고온 코팅 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

High Temperature Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1523350

리서치사:Mordor Intelligence

발행일:2024년 07월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

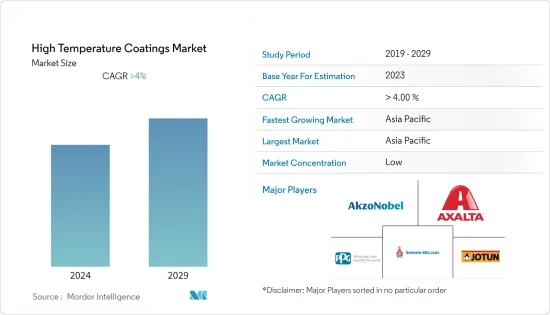

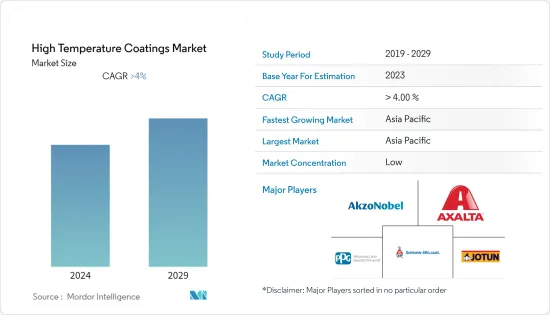

세계의 고온 코팅 시장 규모는 2024년 37억 1,000만 달러로 추정되고, 2024년부터 2029년까지 예측기간 동안 CAGR 4% 이상으로 성장할 전망이며, 2029년에는 47억 3,000만 달러에 이를 것으로 예측됩니다.

고온 코팅 시장은 COVID-19의 대유행에 의해 부정적인 영향을 받았습니다. 일부 국가에서는 전국적인 봉쇄조치가 취해졌고, 엄격한 사회적 피난조치가 건축 및 건설, 자동차, 석유화학산업에 악영향을 미쳤습니다. 그러나 COVID-19 팬데믹 후에는 건축건설활동과 자동차 제조공장이 조업을 재개하여 고온용 도료시장의 부활로 이어졌습니다.

주요 하이라이트

석유화학산업 수요 증가와 무용제 고온 코팅에 대한 선호도 변화는 현재의 연구 시장을 견인할 것으로 예상됩니다.

반면 엄격한 환경규제와 원료가격 변동이 시장 성장을 방해할 것으로 예상됩니다.

신흥 경제와 인프라 프로젝트의 성장은 예측 기간 동안 시장에 기회를 가져올 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상됩니다. 또한 중국, 인도, 일본 등 국가에서의 소비 증가로 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

고온 코팅 시장 동향

석유화학 산업 수요 증가

석유화학 산업은 침식, 부식, 화학적 공격, 마모, 기계적 손상 등의 문제에 항상 직면하고 있으며, 이는 시간이 지남에 따라 인프라 및 장비의 열화를 유발합니다.

고온 코팅은 150℃에서 800℃까지의 온도를 견딜 수 있도록 설계되었습니다. 열 손실을 최소화하고, 단열재 아래의 부식을 억제하고, 열 피로를 유지하며, 효율을 유지하는 데 도움이 됩니다.

에너지 산업과 석유 화학 산업은 가열 처리 장치, 분리기, 퍼니스 및 가열 재료의 운송을 사용하여 중요한 소비자 중 하나가 되었습니다. 고온 코팅은 에너지 손실을 줄이고 비생산 시간을 단축하는 데 도움이 됩니다.

아시아태평양에서는 석유화학 플랜트의 신설에 따라 내열 코팅 수요가 증가하고 있습니다. 예를 들어, 중국에는 305개의 석유화학 플랜트가 계획 및 발표되고 있으며, 2030년까지 총 생산 능력은 약 1억 5,240만 톤이 될 전망입니다. 또한 동기간 자본 지출은 915억 달러에 달할 것으로 예상됩니다.

마찬가지로 북미에서도 다양한 최종사용자 산업에서 석유화학제품 수요가 증가함에 따라 석유화학 산업은 현저한 성장률을 기록했습니다. 온쇼어 및 오프쇼어 탐사 및 생산 활동의 성장, 석유 정제소와 석유 화학 플랜트의 고성장, 기타 화학 플랜트(의약품 포함)의 건설과 현대화가 이 지역의 고온 코팅 수요를 밀어 올렸습니다.

또한 VCI 통계에 따르면 석유화학제품의 수출액은 증가하고 있으며 내열 코팅 시장을 견인하고 있습니다. 중국은 2022년 673억 달러 상당의 석유화학제품을 수출해 세계 주요 수출국이 됐습니다. 미국과 네덜란드가 2위와 3위에 이어 수출액은 438억 달러와 364억 달러였습니다.

