세계 군용 프리깃함 시장 - 점유율 분석, 산업 동향과 통계, 성장 예측(2024-2029년)

Military Frigates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1536931

리서치사:Mordor Intelligence

발행일:2024년 08월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

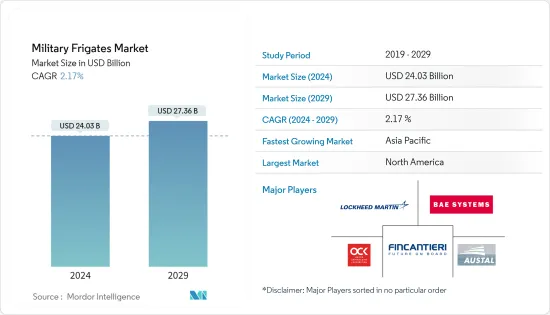

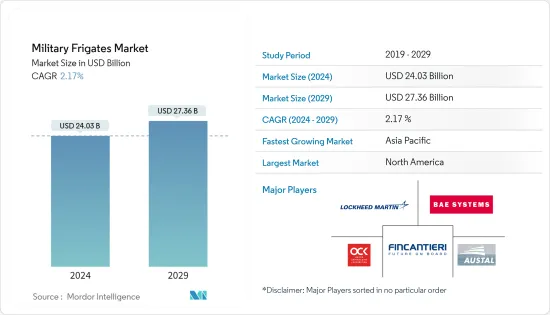

군용 프리깃함 시장 규모는 2024년 240억 3,000만 달러로 추정되며, 2029년 273억 6,000만 달러에 이를 것으로 예측되며, 예측기간(2024-2029년)의 CAGR은 2.17%로 성장할 전망 .

주요 하이라이트

해상 국경 문제와 영토 분쟁 증가로 신형 프리깃함의 개발·조달은 최근 몇 년간 중요성을 늘리고 있습니다. 세계의 지정학적 긴장 증가는 해군력의 전략적 중요성을 부각시키고, 군용 프리깃함에 대한 수요 증가를 조장하고 있습니다. 각국은 중요한 항로를 확보하고, 영해를 지키고, 진화하는 지정학적 과제에 효과적으로 대응하기 위해, 해양 능력을 강화하려고 하고, 그것이 프리깃함의 조달을 뒷받침하고 있습니다.

해양 안보의 중시가 높아짐에 따라 군용 프리깃함 수요가 증폭되고 있습니다. 이 함선은 순찰 활동의 핵심 역할을 하며 각국이 자국의 해안선, 배타적 경제 수역(EEZ), 해상 국경을 감시·보호할 수 있게 합니다. 다양한 해양 안보 우려에 대응하는 프리깃함의 다용도성은 안전한 해양 환경 유지에 있어서 매우 중요한 역할을 강화하고 있습니다. 노후화된 현재의 전투함선군을 대함, 대잠, 방공 능력을 갖춘 프리깃함에 장비된 현대적인 탐지·무기 시스템으로 대체하기 위해 다양한 국가에서 진행중인 업데이트가 시장 성장 을 밀고 있습니다.

군사 현대화 이니셔티브의 급증은 군용 프리깃함 시장을 견인하는 매우 중요한 역할을 합니다. 각국이 방위력 업그레이드를 선호하는 동안 프리깃함은 종합적인 해군 근대화 프로그램의 필수 구성 요소로 부상하고 있습니다. 최첨단 프리깃함의 도입은 보다 광범위한 군사 전략에 부합하며 시장의 지속적인 수요에 기여하고 있습니다.

군용 프리깃함 시장 동향

초계 프리깃함이 군용 프리깃함 시장에서 가장 큰 시장 점유율을 차지할 전망

프리깃함은 순찰 임무가 뛰어나 해상 국경의 감시와 안전 확보, 해적 대처 작전의 실시, 해상법 집행을 위한 다목적 플랫폼을 제공합니다. 다양한 작전 시나리오에 적응할 수 있는 프리깃함은 종합적인 해상 안보 솔루션을 요구하는 국가들에게 필수적인 존재가 되고 있습니다. 첨단 센서와 감시 시스템을 갖춘 프리깃는 뛰어난 감시 능력으로 두드러집니다. 이 기능을 통해 광대한 해역을 효과적으로 모니터링할 수 있어 잠재적인 위협을 조기에 발견하고 적극적이고 전략적인 순찰에 기여할 수 있습니다.

