가정용 전자기

산업용 용도

기타 용도

지역별

북미

미국

캐나다

유럽

영국

독일

프랑스

아시아

중국

인도

일본

호주·뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 상황

기업 개요

JPC Connectivity

Shenzhen Sopto Technology Co. Ltd

Linkreal Co. Ltd

Broadcom

Sumitomo Electric Lightwave Inc.

Black Box

ACT

IOI Technology Corporation

ETU-Link Technology Co. Ltd

Amphenol Corporation

제8장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Global Active Optical Cables Market size is estimated at USD 4.11 billion in 2024, and is expected to reach USD 7.75 billion by 2029, growing at a CAGR of 13.5% during the forecast period (2024-2029).

The active optical cables market is currently experiencing robust growth, and it is expected to grow further owing to the large-scale adoption of cloud-based services, digitalization, 5G, data centers, and other applications.

Key Highlights

The active optical cable (AOC) market is mostly driven by the increasing need for high-speed data transmission in a variety of applications, including data centers, telecommunications, and consumer electronics. The growing need for data through various applications is expected to drive the demand for the AOC Market.

The data center market is growing rapidly owing to the large-scale application of cloud technologies, digitalization, and growing demand for AI/ML. According to Cloudscene, a telecommunication services provider, there are approximately 10,978 data center locations worldwide as of December 2023, with numbers growing rapidly. Data centers require robust and high-speed internet connectivity. Therefore, the growth in the data center market is anticipated to drive the AOC market as well.

5G implementation is poised to meet the escalating demand for efficient communication, which is crucial for enhancing digital operations. While 5G's broader wavelength enables rapid data transmission, its signals are limited in range compared to 3G and 4G. Consequently, a robust 5G network necessitates a dense array of cell towers, each reliant on high-speed cables for signal transmission, thereby bolstering the demand for the AOC market.

GSMA forecasts that 5G connections will account for over half (51%) of all mobile connections by 2029, climbing to 56% by the decade's end, solidifying 5G as the leading connectivity technology. 5G has outpaced all previous mobile generations in its rollout, exceeding 1.6 billion connections by the end of 2023, and it is projected to reach 5.5 billion by 2030. Consequently, as 5G continues its rapid expansion, the global active optical cables market is poised for significant growth in the near future.

Concerns over the security of optical transmissions and potential vulnerabilities in sensitive data applications may impede the widespread adoption of AOCs. Additionally, AOCs often pose greater maintenance and repair challenges compared to traditional copper cables, particularly in sectors requiring swift service interventions.

Global Active Optical Cables (AOC) Market Trends

Rising Demand for Active Optical Cable in Data Centers to Drive the Market

The global active optical cable (AOC) market has witnessed significant growth in recent years, propelled by the surging demand for high-speed data transmission across industries. With technological advancements, the emphasis on efficient and dependable connectivity solutions has never been more critical. Active optical cables (AOCs) stand out as high-speed cabling solutions, incorporating active elements like lasers and photodiodes directly into the cable assembly. These components are pivotal, facilitating the transmission of optical signals through fiber optic cables. In the realm of data centers, the term '200G AOC' specifically denotes cables engineered to support data rates of 200 gigabits per second (Gbps).

Additionally, in high-performance computing (HPC) settings demanding substantial computational power, the 200G AOC facilitates swift data exchange between processors and storage units. Organizations leverage high-performance computing for parallel processing, empowering them to execute advanced programs like AI and data analytics. Data centers, especially those emphasizing AI and machine learning, stand to gain significantly from HPC.

The rise of cloud computing within organizations significantly drives the data center market. According to the Flexera State of the Cloud Report 2023, 72% of companies have adopted hybrid clouds. Yet, this transition frequently means moving beyond conventional private and public cloud infrastructures.

Active optical cables (AOCs) are pivotal in connecting data center cabling racks and switches, enabling seamless communication between switches and servers. Typically, data centers first install switches, then implement structured cabling, and finally, select the appropriate interconnect products for network access. Copper cables are the most cost-effective choice for short distances, defined as under 90 meters for 10G and under 10 meters for 40G. For medium distances spanning under 500 meters for 10G and 150 meters for 40G, multimode VCSEL (vertical cavity surface emitting laser) transceivers are favored, often complemented by AOCs.

India's data center market is set for a significant uptick, with forecasts pointing to a climb to USD 4.6 billion by 2025. This growth is fueled by several factors: a growing domestic internet user base, rising demands for cloud computing, government initiatives driving digitalization, and a shift toward localization by digital service providers. Notably, India's data center sector boasts a significant cost advantage, both in its development and operational phases, compared to more mature markets. Currently, key data center hubs are primarily located in Mumbai, Bengaluru, Chennai, Delhi (NCR), Hyderabad, and Pune, with emerging centers in Calcutta, Kerala, and Ahmedabad. As investments in data centers expand, so does the demand for ancillary infrastructure services covering IT, electrical, mechanical, and general construction throughout India.

