ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

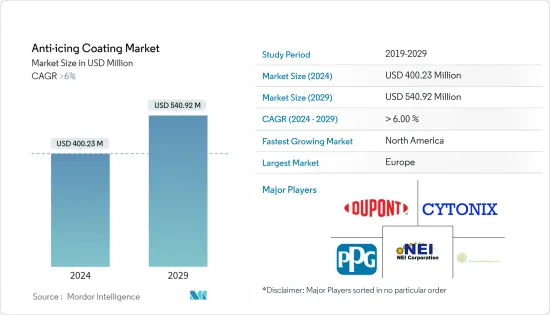

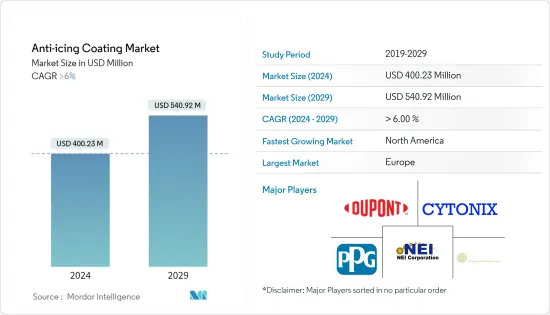

세계의 방빙 코팅 시장 규모는 2024년에 4억 23만 달러에 이르고, 2024-2029년 예측기간 동안 CAGR 6% 이상으로 성장하고, 2029년에는 5억 4,092만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

COVID-19 팬데믹은 세계 폐쇄, 엄격한 사회적 격리 조치, 공급망 혼란으로 인해 시장에 부정적인 영향을 미쳤습니다. 쇄국기간 동안 원재료 가격이 상승한 것도 방빙 코팅제 시장에 악영향을 미치는 원인이 되었습니다.

그러나 규제 해제 후 시장은 순조롭게 회복되었습니다. 자동차, 수송, 건설, IT 및 통신, 신재생에너지산업에서 방빙 코팅제의 소비 증가에 견인되어 시장은 크게 회복되었습니다.

자동차 및 항공우주 분야에서 수요 증가, 한랭지에서 수요 높이, 방빙 코팅의 뛰어난 특성은 방빙 코팅 시장을 견인할 것으로 예상됩니다.

비용 효과적인 대용품이 있다는 것은 시장 성장을 방해할 것으로 예상됩니다.

예측 기간 동안 자기 지속적인 윤활성 동결 방지층의 개척이 시장에 기회를 가져올 것으로 기대됩니다.

유럽이 시장을 독점하고 있는데, 이는 이 지역의 한랭한 기후 조건 하에서 방빙 코팅의 용도가 확대되고 있기 때문에 이는 방빙 코팅 수요를 증가시키고 있습니다.

방빙 코팅 시장 동향

자동차산업과 수송산업이 시장을 독점

방빙 코팅은 에너지 비용과 소비 감소, 기술 제품 성능 향상, 제품 안전성 향상에 기여하며 방빙 코팅 시장을 지원합니다.

자동차 및 운송산업은 한랭한 기후조건하에서 방빙 코팅제가 널리 사용되고 있기 때문에 지배적인 부문이 되고 있습니다. 전기자동차 이니셔티브와 같은 청정에너지 각료회의(CEM) 하에서의 이니셔티브와 전기자동차의 인기 증가는 가까운 미래에 방빙 코팅제의 소비를 촉진할 것으로 보입니다.

세계 자동차 생산량 증가가 방빙 코팅제 시장을 견인할 것으로 예상됩니다. 국제자동차제조자기구(OICA)에 따르면 세계 자동차 생산대수는 2021년 8,021만대에 비해 2022년에는 8,501만대에 이르며 성장률은 6%입니다. 중국, 미국, 인도는 세계에서 가장 눈에 띄는 자동차 시장입니다.

