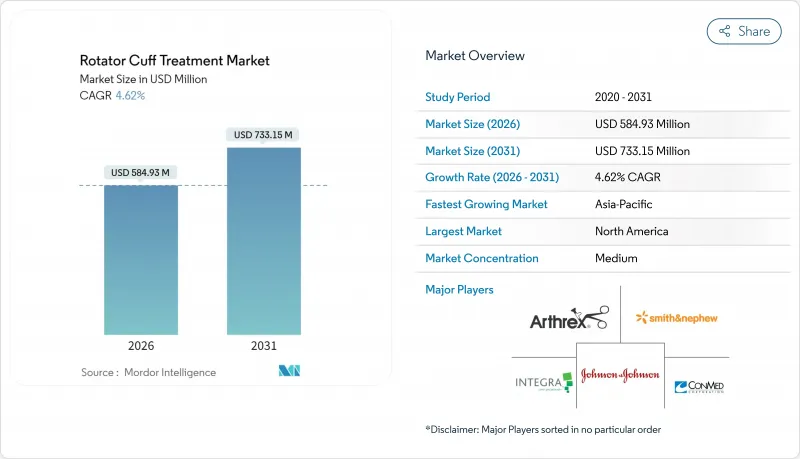

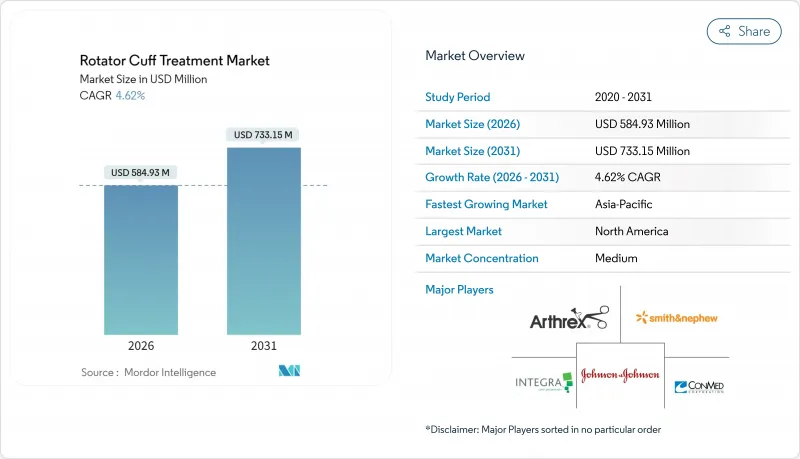

회전근개 치료 시장은 2025년 5억 5,911만 달러로 평가되었고 2026년 5억 8,493만 달러로 성장해 2026-2031년에 걸쳐 CAGR 4.62%로 성장하고, 2031년까지 7억 3,315만 달러에 달할 것으로 예측되고 있습니다.

급속한 고령화에 의한 인구동태적 압력, 두상동작을 수반하는 스포츠에의 참가 증가, 관절경 장치 및 생체 임플란트 포괄 결제 모델에 있어서의 꾸준한 진보가 더해져, 수술 건수와 제품 수요를 끌어 올리고 있습니다. 외과 수술센터(ASC)와 전문 정형외과 클리닉은 병원이 수술 건수의 기반이 되고 있는 반면, 지불 기관이 저비용 시설을 평가하는 경향에서 점유율을 획득하고 있습니다. 로봇 플랫폼, AI 탑재 이미징, 생체 유도성 재료의 조기 도입에 의해 프리미엄 가격 설정이 가능하게 되는 한편, 단열 사이즈에 따라 종래 20-70%의 범위에서 추이해 온 실패율에의 대응도 진행되고 있습니다. 하드웨어, 생물제제, 디지털 툴을 단일 워크플로우에 통합할 수 있는 기업은 재활 기간의 단축과 재수술의 억제를 요구하는 외과의사나 지불자에서의 수요에 부응함으로써 방어 가능한 우위성을 획득하고 있습니다.

