ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

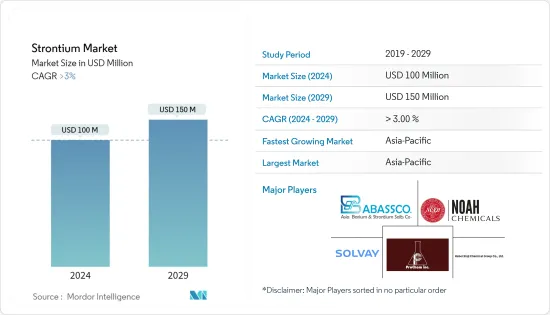

스트론튬 시장 규모는 2024년 1억 달러로 추정되며, 2029년에는 1억 5,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 연평균 3% 이상 성장할 것으로 예상됩니다.

COVID-19는 스트론튬 시장에 부정적인 영향을 미쳤습니다. COVID-19로 인해 스트론튬 채굴, 가공 및 운송 활동이 중단되어 스트론튬 원료 및 중간 제품 수급에 영향을 미쳤습니다. 그러나 조업이 재개되면서 스트론튬 기반 제품의 주요 소비처인 자동차 및 전자제품을 포함한 산업 전반에 걸쳐 경제 활동이 서서히 재개되었습니다. 시장 회복을 주도한 것은 상품 수요의 증가로 스트론튬 함유 제품의 증가로 이어졌습니다.

주요 하이라이트

스트론튬 시장을 견인할 것으로 예상되는 요인은 페인트 및 코팅의 스트론튬 수요 증가와 신흥국의 건설 활동으로 인한 스트론튬 수요 증가입니다.

반면, 스트론튬에 따른 폭발 및 화재의 위험성은 시장 성장을 저해할 것으로 예상됩니다.

질산 스트론튬은 주로 화학, 해양 및 방위 산업에서 사용될 것으로 예상됩니다. 의료 분야에서의 사용 증가는 시장 참여자들에게 유리한 기회를 제공할 것으로 예상됩니다.

중국, 인도, 일본 등의 국가에서 소비가 증가함에 따라 아시아태평양은 예측 기간 동안 시장 우위를 유지할 것으로 예상됩니다.

스트론튬 시장 동향

시장을 독점하고 있는 페인트 및 코팅 부문

황산 스트론튬은 페인트 및 코팅 산업에서 황산 스트론튬으로 사용됩니다. 황산 스트론튬은 백색, 무취, 무해한 화학적 불활성 분말입니다. 안료 익스텐더(필러) 역할을하여 액체 페인트 및 분말 페인트의 성능을 향상시킬 수 있습니다.

또한 높은 도막 피복성, 우수한 기계적 특성, 내염성, 내분무성, 내자외선성 등의 분야에서 우수한 성능을 발휘합니다. 주로 플라스틱, 액체 도료, 분말 도료 등에 사용됩니다.

미국 페인트 협회가 2023년 8월에 발표한 추산에 따르면 미국의 페인트 및 코팅 시장 규모는 2022년 318억 5,000만 달러, 2023년에는 335억 5,000만 달러에 달할 것으로 예상했습니다. 이 금액은 2024년에는 357억 2,000만 달러에 달할 것으로 예상됩니다.

미국 코팅 협회의 연례 보고서에 따르면 미국의 페인트 및 코팅 생산량은 2023년 약 13억 1,000만 갤런에 도달했으며 2024년에는 13억 4,000만 갤런을 초과 할 것으로 예상됩니다.

유럽에는 많은 대형 도장 회사가 있으며, 4대 주요 경제국은 독일, 프랑스, 이탈리아, 스페인, 독일, 프랑스, 이탈리아, 스페인입니다. 독일은 유럽에서 페인트와 코팅의 중요한 공급국이자 시장입니다. 독일에는 페인트, 바니시, 프린터 잉크 분야에서 300개 이상의 제조 회사가 있습니다.