North America to Hold a Major Share

North America boasts the world's largest data center market, currently experiencing a notable rise in hyperscale data center construction. This surge is primarily fueled by the escalating demand for cloud services and the ongoing digital transformation. Recent data from Cloudscene, as of March 2024, highlights the United States as the global leader, housing 5,381 reported data centers. Germany and the United Kingdom follow closely, with 521 and 514 centers, respectively. Historically, copper cables have been the go-to for networking links between servers, routers, and switches. With the expanding data center landscape, the demand for active copper cables in the region is set to rise.

The demand for new data centers in the United States remains strong, with fresh projects unveiled almost weekly. In March 2024, Amazon disclosed its plan to invest a hefty USD 650 million in acquiring a data center adjacent to the Berwick nuclear power plant. This initiative, confirmed by Talen Energy, the operator of the Susquehanna Steam Electric Station in Salem Township, will see Amazon's web services arm spearhead the development of the new data center.

The development of high-speed internet in the United States is also a major factor driving the global AOC market. The US Department of Agriculture (USDA) has pledged a total of USD 97 million to assist operators in establishing networks. These networks are aimed at areas lacking connectivity or falling below the US government's set target of 100 Mbps download and 20 Mbps upload speeds for all American households by 2027. This initiative is set to enhance services for 22,000 subscribers across 11 states.

Green City's Northeast Missouri Rural Telephone Company secured a USD 13.7 million loan to transition six exchanges from copper to fiber-to-the-premises technology. This initiative involves laying down approximately 500 route miles of fiber, with the aim of enhancing services for 1,063 subscribers.

In October 2023, the US Federal Communications Commission (FCC) initiated a significant investment of approximately USD 18.28 billion to strengthen rural broadband infrastructure. This funding, allocated for a 15-year program commencing in January 2024, targets the deployment of 100/20 Mbps broadband to over 700,000 locations. Furthermore, it aims to upgrade existing services for approximately 2 million locations spread across 44 states. This ambitious broadband expansion is set to have a profound impact on the AOC market.

Global Active Optical Cables (AOC) Industry Overview

The active optical cables (AOC) market is fragmented in nature. Some major players in the market studied are ACT, Broadcom Inc., Sumitomo Electric, JPC Connectivity, etc. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

January 2024: OFS, a prominent figure in the fiber optic solutions realm, unveiled its latest innovation: the LaserWave Dual-Band OM4+ Multimode Optical Fiber. This addition to the lineup, alongside the already esteemed OM4 and OM5 offerings, sets new benchmarks in bandwidth, attenuation, and geometry. The LaserWave Dual-Band OM4+ stands out as a premium yet cost-effective fiber, meticulously crafted for bidirectional (BiDi) applications. It is tailored to bolster the upcoming wave of high-density, low-power multimode links. Its capability to deliver performance akin to OM5 at both 850 nm and 910 nm wavelengths is also noteworthy, which is crucial for bidirectional transmissions. This ensures a consistent 100-meter reach, a vital metric for cutting-edge applications like Terabit BiDi Ethernet, including 800G-SR4.2 and 1.6T-SR8.2.

January 2024: Telstra International teamed up with Trans Pacific Networks (TPN) to introduce the Echo cable system, marking the inaugural subsea cable directly linking the United States and Singapore. The initial segment of the Echo cable, a dedicated fiber-optic line linking Guam and the United States, is set for a mid-2024 debut, with subsequent segments slated for 2025. Upon completion, the cable will seamlessly link California, Jakarta, Singapore, and Guam. Telstra emphasizes that this system will not only forge a new route but also promise a network infrastructure characterized by low latency, high speeds, and robust resilience.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definitions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Analysis of Macro-economic Scenarios (Recession, Russia-Ukraine Crisis, etc.)

4.3 An Assessment of the Impact of and Recovery from COVID-19 Pandemic

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Change in the Telecom Sector Toward Faster Optical Networks

5.1.2 Increased Need for Higher Bandwidth

5.1.3 Rising Demand for Active Optical Cable in Data Centers

5.1.4 Digitalization and High Adoption of 5G Connectivity

5.2 Market Challenges

5.2.1 Significant Initial Cost and Optical Network Security Fiber Hacking

5.2.2 Significant Power Consumption Concerns

5.2.3 Lack of Technical Expertise

5.3 Analysis of Pricing and Technical Specifications

5.4 Technology Insights on Direct Attach Cables (Active and Passive) vs. Active Optical Cable

5.5 Global Trade Analysis

5.6 Key Insights into Most Common Form Factor Specifications of AOC

5.7 Key Insights into Various Protocol Types of AOC