중국은 자동차와 부품의 생산 및 수출로 세계를 선도하고 있습니다. 중국은 계속 세계 최대의 자동차 시장입니다. OICA에 따르면 중국의 자동차 생산 대수는 2022년에 합계 2,702만대에 달하고, 동시기의 전년 대비 3% 증가했습니다.

미국은 중국에 이어 세계 2위 자동차 시장으로 세계 자동차 시장에서 큰 점유율을 차지하고 있습니다. OICA에 따르면 2022년 미국 자동차 생산 대수는 2021년 생산 대수 915만대에 비해 1,006만대에 달하고, 성장률은 9%에 달했습니다. 이로 인해 자동차 산업의 성장이 촉진되어 방빙 코팅 시장 수요가 자극되었습니다.

또한 최근에는 항공기 제조업체가 주문 잔여물을 채우기 위해 생산을 가속화하는 방법을 찾고 있습니다. 예를 들어 Boeing Commercial Outlook 2022-2041에 따르면 신형 항공기의 세계 총 납품 수는 2041년까지 4만 1,170대가 될 것으로 추정됩니다. 따라서 항공기 생산 증가는 현재의 연구 시장을 견인할 것으로 예상됩니다.

따라서, 상기 요인들로부터 자동차 및 운송의 최종 사용자 산업이 방빙 코팅 시장을 견인할 것으로 예상됩니다.

유럽이 시장을 독점

유럽은 방빙 코팅 시장을 독점할 것으로 예상됩니다. 항공우주, 통신, 송전선, 건설, 해양 플랫폼 등 많은 산업에서 응용 분야가 확대되고 있는 것은 방빙 코팅제 수요를 촉진할 것으로 예상됩니다.

독일의 자동차 제조업은 유럽의 자동차 생산 전체에서 선두 주주입니다. 이 나라는 Volkswagen, Mercedes-Benz, Audi, BMW, Porsche 등 주요 자동차 제조 브랜드를 보유하고 있습니다. OICA에 따르면 자동차와 소형 상용차의 총 생산 대수는 2021년 330만대에 비해 2022년 367만대에 달하고, 성장률은 11%입니다. 따라서 이러한 자동차산업의 성장도 방빙 코팅제 수요를 견인하고 있습니다.

마찬가지로 프랑스에서도 자동차 산업은 큰 성장률을 기록했습니다. OICA에 따르면 이 나라의 2022년 자동차 총 생산 대수는 138만대로 전년 대비 2%의 성장을 기록했습니다. 승용차, 소형 상용차, 대형 상용차, 버스, 코치는 차량 비용 상승으로 2022년 판매량이 감소했습니다.

독일은 유럽에서 가장 건설 산업이 활발한 나라입니다. 이 나라의 건설 산업은 신규 주택 건설 활동 증가에 견인되어 완만한 성장을 계속하고 있습니다. 예를 들어 Eurostat에 따르면 2022년 건축 건설 수입은 1,140억 달러로, 2024년에는 1,254억 달러에 이를 것으로 예상됩니다. 따라서 건설 산업의 성장이 현재의 연구 시장을 견인 할 가능성이 높습니다.

유럽에서는 항공 교통량이 증가함에 따라 항공기 수요가 증가하고 있습니다. Boeing Commercial Outlook 2022-2041에 따르면 2041년까지 신형 항공기의 총 납품 수는 8,550대, 시장 서비스 금액은 8,500억 달러에 이를 것으로 추정되며, 이에 따라 이 지역의 방빙 코팅제 수요가 증가하고 있습니다.

방빙 코팅은 기계적 강도에 대한 착빙의 영향으로부터 보호하고 유지 보수 비용을 줄이고 원활한 작동을 보장하기 위해 풍력 터빈의 로터 블레이드에 널리 사용됩니다. 유럽에서는 풍력 발전 용량이 증가하고 있습니다. 2022년 유럽은 19기가와트의 풍력 발전 용량을 새로 설치했습니다. 또한 유럽은 2023-2027년에 걸쳐 129GW의 신규 풍력발전소의 설치를 목표로 하고 있습니다. 따라서 풍력에너지 분야의 성장은 이 지역의 방빙 코팅 시장을 견인할 것으로 예상됩니다.