초계 카테고리는 해상 테러 대책에서 가장 중요한 위치를 차지합니다. Frigate는 신속한 대응 능력을 통해 잠재적인 해양 위협을 막고 무력화하는 데 중요한 역할을하며 해양 환경에서 테러/해적 활동으로부터 자신을 보호하는 데 필수적인 자산이되었습니다. 예를 들어 중화민국 해군은 2023년 5월 대만 해군에 12척의 프리깃함을 도입하는 길을 열기 위해 Jong Shyn Shipbuilding Group에 2척의 차세대 국산 경프리깃함을 주문했습니다. 2,500톤의 신형 경프리깃은 '2급함'으로 분류돼 대만 해군의 주력함으로 매일 초계 임무를 담당합니다.

아시아태평양이 예측 기간 동안 가장 높은 성장을 이룰 전망

예측 기간 동안 아시아태평양이 가장 높은 성장을 이룰 것으로 예상됩니다. 이 지역의 국가 간 긴장 증가는 각국이 군사비를 증가시키는 요인입니다. 그러므로 예측 기간 동안 시장 성장을 가속하고 있습니다. 한국, 호주, 인도, 중국, 인도네시아 등의 국가들은 이 지역에서 새로운 프리깃 함의 개발, 건조, 조달에 투자하고 있습니다.

아시아태평양 시장 점유율이 큰 것은 이 지역의 지정학적 중요성에 기인합니다. 남중국해 및 기타 중요한 수로에서의 영향력을 둘러싼 경쟁이 격화되는 가운데 아시아태평양 국가들은 해상 우위를 주장하고 중요한 권익을 지키기 위해 전략적으로 선진적인 프리깃함에 투자 하고 있습니다.

또한 중국, 인도, 일본 등 주요 국가의 적극적인 해군 근대화 노력은 아시아태평양에서의 군용 프리깃함 수요 급증에 크게 기여하고 있습니다. 이들 국가들은 강력한 해군 존재를 유지할 필요성을 인식하고 있으며 종합적인 방어 전략의 일환으로 최신 프리깃 함대에 대한 투자에 박차를 가하고 있습니다. 게다가 Austal, China State Shipbuilding Corporation, Hyundai Heavy Industries(HHI)과 같은 조선회사의 존재도 이 지역에서 프리깃함의 성장을 지지하고 있습니다. 예를 들어, 2021년 10월, 러시아는 인도 해군을 위해 국내에서 건설중인 2척의 크리박급 또는 탈와르급 스텔스 프리깃 '투실'의 첫 1척을 발사했습니다. 이 프리깃함은 인도가 러시아와 계약한 4척의 후속 프리깃함의 일부이며, 그 중 2척은 러시아가 건조중이며, 2척은 기술이전에 의해 인도에서 건조중입니다.

마찬가지로 2023년 10월 인도 국방부는 M/S Cochin Shipyard Limited(CSL)와 'INS Beas'의 라이프 업그레이드 및 리파워링 계약을 총 비용 3,760만 달러로 체결했습니다. INS Beas는 블러프 마푸트라급 프리깃로 증기 추진에서 디젤 추진으로 변경됩니다. INS Beas는 현대화된 무기 세트와 업그레이드된 전투 능력을 갖추고 2026년 인도 해군의 현역 함대에 합류할 예정입니다.

군용 프리깃함 산업 개요

군용 프리깃 함 시장은 세분화되어 많은 기업들이 시장 점유율을 얻기 위해 경쟁하고 있습니다. 시장에서 유명한 기업으로는 Lockheed Martin Corporation, Austal Limited, United Shipbuilding Corporation, Fincantieri S.p.A., BAE Systems plc. 등이 있습니다. 각 회사가 직면하는 주요 문제는 지리적 존재가 제한되어 있다는 것입니다. 예를 들어, BAE Systems plc는 영국과 호주 프리깃함 프로그램을 지원하고, Austal Limited는 호주와 미국 프리깃함을 지원하며, United Shipbuilding Corporation은 주로 러시아 프로그램을 지원합니다. 이러한 지리적 존재가 제한되어 시장은 매우 단편화되어 많은 기업들이 점유율의 일부를 차지하고 있습니다. 해군 프리깃함 개발 프로그램을 지원하기 위해 기업 간의 협력과 파트너십은 기업이 시장에서 강력하고 주도적인 지위를 얻는 데 도움이 될 수 있습니다.

