ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

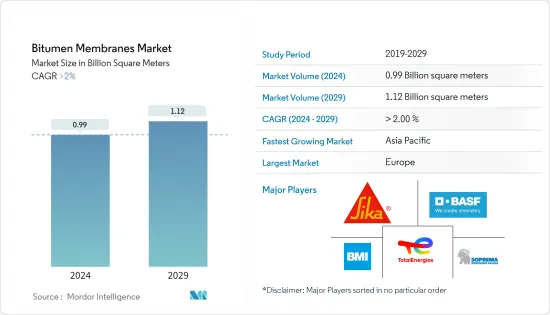

세계 아스팔트 멤브레인 시장 규모는 2024년 9억 9,000만 평방미터로 추정되며, 2029년에는 11억 2,000만 평방미터에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 2% 이상의 CAGR로 성장할 것으로 예상됩니다.

COVID-19는 아스팔트 멤브레인 산업에 큰 영향을 미치고 있습니다. 건설 업계는 각국의 폐쇄, 물류 제약, 공급망 중단, 인력 부족, 부품 공급 제한, 수요 감소, 기업 유동성 감소, 생산 중단으로 인한 생산 중단 등의 문제에 직면하여 부정적인 영향을 경험하고 있습니다. 이에 따라 원자재 공급업체와 관련 기업들은 이 위기 상황에서 업계의 수요에 대응하기 위해 전략을 재검토하고 있습니다. 그러나 이러한 상황은 2021년 초에 회복되어 시장의 성장 궤도를 되찾았습니다.

주요 하이라이트

아시아태평양의 활발한 건설 활동과 방수, 가습, 결속 및 기타 응용 분야 등 다양한 분야에서 멤브레인 응용의 다양성은 시장 수요를 증가시킬 것으로 예상됩니다.

반면, 다양한 용매와 희석제의 존재로 인해 아스팔트 멤브레인과 관련된 잠재적인 건강 및 환경 문제가 시장 성장을 방해하고 있습니다.

그러나 옥상 녹화에 대한 관심이 높아짐에 따라 방수막에 대한 수요가 증가하여 시장에 유리한 기회를 제공할 것으로 예상됩니다.

예측 기간 동안 유럽은 세계 아스팔트 멤브레인 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

아스팔트 멤브레인 시장 동향

건설 업계가 수요를 독식

아스팔트 멤브레인은 건축물의 방수 공사에 널리 사용되어 물의 침투에 대한 보호 장벽을 형성하고 구조물의 손상을 방지하고 긴 수명을 보장하는 데 사용됩니다.

아스팔트 멤브레인은 또한 기초를 물의 침투로부터 보호하고, 특히 지하 구조물의 부식 및 구조물 손상을 방지하는 데 사용됩니다.

아스팔트 멤브레인은 지붕, 테라스, 탱크 라이닝, 기단, 지하 구조물, 지하실 등 다양한 용도로 사용됩니다.

현재 세계 건설 산업은 꾸준히 성장하고 있습니다. 아시아태평양의 건설 산업은 빠른 속도로 성장하고 있으며, 중국, 인도, 동남아시아 국가는 핫스팟으로 부상하고 있습니다.

중국 국가통계국에 따르면, 2022년 중국의 건설 생산액은 31조 2,000억 위안(4조 3,900억 달러)에 달해 전년도 29조 3,100억 위안(4조 1,200억 달러)에 비해 성장세를 기록할 것으로 예상됩니다.

인도 재무부에 따르면, 2023년 인도 전체 건설업의 실질 총부가가치는 9% 이상 증가했지만, 2021년에는 8.6%, 2022년에는 10.7% 감소했습니다.

마찬가지로 미국 인구 조사국에 따르면 미국의 건설업 총 생산액은 2022년 1,660억 달러 이상 증가하여 총 1 조 7,920억 달러에 달할 것으로 예상됩니다. 건설 생산량이 증가함에 따라 건축, 인프라 개발, 개조 및 기타 응용 분야에서 아스팔트 멤브레인에 대한 수요가 증가하여 특수 테이프 시장에 긍정적인 영향을 미칠 가능성이 높습니다.

국립 통계 및 인구조사 연구소에 따르면, 아르헨티나의 건축 허가 면적과 건축 허가 건수는 2022년 1,485만 평방미터와 5만 7,240건에 달해 전년 대비 성장세를 기록했다고 합니다.

마찬가지로 OICA에 따르면 2022년 프랑스에서는 138만 대 이상의 자동차가 생산되었으며, 이 중 승용차가 73.05%를 차지했다고 합니다. 이는 전년도 전체 자동차 생산량에 비해 증가했습니다.

위의 요인들은 예측 기간 동안 이 지역의 아스팔트 멤브레인 소비 수요 증가에 기여하고 있습니다.