위의 요인들로부터 석유화학산업의 고온 코팅 수요는 예측 기간 동안 증가할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

아시아태평양은 고온 코팅의 가장 크고 가장 빠르게 성장하는 시장입니다. 높은 경제 성장률, 제조업 성장, 저비용 노동력, 외국투자 증가, 최종 사용자 산업 수요 증가, 선진국에서 신흥국으로의 세계 생산 이동 등이 이 지역 시장 성장을 가져온 주요 요인입니다.

이 지역의 건설, 석유화학, 자동차 산업의 성장이 증가함에 따라 이 지역의 고온 코팅에 대한 수요가 더욱 높아지고 있습니다. 자동차 산업과 석유 화학 산업에서 고온 페인트는 보호 페인트로 사용됩니다.

중국은 아시아태평양에서 가장 큰 건설 시장 중 하나입니다. 중국국가통계국에 따르면 이 나라의 건설공사 생산액은 2021년 29조 3,100억 위안(4조 840억 달러)에 비해 2022년에는 31조 2,000억 위안(4조 3,400억 달러) 도달합니다. 또한 투자 부동산으로 사용되는 주택에 대한 수요도 증가하고 있습니다. 중국은 2030년까지 약 13조 달러를 건축물에 투입할 것으로 예상되고 있으며, 고온용 도료에 있어서 밝은 시장 전망을 창출하고 있습니다.

중국은 이 지역에서 가장 큰 자동차 제조업체입니다. OICA(The Organisation Internationale des Constructeurs d'Automobiles)에 따르면 중국의 자동차 생산 대수는 2022년에 2,702만대에 달하고, 동시기의 전년 대비 3% 증가했습니다.

인도는 이 지역에서 2위의 자동차 제조업체가 됐습니다. OICA에 따르면 2022년 자동차 생산 대수는 545만대에 달하고, 2021년 439만대에서 24% 증가했습니다. 이러한 이유의 자동차 생산량 증가로 자동차 코팅 수요가 증가하고 고온 코팅 시장을 견인할 것으로 예상됩니다.

인도에서도 마찬가지로 석유화학산업이 최근 현저한 성장을 이루고 있습니다. 화학제품 및 석유화학제품부에 따르면 인도의 화학제품 및 석유화학제품(CPC) 산업은 2022년 1,780억 달러를 기록했으며, 2025년에는 3,000억 달러에 이를 것으로 예상됩니다. 이와 같이 화학제품 및 석유화학제품산업의 성장은 이 나라에서 고온 코팅 수요를 촉진할 것으로 예상됩니다.

위와 같은 요인으로 인해 아시아태평양의 고온 코팅 수요는 예측 기간 동안 크게 늘어날 것으로 예상됩니다.

고온 코팅 산업 개요

고온 코팅 시장은 부분적으로 세분화됩니다. 이 시장의 주요 기업(순부동)에는 Akzo Nobel NV, Axalta Coating Systems, Jotun, PPG Industries Inc., The Sherwin-Williams Company 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

석유화학산업에서의 수요 증가

무용제 고온 코팅에의 기호의 변화

기타 촉진요인

억제요인

엄격한 환경 규제

원재료 가격 변동

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(시장 규모 : 금액)

유형별

에폭시

실리콘

폴리에스테르

아크릴

알키드

기타 유형(폴리우레탄, 비닐 에스테르 등)

기술별

수성

용제 베이스

파우더

최종 사용자 산업별

항공우주 및 방위

자동차

석유화학

건축 및 건설

기타 최종 사용자 산업(해양, 수처리 등)

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

노르딕

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

나이지리아

카타르

이집트

UAE

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%) 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Akzo Nobel NV

Aremco

Axalta Coating Systems

Carboline

Chemcote PTY LTD

GENERAL MAGNAPLATE CORPORATION

Hempel A/S

Jotun

PPG Industries Inc.

The Sherwin-Williams Company

Valspar

제7장 시장 기회 및 향후 동향

신흥 경제국의 성장 및 인프라 프로젝트

기타 기회

AJY

영문 목차

영문목차

The High Temperature Coatings Market size is estimated at USD 3.71 billion in 2024, and is expected to reach USD 4.73 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The high temperature coatings market had negatively affected by the COVID-19 pandemic. Due to nationwide lockdowns in several countries, strict social distancing measures negatively affected the building and construction, automotive, and petrochemical industries. However, post-COVID pandemic, the building construction activities and automotive manufacturing plants resumed their operations, which helped to revive the market for high-temperature coatings.

Key Highlights

The growing demand from petrochemical industries and the shift in preference towards solvent-free high-temperature coatings is expected to drive the current studied market.

On the flip side, the stringent environmental regulations and the volatility in raw material prices are expected to hinder the growth of the market.

The growth of emerging economies and infrastructure projects is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

High Temperature Coatings Market Trends

Growing Demand from Petrochemical Industry

The petrochemical industry is constantly faced with problems like erosion, corrosion, chemical attack, wear, abrasion, and mechanical damage, which cause deterioration of infrastructure and equipment over time.