예를 들어, 미국 해군은 2021년 5월 Constellation 클래스의 차기 프리깃함의 건조를 시작하기 위해 Fincantieri Marinette Marine에 5억 5,400만 달러의 계약을 발행했습니다. 이 계약은 Constellation 클래스의 두 번째 선체 인 USS Congress(FFG-63)에 대한 것입니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

시장 성장 억제요인

Porter's Five Forces 분석

구매자/소비자의 협상력

공급기업의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

용도별

순찰

호위

기타 용도

지역별

북미

미국

캐나다

유럽

이탈리아

영국

스페인

프랑스

독일

러시아

기타 유럽

아시아태평양

중국

대만

인도

한국

호주

기타 아시아태평양

라틴아메리카

멕시코

브라질

기타 라틴아메리카

중동 및 아프리카

터키

이집트

사우디아라비아

기타 중동 및 아프리카

제6장 경쟁 구도

벤더의 시장 점유율

기업 프로파일

BAE Systems plc

Fincantieri SpA

Naval Group

Damen Shipyards Group

Fr. Lurssen Werft GmbH & Co. KG

thyssenkrupp AG

United Shipbuilding Corporation

Rosoboronexport

General Dynamics Corporation

Lockheed Martin Corporation

Austal Limited

China Shipbuilding Industry Trading Co., Ltd.

제7장 시장 기회와 앞으로의 동향

JHS

영문 목차

영문목차

The Military Frigates Market size is estimated at USD 24.03 billion in 2024, and is expected to reach USD 27.36 billion by 2029, growing at a CAGR of 2.17% during the forecast period (2024-2029).

Key Highlights

Development and procurement of new frigates have gained importance in the past few years due to the increasing border issues and territorial conflicts at sea. Escalating geopolitical tensions globally underscores the strategic importance of naval forces, fostering a heightened demand for military frigates. Nations seek to bolster their maritime capabilities to secure vital sea routes, protect territorial waters, and respond effectively to evolving geopolitical challenges, thereby driving the procurement of frigates.

The increasing emphasis on maritime security amplifies the demand for military frigates. These vessels serve as linchpins in patrolling activities, enabling nations to monitor and safeguard their coastlines, Exclusive Economic Zones (EEZs), and maritime borders. The versatility of frigates in addressing diverse maritime security concerns reinforces their pivotal role in maintaining a secure maritime environment. The ongoing replacement programs in various countries to replace the current aging fleet of combat ships with modern detection and weapon systems equipped with frigates that have anti-ship, anti-submarine, and air-defense capabilities are propelling the growth of the market.

The surge in military modernization initiatives plays a pivotal role in driving the market for military frigates. As nations prioritize upgrading their defense capabilities, frigates emerge as integral components of comprehensive naval modernization programs. The incorporation of state-of-the-art frigates aligns with broader military strategies, contributing to sustained demand in the market.

Military Frigates Market Trends

Patrol Frigates are Expected to Have the Largest Market Share of the Military Frigates Market

Frigates excel in patrol duties, providing a versatile platform for monitoring and securing maritime borders, conducting anti-piracy operations, and enforcing maritime laws. Their adaptability in diverse operational scenarios makes them indispensable for nations seeking comprehensive maritime security solutions. Frigates, equipped with advanced sensors and surveillance systems, stand out for their superior surveillance capabilities. This feature enables effective monitoring of vast oceanic areas, allowing for early detection of potential threats and contributing to proactive and strategic patrolling.

The patrol category holds paramount importance in counter-terrorism efforts at sea. Frigates, with their swift response capabilities, play a critical role in intercepting and neutralizing potential maritime threats, making them integral assets in safeguarding against terrorist/pirate activities in maritime environments. For instance, in May 2023, the Republic of China (ROC) Navy gave a contract to Jong Shyn Shipbuilding Group for two next-generation domestic Light Frigates paving the road to introduce 12 frigates for the Taiwanese Navy. The new 2,500-ton Light Frigates are classified as "Second class ships" and will act as the workhorses of the Taiwanese Navy, taking over the day-to-day patrol missions.