유럽이 시장을 독식

유럽은 예측 기간 동안 세계 아스팔트 멤브레인 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

독일은 유럽에서 가장 큰 건설 산업입니다. 독일 연방 통계청(독일 연방 당국)에 따르면 독일의 주택 건설 수입은 2023년 579억 5 천만 유로(625억 달러)에 달했지만 2022년 610억 유로(657억 9 천만 달러)에 비해 수익이 감소했습니다.

또한, 독일의 비주거 및 상업용 건물은 향후 몇 년 동안 큰 성장을 보일 것으로 예상됩니다. 저금리, 실질 가처분 소득 증가, 유럽연합(EU)과 독일 정부의 많은 투자가 성장을 뒷받침하고 있습니다.

영국의 주택 건설은 꾸준히 성장하고 있습니다. 그러나 영국의 비주거 부문은 어려움을 겪고 있으며, 예측 기간 동안 회복될 것으로 예상됩니다.

또한 아스팔트 멤브레인은 자동차 제조 공정에 직접 적용되지는 않지만 아스팔트 기반 제품은 녹 방지, 방음 및 전반적인 운전 경험을 개선하여 자동차의 내구성, 편안함 및 성능을 향상시키는 역할을 합니다.

국제자동차산업연맹(OICA)에 따르면 2022년 이탈리아의 자동차 부문은 약 151만 대의 자동차 판매를 기록했으며, 승용차가 87.45%를 차지했다고 합니다. 이탈리아의 신차 등록은 전년 대비 9.8% 감소했는데, 이는 다양한 자동차 카테고리의 판매 감소에 기인합니다. 그럼에도 불구하고 이탈리아는 2022년에도 유럽 4위의 자동차 시장 지위를 유지했습니다.

따라서 예측 기간 동안 유럽 국가에서는 아스팔트 멤브레인에 대한 수요가 증가할 것으로 예상됩니다.

아스팔트 멤브레인 산업 개요

세계 아스팔트 멤브레인 시장은 부분적으로 세분화되어 있습니다. 조사 대상 시장의 주요 기업으로는 Sika AG, SOPREMA S.A.S., BMI Group, TotalEnergies, BASF SE 등이 있습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

아시아태평양의 건설 활동 성장

멤브레인 용도 다양성

기타 촉진요인

성장 억제요인

잠재적 건강·환경 문제

기타

업계 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(수량 기준 시장 규모)

등급

아택틱 폴리프로필렌

스티렌-부타디엔-스티렌

기타

제품 유형

시트

액체

최종 이용 산업

건설

자동차

기타

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

나이지리아

카타르

이집트

아랍에미리트

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 순위 분석

주요 기업의 전략

기업 개요

ARDEX Group

BASF SE

BMI Group

Bondall

Firestone Building Products Company, LLC

IKO PLC

Isoltema Spa

Sika AG

SOPREMA S.A.S

Tiki Tar Industries India Ltd

TotalEnergies

제7장 시장 기회와 향후 동향

옥상 녹화에 대한 관심 상승이 방수 멤브레인 수요를 지지

ksm

영문 목차

영문목차

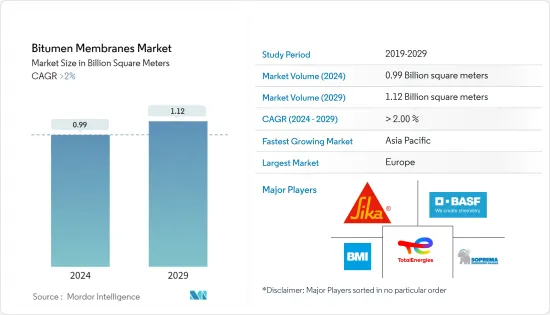

The Bitumen Membranes Market size is estimated at 0.99 Billion square meters in 2024, and is expected to reach 1.12 Billion square meters by 2029, growing at a CAGR of greater than 2% during the forecast period (2024-2029).

COVID-19 has had a significant impact on the bitumen membrane industry. The construction industry has faced challenges such as lockdowns in different countries, logistical constraints, supply chain interruptions, workforce shortages, limited component availability, decreased demand, low company liquidity, and manufacturing shutdowns due to lockdowns, has experienced adverse impacts. In response, raw material suppliers and affiliated businesses are compelled to reassess their strategies to address the industry's needs during this crisis period. However, the condition recovered in early 2021, thereby restoring the market's growth trajectory.

Key Highlights

The growing construction activities in the Asia-Pacific region and the versatility of membrane applications in various areas, such as waterproofing, humidifying, binding, and other applications, are likely to enhance market demand.

On the flip side, the potential health and environmental issues affiliated with bitumen membranes due to the presence of various solvents and diluents are hindering the growth of the market.

Nevertheless, the rising interest in green roofs to boost demand for waterproofing membranes is expected to offer lucrative opportunities to the market.