세계도료코팅협회(WPCIA) 보고서에 포함된 도료 및 코팅 분야의 주요 기업으로는 Sherwin Williams, PPG Industries Inc., Akzo Nobel NV, and Nippon Paint Holdings 등이 있습니다.

이것은 다양한 분야에 대한 자금 투입을 가능하게 하고, 전 세계 페인트 및 코팅제에 대한 수요를 증가시켜 스트론튬 시장을 지원할 것입니다.

아시아태평양이 시장을 지배

아시아태평양은 페인트, 코팅, 화장품, 전기 및 전자기기 등 스트론튬을 원료로 한 다양한 최종 제품의 생산과 소비로 인해 스트론튬의 가장 중요한 시장입니다.

인도 상무부 산업 및 국내 무역 진흥국(인도)이 발표한 보고서에 따르면 2022 회계연도 인도 페인트 부문의 교역액은 600억 루피를 넘어섰습니다. 인도의 페인트 및 관련 제품 수출액은 약 229억 6,000만 인도 루피, 수입액은 377억 인도 루피 이상이었습니다.

또한 중국 건설 업계는 아시아태평양이 가장 빠르게 성장하고 인도가 그 뒤를 이을 것으로 예상하고 있습니다. 중국 정부는 주택 수요 증가에 대응하기 위해 저렴한 주택을 건설할 수 있도록 더 많은 자금을 지원하고 있습니다. 인프라 부문은 인도 정부의 주요 중점 분야 중 하나입니다.

중국의 건축 및 건설 산업은 빠른 속도로 성장하고 있습니다. 중국 국가통계국이 발표한 추산에 따르면 2022년 말 중국의 건설 생산액은 약 31조 2,000억 위안(4조 3,100억 달러), 2023년에는 31조 5,900억 위안(4조 3,700억 달러)에 달할 것으로 추산됩니다.

이러한 모든 건설 활동과 정부 정책으로 인해 건축 프로젝트가 증가하여 페인트와 바니시의 수요가 증가할 것으로 예상됩니다.

아시아태평양의 많은 산업이 성장을 추구함에 따라 스트론튬에 대한 수요도 향후 5년 동안 증가할 것으로 예상됩니다.

스트론튬 산업 개요

스트론튬 시장은 그 특성상 매우 세분화되어 있습니다. 시장의 주요 기업은(순서에 관계없이) Solvay, Abassco, Hebei Xinji Chemical Group, Noah Chemicals, ProChem Inc. 등입니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

페인트 및 코팅 부문으로부터의 수요 증가

아시아태평양 신흥 국가의 건설 활동 증가

성장 억제요인

스트론튬에 따른 폭발·화재 위험성

기타 저해요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

가격 동향

제5장 시장 세분화

제품별

탄산 스트론튬

황산 스트론튬

질산 스트론튬

기타 제품(수산화 스트론튬)

용도별

전기·전자

의료·치과

페인트 및 코팅

퍼스널케어

폭죽

기타 용도(유리, 세라믹)

지역별

생산 분석

중국

스페인

터키

멕시코

이란

아르헨티나

세계 기타 지역

소비 분석별

아시아태평양

중국

인도

일본

한국

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

터키

러시아

노르딕

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

나이지리아

이집트

카타르

아랍에미리트

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율(%)/순위 분석

주요 기업의 전략

기업 개요

Abassco

Barium & Chemicals Inc.

Chongqing Yuanhe Fine Chemicals Inc.

Fertiberia

Hebei Xinji Chemical Group Co. Ltd

Joyieng Chemical Limited

KBM Affilips

Nanjing Jinyan Strontium Industry Co. Ltd

Noah Chemicals

ProChem Inc.