Asia-Pacific Expected to Witness Highest Growth During the Forecast Period

The Asia-Pacific region is anticipated to have the highest growth during the forecast period. The escalated tensions between the countries in this region have led to countries increasing their military spending. Thus, this is boosting the growth of the market during the forecast period. Countries like South Korea, Australia, India, China, and Indonesia are investing in the development, building, and procurement of new frigates in this region.

Asia-Pacific's substantial market share can be attributed to the geopolitical significance of the region. With increasing competition for influence in the South China Sea and other critical waterways, nations in the Asia-Pacific are strategically investing in advanced frigates to assert maritime dominance and protect vital interests.

Moreover, the proactive naval modernization efforts of key countries like China, India, and Japan significantly contribute to the burgeoning demand for military frigates in Asia Pacific. These nations recognize the imperative of maintaining a robust naval presence, spurring investments in modern frigate fleets as part of comprehensive defense strategies. Additionally, the presence of shipbuilding companies, like Austal, China State Shipbuilding Corporation, and Hyundai Heavy Industries (HHI), is also supporting the growth of frigates in this region. For instance, in October 2021, Russia launched the first of two Krivak or Talwar-class stealth frigates, Tushil, being built in the country for the Indian Navy. The frigate is part of four follow-on frigates contracted by India from Russia, of which Russia is building two, and two are under construction in India through the transfer of technology.

Similarly, in October 2023, the Indian Ministry of Defense signed a contract for the life Upgrade and Re-Powering of "INS Beas" with M/S Cochin Shipyard Limited (CSL) at an overall cost of USD 37.60 million. INS Beas is a Brahmaputra Class Frigate to be re-powered from Steam to Diesel Propulsion. INS Beas will join the active fleet of the Indian Navy with a modernized weapon suite and upgraded combat capability in 2026.

Military Frigates Industry Overview

The military frigates market is fragmented, with many companies competing to gain market share. Some of the prominent players in the market are Lockheed Martin Corporation, Austal Limited, United Shipbuilding Corporation, Fincantieri S.p.A., and BAE Systems plc. The major issue faced by the companies is limited geographical presence. For instance, BAE Systems plc supports the frigate programs of the United Kingdom and Australia, Austal Limited supports frigates in Australia and the United States, and United Shipbuilding Corporation majorly supports the programs of Russia. Due to such a limited geographical presence, the market is highly fragmented, with many companies taking a part of the share. The collaborations and partnerships between the players to support the frigate development programs of the naval forces may help the companies gain a strong and leading position in the market.

For instance, in May 2021, the US Navy issued a USD 554 million contract to Fincantieri Marinette Marine to start building the next frigate in the Constellation class. The award is for the future USS Congress (FFG-63), which is the second hull in the Constellation class.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Buyers/Consumers

4.4.2 Bargaining Power of Suppliers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Application

5.1.1 Patrol

5.1.2 Escort

5.1.3 Other Applications

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.2 Europe

5.2.2.1 Italy

5.2.2.2 United Kingdom

5.2.2.3 Spain

5.2.2.4 France

5.2.2.5 Germany

5.2.2.6 Russia

5.2.2.7 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 Taiwan

5.2.3.3 India

5.2.3.4 South Korea

5.2.3.5 Australia

5.2.3.6 Rest of Asia-Pacific

5.2.4 Latin America

5.2.4.1 Mexico

5.2.4.2 Brazil

5.2.4.3 Rest of Latin America

5.2.5 Middle-East and Africa

5.2.5.1 Turkey

5.2.5.2 Egypt

5.2.5.3 Saudi Arabia

5.2.5.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 BAE Systems plc

6.2.2 Fincantieri S.p.A.

6.2.3 Naval Group

6.2.4 Damen Shipyards Group

6.2.5 Fr. Lurssen Werft GmbH & Co. KG

6.2.6 thyssenkrupp AG

6.2.7 United Shipbuilding Corporation

6.2.8 Rosoboronexport

6.2.9 General Dynamics Corporation

6.2.10 Lockheed Martin Corporation

6.2.11 Austal Limited

6.2.12 China Shipbuilding Industry Trading Co., Ltd.