따라서 이러한 모든 시장 동향은 예측 기간 동안 지역의 방빙 코팅 시장 수요를 촉진할 것으로 예상됩니다.

방빙 코팅 산업 개요

방빙 코팅 시장은 부분적으로 통합되어 있습니다. 이 시장의 주요 기업으로는 NEI Corporation, Cytonix, PPG Industries, Inc., DuPont, NanoSonic, Inc. 등을 들 수 있습니다(순부동).

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

자동차 및 항공우주 분야로부터 수요 증가

한랭지에서의 높은 수요

방빙 코팅의 뛰어난 특성

억제요인

비용 효율적인 대체품의 이용 가능성

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(시장 규모 : 금액 기준)

기판

금속

유리

세라믹

콘크리트

최종 사용자 산업

자동차 및 운송

건설

통신

신재생에너지

기타 최종 사용자 산업

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

합병·인수, 합작 사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

Aerospace & Advanced Composites GmbH

Battelle Memorial Institute

CG2 Nanocoatings

Cytonix

DuPont

Fraunhofer

Helicity Technologies, Inc.

HygraTek

NanoSonic, Inc.

NEI Corporation

Opus Materials Technologies

PPG Industries, Inc.

제7장 시장 기회와 앞으로의 동향

지속 가능한 자기 윤활 방빙 코팅의 개발

기타 기회

JHS

영문 목차

영문목차

The Anti-icing Coating Market size is estimated at USD 400.23 million in 2024, and is expected to reach USD 540.92 million by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

Key Highlights

The COVID-19 pandemic negatively impacted the market due to worldwide lockdowns, strict social distancing measures, and disruptions in supply chains, which had adverse effects on the market for anti-icing coatings. The prices of raw materials increased during the lockdown, further contributing to the negative impact on the anti-icing coatings market.

However, the market recovered well after the restrictions were lifted. It rebounded significantly, driven by increased consumption of anti-icing coatings in the automotive, transportation, construction, telecommunication, and renewable energy industries.

The growing demand from the automotive and aerospace sectors, high demand in cold climatic conditions, and the superior properties of anti-icing coatings are expected to drive the market for anti-icing coatings.

The availability of cost-effective alternate substitutes for anti-icing coatings is expected to hinder market growth.

The development of a self-sustainable lubricating anti-icing layer is expected to create opportunities for the market during the forecast period.

The European region dominates the market, owing to the growing application of anti-icing coatings in cold climatic conditions in the region, which augments the demand for anti-icing coatings.

Anti-Icing Coating Market Trends

Automotive and Transportation Industries to Dominate The Market

Anti-icing coatings help reduce the cost and consumption of energy, enhance the performance of technical goods, and contribute to product safety, which will provide a boost to the anti-icing coating market.

The automotive and transportation industry stands to be the dominant segment owing to the extensive consumption of anti-icing coatings in vehicles under cold climatic conditions. The initiatives under the Clean Energy Ministerial (CEM), like the electric vehicle initiative and the growing popularity of electric vehicles, are likely to drive the consumption of anti-icing coatings in the near future.

The increase in the global production of automotive vehicles is expected to drive the market for anti-icing coatings. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), global automotive vehicle production reached 85.01 million in 2022, compared to 80.21 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

China is the world's leading producer and exporter of automobiles and their parts. China continues to be the world's largest vehicle market. According to OICA, automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

The United States is the second-largest automotive market in the world after China, which occupies a significant share of the global automotive vehicles market. According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. This enhanced the growth of the automobile industry, which has stimulated the market demand for anti-icing coatings.