SAKAI CHEMICAL INDUSTRY CO. LTD

Shenzhou Jiaxin Chemical Co. Ltd

Shijiazhuang Zhengding JINSHI Chemical Co. Ltd

Solvay

제7장 시장 기회와 향후 동향

화학, 해양, 방위 분야에서의 질산 스트론튬 사용 증가

의료 분야에서의 사용 증가

ksm

영문 목차

영문목차

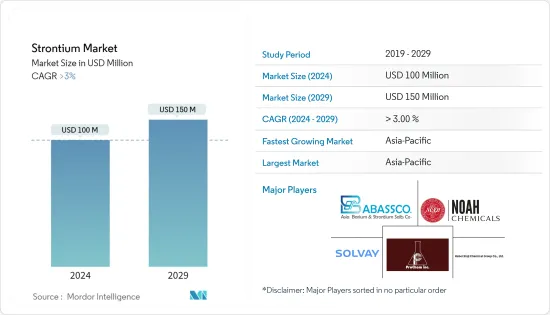

The Strontium Market size is estimated at USD 100 million in 2024, and is expected to reach USD 150 million by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the strontium market. The pandemic disrupted strontium mining, processing, and transportation activities, affecting the availability of strontium raw materials and intermediate products. However, as lockdowns were lifted, economic activities gradually resumed across industries, including automotive and electronics, which are significant consumers of strontium-based products. The market recovery was driven by increased demand for goods, which led to a rise in strontium-content products.

Key Highlights

The factors that are expected to drive the strontium market are the rising demand for strontium from paints and coatings and the increasing demand for strontium from construction activities in developing countries.

On the flip side, the risk of explosion and fire hazards that are associated with strontium is expected to hinder the growth of the market.

It is expected that strontium nitrate will be used majorly in the chemical, marine, and defense industries. The increasing usage in the medical field is expected to provide lucrative opportunities for the market players.

Due to increasing consumption in countries such as China, India, and Japan, the Asia-Pacific is expected to maintain its dominance of the market during the forecast period.

Strontium Market Trends

Paints and Coatings Segment to Dominate the Market

Strontium sulfate is used in the paint and coating industry as strontium sulfate. Strontium sulfate is a white, odorless, and unhazardous chemical inert powder. It improves the performance of liquid paint and powder coatings by acting as a pigment extender (filler).

In addition, it provides higher film coverage, more extraordinary mechanical properties, and excellent performance in the areas of salt, fog, or UV resistance. It's mainly used in plastics, liquid paints, powder coats, and so on.

According to the estimate released by the American Coatings Association in August 2023, the market value of paints and coatings in the United States was USD 31.85 billion in 2022 and USD 33.55 billion in 2023. This value is expected to reach USD 35.72 billion in 2024.

The volume of paint and coating production in the United States reached about 1.31 billion gallons in 2023, according to an annual report from the American Coatings Association. It is forecasted that the industry's production will surpass 1.34 billion gallons in 2024.

Europe is home to a multitude of large painting companies, with its four largest mainland economies: Germany, France, Italy, and Spain. Germany is a significant provider and market of paints and coatings in Europe. It is home to over 300 production companies in the field of paint, varnish, and printer ink.

Some of the key firms in the paints and coatings sector included in the World's Paints and Coatings Association (WPCIA) report are Sherwin Williams, PPG Industries Inc., Akzo Nobel NV, and Nippon Paint Holdings Co. Ltd.

This will make it possible to invest more money in different sectors, which will increase demand for paints and coatings from all over the world and help the strontium market.

Asia-Pacific Region to Dominate the Market

Due to the production and consumption of a wide range of end products made from strontium, including paints and coatings, cosmetics, electrical and electronic equipment, and others, the Asia Pacific region is the most critical market for strontium.

According to the report published by the Department of Commerce (India), Department for Promotion of Industry and Internal Trade (India), in fiscal year 2022, the trade value of India's paint sector was over INR 60 billion. The value of exported paint and associated products in the country stood at around INR 22.96 billion, compared to more than INR 37.7 billion for imports.

In addition, Asia-Pacific is likely to grow fastest in Chinese construction, followed by India. In order to meet the increasing demand for housing, the Chinese government has provided more funds so that affordable houses can be built. The infrastructure sector has become one of the main focus areas of the government in India.