두상 운동을 동반한 스포츠 참여는 특히 사춘기 및 주말 선수층에서 훈련 부하가 생리적 한계를 초과하는 경우가 많아 힘줄 손상의 발생률을 꾸준히 증가시키고 있습니다. 수영에서는 5년간 8만 2,000건 이상의 상지 손상이 보고되어 그 대부분이 10-19세의 연령층에서 발생하고 있습니다. 미식축구와 같은 콘택트 스포츠에서는 타박상에서 대규모 단열에 이르는 손상 패턴이 보이고, 보존적 치료가 실패할 경우 수시로 외과적 개입으로 진전합니다. 결과적인 사례 수는 수술 및 비 수술 치료에 대한 수요를 모두 촉진하고 있으며 스포츠 의료 센터는 가장 급성장하는 최종 사용자 채널로 자리 잡고 있습니다. 경기 시즌이 장기화되고 레크리에이션 리그가 증가함에 따라 의료 시스템은 조기 진단, 이미징 및 재활 채널에 더 많은 자원을 할당하고 있으며, 이는 힘줄 손상 치료 시장의 확대로 이어지고 있습니다.

60세 이상의 분들의 절반 이상이, 정도의 차이는 있지만 회전 근개 퇴행을 나타내고 있으며, 자연 발생하는 무증상의 단열이 증상을 수반하는 질환으로 진행하는 것으로, 수술 수요를 견인하고 있습니다. 미국의 연간 어깨 관절 치환술 건수는 2025년까지 25만 건에 달할 것으로 예측되고 있으며, 고령층에서의 건판 단열성 관절증의 경제적 부담의 크기를 부각하고 있습니다. 장기 연구는 역견관절치환술의 10년 재치환율 프리 생존율은 88%인 것으로 나타났으며, 임플란트의 내구성에 대한 외과의사의 신뢰를 높여 유럽과 아시아 전역에서의 보급을 촉진하고 있습니다. 평균 수명 연장과 노인들의 활성 라이프 스타일 지향이 결합되어 수술 건수를 유지하고 힘줄 손상 치료 시장의 디바이스, 생물 제제, 재활 각 부문에서 안정적인 수익 기반을 지원합니다.

관절경하 수술의 평균 치료 비용은 4,094달러이며, 앵커 선택과 수술 시간이 주요 비용 요인입니다. 생체유도성 장치는 고가격대의 정가 설정으로 인해 보험 상환이 지연된 신흥 시장에서는 접근이 제한됩니다. 미국의 보험사는 풍선 스페이서를 실증되지 않고 의료적으로 필요하지 않다고 표시하여 신기술에 따른 상환 위험을 여실히 보여주고 있습니다. 일본의 규제 환경은 입증된 임플란트를 선호하기 때문에 신제품 출시 일정을 더욱 복잡하게 하고 있습니다. 이러한 비용면과 규제면의 압력은 특히 의료 예산이 박박하고 있는 지역에서 성장을 억제하는 요인이 되고 있습니다.

2025년 시점의 회전근개 치료 시장 규모에서 외과적 치료법이 68.94%를 차지합니다. 이것은 관절경 기술의 세련화와 임플란트의 내구성 향상에 뒷받침됩니다. 생체유도 패치, 2열 고정술, 역견관절 치환술은 적응 범위를 확대하고 재단열 위험을 감소시킵니다. 로봇 지원 수술은 습득 기간을 단축하고 지역 의료 현장으로의 보급을 촉진합니다. 한편, 물리치료와 완화 케어는 5.98%의 연평균 복합 성장률(CAGR)을 나타내고 금액 기준 대체요법을 요구하는 지불자층 사이에서 지지를 확대하고 있습니다. 무작위화 연구에 따르면 특정 광범위한 단열 사례에서 구조화된 운동 요법과 항염증 주사를 병용함으로써 최대 96%의 증상 완화가 확인되었습니다. 수술연기와 통증 억제를 목적으로 하는 코르티코스테로이드나 히알루론산을 주성분으로 하는 약제요법이 배합되는 한편, 오르소바이오로직스(뼈 및 관절 재생 의료)는 혁신의 최전선에 위치해, 근거가 성숙함에 따라 투자를 모으고 있습니다.

보존적 치료의 급속한 보급은 발표 패턴을 바꾸고 수술까지의 기간을 연장하지만 근치적 수술에 대한 장기 수요를 감소시키지 않습니다. 운동 요법이나 주사 요법이 효과를 나타내지 않는 경우, 환자는 관절경 수술이나 인공 관절 치환술로 진행되는 경우가 많아, 거기에서는 보다 고도로 고가의 기술이 이용됩니다. 따라서 적극적인 조기 재활과 후기 단계의 수술 혁신의 상호 작용은 힘줄 손상 치료 시장을 먹지 않고 종합적으로 확대하는 요인이됩니다.