Furthermore, recently, aircraft manufacturers have been looking for ways to accelerate production to fill order backlogs. For instance, according to the Boeing Commercial Outlook 2022-2041, the total global deliveries of new airplanes are estimated to be 41,170 by 2041. Thus, the increased aircraft production is expected to drive the current studied market.

Hence, owing to the above-mentioned factors, the automotive and transportation end-user industry is expected to drive the market for anti-icing coatings.

Europe Region to Dominate the Market

The European region is expected to dominate the market for anti-icing coatings. The increasing application in many industries, including aerospace, telecommunications, power lines, construction, and offshore platforms, is expected to propel the demand for anti-icing coatings.

The automobile manufacturing industry in Germany is a prominent shareholder of the overall automotive production in the European region. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, Porsche, etc. According to OICA, the total production volume of cars and light commercial vehicles reached 3.67 million units in 2022, compared to 3.30 million units manufactured in 2021, at a growth rate of 11%. Therefore, such growth in the automotive industry has also been driving the demand for anti-icing coatings.

Similarly, in France, the automotive industry registered a significant growth rate. According to OICA, the total production of vehicles in the country amounted to 1.38 million units in 2022, registering a growth of 2% from the previous year. Passenger cars, light commercial vehicles, heavy commercial vehicles, buses, and coaches witnessed a decline in 2022 sales in the country owing to the growing cost of vehicles.

Germany has the most significant construction industry in Europe. The country's construction industry has been growing slowly, driven by increasing new residential construction activities. For instance, according to Eurostat, the building construction revenue is registered at USD 114 billion in 2022 and is expected to reach USD 125.4 billion by 2024. Thus, growth in the construction industry is likely to drive the current studied market.

In Europe, with the increase in air traffic, the demand for aeroplanes is increasing in the country. According to the Boeing Commercial Outlook 2022-2041, the total deliveries of new airplanes are estimated to be 8,550 units by 2041, with a market service value of USD 850 billion, thereby increasing the demand for anti-icing coatings in the region.

Anti-icing coatings are widely used on rotor blades of wind turbines to protect against the effect of icing on mechanical strength, reduce maintenance costs, and ensure smooth operations. Europe is increasing its wind energy generation capacity. In 2022, Europe installed 19 gigawatts of new wind energy capacity. Furthermore, Europe aims to install 129 GW (gigawatts) of new wind farms over the period 2023-2027. Thus, the growth in the wind energy sector is expected to drive the anti-icing coating market in the region.

Hence, all such market trends are expected to drive the demand for the anti-icing coating market in the region during the forecast period.

Anti-Icing Coating Industry Overview

The anti-icing coating market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) NEI Corporation, Cytonix, PPG Industries, Inc., DuPont, and NanoSonic, Inc., amongst others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing demand from Automotive and Aerospace Sector

4.1.2 High Demand in Cold Climatic Conditions

4.1.3 Superior Properties of Anti-icing Coatings

4.2 Restraints

4.2.1 Availability of Cost-Effective Alternate Substitutes

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Substrate

5.1.1 Metal

5.1.2 Glass

5.1.3 Ceramics

5.1.4 Concrete

5.2 End User Industry

5.2.1 Automotive and Transportation

5.2.2 Construction

5.2.3 Telecommunication

5.2.4 Renewable Energy

5.2.5 Other End-User Industries (Marine, Industrial, etc.)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Aerospace & Advanced Composites GmbH

6.4.2 Battelle Memorial Institute

6.4.3 CG2 Nanocoatings

6.4.4 Cytonix

6.4.5 DuPont

6.4.6 Fraunhofer

6.4.7 Helicity Technologies, Inc.

6.4.8 HygraTek

6.4.9 NanoSonic, Inc.

6.4.10 NEI Corporation

6.4.11 Opus Materials Technologies

6.4.12 PPG Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Development of Self Sustainable Lubricating Anti-Icing Layer