The Chinese building and construction industry is expanding at a rapid pace. Construction output in China was estimated to be worth about CNY 31.2 trillion (USD 4.31 trillion) at the end of 2022, reaching CNY 31.59 trillion by 2023 (USD 4.37 trillion), according to an estimate released by the Chinese National Statistics Office.

The number of building projects in this country is expected to increase due to all these construction activities and government measures, which are expected to lead to a higher demand for paints and varnishes.

The demand for strontium is also expected to increase over the next five years, as many industries in Asia-Pacific are looking for growth.

Strontium Industry Overview

The strontium market is highly fragmented in nature. The major players in the market include (not in any particular order) Solvay, Abassco, Hebei Xinji Chemical Group Co. Ltd, Noah Chemicals, and ProChem Inc.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increased Demand from the Paints and Coatings Segment

4.1.2 Increasing Construction Activities in Emerging Economies of Asia-Pacific

4.2 Restraints

4.2.1 Risk of Explosion and Fire Hazards Associated with Strontium

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Price trends

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Product

5.1.1 Strontium Carbonate

5.1.2 Strontium Sulfate

5.1.3 Strontium Nitrate

5.1.4 Other Products (Strontium Hydroxide)

5.2 By Application

5.2.1 Electrical and electronics

5.2.2 Medical and Dental

5.2.3 Paints and Coatings

5.2.4 Personal Care

5.2.5 Pyrotechnic

5.2.6 Other Applications (Glass and Ceramics)

5.3 By Geography

5.3.1 Production Analysis

5.3.1.1 China

5.3.1.2 Spain

5.3.1.3 Turkey

5.3.1.4 Mexico

5.3.1.5 Iran

5.3.1.6 Argentina

5.3.1.7 Rest of the World

5.3.2 By Consumption Analysis

5.3.2.1 Asia-Pacific

5.3.2.1.1 China

5.3.2.1.2 India

5.3.2.1.3 Japan

5.3.2.1.4 South Korea

5.3.2.1.5 Thailand

5.3.2.1.6 Malaysia

5.3.2.1.7 Indonesia

5.3.2.1.8 Vietnam

5.3.2.1.9 Rest of Asia-Pacific

5.3.2.2 North America

5.3.2.2.1 United States

5.3.2.2.2 Canada

5.3.2.2.3 Mexico

5.3.2.3 Europe

5.3.2.3.1 Germany

5.3.2.3.2 United Kingdom

5.3.2.3.3 Italy

5.3.2.3.4 France

5.3.2.3.5 Spain

5.3.2.3.6 Turkey

5.3.2.3.7 Russia

5.3.2.3.8 NORDIC

5.3.2.3.9 Rest of Europe

5.3.2.4 South America

5.3.2.4.1 Brazil

5.3.2.4.2 Argentina

5.3.2.4.3 Colombia

5.3.2.4.4 Rest of South America

5.3.2.5 Middle East and Africa

5.3.2.5.1 Saudi Arabia

5.3.2.5.2 South Africa

5.3.2.5.3 Nigeria

5.3.2.5.4 Egypt

5.3.2.5.5 Qatar

5.3.2.5.6 United Arab Emirates

5.3.2.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Abassco

6.4.2 Barium & Chemicals Inc.

6.4.3 Chongqing Yuanhe Fine Chemicals Inc.

6.4.4 Fertiberia

6.4.5 Hebei Xinji Chemical Group Co. Ltd

6.4.6 Joyieng Chemical Limited

6.4.7 KBM Affilips

6.4.8 Nanjing Jinyan Strontium Industry Co. Ltd

6.4.9 Noah Chemicals

6.4.10 ProChem Inc.

6.4.11 SAKAI CHEMICAL INDUSTRY CO. LTD

6.4.12 Shenzhou Jiaxin Chemical Co. Ltd

6.4.13 Shijiazhuang Zhengding JINSHI Chemical Co. Ltd

6.4.14 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Use of Strontium Nitrate in the Chemical, Marine, and Defense Sectors