High-temperature coatings are designed to withstand temperatures from 150°C to 800°C. It helps minimize heat losses, keep corrosion under insulation in check, maintain thermal fatigue, and maintain efficiency.

Energy and Petrochemical industries are among the critical consumers owing to the use of heater-treaters, separators, furnaces, and the transport of heated materials. High-temperature coatings help decrease energy losses and reduce non-productive time.

In the Asia-Pacific region, the demand for heat-resistant coatings is increasing with the development of new petrochemical plants. For instance, China has 305 planned and announced petrochemical plants, with a total capacity of about 152.4 mtpa by 2030. China is also expected to reach a capital expenditure of USD 91.5 billion over the same period.

Similarly, in North America, the petrochemical industry registered a significant growth rate due to rising demand for petrochemicals from various end-user industries. The growth in onshore/offshore exploration and production activities, high growth observed in oil refineries and petrochemical plants, and the building and modernization of other chemical plants (which include pharmaceuticals) boosted the demand for high-temperature coatings in the region.

Furthurmore according to VCI statistics the export value of petrochemicals is rising therbey driving the market for heat resistant coatings. China exported over USD 67.3 billion worth of petrochemicals in 2022, becoming the world's major exporting country. The United States and the Netherlands followed second and third, with an export value of USD 43.8 billion and USD 36.4 billion.

Owing to the above-mentioned factors, the demand for high-temperature coatings from the petrochemical industry is expected to increase over the forecast period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region represents the largest and fastest-growing market for high-temperature coatings. High economic growth rate, growing manufacturing industries, low-cost labor, increasing foreign investments, increasing demand from end-user industries, and the global shift in production from developed countries to emerging countries in the region are some of the major factors leading to the growth of the market in the region.

The escalating growth of the construction, petrochemical, and automotive industries in the region is further driving the demand for high-temperature coatings in the region. In the automotive and petrochemical industries the high temperature coatings are used as protective coatings.

China is one of the largest construction markets in the Asia-Pacific region. According to the National Bureau of Statistics of China, the output value of construction works in the country accounted for CNY 31.2 trillion (USD 4.34 trillion) in 2022, as compared to CNY 29.31 trillion (USD 4.084 trillion) in 2021. Additionally, demand is increased for residences that are used as investment properties. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for high temperature coatings.

China is the largest automotive vehicle manufacturer in the region. According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

India has become the second-largest automotive vehicle manufacturer in the region. According to OICA, the total production volume of automotive vehicles reached 5.45 million units in 2022, indicating a growth of 24% as compared to 4.39 million units registered in 2021. Thus, the increase in the production of automotive vehicles is expected to drive the demand for automotive coatings, thereby driving the market for high temperature coatings.

Similarly in India the petrochemical industry registered a significant growth in recent years. According to the Department of Chemicals & Petrochemicals, India's chemical and petrochemical (CPC) industry registered USD 178 billion in 2022, and it is expected to reach USD 300 billion by 2025. Thus the growth in chemical and petrochemical industries is expected to drive the demand for high temperature coatings in the country.

Owing to the above mentioned factors, the demand for high-temperature coatings in Asia-Pacific region is expected to grow considerably over the forecast period.

High Temperature Coatings Industry Overview

The high-temperature coatings market is partially fragmented in nature. Some of the major players in the market (not in any particular order) include Akzo Nobel N.V., Axalta Coating Systems, Jotun, PPG Industries Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from Petrochemical Industry

4.1.2 Shift in Preference Toward Solvent-Free High Temperature Coatings

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Environmental Regulations

4.2.2 Volatility in Raw Material Prices

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Epoxy

5.1.2 Silicone

5.1.3 Polyester

5.1.4 Acrylic

5.1.5 Alkyd

5.1.6 Other Types (Polyurethane, Vinyl Ester, etc.)

5.2 Technology

5.2.1 Water based

5.2.2 Solvent based

5.2.3 Powder

5.3 End-user Industry

5.3.1 Aerospace and Defense

5.3.2 Automotive

5.3.3 Petrochemical

5.3.4 Building and Construction

5.3.5 Other End-user Industries (Marine, Water Treatment, etc.)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Spain

5.4.3.6 NORDIC

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Nigeria

5.4.5.2 Qatar

5.4.5.3 Egypt

5.4.5.4 UAE

5.4.5.5 Saudi Arabia

5.4.5.6 South Africa

5.4.5.7 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Akzo Nobel N.V.

6.4.2 Aremco

6.4.3 Axalta Coating Systems

6.4.4 Carboline

6.4.5 Chemcote PTY LTD

6.4.6 GENERAL MAGNAPLATE CORPORATION

6.4.7 Hempel A/S

6.4.8 Jotun

6.4.9 PPG Industries Inc.

6.4.10 The Sherwin-Williams Company

6.4.11 Valspar

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 The Growth of Emerging Economies and Infrastructure Projects