북미는 2025년 견회전근개 치료 시장 규모의 39.82%를 차지했고 연간 50만 건을 넘는 수복 수술 건수와 명확한 메디케어 상환 가이드라인에 뒷받침되고 있습니다. 외래수술센터(ASC)의 견고한 성장은 치료 결과를 손상시키지 않고 비용 효과를 평가하는 종합적인 결제 실험 때문입니다. 확립된 공급 파트너십을 통해 생체유도 임플란트 및 로봇 시스템의 신속한 도입이 가능해져 AI 구동의 이미징 프로토콜이 진단 사이클을 단축하고 있습니다. 캐나다의 국민 모두 보험 제도는 광범위한 액세스를 확보하고 있습니다만, 대기 시간의 압박이 민간 시장의 활성화를 촉진해, 의료 관광을 인접하는 미국주로 유도. 이에 따라 회선근 회전근개 치료 시장에서 지역의 우위성이 강화되고 있습니다.

아시아태평양은 CAGR 6.28%에서 가장 빠르게 성장하는 지역입니다. 일본의 400억 달러 규모의 의료기기 시장은 실적 있는 기술을 중시하는 한편, 국내 제조업체가 세계의 대기업과 제휴해 생산의 현지화를 진행하는 가운데, 차세대 임플란트에 대한 관심이 높아지고 있습니다. 중국에서는 공적 보험제도의 개혁에 의해 정형외과의 보험 적용 범위가 확대되고, 주요 병원에서는 고도의 관절경 수술실이 도입되고 있습니다. 인도에서는 크리켓과 배드민턴을 중심으로 한 스포츠 인구의 급증으로 구미와 비슷한 부상자 수가 증가하는 경향이 있습니다. 외과의 부족이나 규제의 불통일은 여전히 과제이지만, 휄로우십 교류나 규제 조화의 대처에 의해 장벽이 서서히 완화되어, 인구가 많은 경제권에 있어서 힘줄 손상 치료 시장 규모 확대가 가능해지고 있습니다.

유럽에서는 고령화와 높은 증거 기준이 명확한 임상 데이터를 가진 제품을 우대하고 꾸준히 낮은 성장을 유지하고 있습니다. 독일과 영국은 생체 임플란트나 로봇 플랫폼의 도입을 주도하는 한편, 지중해 연안 시장에서는 우선 비용 효율적인 물리치료를 우선하고 보존적 치료가 불충분한 경우에만 수술로 이행하는 경향이 있습니다. 브렉지트에 의해 규제의 차이가 발생했지만, 상호 승인 협정에 의해 의료기기의 유통은 유지되고 있습니다. 유럽연합의 의료기기규칙(MDR)은 시판 후 조사의 요건을 강화하고, 각 회사는 임상 증거 창출에 많은 투자를 하고 있습니다. 이러한 요인들이 함께, 유럽 전역에서 균형을 유지하면서도 증거 주도형 힘줄 손상 치료 시장이 형성되고 있습니다.

The rotator cuff treatment market is expected to grow from USD 559.11 million in 2025 to USD 584.93 million in 2026 and is forecast to reach USD 733.15 million by 2031 at 4.62% CAGR over 2026-2031.

Demographic pressures from a rapidly aging population, heavier participation in overhead sports, and steady advances in arthroscopic devices, biologic implants, and bundled-payment care models collectively lift procedure volumes and product demand. Hospitals continue to anchor procedure throughput, yet ambulatory surgical centers (ASCs) and specialty orthopedic clinics capture share as payers reward lower-cost sites. Early-stage adoption of robotic platforms, AI-enabled imaging, and bioinductive materials allows premium pricing while addressing failure rates that have historically ranged between 20% and 70%, depending on tear size. Companies that can combine hardware, biologics, and digital tools into a single workflow gain a defensible edge as surgeons and payers look for solutions that shorten rehabilitation times and curb revision procedures.

Athletic participation in overhead sports steadily increases rotator cuff injury incidence, especially among adolescents and weekend warriors whose training loads often exceed physiological limits. Swimming contributed more than 82,000 upper-extremity injuries over five years, with most events occurring in the 10-19 age group. Contact sports such as American football show injury patterns ranging from contusions to massive tears that frequently progress to surgical intervention when conservative care fails. The resulting case load fuels both surgical and non-surgical demand, with sports medicine centers positioned as the fastest-growing end-user channel. As competitive seasons lengthen and recreational leagues proliferate, healthcare systems allocate more resources to early diagnosis, imaging, and rehabilitation pathways that widen the rotator cuff treatment market.