The European region is expected to account for the largest share of the global bitumen membranes market over the forecast period.

Bitumen Membranes Market Trends

Construction Industry to Dominate the Demand

Bitumen membranes are extensively used for waterproofing in construction and are used to create a protective barrier against water penetration, preventing damage to structures and ensuring longevity.

They are also used to safeguard foundations against water infiltration, and bitumen membranes prevent corrosion and structural damage, particularly in below-ground structures.

Bitumen membranes are used for various applications, which include roofing, terraces, tank lining, podiums, below-grade structures, and basements, among others.

Currently, the global construction industry has been growing steadily. The construction industry in the Asia-Pacific region is growing at a significant pace, with China, India, and Southeast Asian countries being in the hotspot.

According to the National Bureau of Statistics of China, the construction output value in China has reached CNY 31.2 trillion (USD 4.39 trillion) in 2022 and registered growth when compared to CNY 29.31 trillion (USD 4.12 trillion) in the previous year.

As per the Ministry of Finance (India), in FY2023, the real gross value added in the construction industry across India increased by more than 9%, whereas during FY 2021 and FY2022, it was -8.6% and 10.7%, respectively.

Simialry, according to the US Census Bureau, the total value of construction output in the United States increased by more than USD 166 billion in 2022, reaching a total of USD 1,792 billion. As construction output expands, the need for bitumen membranes in applications like building, infrastructure development, and renovation is likely to increase, positively influencing the specialty tape market.

According to the National Institute of Statistics and Censuses, the surface area of buildings authorized for construction and number of building permits in Argentina has reached 14.85 million square meters and 57.24 thousands in 2022 and registred growth when compared to the previous years data.

Similarly, according to OICA, France witnessed the production of more than 1.38 million motor vehicles in 2022, with passenger cars constituting 73.05 percent of this total. This marked an increase in growth compared to the overall vehicle production in the preceding year.

The factors above contribute to the increasing demand for bitumen membranes consumption in the region during the forecast period.

Europe Region to Dominate the Market

The European region is expected to account for the largest share in the global bitumen membranes market over the forecast period.

Germany has the largest construction industry in Europe. According to the Federal Statistical Office (a federal authority of Germany), revenue in housing construction in Germany has reached EUR 57.95 billion (USD 62.50 billion) in 2023, however registred less revunes when comapred with EUR 61 billion ((USD 65.79 billion)) in 2022.

Additionally, the non-residential and commercial buildings in the country are expected to witness significant growth prospects in the coming years. Lower interest rates, an increase in real disposable incomes, and numerous investments by the European Union and the German governments support the growth.

Residential construction in the United Kingdom is witnessing steady growth. However, the non-residential sector in the country is struggling and is expected to recover during the forecast period.

Furthur, while bitumen membranes are not directly applied in the automotive manufacturing process, bitumen-based products play a role in enhancing the durability, comfort, and performance of vehicles by providing protection against rust, dampening noise, and improving overall driving experience.

According to The International Organization of Motor Vehicle Manufacturers (OICA), in 2022, Italy's automotive sector recorded the sale of approximately 1.51 million motor vehicles, with passenger cars constituting 87.45 percent of this total. The overall new vehicle registrations in the country witnessed a 9.8 percent year-over-year decline, attributed to reduced sales in various vehicle categories. Nevertheless, Italy retained its position as the fourth-largest vehicle market in Europe for the year 2022.

Therefore, the demand for bitumen membranes is expected to grow in European countries during the forecast period.

Bitumen Membranes Industry Overview

The global bitumen membranes market is partially fragmented. The major companies of the market studied include (not in any particular order) Sika AG, SOPREMA S.A.S. , BMI Group, TotalEnergies, and BASF SE, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Construction Activities in Asia-Pacific Region

4.1.2 Versatility of Membrane Applications

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Potential Health and Environmental Issues

4.2.2 Others

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (market size in volume)

5.1 Grade

5.1.1 Atactic Polypropylene

5.1.2 Styrene-Butadiene-Styrene

5.1.3 Others

5.2 Product Type

5.2.1 Sheets

5.2.2 Liquids

5.3 End-user Industry

5.3.1 Construction

5.3.2 Automotive

5.3.3 Others

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 Nordic

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle-East & Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 United Arab Emirates

5.4.5.7 Rest of Middle-East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis**

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 ARDEX Group

6.4.2 BASF SE

6.4.3 BMI Group

6.4.4 Bondall

6.4.5 Firestone Building Products Company, LLC

6.4.6 IKO PLC

6.4.7 Isoltema Spa

6.4.8 Sika AG

6.4.9 SOPREMA S.A.S

6.4.10 Tiki Tar Industries India Ltd

6.4.11 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Interest in Green Roofs to Boost Demand for Waterproofing Membranes