More than half of people aged 60 years or older show some degree of rotator cuff degeneration, converting naturally occurring asymptomatic tears into symptomatic disease that drives procedure demand. Annual shoulder arthroplasty volumes in the United States alone are projected to reach 250,000 by 2025, underlining the economic burden of cuff tear arthropathy in senior cohorts. Long-term studies show 88% revision-free survivorship for reverse shoulder arthroplasty at 10 years, reinforcing surgeon confidence in implant longevity and sparking wider adoption across Europe and Asia. Rising life expectancy, combined with a preference for active lifestyles among seniors, sustains procedure volumes and underpins a stable revenue base across device, biologic, and rehabilitation segments of the rotator cuff treatment market.

Average episode cost for arthroscopic repair is USD 4,094, with anchor choice and procedure duration the main cost drivers. Bioinductive devices carry premium list prices, limiting access in emerging markets where insurance reimbursements lag. U.S. insurers label balloon spacers "unproven and not medically necessary", illustrating the reimbursement risk attached to newer technologies. Japan's regulatory environment, favoring proven implants, further complicates launch timelines for novel products. These cost and regulatory pressures temper growth, especially where healthcare budgets remain tight.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Surgical modalities account for 68.94% of rotator cuff treatment market size in 2025, supported by refined arthroscopic techniques and improved implant survivorship. Bioinductive patches, double-row fixation, and reverse shoulder arthroplasty extend indications and reduce re-tear concerns. Robotic applications shorten learning curves, facilitating wider diffusion into community settings. Yet physiotherapy and palliative care post 5.98% CAGR and gain traction among payers seeking value-based alternatives. Randomized studies show up to 96% symptom relief in select massive tears when structured exercise is coupled with anti-inflammatory injections. Pharmaceutical interventions featuring corticosteroids or hyaluronic acid are prescribed to delay surgery and curb pain, while orthobiologics sit at the innovation frontier, attracting investment as evidence matures.

Fast uptake of conservative regimens changes referral patterns and elongates time to surgery, but it does not diminish long-term demand for definitive procedures. When exercise or injections fail, patients often progress to arthroscopy or arthroplasty where the technology stack becomes more sophisticated and expensive. Thus, the interplay between aggressive early rehabilitation and late-stage surgical innovation collectively enlarges the rotator cuff treatment market rather than cannibalizing it.

The Rotator Cuff Treatment Market Report is Segmented by Treatment Type (Surgical/Curative Treatment, Physiotherapy/Palliative Treatment, Pharmaceutical/Preventive Treatment, Orthobiologics), Injury Severity (Full-Thickness Tear, Partial-Thickness Tear), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America holds 39.82% of rotator cuff treatment market size in 2025, sustained by procedure volumes exceeding 500,000 annual repairs and clear Medicare guidelines for reimbursement. Robust ASC growth stems from bundled-payment experiments that reward cost-efficiency without sacrificing outcomes. Established supply partnerships allow rapid uptake of bioinductive implants and robotic systems, while AI-driven imaging protocols shorten diagnostic cycles. Canada's universal coverage keeps access wide but wait-time pressures spur a private market that pulls medical tourism into adjacent U.S. states, reinforcing regional dominance of the rotator cuff treatment market.

Asia-Pacific is the fastest-growing territory at 6.28% CAGR. Japan's USD 40 billion medical device sector favors proven technology yet shows rising interest in next-gen implants as domestic manufacturers collaborate with global giants to localize production. China's reform of public insurance widens orthopedic coverage, while top hospitals install advanced arthroscopy suites. India's booming sports community, centered on cricket and badminton, propels injury volumes similar to Western patterns. Surgeon shortages and regulatory heterogeneity remain challenges, but fellowship exchanges and harmonization efforts gradually ease barriers, enabling the rotator cuff treatment market to gain scale in populous economies.

Europe posts steady but lower growth, powered by aging demographics and high evidence thresholds that favor products with clear clinical data. Germany and the United Kingdom lead in adopting biologic implants and robotic platforms, whereas Mediterranean markets lean toward cost-efficient physiotherapy first, advancing to surgery only when conservative care fails. Brexit brought regulatory divergence, but mutual recognition agreements maintain device flow. The European Union's Medical Device Regulation tightens post-market surveillance requirements, prompting companies to invest heavily in clinical evidence generation. These factors collectively shape a balanced but evidence-driven rotator cuff treatment market across the continent.